TODAY’S GAME PLAN: from the trading

desk, this is not research

DATA/HEADLINES: 8:30ET New York Fed Services Business Activity, Retail Sales, Import Price Index, Export Price

Index; 9:00ET Fed’s Barr speaks, Fed’s Bowman speaks; 9:15ET Industrial Production, Capacity Utilization, Manufacturing Production; 10:00ET Business Inventories, NAHB Housing Market Index; 1:00ET 20 Year Bond Auction; 2:00ET Fed Beige Book; 3:00ET Fed’s Williams

speaks

TODAY’S HIGHLIGHTS and News:

-

Record-breaking cold expected across the Rocky Mountains, Great Plains and Midwest

-

The Fed has tended to ease about six months after its final rate hike

-

China birth rates fell to a record low in 2023

-

Jamie Dimon talks up Trump policies on CNBC in Davos

World stocks fell as markets grappled with a central bank push back against interest rate cut expectations and signs of a patchy economic recovery for China. China

data pointed to a worsening property crisis as home prices fell the most in almost nine years in December. Inflation concerns also dented risk appetite after Britain’s annual rate of consumer price inflation sped up for the first time in 10 months in December.

Data showed UK headline CPI surprised at 4.0% versus consensus 3.8% and core at 5.1% versus 4.9% forecast. The ECB is “likely” to cut rates by or in the summer, Christine Lagarde said, adding that overoptimistic rate-cut bets in the market don’t help. In the

Red Sea, tensions remained high as the US mounted fresh strikes against Iran-aligned Houthi militants in Yemen on Tuesday after a Houthi missile hit a Greek vessel.

EQUITIES:

US equity futures are lower amid broad weakness in Europe and Asia overnight. Russell 2000 small cap index sharply underperforms and the VIX hit a two month high, as investors’ optimism

for interest rate cuts got a reality check. Stocks have struggled as policymakers push back against persistent bets that central banks will cut rates early and often in 2024. State Street CEO Ron O’Hanley said he believes that Fed will err to the side of

holding rates as the “danger of undershooting is far greater than the danger of overshooting.” Regional banks fourth-quarter results are in focus this morning after earnings from Wall Street’s big lenders got a mixed reception.

US Bancorp (USB +0.3%) reported earnings that beat analysts’ estimates as the bank benefits from elevated interest rates. Earnings will include Citizens Financial Group (CFG),

US Bancorp (USB), Charles Schwab (SCHW), and Prologis (PLD) posting their results before the open. Kinder Morgan (KMI) and Discover Financial (DFS) report after the close.

Futures ahead of the bell: E-Mini S&P -0.4%, Nasdaq -0.5%, Russell 2000 -1.3%, Dow -0.3%.

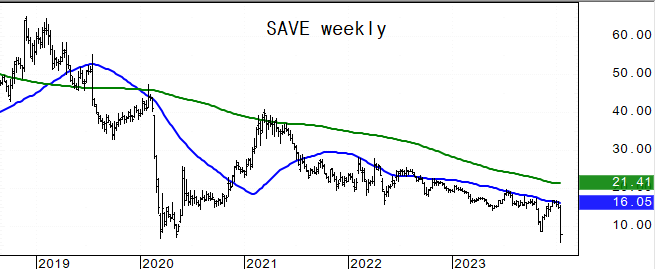

In premarket trading, Spirit Airlines (SAVE) declines 15% after a federal judge blocked JetBlue’s $3.8 billion acquisition of the budget airline. US-listed Chinese stocks fell , with

the exchange-traded KraneShares CSI China Internet Fund (KWEB) trading more than 3% lower. Allakos (ALLK) drops 10%, set to extend Tuesday’s 60% plunge after the drug developer was downgraded to hold at Jefferies following two mid-stage trials that failed

to meet their main goals. Fisker (FSR) drops 3% after TD Cowen downgrades to market perform, saying the electric-vehicle maker’s growing pains are continuing to accumulate. Interactive Brokers (IBKR) falls 4% after the firm reported fourth-quarter total net

interest income that missed estimates. Mattel (MAT) falls 3% after Morgan Stanley downgrades the toymaker to equal-weight, citing limited growth drivers. Morgan Stanley (MS) slips 1% after being downgraded to neutral at JPMorgan. Charles Schwab Corp. reported

a decline in net new assets in the fourth quarter, as the brokerage navigated a tumultuous year. Schwab (SCHW -1%) said net new assets were $66.3 billion, a 48% drop on the year which also missed analyst estimates.

European equities are broadly lower with all sectors in the red as real estate and energy lead losses. The UK, Portugal, Finland are the main underperformers in the region. UK equity

markets plunged after a surprise rise in inflation. The Stoxx Europe 600 fell as sectors with high exposure to China, such as mining, autos, retail and luxury underperformed. Shell Plc was the biggest drag on the index as it halted oil tanker transits through

the Red Sea. European luxury stocks like LVMH and Richemont slid on China worries, Adidas and Puma were also hit. Stoxx 600 -1.3%, DAX -1%, CAC -1.1%, FTSE 100 -1.7%. REITS -3.1%, Utilities -2.3%, Retail -2.1%, Energy -2.1%. Technology is best performer but

still down 0.6%.

Shares in Asia had their biggest drop since August as China’s latest economic data underscored a patchy recovery. Data showed a slump in home prices worsened while retail sales fell short

of estimates in December, even as the nation reached its goal for 2023 economic growth. The MSCI Asia Pacific Index dropped 1.7%, with tech giants such as Tencent and Samsung Electronics among the biggest contributors to losses. Japanese stocks fared better

than regional peers, thanks to a slump in the yen. Chinese equities led regional losses, with the Hang Seng China Enterprises Index falling nearly 4%. The Hang Seng Index fell for a third straight day; down 6% on the week with losses of over 10% year to date.

A Bank of America survey shows shorting China equities remains one of the most crowded trades on Wall Street. Hang Seng Tech -5%, Hang Seng Index -3.7%, Kospi -2.5%, Sensex -2.2%, CSI 300 -2.2%, Singapore -1.3%, Taiwan -1.1%, Philippines -1%, Topix -0.3%,

ASX 200 -0.3%, Vietnam -0.05%.

FIXED INCOME:

The Treasuries curve is aggressively flatter on the day, with front-end underperforming following a wider bear flattening move in gilts after UK inflation figures.

Long-end Treasury yields slightly richer on the day while front-end of the curve is cheaper by around 6bp vs Tuesday close. Treasury auctions include $13b 20-year bond reopening today, with $18b 10-year TIPS new issue expected Thursday. WI 20-year at ~4.40%

is ~19bp cheaper than December’s stop-out, which tailed the WI by 1.5bp. Markets price in a 65% chance of a Fed rate cut in March, according to the CME FedWatch tool, compared with the 81% likelihood at the start of the week. 10 year yield ~4.07%; 2 year

yield ~4.28%.

METALS:

Gold steadied, after falling the most in six weeks yesterday, as investors dialed back expectations on how soon the Federal Reserve will cut interest rates. The precious

metal declined 1.4% on Tuesday after Fed Governor Christopher Waller appeared to push back against expectations for as many as six rate reductions this year. The comments — although not outright hawkish — prompted swaps traders to recalibrate bets on the timing

of cuts. Spot gold -0.05%, silver -0.4%.

ENERGY:

The risk-off sentiment pushed Oil prices lower as economic growth in China, the world’s second-largest crude user, slightly missed expectations, raising concerns

about future demand. Still, China’s oil refinery throughput in 2023 rose 9.3% to a record high, indicating elevated demand even if it lagged some analysts’ expectations. Overall oil exports from Russia and Central Asia declined 12% MoM. OPEC said. OPEC expects

global oil demand to slow next year, even as it raised its economic forecast as easing inflation spurs global growth. WTI -2%, Brent -1.7%, US Nat Gas -2.5%, RBOB -1.6%.

CURRENCIES:

In currency markets, risk-sensitive currencies faced pressure due to disappointing economic data from China. Sterling rose as UK inflation data surprised on the

upside, dampening BoE rate cut expectations. The euro fluctuates amid statements from ECB President Christine Lagarde. Investor bets for ECB rate cuts are excessive and possibly self-defeating because they could hold back monetary easing, Dutch central bank

chief Klaas Knot told CNBC today. The US dollar hovered near a one-month high after comments from US Federal Reserve officials lowered expectations for aggressive interest rate cuts. US$ Index +0.05%, GBPUSD +0.3%, USDJPY +0.4%, EURUSD -0.05%, AUDUSD -0.5%,

NZDUSD -0.3%, USDCHF +0.4%.

Bitcoin -1.7%, Ethereum -2.2%.

TECHNICAL LEVELS:

|

ESH24 |

10 Year Yield |

Feb Gold |

Feb WTI |

Spot $ Index |

|

|

Resistance |

4900.00 |

5.250% |

2180.0 |

80.50 |

107.350 |

|

|

4862.00 |

5.000% |

2152.3 |

78.15 |

106.000 |

|

|

4841.50 |

4.550% |

2117.0 |

77.83 |

104.780 |

|

|

4828.50 |

4.185% |

2100.0 |

75.80 |

103.440 |

|

|

4815.00 |

4.050% |

2067.3 |

74.24 |

103.225 |

|

Settlement |

4798.50 |

2030.2 |

72.40 |

||

|

|

4768.00 |

3.780% |

2025.6 |

70.13 |

101.600 |

|

|

4754.00 |

3.640% |

2013.2 |

69.28 |

100.550 |

|

|

4717.00 |

3.245% |

1978.2 |

67.98 |

100.000 |

|

|

4702.00 |

3.000% |

1960.8 |

66.63 |

99.580 |

|

Support |

4660/65 |

2.700% |

1949.1 |

62.00 |

98.940 |

Colors within the report:

Green is always the 200 period (day, week).

Red is always 21,

Blue = 50,

Brown =

100 *Stars have added importance

- Upgrades

- Accenture (ACN) Raised to Outperform at BNPP Exane; PT $440

- Burlington Stores (BURL) Raised to Overweight at Piper Sandler; PT $240

- CNH Industrial (CNHI) Raised to Buy at Goldman; PT $19

- ExlService (EXLS) Raised to Buy at Citi; PT $36

- Futu Holdings (FUTU) ADRs Raised to Overweight at JPMorgan; PT $64

- Instacart (CART) Raised to Outperform at Wolfe; PT $35

- Lazard Inc (LAZ) Raised to Buy at CFRA; PT $45

- Marathon Digital Holding (MARA) Raised to Buy at BTIG; PT $27

- Nutanix (NTNX) Raised to Outperform at William Blair

- Phreesia (PHR) Raised to Buy at DA Davidson; PT $32

- Polaris (PII) Raised to Overweight at Morgan Stanley

- Revolve Group (RVLV) Raised to Overweight at Piper Sandler; PT $21

- Shinhan Financial (055550 KS) ADRs Raised to Buy at BofA

- Twist Bioscience (TWST) Raised to Buy at Goldman; PT $45

- Woori Financial (316140 KS) ADRs Raised to Buy at BofA

- Downgrades

- Accolade (ACCD) Cut to Neutral at DA Davidson; PT $14

- Allakos (ALLK) Cut to Hold at Jefferies; PT $1.50

- Cut to Market Perform at LifeSci Capital

- Ansys (ANSS) Cut to Peerperform at Wolfe

- Cut to Neutral at Rosenblatt Securities Inc; PT $345

- Axonics Inc (AXNX) Cut to Hold at Needham

- Boston Properties (BXP) Cut to Hold at Hedgeye

- CrowdStrike (CRWD) Cut to Hold at WestPark Capital

- DXC Technology (DXC) Cut to Sell at Citi; PT $21

- Fisker (FSR) Cut to Market Perform at Cowen; PT $1

- Fortinet (FTNT) Cut to Neutral at Daiwa; PT $62

- Cut to Equal-Weight at Capital One; PT $62

- Globant (GLOB) Cut to Neutral at Grupo Santander; PT $260

- Luminar (LAZR) Cut to Hold at Deutsche Bank; PT $19

- Mattel (MAT) Cut to Equal-Weight at Morgan Stanley

- Morgan Stanley (MS) Cut to Market Perform at KBW; PT $91

- Cut to Neutral at JPMorgan; PT $87

- Pandora (PNDORA DC) ADRs Cut to Hold at Hedgeye

- Papa John’s (PZZA) Cut to Hold at Hedgeye

- Rent the Runway (RENT) Cut to Neutral at Piper Sandler; PT 75 cents

- Rivian (RIVN) Cut to Hold at Deutsche Bank; PT $19

- SolarEdge (SEDG) Cut to Underweight at Barclays; PT $50

- Spirit Air (SAVE) Cut to Negative at Susquehanna; PT $5

- Cut to Neutral at Seaport Global Securities

- Teladoc (TDOC) Cut to Neutral at DA Davidson; PT $22

- Initiations

- American Coastal (ACIC) Rated New Outperform at Raymond James; PT $15

- Aramark (ARMK) Reinstated Buy at Goldman; PT $33

- AutoNation (AN) Rated New Outperform at Evercore ISI; PT $185

- Cloudflare (NET) Rated New Equal-Weight at Capital One; PT $83

- E2open (ETWO) Rated New Equal-Weight at Morgan Stanley; PT $4

- EastGroup (EGP) Rated New Buy at Hedgeye

- EchoStar (SATS) Rated New Neutral at JPMorgan; PT $18

- European Wax (EWCZ) Rated New Sell at Hedgeye

- Global-e Online (GLBE) Rated New Overweight at Wells Fargo; PT $50

- Hershey (HSY) Rated New Buy at President Capital Management; PT $220

- Infosys (INFO IN) ADRs Rated New Outperform at BNPP Exane; PT $24

- Lithia & Driveway (LAD) Rated New Outperform at Evercore ISI; PT $400

- Nuvei (NVEI CN) Rated New Equal-Weight at Wells Fargo; PT C$39.12

- Paymentus (PAY) Rated New Equal-Weight at Wells Fargo; PT $17

- Paysafe (PSFE) Rated New Buy at BTIG; PT $19

- Realty Income (O) Rated New Buy at Hedgeye

- Remitly (RELY) Rated New Underweight at Wells Fargo; PT $16

- Rio Tinto (RIO LN) ADRs Rated New Buy at Berenberg; PT $79

- Rocket Lab USA (RKLB) Rated New Overweight at KeyBanc; PT $8

- Spirit Aero (SPR) Rated New Sector Weight at KeyBanc

- Rated New Buy at Citi

- TransDigm (TDG) Rated New Overweight at KeyBanc; PT $1,180

- Wells Fargo (WFC) Rated New Buy at Punto Casa de Bolsa; PT $59.90

- Wipro (WPRO IN) ADRs Rated New Underperform at BNPP Exane; PT $5.20

- Zscaler (ZS) Rated New Sector Weight at KeyBanc

Data sources: Bloomberg, Reuters, CQG

Comments are closed