TODAY’S GAME PLAN: from the trading

desk, this is not research

DATA/HEADLINES: 9:45ET S&P Global US Manufacturing/Services PMIs, BOC Rate Decision; 1:00ET 5 year note auction

US manufacturing PMI probably dipped to 47.6 in January from 47.9 last month

TODAY’S HIGHLIGHTS and News:

-

Tesla plans a new mass-market EV with production starting in mid-2025

-

Russian plane carrying 74 passengers, mostly Ukrainian military prisoners for an exchange, crashed

-

China “Unexpectedly” Cuts Required Reserve Ratio

-

The shelves of CVS in Columbia Heights (in DC) have been empty for over a year; Street vendors openly resell the stolen items outside the store

-

New Hampshire exit polls show 70% of Nikki Haley voters were “undeclared”

Global shares rose, fueled by positive tech earnings and on optimism Chinese authorities will offer support to its stock markets. China’s PBoC announced it will cut

the reserve requirement ratio by 0.5% on Feb 5th and hinted at more support measures to come, showing an urgency to shore up its economy. It is the biggest such cut since December 2021. The European Central Bank meets on Thursday and is widely expected to

keep rates unchanged. A coalition of 24 nations led by the US and UK conducted new strikes against Houthi fighters in Yemen on Tuesday. The strikes were aimed at stopping the Houthis’ attacks on global trade, Britain said. The US also carried out strikes against

Iran-linked militia in Iraq on Tuesday, following an attack on an Iraqi air base that wounded US forces. Disruptions to shipping in the Red Sea caused manufacturing supply chains to lengthen for the first time in a year, fueling fears of broader economic fallout.

EQUITIES:

US equity futures extended gains as a wave of positive earnings from technology companies reinforced the picture of a broadly robust corporate sector. Netflix rallied sharply in extended

trading Tuesday after the video streaming service handily beat subscriber estimates in the fourth quarter. Boeing CEO Dave Calhoun is meeting senators in DC today and tomorrow as the company faces questions about its quality control and aircraft safety.

Today’s earnings include Tesla, IBM, CSX, Abbott, Freeport-McMoRan, Kimberly-Clark, Las Vegas Sands.

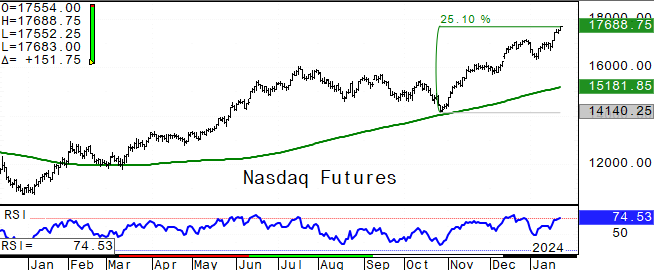

Futures ahead of the bell: E-Mini S&P +0.5%, Nasdaq +0.8%, Russell 2000 +1.1%, Dow +0.3%.

In pre-market trading, Netflix advanced about 10% after posting its best quarter for sign-ups since early in the pandemic. Streaming peers also gain: Roku (ROKU) +2.7%. AT&T (T) fell

5% after its adjusted EPS forecast missed and projected 2024 earnings fell far below analysts’ estimates. Texas Instruments (TXN) fell over 3% after a disappointing quarterly forecast. DuPont de Nemours (DD) falls 11% after forecasting first-quarter sales

that are below analysts’ estimates on weak demand from China. EBay (EBAY) gains 4.5% in the wake of a plan to cut jobs. Intuitive Surgical (ISRG) climbs 6% after the company confirmed its application with US regulators for a next-generation robotic surgical

system. US-listed Chinese stocks rally after officials stepped up stimulus measures. Alibaba (BABA) +1.7%, Baidu (BIDU) +2.4%, PDD Holdings (PDD) +2.2%, JD.com (JD) +2%, NetEase (NTES) +4%. Earnings include Tesla, IBM, CSX, Abbott, Freeport-McMoRan, Kimberly-Clark,

Las Vegas Sands.

European gauges are higher, boosted by technology stocks after software firm SAP and chip-making equipment maker ASML Holding posted strong earnings. ASML, a bellwether for the industry’s

health, rose as much as 7.5% after orders more than tripled last quarter. SAP jumped after announcing plans to restructure operations and increase focus on AI. The Stoxx 600 Index gained 1% with technology and REITs outperforming while telecom lagged. Utilities

and renewables were boosted by Siemens Energy AG’s strong beat. EasyJet Plc shares also rose after the airline’s trading update. The eurozone economy showed signs of a nascent recovery at the start of the year after a contraction in business activity eased

slightly and price pressures intensified, according to a closely watched survey. S&P Global’s flash eurozone PMI rose to a six-month high of 47.9, up from 47.6, but still remains in contraction. UK PMI surprisingly rose in January to the highest level in seven

months. Stoxx 600 +1%, DAX +1.4%, CAC +0.9%, FTSE 100 +0.4%. Technology +4%, Basic Resources +1.8%, REITs +1.7%. Telecom is flat.

Shares in Asia were mixed, with Hong Kong jumping on China’s market rescue plan, while Japanese stocks fell on the central bank governor’s hawkish tone. Japan unexpectedly posted a trade

surplus in December as exports climbed. The MSCI Asia Pacific Index was little changed. with Alibaba and Tencent among the biggest boosts, while Samsung and Sony dragged on the regional benchmark. China’s mutual fund houses are trying to tamp down investors’

enthusiasm for US stocks, putting new restrictions on buying into their products. Hang Seng Index +3.6%, Thailand +1.8%, Shanghai Composite +1.8%, CSI 300 +1.4%, Sensex +1%, Philippines +0.9%, Taiwan was flat. Kospi -0.35%, Vietnam -0.4%, Nikkei 225 -0.8%.

FIXED INCOME:

Treasury yields are lower across the board, led by the belly of the curve. During the Asia session, spillover to Treasuries was limited as JGBs sold off on mounting

sentiment that Bank of Japan will soon take a hawkish turn. Germany auctioned 14yr and 24yr bonds and Portugal 5yr, 18yr and 21yr paper. US 10-year yields around 4.11%, richer by 2bp on the day. Treasury auction cycle continues with $61b 5-year notes today;

Tuesday’s 2-year note sale stopped on the screws; cycle concludes Thursday with $41b 7-year notes. Markets are now pricing in a 47% chance of a rate cut in March from the Fed, according to the CME FedWatch tool, compared to the 88% chance priced in a month

earlier.

METALS:

Gold rose slightly — after edging higher on Tuesday — as markets remained cautious ahead of US economic data that may provide a steer on the outlook for monetary

easing. Gold is holding near its 50-day moving average, a key support level in recent months, as traders await more clues on the Fed’s rate path. With fourth-quarter GDP due tomorrow and the core PCE deflator Friday, any signs that rates will stay higher

for longer will probably be negative for gold. Spot gold +0.2%, silver +1.6%.

ENERGY:

Oil prices fluctuated in a tight range overnight as traders weighed the impact from escalating geopolitical tensions and concerns over tepid demand. US forces carried

out airstrikes against an Iran-backed militia in Iraq after the group had attacked an air base where American troops are stationed. Slowing demand and surprisingly robust growth in non-OPEC+ output — especially from the US — signal a well-supplied oil market.

North Dakota brought some oil output back online after weather-related disruption. Qatar is delaying some LNG shipments to Europe because of longer travel times. WTI +0.2%, Brent +0.2%, US Nat Gas +0.4%, RBOB +0.1%.

CURRENCIES:

In currency markets, the euro rose as investors judged the eurozone PMI data reduced chances of early rate cuts. A deeper downturn in French and German business activity

offset an improvement in the rest of the region. The US$ index slipped, but is still up nearly 2% this month, on course for its strongest monthly performance since September as traders walk back their expectations of early and steep Fed interest rate cuts.

The Japanese yen, meanwhile, strengthened as investors firmed up bets that the Bank of Japan will exit stimulus in coming months. Sterling spiked after Britain’s PMI figures were better than expected. US$ Index -0.5%, GBPUSD +0.5%, EURUSD +0.5%, USDJPY -0.8%,

AUDUSD +0.3%, USDCAD -0.05%, USDCHF -0.8%, USDSEK -0.7%.

Bitcoin +2%, Ethereum 1.5%.

TECHNICAL LEVELS:

|

ESH24 |

10 Year Yield |

Feb Gold |

March WTI |

Spot $ Index |

|

|

Resistance |

|

5.000% |

2152.3 |

81.37 |

109.120 |

|

|

5000.00 |

4.755% |

2117.0 |

80.50 |

107.350 |

|

|

4981.00 |

4.550% |

2100.0 |

78.15 |

106.000 |

|

|

4950.00 |

4.255% |

2062.3 |

77.71 |

104.780 |

|

|

4921/25 |

4.150% |

2027.5 |

75.52 |

103.480 |

|

Settlement |

4895.00 |

2025.8 |

74.37 |

||

|

|

4856.00 |

4.070% |

2012.3 |

73.65 |

102.955 |

|

|

4835.00 |

3.780% |

1978.3 |

70.13 |

102.530 |

|

|

4814.00 |

3.640% |

1960.8 |

69.28 |

101.780 |

|

|

4804.00 |

3.245% |

1949.1 |

67.98 |

101.280 |

|

Support |

4784.00 |

3.000% |

1938.8 |

66.63 |

100.000 |

Colors within the report:

Green is always the 200 period (day, week).

Red is always 21,

Blue = 50,

Brown =

100 *Stars have added importance

- Upgrades

- Acadia Pharma (ACAD) Raised to Buy at Needham; PT $37

- AMD (AMD) Raised to Buy at New Street Research; PT $215

- Capital City Bank (CCBG) Raised to Buy at Janney Montgomery; PT $37.50

- CrossFirst Bankshares (CFB) Raised to Overweight at Stephens; PT $18

- DTE Energy (DTE) Raised to Buy at CFRA

- Endeavour Mining (EDV CN) Raised to Buy at Liberum; PT C$28.22

- Figs (FIGS) Raised to Equal-Weight at Barclays; PT $7

- Squarespace (SQSP) Raised to Market Outperform at JMP; PT $40

- StoneCo (STNE) Raised to Neutral at Bradesco BBI; PT $23

- Sunoco (SUN) Raised to Buy at Citi; PT $65

- Tencent Music (TME) ADRs Raised to Buy at UBS; PT $10.50

- Verizon (VZ) Raised to Outperform at Daiwa; PT $47

- Webster Financial (WBS) Raised to Overweight at JPMorgan; PT $65

- XP Inc. (XP) Raised to Outperform at Bradesco BBI; PT $32

- Downgrades

- Biogen (BIIB) Cut to Neutral at UBS

- Brilliant Earth Group (BRLT) Cut to Market Perform at Cowen; PT $3.40

- Canadian National (CNR CN) Cut to Reduce at Veritas Investment Research Co; PT C$168

- Danaher (DHR) Cut to Equal-Weight at Barclays; PT $240

- DXC Technology (DXC) Cut to Underweight at JPMorgan; PT $24

- Endava (DAVA) ADRs Cut to Equal-Weight at Morgan Stanley; PT $80

- Epam Systems (EPAM) Cut to Underweight at Morgan Stanley; PT $250

- Home Bancorp (HBCP) Cut to Neutral at Piper Sandler; PT $43

- Inhibrx (INBX) Cut to Market Perform at LifeSci Capital; PT $36

- Insteel Industries (IIIN) Cut to Market Perform at Kansas City Capital

- Mosaic (MOS) Cut to Neutral at Mizuho Securities

- Netflix (NFLX) Cut to Hold at Deutsche Bank; PT $525

- NuStar Energy (NS) Cut to Hold at Stifel; PT $23

- PagerDuty Inc (PD) Cut to Equal-Weight at Morgan Stanley

- Plug Power (PLUG) Cut to Underperform at BMO; PT $2.50

- Stellantis (STLA) Cut to Hold at HSBC

- Thermo Fisher (TMO) Cut to Equal-Weight at Barclays

- Tilly’s (TLYS) Cut to Neutral at B Riley; PT $8.75

- Uber (UBER) Cut to Hold at Gordon Haskett

- Ultrapar (UGPA3 BZ) ADRs Cut to Reduce at HSBC; PT $4.70

- Vertex Pharmaceuticals (VRTX) Cut to Sell at Canaccord; PT $379

- Initiations

- Alignment Healthcare (ALHC) Rated New Buy at Stifel; PT $11

- Apollo Medical (AMEH) Rated New Buy at Stifel; PT $45

- Autolus Therapeutics (AUTL) ADRs Rated New Buy at KBC Securities

- Ford (F) Rated New Sell at Redburn; PT $10

- General Motors (GM) Rated New Neutral at Redburn; PT $40

- Nikola (NKLA) Rated New Outperform at Baird; PT $2

- Polestar (PSNY) ADRs Rated New Underperform at Bernstein; PT $1.15

- Stellantis (STLA) Rated New Buy at Redburn; PT $29.35

- Tesla (TSLA) Reinstated Sell at Redburn; PT $170

Data sources: Bloomberg, Reuters, CQG

Comments are closed