TODAY’S GAME PLAN: from the trading

desk, this is not research

DATA/HEADLINES: 8:30ET *Employment Report; 10:00ET U. of Mich. Sentiment, Factory Orders, Durable Goods Orders

HAPPY GROUNDHOG DAY

TODAY’S HIGHLIGHTS and News:

-

Punxsutawney Phil did not see his shadow today, which means he’s predicting an early spring; he and his ancestors have only been right 39% of the time

-

Fed Chairman Powell will be on 60 Minutes this Sunday to discuss inflation risks, expected rate cuts

-

The rush into tech is resembling the bubble of 1999, BofA strategists led by Michael Hartnett said

-

Mark Zuckerberg stands to receive a $700 million payout every year from Meta’s first-ever dividend

-

Visa said it blocked a record $40 billion of suspected fraud in 2023

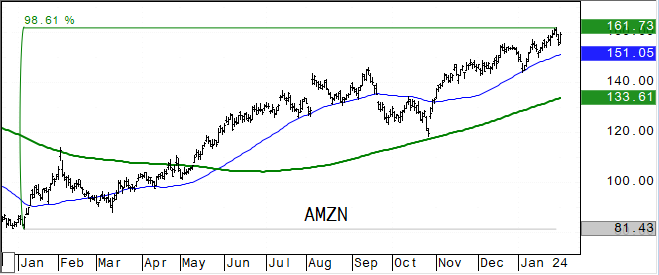

Global equities rose as bumper earnings at Amazon and Meta helped buoy world stocks ahead of key US jobs data even though China shares fell to new five-year lows,

posting their worst weekly drop in five years. Concerns over China’s economic challenges and renewed US regional bank worries, failed to put a significant dent in world stock markets, with investors taking comfort from upbeat earnings. Global equity funds

attracted a net $7.43 billion in inflows during the week to January 31, contrasting with outflows seen during the previous five weeks. Asian equity funds attracted $3.7 billion, the biggest inflow in three weeks.

EQUITIES:

US equity futures are higher after tech mega caps Meta Platforms and Amazon.com posted blowout earnings and as investors awaited a jobs report expected to support the case for interest-rate

cuts. Amazon.com jumped 6% overnight after reporting higher-than-expected holiday-quarter sales and profited from its fast-growing AI-powered cloud business. Big Oil added to the earnings buzz, with Chevron and Exxon Mobil shares rising after both beat profit

expectations. Stock buybacks are projected to increase this year after ebbing in 2023, fueled by forecasts of stronger earnings. S&P 500 companies are expected to increase earnings by 10% in 2024 after a 3% rise in 2023, according to LSEG data. Buybacks

are seen rising by at least 4% this year, according to Goldman Sachs. The S&P 500 is trading at a forward price-to-earnings ratio of 20 times, well above its long term average of 15.7 times, according to LSEG Datastream.

Futures ahead of the data: E-Mini S&P +0.7%, Nasdaq +1.1%, Russell 2000 +0.2%, DJI +0.1%

In pre-market trading, Meta soared 17% and Amazon rallied 7% after the tech behemoths smashed quarterly profit expectations. The pair’s results boosted social media and e-commerce peers,

with Snap up 5.8% and Shopify rising 3%. Meta also introduced its first ever dividend. Apple slipped over 2% after its earnings showed weakness in China. Intel fell 1% after the WSJ reported it’s delaying a $20 billion chip project planned for Ohio. Cigna

(CI) rises 4% after the health insurer earnings beat. Atlassian (TEAM) falls 8.4% as analysts said the application software company’s cloud metrics came in short of expectations. Bristol-Myers (BMY) gains 3% after forecasting 2024 profit above Wall Street

estimates. Clorox Co. (CLX) rises 11% after it raised its sales and profit forecast for the year. Skechers USA (SKX) tumbles 9.3% after the footwear company’s full-year projections fell short. Deckers Outdoor (DECK) gains 9.4% after the maker of Hoka running

shoes boosted its year profit and sales forecast. Solo Brands (DTC) falls 2.2% as JPMorgan double-downgrades the stock to its only underweight rating

European gauges advanced following strong gains on Wall Street that were fueled by better-than-expected earnings from tech companies. The Stoxx 600 index was also buoyed by positive earnings

news, with Mercedes-Benz Group AG shares rising as much as 3.3% after it reported better-than-expected industrial cash flow for last year. Danske Bank A/S climbed 7% after Denmark’s largest lender said it will buy back its stock for the first time in six years.

Delivery Hero SE slumped as much as 13% after a report that the food delivery firm’s talks to sell its Southeast Asia business to Grab collapsed. Autos and real estate stocks are leading gains, while energy lags. Germany’s DAX Index hits a new intraday record

high. Stoxx 600 +0.7%, DAX +0.8%, CAC +0.6%, FTSE 100 +0.4%. REITs +1.7%, Autos +1.6%, Retail +1.4%. Energy -0.7%, Basic Resources -0.2%.

Markets in Asia were mostly higher, led by Korean shares, while Chinese stocks slumped in their worst weekly show in years. A sense of panic gripped Chinese investors as shares swung

sharply in the final hours of trading before closing at a five-year low. The CSI 300 Index slid as much as 3.4% at one point. The Shanghai Composite ended the week down 6.2%, its largest weekly loss since October 2018, with investors disappointed by cautious

and piecemeal government stimulus measures. The MSCI Asia Pacific Index rose 0.7%, its biggest weekly gain on the year. Korean stocks posted their best week since November 2022 amid continued optimism for a regulatory push to boost valuations and corporate

governance. Kospi +2.9%, ASX 200 +1.5%, Philippines +1.3%, Thailand +1.2%, Singapore +1.2%, Sensex +0.6%, Taiwan +0.5%, Nikkei 225 +0.4%. Vietnam -0.05%, Hang Seng Index -0.2%, CSI 300 -1.2%, Shanghai Composite -1.5%.

FIXED INCOME:

Treasuries were steady after their advance Thursday that was spurred by traders pricing in a faster pace of Fed rate cuts in the wake of renewed concerns around the

health of US regional banks. January’s US payrolls report is the main event today. JPMorgan expects an upside surprise for jobs, and recommends selling five-year Treasuries, though it remains bullish on the longer-term outlook. US yields are narrowly mixed

with the curve flatter, pushing 2s10s and 5s30s spreads beyond Thursday’s lows. 10-year yields little changed around 3.88%.

METALS:

Gold steadied and is headed for its largest weekly increase since the start of December as falling Treasury yields offered support for the metal, with concerns over

US regional banks spurring traders to price in a more rapid pace of Federal Reserve interest-rate cuts. Traders will look closely at today’s US nonfarm payrolls data, which are expected to show a slowdown in new jobs added to the economy. Spot gold +0.1%,

silver -0.1%.

ENERGY:

Oil prices slipped after the OPEC+ group’s decision to keep its production policy unchanged on Thursday, and both benchmarks remained on track for weekly losses on

China demand growth fears. OPEC+ will decide in March whether or not to extend voluntary oil production cuts in place for the first quarter, two OPEC+ sources said. Oil is headed for the biggest weekly loss since early November as negotiations advance for

an agreement to pause the Israel-Hamas war. WTI -0.5%, Brent -0.4%, US Nat Gas -0.5%, RBOB -0.6%.

CURRENCIES:

Currency moves were quiet ahead of US non-farm payrolls, which probably rose 185,000 in January, less than December’s strong 216,000. The dollar inched lower against

most Group-of-10 currencies. The yen eased, while the pound extended gains as investors expect the Bank of England will take its time to cut interest rates this year. US$ Index -0.05%, GBPUSD +0.2%, EURUSD +0.1%, USDJPY +0.1%, AUDUSD +0.6%, USDCHF -0.2%.

Bitcoin +0.05%, Ethereum +0.4%.

TECHNICAL LEVELS:

|

ESH24 |

10 Year Yield |

April Gold |

March WTI |

Spot $ Index |

|

|

Resistance |

5041.00 |

4.755% |

|

85.00 |

109.120 |

|

|

5020.00 |

4.550% |

2152.3 |

83.30 |

107.350 |

|

|

5000.00 |

4.255% |

2117.0 |

81.37 |

106.000 |

|

|

4981.00 |

4.135% |

2100.0 |

80.50 |

104.780 |

|

|

4965.00 |

4.080% |

2083.2 |

79.52 |

103.535 |

|

Settlement |

4928.50 |

2071.1 |

73.82 |

||

|

|

4926.00 |

3.780% |

2041.6 |

75.47 |

102.895 |

|

|

4903.00 |

3.640% |

2028.5 |

73.58 |

102.530 |

|

|

4864.00 |

3.245% |

1979.3 |

72.13 |

101.780 |

|

|

4829.00 |

3.000% |

1960.8 |

70.19 |

101.280 |

|

Support |

4799.00 |

|

1949.1 |

69.28 |

100.000 |

Colors within the report:

Green is always the 200 period (day, week).

Red is always 21,

Blue = 50,

Brown =

100 *Stars have added importance

- Upgrades

- Allegro MicroSystems (ALGM) Raised to Outperform at Wolfe; PT $35

- CMS Energy (CMS) Raised to Buy at Guggenheim; PT $64

- Coca-Cola Femsa (KOFUBL MM) ADRs Raised to Overweight at JPMorgan; PT $102

- Corteva (CTVA) Raised to Neutral at BNPP Exane; PT $53

- Global Payments (GPN) Raised to Outperform at Evercore ISI

- Janus Henderson (JHG) Raised to Neutral at JPMorgan; PT $31

- Lundin Mining (LUN CN) Raised to Buy at Pareto Securities; PT C$13.28

- Macy’s (M) Raised to Neutral at Citi; PT $18

- Pan Global Resources (PGZ CN) Raised to Buy at Echelon Wealth

- SAP (SAP GR) ADRs Raised to Buy at Jefferies; PT $206

- Downgrades

- Alphabet (GOOGL) Cut to Accumulate at Phillip Secs; PT $154

- BCE (BCE CN) Cut to Hold at TD; PT C$55

- Bio-Techne (TECH) Cut to Hold at Stifel; PT $65

- Evans Bancorp (EVBN) Cut to Neutral at Piper Sandler

- Gold Fields (GFI SJ) ADRs Cut to Underperform at BMO; PT $12

- Guardion Health Sciences (GHSI) Cut to Hold at Maxim

- Illinois Tool (ITW) Cut to Sell at CFRA

- Lancaster Colony (LANC) Cut to Equal-Weight at Stephens

- New York Community Bancorp (NYCB) Cut to Hold at Deutsche Bank; PT $7

- Oaktree Specialty (OCSL) Cut to Market Perform at KBW; PT $19

- Solo Brands (DTC) Cut to Underweight at JPMorgan

- Starbucks (SBUX) Cut to Neutral at President Capital Management

- Tractor Supply (TSCO) Cut to Outperform at Raymond James; PT $250

- Vertex Pharmaceuticals (VRTX) Cut to Market Perform at Bernstein

- WEC Energy (WEC) Cut to Underweight at JPMorgan; PT $84

- Initiations

- Encore Energy (EU CN) Rated New Buy at B Riley; PT C$8.03

- Goeasy (GSY CN) Rated New Outperform at RBC; PT C$193

- Intel (INTC) Rated New Neutral at President Capital Management; PT $47

- Rated New Buy at Huatai Research; PT $65

- Montage Gold (MAU CN) Reinstated Buy at Stifel Canada; PT C$1.50

- Neurocrine Bio (NBIX) Rated New Buy at Dr. Kalliwoda Equity Research

- Redwire (RDW) Rated New Overweight at Cantor; PT $5

- TuSimple Holdings (TSP) Reinstated Market Perform at Cowen; PT $1.50

Data sources: Bloomberg, Reuters, CQG

Comments are closed