TODAY’S GAME PLAN: from the trading

desk, this is not research

DATA/HEADLINES: 8:30ET Core PCE Price Index m/m, Personal Income m/m, Personal Spending m/m,10:00ET Pending Home

Sales MoM, 11:00ET Kansas City Fed Services Activity, 1:00PM ET Baker Hughes US Rig Count

TODAY’S HIGHLIGHTS and News:

-

Jamie Dimon has moved some of the bank’s top managers into new senior roles as he prepares potential successors.

-

North Carolina sea turtles are dying due to plunging temperatures

-

Jannik Sinner defeats Novak Djokovic in Australian Open semifinals, becomes youngest to reach men’s finals

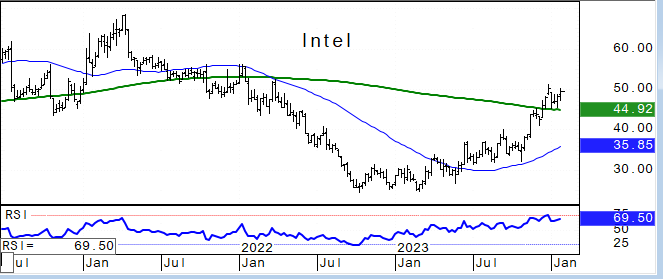

Global shares were mixed on Friday, as US equity futures dropped after Intel’s disappointing outlook dragged the Nasdaq down after six days of gains. The chipmaker

tumbled premarket as it faces weakening demand in the lucrative market for data center chips. Investors channeled $17.6 billion into global equity funds in the week through Jan. 24, Bank of America Corp. strategists said, citing EPFR data, while US equity

funds took in $5.3 billion. In Asia, stocks halted their winning streak as confidence in China’s rescue measures diminished. Chinese equities pulled in $11.9 billion in the week through Wednesday, the second-biggest inflow ever and largest since July 2015,

BofA strategists said. Meanwhile European gauges were lifted by positive earnings from LVMH, boosting luxury goods firms. Benchmark Treasuries saw a slight increase, while the dollar and oil both experienced declines.

EQUITIES:

US equity futures were lower and retreated from a record high at the week’s end, as disappointing earnings from Intel dampen the euphoria about Big Tech. Intel shares slumped 11% after

the chipmaker gave a first-quarter forecast that was much weaker than expected. Analysts note that the company’s solid 4Q results were overshadowed by its weak guidance for the current quarter. Other notable pre-market movers include Coinbase rising 4.5%,

with crypto stocks broadly climbing amid a gain in Bitcoin, after Oppenheimer raised its recommendation to outperform. KLA Corporation shares dropped after providing guidance below estimates. Snap shares rose 3% after Deutsche Bank upgraded its rating, citing

a positive outlook for online advertising in Q4. T-Mobile shares declined 2% as Q4 earnings per share missed estimates. Visa (V US) shares fell 3.2% despite a robust fiscal first quarter, with concerns about potential weather-related impacts on January volumes

and higher operating expenses. Earnings today include AmEx(+3% pre market) , ADM, Colgate-Palmolive, First Citizens.

*US DEC. CORE PCE PRICE INDEX RISES 2.9% Y/Y; EST. 3.0%. Dec Core PCE Prices 0.172% (consensus 0.2%, prior 0.1%). Dec PCE Prices 0.167% (consensus 0.2%, prior -0.1%)

Futures ahead of the bell: E-Mini S&P -0.1%, Nasdaq -0.5%, Russell 2000 +0.3%, Dow -0.1%.

European gauges edged higher and approached their January 2022 high. Luxury and food/beverage stocks led gains, and the consumer products/services subindex saw its most significant jump

in over a year, boosted by LVMH’s strong sales update. Remy Cointreau SA advanced due to planned cost cuts, offsetting a sales drop. Chip stocks declined following Intel Corp.’s disappointing forecast. European stocks, having a mixed start to the year, were

on track for their best week since November after a late 2023 rally. The European Central Bank’s decision to keep rates unchanged and Christine Lagarde’s mention of possible rate cuts around mid-2024 signaled ongoing monetary policy considerations. Volvo AB

declined after missing quarterly order intake expectations, while Lonza Group AG surged, naming former Unilever CFO Jean-Marc Huet as its new chairman. Stoxx 600 +1.1%, DAX +0.1%, CAC +2.2%, FTSE 100 +1.3%

Asian stocks declined, ending a six-day winning streak, as tech shares stumbled, and the China rally paused due to skepticism about the impact of market rescue measures. The MSCI Asia

Pacific Index dropped up to 0.5%, with Toyota, Alibaba, and Tencent being significant drags. Chip and PC stocks fell following a disappointing outlook from Intel. Chinese equities retreated after experiencing their most substantial three-day advance since

2022, driven by optimism about Beijing’s recent efforts to support the economy and stabilize markets. Investors are now assessing the duration of these gains. Japanese benchmarks led declines in the region, while shares in Singapore and South Korea saw gains.

Pertamina Geothermal shares jumped up to 20% after being added to an index of Indonesia’s 45 most traded stocks, while Chandra Asri dropped by the same percentage on removal. China real estate stocks extended their recent rally after a regulator indicated

guidance for increased credit support for the economy while maintaining stability in property credit. Notable movers included Cnooc, rising as much as 2.9% in Hong Kong, Kia climbing 2.9%, and Sumco shares falling as much as 6.6% after being downgraded by

CLSA due to ongoing weakness in the industry. CSI 300 -0.2%, Hang Seng Index -1.6%, Taiwan -0.04%, ASX 200 +0.5%, Topix -1.3%, Kospi +0.3%. Vietnam +0.4%, Sensex -0.5%, Indonesia -0.9%.

FIXED INCOME:

Treasuries show a narrow mix with a flatter yield curve, reversing some of Thursday’s steepening in 2s10s and 5s30s spreads. The adjustment precedes a crucial inflation reading for December.

German short-term bonds continue to outperform since Wednesday’s ECB meeting. Long-end US yields decrease by less than 1bp, while the front-end is less than 2bp cheaper, and the belly remains largely unchanged, with 10-year yields hovering around 4.115%. The

yield curve flattens slightly, with 2s10s compressing by about 2bp and 5s30s by approximately 1bp on the day.

METALS:

Gold prices showed minimal movement and are on track for a second consecutive weekly decline as traders await US data for insights into the Federal Reserve’s future monetary policy decisions.

The precious metal remains in a sideways trend, with upside potential constrained due to uncertainty ahead of the US core PCE price index data for December. Spot gold +0.05%, silver -0.1%

ENERGY:

Oil prices edged lower, however still on track for the biggest weekly gain since October. Lower US stockpiles and expectations of increased government stimulus in

China contributed to crude breaking out of its recent range. Brent traded near $82 a barrel, having risen 3% in the previous session, and surpassing its key 200-day moving average for the first time since November. The rise in oil prices has been driven by

heightened tensions in the Middle East, with the US acting against Iran-backed Houthi rebels in Yemen and drone attacks on Russian refineries threatening crude flows amid the ongoing conflict in Ukraine. WTI -1%, Brent -0.7%, US Nat Gas +1.1%, RBOB -0.9%.

CURRENCIES:

In currency markets, the dollar weakened against most Group-of-10 currencies, and Treasury yields edged lower as traders awaited US personal consumption expenditure

data to assess the Federal Reserve’s interest-rate trajectory. USD/JPY fell as Bank of Japan board members intensify discussions about the timing of an exit from negative interest rates, potentially fueling expectations of a move in March or April. EUR/USD

remained little changed after European Central Bank President Christine Lagarde affirmed that the central bank might begin lowering rates from around mid-2024. US$ -0.3%, GBPUSD +0.2%, USDJPY -0.02%, EURUSD +0.2%, AUDUSD +0.1%, NZDUSD +0.2%, USDCHF +0.4%,

USDNOK +0.05%.

Bitcoin +3.3%, Ethereum +1.2%. Bitcoin rose past $41,000 amid a slowdown in outflows from the $20 billion Grayscale Bitcoin Trust that strategists said may help

to stanch a two-week slump in the token.

TECHNICAL LEVELS:

|

ESH24 |

10 Year Yield |

Feb Gold |

March WTI |

Spot $ Index |

|

|

Resistance |

5.000% |

2152.3 |

82.08 |

109.120 |

|

|

|

5000.00 |

4.755% |

2117.0 |

81.37 |

107.350 |

|

|

4981.00 |

4.550% |

2100.0 |

80.50 |

106.000 |

|

|

4950.00 |

4.255% |

2062.3 |

78.15 |

104.780 |

|

|

4933/34 |

4.135% |

2027.5 |

77.66 |

103.480 |

|

Settlement |

|

|

|

||

|

|

4865.00 |

4.070% |

2012.3 |

73.65 |

102.955 |

|

|

4845.00 |

3.780% |

1978.3 |

70.13 |

102.530 |

|

|

4817.00 |

3.640% |

1960.8 |

69.28 |

101.780 |

|

|

4790.00 |

3.245% |

1949.1 |

67.98 |

101.280 |

|

Support |

4746/50 |

3.000% |

1938.8 |

66.63 |

100.000 |

Colors within the report:

Green is always the 200 period (day, week).

Red is always 21,

Blue = 50,

Brown =

100 *Stars have added importance

-

Upgrades

-

American

Air (AAL) Raised to Buy at Seaport Global Securities; PT $23 -

Raised

to Outperform at Cowen; PT $21 -

Asur (ASURB

MM) ADRs Raised to Buy at Goldman; PT $326 -

Bread

Financial Holdings (BFH) Raised to Outperform at Oppenheimer -

Coinbase (COIN)

Raised to Outperform at Oppenheimer; PT $160 -

Coterra

Energy Inc (CTRA) Raised to Positive at Susquehanna; PT $30 -

GAP

Airports (GAPB MM) ADRs Raised to Buy at Goldman; PT $175 -

Health

Catalyst (HCAT) Raised to Buy at Guggenheim; PT $14 -

IBM (IBM)

Raised to Buy at President Capital Management; PT $215 -

Seagate (STX)

Raised to Buy at CFRA -

Snap (SNAP)

Raised to Buy at Deutsche Bank; PT $19 -

UMC (2303

TT) ADRs Raised to Hold at HSBC; PT $9.93 -

Vera

Therapeutics (VERA) Raised to Strong Buy at Raymond James -

Downgrades

-

Amerant

Bancorp (AMTB) Cut to Neutral at Piper Sandler; PT $25 -

Archer-Daniels-Midland (ADM)

Cut to Neutral at UBS; PT $51 -

Eagle

Bulk (EGLE) Cut to Hold at Stifel; PT $55 -

Eldorado

Gold (ELD CN) Cut to Hold at Stifel Canada; PT C$17.25 -

eXp

World Holdings (EXPI) Cut to Neutral at DA Davidson; PT $15 -

First

Bancshares/MS (FBMS) Cut to Market Perform at KBW; PT $28 -

Intel (INTC)

Cut to Hold at Summit Insights -

Karuna

Therapeutics (KRTX) Cut to Neutral at Mizuho Securities; PT $330 -

Lufax (LU)

ADRs Cut to Neutral at BofA; PT $2.80 -

Moneta

Gold Inc (ME CN) Cut to Speculative Buy at Stifel Canada; PT C$3 -

Northrop

Grumman (NOC) Cut to Sector Perform at RBC; PT $450 -

Range

Resources (RRC) Cut to Neutral at Susquehanna; PT $34 -

Southwestern

Energy (SWN) Cut to Neutral at Susquehanna; PT $6.50 -

Tidewater

Renewables (LCFS CN) Cut to Sector Perform at National Bank -

U.S.

Bancorp (USB) Cut to Neutral at Piper Sandler -

Valero

Energy (VLO) Cut to Hold at CFRA; PT $138 -

Initiations

-

Consensus

Cloud (CCSI) Rated New Neutral at BTIG -

MongoDB (MDB)

Reinstated Neutral at DA Davidson; PT $405 -

Perspective

Therapeutics (CATX) Rated New Buy at B Riley; PT $1.20 -

Recursion

Pharma (RXRX) Rated New Market Perform at Cowen -

Schrodinger (SDGR)

Rated New Outperform at Cowen; PT $42 -

Strawberry

Fields REIT (STRW) Rated New Buy at Colliers; PT $10 -

ZKH

Group (ZKH) ADRs Rated New Buy at Deutsche Bank; PT $21.30 -

ZYUS

Life Sciences Corp (ZYUS CN) Reinstated Speculative Buy at Stifel Canada; PT C$1.50

Data sources: Bloomberg, Reuters, CQG

Comments are closed