TODAY’S GAME PLAN: from the trading

desk, this is not research

DATA/HEADLINES: 10:00ET Yellen testifies at House committee; 12:00ET Fed’s Mester speaks; 1:00ET 3-Year Note Auction,

Fed’s Kashkari speaks; 2:00ET Fed’s Collins speaks

TODAY’S HIGHLIGHTS and News:

-

Citi Says US Tech Stocks Face Risk Of Big Selloff On Positioning

-

ICE & HSI arrested several of the illegal immigrants believed to be involved in the mob beating of two NYPD officers

-

Country singer Toby Keith dead at 62 after battle with cancer

-

SEC set to adopt Treasury market dealer rule as part of market overhaul

-

Boeing workers are demanding a 40% pay rise over three or four years

Global shares rose, boosted by a sharp rise in Chinese stocks as Beijing ramped up efforts to help its slumping market. According to Bloomberg News, President Xi

Jinping is set to address the challenges facing the stock market in discussions with financial regulators. Additionally, regulators unveiled additional restrictions on short selling, and state investors said they were expanding their stock buying plans. German

industrial orders unexpectedly jumped 8.9% in December; its highest month-on-month increase in more than three years. Meanwhile, the United States continued its campaign against Iran-backed Houthis in Yemen, whose attacks on shipping vessels have disrupted

global oil trading routes.

EQUITIES:

US equity futures fluctuated amid dimming hopes for interest rate cuts, as investors looked ahead to the next batch of quarterly results. A raft of Federal Reserve officials are due to

speak this week, which may add additional insight into the central bank’s thinking. Strong US economic data has forced traders to reduce their bets on interest rate cuts. Deutsche Bank scrapped its call for a US recession, saying that there’s less of a downside

risk to growth as financial conditions ease. Citigroup strategists warned that positioning in US technology stocks is now so bullish that any selloff could trigger a wider rout.

Futures ahead of the bell: E-Mini S&P +0.05%, Nasdaq +0.1%, Russell 2000 -0.2%, DJI -0.05%

In pre-market trading, US-listed shares of Chinese e-commerce firms Alibaba (BABA), JD.com (JD) and PDD Holdings (PDD), rose between 4% and 5.6%, while iShares China Large-Cap ETF (FXI)

climbed nearly 4%. Palantir surged as much as 20% premarket after reporting its first annual profit, driven by AI demand. Chegg (CHGG) falls 7% after the online educational services company provided a disappointing forecast. Coherent (COHR) jumps 11% after

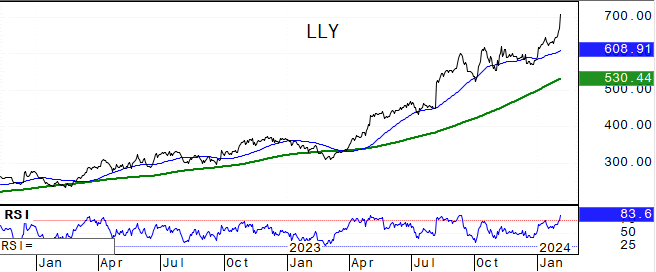

the company posted 2Q results that beat, with analyst positive on demand for the company’s AI-related datacom transceivers. Eli Lilly (LLY) gains 3% after forecasting 2024 sales ahead of estimates as the company rolls out Zepbound, its weight-loss shot. FMC

(FMC) falls 14% after the pesticide maker posted quarterly results and an earnings outlook that trailed analyst estimates. NXP Semi (NXPI) gains 3% as the chipmaker reported better-than-expected fourth quarter revenue and adjusted EPS. Rambus (RMBS) drops

10% after the semiconductor maker’s first-quarter revenue forecast fell short of estimates. Spotify (SPOT) climbs 7% after the music-streaming company gave a first-quarter forecast that was stronger than expected. Symbotic (SYM) slumps 17% after the robotics

warehouse automation company’s forecast for second-quarter missed estimates. Varonis Systems (VRNS) rises 7% after the data security firm’s 4Q results and outlook beat expectations.

European gauges are holding gains after slipping from early highs amid a rush of earnings as investors assessed China’s market-rescue efforts. The FTSE 100 is outperforming, boosted by

strong results from BP (+5.7%). The oil major also announced plans to repurchase $3.5 billion of shares in first half. That offset declines for UBS Group AG after its earnings disappointed. Infineon Technologies fell over 3% after it lowered its revenue forecast

as the German chipmaker is hit by a broader slump in semiconductor demand. Novartis AG agreed to buy MorphoSys AG (+14%) for €2.7 billion to add cancer treatments to its pipeline. Stoxx 600 +0.2%, DAX +0.1%, CAC +0.4%, FTSE 100 +0.6%. Energy sector leads gains,

+1.9%. Banks +0.9%, Retail +0.7%, Insurance +0.5%. Utilities -1.1%, Financial Services -1%, Telecom -0.8%.

Asian stocks were mixed with Chinese shares advancing due to increased market rescue measures, while several other markets declined amid diminished expectations for a rapid Federal Reserve

shift towards monetary easing. The MSCI Asia Pacific Index was little changed. Beaten down Chinese stocks saw their best single-day gain in two years on a slew of signals that authorities are strengthening their resolve to support slumping markets. President

Xi is set to receive a briefing from the CSRC on financial markets as soon as today, underscoring urgency in top leadership to prop up markets. Central Huijin Investment, a key unit of the nation’s sovereign wealth fund, vowed to expand purchasing exchange-traded

funds. Equities in Japan, Australia and South Korea fell as investors evaluated strong US service-industry data and cautious comments from some Fed officials. Australia’s central bank held interest rates steady at a 12-year high of 4.35% but cautioned that

a further increase could not be ruled out given inflation was still too high. Taiwan and New Zealand’s markets were closed for holidays. Hang Seng Tech Index +6.7%, Hang Seng Index +4%, CSI 300 +3.5%, Thailand +0.9%, Sensex +0.6%, Vietnam +0.2%. ASX 200 -0.6%,

Kospi -0.6%, Singapore -0.3%, Topix -0.7%.

FIXED INCOME:

Treasuries curve edges steeper with yields narrowly mixed and front-end outperforming slightly on the day. 10-year, little changed at 4.16% in a narrow daily range

after climbing 28bp over past two sessions. US session features several Fed speakers and start of Treasury auction cycle with 3-year note sale, followed by $42b 10-year and $25b 30-year new issues Wednesday and Thursday. The US securities regulator is set

to adopt a rule requiring proprietary traders and other firms that routinely deal in US government bonds to register as broker-dealers, subjecting them to stricter oversight. The rule is part of a broader effort to fix structural issues regulators say are

causing liquidity problems in the $26 trillion Treasury market.

METALS:

Gold steadied above a one-week low, with optimism for imminent US interest-rate cuts fading as strong economic data suggested the Federal Reserve’s inflation fight

isn’t done yet. Spot gold +0.05%, silver -0.2%.

ENERGY:

Oil prices edged higher as traders took stock of a visit to the Middle East by US Secretary of State Antony Blinken to discuss a ceasefire offer in the region. Palestinians

hope the visit will secure a ceasefire prior to a threatened Israeli assault on Rafah, a border city where approximately half of the Gaza Strip’s population seeks refuge. The ceasefire offer, delivered to Hamas last week by Qatari and Egyptian mediators,

still awaits a reply from the militants. Russia’s seaborne crude shipments rebounded strongly from two weeks of disruptions, with record-equaling flows from the country’s main export terminals. WTI +0.5%, Brent +0.8%, US Nat Gas -0.2%, RBOB +0.7%.

CURRENCIES:

In currency markets, the dollar hovered near a three-month high after data on Monday showed the US services sector growth picked up in January, adding to growing

doubts about the slew of Fed rate cuts priced in for this year. A relatively hawkish tone of the RBA’s policy statement briefly boosted the Australian dollar. The Swiss franc fell to its weakest against the greenback in nearly two months, pressured by its

low yield. US$ Index +0.1%. GBPUSD +0.1%, USDJPY +0.05%, EURUSD -0.15%, AUDUSD +0.1%, NZDUSD -0.1%, USDCHF +0.3%.

Bitcoin +1%, Ethereum +1.7%.

TECHNICAL LEVELS:

|

ESH24 |

10 Year Yield |

April Gold |

March WTI |

Spot $ Index |

|

|

Resistance |

5063.00 |

|

2152.3 |

84.60 |

110.000 |

|

|

5041.00 |

5.000% |

2117.0 |

81.37 |

109.120 |

|

|

5020.00 |

4.700% |

2100.0 |

78.15 |

107.350 |

|

|

5000.00 |

4.550% |

2083.2 |

75.47 |

106.000 |

|

|

4975.00 |

4.255% |

2043.1 |

73.39 |

104.780 |

|

Settlement |

4962.00 |

2042.9 |

72.78 |

||

|

|

4926.00 |

4.090% |

2027.7 |

70.19 |

103.565 |

|

|

4908/16 |

3.780% |

1979.5 |

68.28 |

102.895 |

|

|

4895.00 |

3.640% |

1960.8 |

67.71 |

102.330 |

|

|

4866.00 |

3.245% |

1942.7 |

66.80 |

101.780 |

|

Support |

4815.00 |

3.000% |

|

63.64 |

101.350 |

Colors within the report:

Green is always the 200 period (day, week).

Red is always 21,

Blue = 50,

Brown =

100 *Stars have added importance

- Upgrades

- Everbridge (EVBG) Raised to Equal-Weight at Wells Fargo; PT $28

- Li Auto (LI) ADRs Raised to Buy at Deutsche Bank; PT $41

- Open Lending (LPRO) Raised to Equal-Weight at Morgan Stanley; PT $7

- Palantir (PLTR) Raised to Neutral at Citi; PT $20

- Raised to Hold at Jefferies; PT $22

- UPS (UPS) Raised to Buy at UBS; PT $175

- Varonis Systems (VRNS) Raised to Outperform at Wedbush; PT $65

- Downgrades

- Air Products (APD) Cut to Neutral at Seaport Global Securities

- Cut to Equal-Weight at Wells Fargo; PT $240

- Catalent (CTLT) Cut to Sector Perform at RBC; PT $63.50

- Cut to Equal-Weight at Stephens; PT $63.50

- Chegg (CHGG) Cut to Underweight at Piper Sandler; PT $8.50

- Chevron (CVX) Cut to Hold at DZ Bank; PT $160

- Embraer (EMBR3 BZ) ADRs Cut to Hold at HSBC; PT $19

- Euronav (EURN BB) Cut to Hold at Deutsche Bank

- Illinois Tool (ITW) Cut to Underweight at Wells Fargo; PT $240

- Infosys (INFO IN) ADRs Cut to Hold at HSBC; PT $21.10

- McDonald’s (MCD) Cut to Neutral at BTIG

- Cut to Hold at CFRA; PT $310

- Napco Security Technologies (NSSC) Cut to Inline at Imperial; PT $45

- ON Semi (ON) Cut to Neutral at Fubon; PT $85

- Plug Power (PLUG) Cut to Neutral at Seaport Global Securities

- Saia (SAIA) Cut to Hold at Stifel; PT $526

- Tesla (TSLA) Cut to Neutral at Daiwa; PT $195

- Valeo Pharma (VPH CN) Cut to Speculative Buy at Paradigm Capital

- Initiations

- Biomea Fusion (BMEA) Rated New Buy at Truist Secs; PT $55

- Bloom Energy (BE) Rated New Neutral at Redburn; PT $12.50

- Flywire (FLYW) Rated New Buy at Deutsche Bank; PT $27

- LeddarTech (LDTC) Rated New Buy at Roth MKM; PT $7

- Paycom Software (PAYC) Rated New Neutral at BTIG

- Paycor HCM (PYCR) Rated New Buy at BTIG; PT $26

- Paylocity (PCTY) Rated New Buy at BTIG; PT $200

- Plug Power (PLUG) Rated New Neutral at Redburn; PT $4.50

- TKO (TKO) Rated New Buy at Northcoast; PT $105

- UFP Technologies (UFPT) Rated New Sector Weight at KeyBanc

- Well Health Technologies (WELL CN) Rated New Outperform at RBC; PT C$5.50

Data sources: Bloomberg, Reuters, CQG

Comments are closed