TODAY’S GAME PLAN: from the trading

desk, this is not research

DATA/HEADLINES: 8:30ET Chicago Fed Nat Activity Index, GDP, Personal Consumption, Core PCE Price Index QoQ, Advance

Goods Trade Balance, Retail Inventories MoM, Wholesale Inventories MoM, Durable Goods Orders, Cap Goods, Initial Jobless Claims; 10:00ET New Home Sales MoM; 11:00ET Kansas City Fed Manf. Activity; 1:00ET 7 Year Auction

I am out the rest of the week, have a great weekend

TODAY’S HIGHLIGHTS and News:

-

US Supreme Court allows Alabama to carry out first-ever execution by nitrogen gas, scheduled today

-

US and Iraq are expected to soon begin talks on the future of the US military presence in the country

-

COVID variant JN.1 is not more severe, early CDC data suggest

-

Boeing’s planned production increases for the 737 Max were halted by the FAA

-

Donald Trump said anybody contributing to Nikki Haley’s campaign “from this moment” will be permanently barred from the MAGA camp

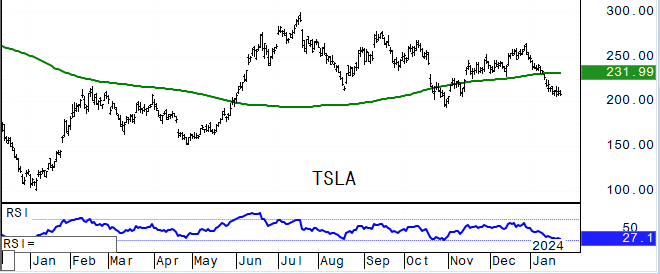

Global stocks paused as disappointing results from Tesla took the edge off the recent rally, and investors prepared for an ECB meeting and economic growth data from

the US. A surge in Chinese markets on the back of revived investor confidence helped offset a more muted performance elsewhere. Investors expect no change in monetary policy from the ECB and are looking for guidance from central bank President Christine Lagarde

for what to expect in terms of potential rate cuts this year. The headline German Ifo business confidence index fell to 85.2 in January, to its lowest level since May 2020. Turkey’s central bank hiked its key interest rate by another 250 basis points to 45%

as inflation increased to 64.8%.

EQUITIES:

US equity futures fluctuated as investors await the fourth-quarter gross domestic product report and examined the latest earnings reports. The GDP figure is expected to show that the

US economy expanded at a 2% seasonally adjusted annualized pace, down from 4.9% in the previous quarter. A slew of other figures are also due, including inventories, new home sales and weekly unemployment claims.

Futures ahead of the bell: E-Mini S&P +0.05%, Nasdaq +0.2%, Russell 2000 +0.3%, Dow -0.05%.

In pre-market trading, Tesla dropped more than 8% after the electric vehicle maker missed earnings estimates and flagged slower growth this year. In a rare move, the company chose not

to offer a full-year target. International Business Machines (IBM) gained 7% after delivering a positive revenue outlook. Boeing (BA) dropped more than 3% after the US Federal Aviation Administration halted planned increases in production of the 737 Max.

American Airlines (AAL) gains 4% after forecasting full year profit that’s above analyst expectations. Comcast Corp. (CMCSA) gains 2% after posting better-than-expected earnings and sales. Humana (HUM) plunges 13% after the company withdrew its 2025 earnings

target and forecast 2024 profit far lower than estimates. Paramount Global (PARA) advances 3% after Bloomberg reported that Skydance Media’s David Ellison made an offer to buy National Amusements. Sherwin-Williams (SHW) falls 5% after providing a 2024 profit

forecast that disappointed. Virtu Financial (VIRT) slumps 5% after the financial services firm reported adjusted Ebitda for the fourth quarter that missed.

European gauges are lower on a busy day for earnings and as investors prepare for the latest monetary policy decision from the European Central Bank today. German business morale unexpectedly

worsened in January, declining for a second straight month. The start of the new year has brought mass farmer protests and nationwide rail strikes, as discontent grows over economic policies. Surging freight rates provide another reason for the ECB to temper

hopes for early rate cuts. The Stoxx Europe 600 slipped as Autos, REITs and Banks weigh. Among individual movers, European chipmaker STMicroelectronics NV dropped after reporting softer customer orders and giving weaker sales guidance. Nokia Oyj climbed after

a better-than-expected fourth quarter. Publicis Groupe SA rose as revenue beat expectations. Stoxx 600 -0.3%, DAX -0.5%, CAC -0.5%, FTSE 100 -0.2%. Autos -1.3%, REITs -1.3%, Banks -1%. Media +0.4%, Technology +0.2%.

Asian stocks were mixed, with the MSCI Asia Pacific Index trading in a narrow range. Chinese blue-chips staged a robust rally, with the Shanghai Composite up 3% in its largest daily gain

in nearly two years, after a series of measures by Beijing authorities to prop up the economy and the stock market. China and Hong Kong stocks led gains in the region with the CSI property index jumping 5.2%. EV makers fell after Tesla warned of bleak volume

growth. South Korea’s GDP grew 2.2% year on year in the fourth quarter, beating expectations. CSI 300 +2%, Hang Seng Index +2%, Taiwan +0.7%, ASX 200 +0.5%, Topix +0.1%, Kospi +0.03%. Vietnam -0.2%, Sensex -0.5%, Indonesia -0.7%.

FIXED INCOME:

Treasuries are slightly richer across the curve, outperforming core European rates and partially unwinding a late slide Wednesday spurred by soft 5-year note auction.

Bunds lag ahead of the European Central Bank meeting. Japan saw weak demand for its 40-year bond as several life insurers stayed away from the bidding process. The US 30-year yield eased about 2 basis points, having climbed Wednesday to its highest level

this year after a poor debt auction and on anticipation of a heavy government borrowing schedule. The Fed raised the cost of its Bank Term Funding Program, effectively shutting down what The Economist called “a free-money machine for banks.” US session includes

first estimate of 4Q GDP and weekly jobless claims data. Treasury auction cycle concludes with $41b 7-year note sale after Wednesday’s sloppy 5-year note sale tailed by 2bp. 10-year yields around 4.17%; 2-year yield around 4.39%.

METALS:

Gold steadied as traders await several US reports that should provide more clarity on the nation’s economic health, following signs earlier this week that business

activity is stronger than expected. Spot gold +0.1%, silver +0.8%.

ENERGY:

Oil prices rose after data showed US crude stockpiles fell more than expected last week, while China’s stimulus measures reinforced optimism over energy consumption

there. The draw was driven by a stark drop in US crude imports as winter weather shut in refineries. Meanwhile, geopolitical tensions in the Middle East remained in focus. A fire damaged Rosneft PJSC’s major Tuapse refinery early on Thursday, the latest in

a string of incidents at the nation’s downstream and energy-export facilities blamed on drone attacks by Ukraine. WTI +1%, Brent +0.9%, US Nat Gas +2.6%, RBOB +1%.

CURRENCIES:

Currencies traded in muted ranges. The dollar is under modest pressure, as traders took profit on its recent rise, with less than a week to go for the Fed’s next

meeting. The euro rebounded from earlier losses as traders awaited the European Central Bank’s interest-rate decision. Elsewhere, the Norwegian krone rallied after the Norges Bank policy decision, keeping borrowing costs at a 16-year high. US$ Index is flat,

GBPUSD is flat, USDJPY +0.1%, EURUSD +0.05%, AUDUSD +0.1%,NZDUSD +0.1%, USDCHF +0.3%, USDNOK -0.05%.

Bitcoin +0.5%, Ethereum -0.1%. Bruised by stock market, Chinese rush into banned bitcoin. More and more Chinese investors are using creative ways to own bitcoin and

other crypto assets that they believe are safer than investing in crumbling stock and property markets at home.

TECHNICAL LEVELS:

|

ESH24 |

10 Year Yield |

Feb Gold |

March WTI |

Spot $ Index |

|

|

Resistance |

5000.00 |

5.000% |

2152.3 |

81.37 |

109.120 |

|

|

4981.00 |

4.755% |

2117.0 |

80.50 |

107.350 |

|

|

4950.00 |

4.550% |

2100.0 |

78.15 |

106.000 |

|

|

4933/34 |

4.255% |

2062.3 |

77.66 |

104.780 |

|

|

4909.00 |

4.135% |

2027.5 |

75.52 |

103.480 |

|

Settlement |

4898.00 |

2016.0 |

75.09 |

||

|

|

4865.00 |

4.070% |

2012.3 |

73.65 |

102.955 |

|

|

4845.00 |

3.780% |

1978.3 |

70.13 |

102.530 |

|

|

4817.00 |

3.640% |

1960.8 |

69.28 |

101.780 |

|

|

4790.00 |

3.245% |

1949.1 |

67.98 |

101.280 |

|

Support |

4746/50 |

3.000% |

1938.8 |

66.63 |

100.000 |

Colors within the report:

Green is always the 200 period (day, week).

Red is always 21,

Blue = 50,

Brown =

100 *Stars have added importance

- Upgrades

- AlTi Global (ALTI) Raised to Strong Buy at Raymond James; PT $9

- ASML (ASML NA) ADRs Raised to Buy at Fubon; PT $980

- Avis Budget (CAR) Raised to Buy at Deutsche Bank; PT $248

- Covenant Logistics Group (CVLG) Raised to Outperform at Cowen; PT $66

- Enerflex (EFX CN) Raised to Outperform at National Bank; PT C$10

- First Community/SC (FCCO) Raised to Outperform at Raymond James

- Netflix (NFLX) Raised to Buy at DZ Bank; PT $600

- Outlook Therapeutics Inc (OTLK) Raised to Buy at Guggenheim; PT $2

- Raised to Buy at Brookline Capital

- Radcom (RDCM) Raised to Buy at Needham; PT $14

- Stock Yards Bancorp (SYBT) Raised to Overweight at Stephens; PT $62

- Tal Education (TAL) ADRs Raised to Overweight at JPMorgan; PT $15

- Vericel (VCEL) Raised to Buy at Truist Secs; PT $51

- Downgrades

- B2Gold (BTO CN) Cut to Neutral at CIBC; PT C$4.85

- Boeing (BA) Cut to Neutral at BofA; PT $225

- Columbia Banking (COLB) Cut to Outperform at Raymond James

- Hanmi Financial (HAFC) Cut to Neutral at Janney Montgomery; PT $19

- Hertz (HTZ) Cut to Hold at Deutsche Bank; PT $9

- Cut to Neutral at JPMorgan; PT $11

- OrthoPediatrics (KIDS) Cut to Hold at Truist Secs; PT $31

- TE Connectivity (TEL) Cut to Hold at CFRA; PT $155

- Tesla (TSLA) Cut to Neutral at KGI Securities; PT $213

- Venus Concept Inc (VERO) Cut to Neutral at Ladenburg Thalmann

- VF Corp (VFC) Cut to Sell at Williams Trading; PT $13

- Initiations

- Axsome Therapeutics (AXSM) Rated New Outperform at RBC; PT $126

- Bio-Rad (BIO) Rated New Buy at Baptista Research; PT $435.60

- Bloom Energy (BE) Rated New Buy at BTIG; PT $21

- CACI (CACI) Rated New Hold at Baptista Research; PT $368.80

- Computer Modelling Group (CMG CN) Rated New Outperform at National Bank

- DDC Enterprise (DDC) Rated New Buy at Benchmark; PT $8

- Dream Impact Trust (MPCT-U CN) Rated New Hold at Desjardins; PT C$7.75

- Gentex (GNTX) Rated New Hold at Baptista Research; PT $36.60

- Hasbro (HAS) Rated New Outperform at Baptista Research; PT $57.40

- IPG Photonics (IPGP) Rated New Buy at Seaport Global Securities

- New Oriental Education (EDU) ADRs Reinstated Buy at BOCOM Intl; PT $96

- Norwegian Cruise (NCLH) Rated New Hold at Baptista Research; PT $18.80

- PVH (PVH) Rated New Underperform at Baptista Research; PT $118.30

- Vera Therapeutics (VERA) Rated New Outperform at Oppenheimer; PT $26

- Vestis (VSTS) Rated New Neutral at Goldman; PT $22

- Whirlpool (WHR) Rated New Hold at Baptista Research; PT $127.20

- Wyndham Hotels (WH) Rated New Hold at Baptista Research; PT $88.10

Data sources: Bloomberg, Reuters, CQG

Comments are closed