TODAY’S GAME PLAN: from the trading

desk, this is not research

DATA/HEADLINES: 11:00ET NY Fed 1-Yr Inflation Expectations; 12:30ET Fed’s Bostic speaks; 3:00ET Consumer Credit

On Friday, the BLS reported that in December the number of full-time jobs plunged by 1.531 million to 133.2 million, the biggest monthly drop since the record covid crash of 14.7 million

jobs. The number of part-timers soared by a whopping 762,000. Multiple jobholders surged by 222K, and at 8.565 million was the highest print on record.

TODAY’S HIGHLIGHTS and News:

-

Israeli strike on South Lebanon kills senior commander in Hezbollah’s elite Radwan force

-

China to sanction five US defense manufacturers over US arms sales to Taiwan

-

China detained the head of an overseas consulting firm for allegedly spying for the UK

-

The Falcons fired coach Arthur Smith just hours after a third straight losing season

Global shares dipped while bonds steadied as investors recalibrated their bets in the wake of last week’s selloff. Markets are looking for direction after mixed US

economic data on Friday capped a week that saw global equities sink the most since October on speculation the Federal Reserve was in no rush to reduce interest rates. The US inflation print due Thursday as well as the start of earnings season at the end of

the week may offer investors further catalysts. Secretary of State Antony Blinken held more talks with Arab leaders today as part of a diplomatic push to stop the war in Gaza from spreading further. The US warned the Israel-Hamas war could “easily” turn into

a full-blown Middle East conflict.

EQUITIES:

US equity futures are mixed after Wall Street started the year with a weekly loss and investors began turning their attention to the kickoff of earnings season and a busy day in deal

news. Traders will be watching the release of US inflation figures on Thursday for a sense of the central bank’s next monetary policy decision. The November-December rally has stretched positioning and led to complacent sentiment, JPMorgan said. Morgan Stanley’s

Michael Wilson sees equities stalling until economic growth picks up, and recommended investors focus on single stocks. Goldman is optimistic on US corporate earnings. Congressional leaders announced a bipartisan deal on top-line spending levels for the current

fiscal year, lessening the chances of a partial shutdown on January 20.

Futures ahead of the bell: E-Mini S&P +0.05%, Nasdaq +0.15%, Russell 2000 -0.1%, Dow -0.3%.

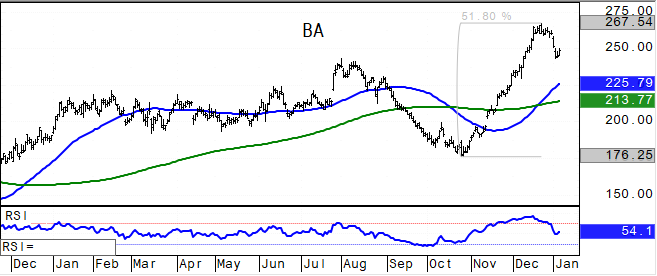

In pre-market trading, Boeing (BA) fell as much as 9.8% as carriers pull the 737 Max 9 model after a door-shaped panel on a brand-new Alaska Airlines jet blew out. The FAA grounded 171

planes. Alaska Air fell 6%, and United was down 2.7% after saying they were grounding their MAX 9 jets. Spirit AeroSystems Holdings, which installed the panel, slumped 21%. Harpoon Therapeutics (HARP) shares jumped over 100% on news that Merck is discussing

paying roughly $23 a share for the cancer drugmaker. An agreement may be announced within days. Synopsys is in advanced talks to acquire engineering software provider Ansys (ANSS +1.5%) for around $35 billion in a stock-and-cash deal. Johnson & Johnson announced

today it has entered into a definitive agreement to acquire Ambrx Biopharma (AMAM +28%) in an all-cash deal with equity value of $2B. Axonics (AXNX) gains 21% after Boston Scientific entered into a definitive agreement to acquire the medical technology company.

Southwestern Energy and Chesapeake Energy are close to announcing a merger, the Wall Street Journal reported. Crocs (CROX) rises 7.6% after the footwear company boosted revenue forecasts. DoorDash (DASH) gains 3.6% after Jefferies upgraded the online food-delivery

company to buy. Genesco (GCO) tumbles 16% after the footwear and accessories retailer cut its forecast. Moderna (MRNA) rises 1% after product sales for 2023 modestly beat analyst estimates.

European gauges pared an early retreat to trade mixed. Energy stocks lead declines as oil dropped after Saudi Arabia cut official selling prices. Shell Plc also declined as the company

said it expects 4Q profits from buying and selling oil products and chemicals to be lower. Boeing suppliers fell as the company’s 737 Max 9 model was grounded for inspections. Airbus SE shares rose. ASML Holding NV was among the strongest gainer in the index

after it was upgraded at Kepler Cheuvreux. On the data front, German factory orders rose much less than anticipated in November at 0.3 versus 1.1 expected, a discouraging sign for Europe’s largest economy. Swiss inflation accelerated to 1.7% in December.

Stoxx 600 -0.03%, DAX +0.2%, CAC +0.05%, FTSE 100 -0.1%. Energy -1.7%, Basic Resources -0.9%, REITs -0.8%. Industrials +0.3%, Technology +0.3%, Autos +0.2%.

Asia stocks fell, weighed by Chinese and Hong Kong shares as concerns over the country’s regulatory developments in the technology space and the broader economy’s growth persisted. The

MSCI Asia Pacific excluding Japan Index slid 1%, with tech stocks weighing most. Concerns over China’s economy remain as the latest factory activity and home sales data showed few signs of improvement. Most Chinese healthcare stocks declined after President

Xi Jinping’s remarks on the economy ignited a new wave of trade tensions. The Hang Seng China Enterprises Index had its lowest close since November 2022. South Korea’s regulator is launching a wider probe into local banks and brokers which sold exotic notes

linked to Chinese stocks. Markets in Japan were closed for a holiday. Hang Seng Tech -3%, Hang Seng Index -1.9%, CSI 300 -1.3%, Sensex -0.9%, ASX 200 -0.5%, Kospi -0.4%. Vietnam +0.5%, Taiwan +0.3%.

FIXED INCOME:

Treasuries are little changed across the curve, outperforming core European rates. It’s a busy week for sovereign debt supply including Treasury auctions and EU

5- and 10-year offerings. Data highlights this week include US CPI and PPI. US 10-year yield is around 4.06%, near the high of the daily range, with curve spreads slightly steeper. Treasury auctions resume Tuesday with $52b 3-year notes, followed by $37b

10- and $21b 30-year sales Wednesday and Thursday.

METALS:

Gold resumed its slide after whipsawing moves at the end of last week, with a recent rebound in the dollar and US bond yields posing a threat to the precious metal’s

appeal. Gold initially dropped and US government bond yields jumped on Friday after an unexpected acceleration in job growth fueled speculation the Fed will be in no rush to reduce rates. Both quickly reversed course after services data showed the sector came

close to stagnating at the end of the year. Investors await a US inflation print due Thursday. Spot gold -1%, silver -1.3%

ENERGY:

Oil prices fell sharply due to significant price reductions from Saudi Arabia and an increase in OPEC output, countering concerns about growing geopolitical tensions

in the Middle East. On Sunday rising supply and competition with rival producers prompted Saudi Arabia to cut official selling prices for all regions. The reductions underscored a worsening global outlook amid strong global supply, including from the US,

and outweighed concern over Red Sea tensions and supply disruptions in Libya. Libya declared force majeure at the Sharara field following its closure. European natural gas futures slumped as the severe cold snap gripping the continent appeared to hardly dent

supplies. WTI -2.7%, Brent -2.5%, US Nat Gas -3.1%, RBOB -2.6%.

CURRENCIES:

In currency markets, the dollar inched higher and had mixed performance against G-10 peers. The Norwegian krone leads G-10 losses as oil prices decline. USD/JPY recovered

from a 0.4% drop, with Tokyo CPI watched for its impact on Bank of Japan rate hike expectations. EUR/USD slipped after German factory orders disappointed but has since recovered. US$ Index +0.1%, GBPUSD -0.1%, EURUSD +0.05%, USDJPY -0.05%, AUDUSD -0.4%, USDNOK

+1%, NZDUSD -0.5%.

Bitcoin +1.6%, Ethereum +1%. There is much speculation around the founder(s) — Satoshi Nakamoto – who created Bitcoin on June 3, 2009. The mystery person or group

(or government agency) has been MIA since 2011. Yet 1 million bitcoins remain in their original account, untouched. His wallet is estimated to be up to $73 billion, and if this is indeed an individual, he or she is one of the top 15 richest people in the world.

They have never moved a fraction of a BTC from their account.

Only 2.3% of bitcoin owners own a full bitcoin, while 74% own less than 0.01 BTC. Armstrong Economics.

TECHNICAL LEVELS:

|

ESH24 |

10 Year Yield |

Feb Gold |

Feb WTI |

Spot $ Index |

|

|

Resistance |

4841.50 |

5.250% |

2180.0 |

86.00 |

107.350 |

|

|

4811.50 |

5.000% |

2152.3 |

84.60 |

106.000 |

|

|

4788.00* |

4.550% |

2117.0 |

81.37 |

104.780 |

|

|

4772.00 |

4.280% |

2100.0 |

77.80 |

103.650 |

|

|

4755.00 |

4.035% |

2072.5 |

75.29 |

103.420 |

|

Settlement |

4734.75 |

2049.8 |

73.81 |

||

|

|

4700.00 |

3.780% |

2021.0 |

71.17 |

101.600 |

|

|

4666/70* |

3.640% |

1987.9 |

69.28 |

100.550 |

|

|

4647.00 |

3.245% |

1976.5 |

67.98 |

100.000 |

|

|

4594.00 |

3.000% |

1960.8 |

66.63 |

99.580 |

|

Support |

4575.00* |

2.700% |

1949.1 |

62.00 |

98.940 |

Colors within the report:

Green is always the 200 period (day, week).

Red is always 21,

Blue = 50,

Brown =

100 *Stars have added importance

- Upgrades

- Algonquin Power (AQN CN) Raised to Outperform at BMO; PT C$10.01

- American Air (AAL) Raised to Overweight at Morgan Stanley; PT $20

- Aon PLC (AON) Raised to Overweight at JPMorgan; PT $321

- Beacon Roofing (BECN) Raised to Outperform at William Blair

- Brown & Brown (BRO) Raised to Buy at Goldman; PT $83

- Raised to Outperform at RBC; PT $81

- Cboe (CBOE) Raised to Overweight at Barclays; PT $204

- Chevron (CVX) Raised to Buy at Jefferies; PT $184

- Core & Main (CNM) Raised to Buy at Citi

- DoorDash (DASH) Raised to Buy at Jefferies; PT $130

- Dow (DOW) Raised to Neutral at On Field; PT $57

- Eagle Materials (EXP) Raised to Buy at Loop Capital; PT $240

- Enphase Energy (ENPH) Raised to Overweight at Wells Fargo

- Epam Systems (EPAM) Raised to Buy at HSBC; PT $350

- Fastly (FSLY) Raised to Sector Perform at RBC; PT $18

- FedEx (FDX) Raised to Buy at Melius

- Fiserv (FI) Raised to Overweight at KeyBanc; PT $160

- Franklin Resources (BEN) Raised to Equal-Weight at Wells Fargo

- Gitlab (GTLB) Raised to Buy at Mizuho Securities; PT $73

- Installed Building (IBP) Raised to Buy at Loop Capital; PT $205

- Intercontinental Exchange (ICE) Raised to Overweight at Barclays

- Kyndryl (KD) Raised to Outperform at Evercore ISI; PT $26

- MetLife (MET) Raised to Buy at Goldman; PT $80

- NEXTracker (NXT) Raised to Overweight at Wells Fargo

- RenaissanceRe (RNR) Raised to Neutral at JPMorgan; PT $204

- Toll Brothers (TOL) Raised to Outperform at Wolfe; PT $118

- TopBuild (BLD) Raised to Buy at Loop Capital; PT $405

- Tuya (TUYA) ADRs Raised to Buy at Goldman; PT $2.75

- Upwork (UPWK) Raised to Buy at Jefferies; PT $20

- Downgrades

- Agilon Health (AGL) Cut to Market Perform at Leerink

- Cut to Peerperform at Wolfe

- Cut to Hold at Stifel; PT $10

- Allovir (ALVR) Cut to Underweight at Morgan Stanley; PT 50 cents

- American Express (AXP) Cut to Underperform at Baird; PT $190

- Ardagh Metal Packaging (AMBP) Cut to Equal-Weight at Barclays; PT $4

- Argo Blockchain (ARB LN) ADRs Cut to Neutral at Compass Point; PT $3

- Array (ARRY) Cut to Equal-Weight at Wells Fargo

- Capital One (COF) Cut to Neutral at Baird; PT $145

- ChampionX (CHX) Cut to Neutral at Piper Sandler; PT $32

- Chubb (CB) Cut to Neutral at Goldman; PT $222

- Citigroup (C) Cut to Sell at SocGen; PT $43

- CME Group (CME) Cut to Equal-Weight at Barclays; PT $222

- CMS Energy (CMS) Cut to Neutral at Seaport Global Securities

- Deere (DE) Cut to Hold at Melius; PT $478

- DTE Energy (DTE) Cut to Neutral at Seaport Global Securities

- Ecolab (ECL) Cut to Neutral at Seaport Global Securities

- Endava (DAVA) ADRs Cut to Hold at HSBC; PT $80

- Exelon (EXC) Cut to Neutral at Seaport Global Securities

- Ferguson (FERG) Cut to Market Perform at Raymond James

- Fidelis Insurance (FIHL) Cut to Neutral at JPMorgan; PT $15

- First Solar (FSLR) Cut to Equal-Weight at Wells Fargo

- Frontier Airlines (ULCC) Cut to Equal-Weight at Morgan Stanley; PT $8

- Garmin (GRMN) Cut to Neutral at JPMorgan; PT $135

- Hartford Financial (HIG) Cut to Neutral at JPMorgan; PT $91

- Helmerich & Payne (HP) Cut to Neutral at Piper Sandler; PT $41

- iClick (ICLK) ADRs Cut to Neutral at Citi; PT $4

- Linde (LIN) Cut to Neutral at Seaport Global Securities

- Markel Group Inc (MKL) Cut to Sector Perform at RBC; PT $1,475

- MarketAxess (MKTX) Cut to Equal-Weight at Barclays; PT $291

- Marsh & McLennan (MMC) Cut to Sell at Goldman; PT $185

- Navient (NAVI) Cut to Underperform at Cowen; PT $15

- Okta (OKTA) Cut to Neutral at Mizuho Securities; PT $85

- Pool Corp (POOL) Cut to Hold at Loop Capital; PT $415

- PulteGroup (PHM) Cut to Neutral at Citi

- Sherwin-Williams (SHW) Cut to Neutral at Seaport Global Securities

- SiteOne Landscape (SITE) Cut to Hold at Loop Capital; PT $165

- Southwest Air (LUV) Cut to Underperform at Bernstein; PT $24

- SunPower (SPWR) Cut to Underweight at Wells Fargo

- T. Rowe (TROW) Cut to Underweight at Wells Fargo

- TD SYNNEX (SNX) Cut to Neutral at JPMorgan; PT $113

- Terran Orbital Corp (LLAP) Cut to Neutral at B Riley; PT $1.35

- Theravance Bio (TBPH) Cut to Inline at Evercore ISI; PT $8

- Voya Financial (VOYA) Cut to Neutral at Goldman; PT $82

- W R Berkley Corp (WRB) Cut to Sector Perform at RBC; PT $73

- Wells Fargo (WFC) Cut to Neutral at Baird; PT $55

- ZoomInfo (ZI) Cut to Underperform at RBC; PT $14

- Initiations

- Aramark (ARMK) Rated New Buy at Truist Secs

- Complete Solaria (CSLR) Rated New Overweight at Cantor; PT $6

- Couchbase (BASE) Rated New Overweight at Wells Fargo; PT $26

- International Paper (IP) Reinstated Neutral at BNPP Exane; PT $37.10

- KeyCorp (KEY) Rated New Market Perform at Raymond James

- ManpowerGroup (MAN) Rated New Market Perform at William Blair

- NioCorp Developments (NB CN) Rated New Corporate at Edison Investment Research

- Paccar (PCAR) Reinstated Overweight at Morgan Stanley; PT $125

- Packaging Corp (PKG) Reinstated Outperform at BNPP Exane; PT $183

- Stryker (SYK) Rated New Add at CTBC Securities; PT $345

- Vera Therapeutics (VERA) Rated New Overweight at Cantor

- WestRock (WRK) Reinstated Outperform at BNPP Exane; PT $50.10

Data sources: Bloomberg, Reuters, CQG

Comments are closed