TODAY’S GAME PLAN: from the trading

desk, this is not research

DATA/HEADLINES 9:00ET Fed’s Perli speaks at NABE; 9:30ET Fed’s Bostic speaks; 10:00ET Wholesale Trade Sales, Inventories;

10:15ET Janet Yellen speaks; 11:00ET NY Fed 1-Yr Inflation Expectations; 1:00ET

President Biden to speak regarding Israel and Hamas, 3 Year Auction, Fed’s Waller speaks; 3:00ET Fed’s Kashkari speaks

TODAY’S HIGHLIGHTS:

- President’s brother Frank Biden speaks out following naked selfie –

Newsweek - All Israeli coalition partners agree to the possible formation of a national unity government

- The Powerball jackpot climbed to an estimated $1.75B

Global shares rallied after dovish comments by Federal Reserve officials and the prospect of more economic stimulus by China brought some risk appetite back to markets,

but violence in the Middle East made for nervous trading. The conflict between Israel and Hamas entered its fourth day, with at least 1,500 fatalities so far. Overnight, Israel struck the Gaza Strip and called up an unprecedented 300,000 reservists as it

prepares for the next phase of its retaliation. The US said security assistance and aid is on the way. The European Union asked Israel and Palestinian foreign ministers to attend an emergency meeting of EU ministers today. Meanwhile, the International Monetary

Fund cut its growth forecasts for China and the euro area and said overall global growth remained low and uneven despite what it called the “remarkable strength” of the US economy. The IMF raised its 2023 output growth estimate for Latin America and the Caribbean

to 2.3% from July’s 1.9% due to faster expected growth in Brazil and Mexico. The MSCI All-World index rose for a fifth day, up 0.5%.

EQUITIES:

US equity futures have pared gains made after Federal Reserve officials signaled the recent yield surge could justify caution on interest rates. An escalation of tensions in the Middle

East, however, remains a risk for markets, with Israel mobilizing its military forces near Gaza, and questions being asked about Iran’s role in the bloody incursion. Another risk for US stocks may come from fiscal policy constraints at a time when the Fed

is still fighting high inflation, according to Morgan Stanley’s Michael Wilson. In other news, GM workers in Canada are going on strike after contract talks failed.

Futures ahead of the bell: E-Mini S&P +0.05%, Nasdaq +0.05%, Russell 2000 -0.1%, Dow +0.1%.

In pre-market trading, PepsiCo rose 3% on a core EPS beat and higher full-year outlook. Akero Therapeutics (AKRO) plunges 63% after study results from a mid-stage trial of its liver disease

drug disappointed. Coherent (COHR) gains over 9% after confirming that Denso and Mitsubishi Electric agreed to invest an aggregate $1 billion in its silicon carbide business. Corning (GLW) is down 2.5% after being downgraded to neutral from overweight at JPMorgan.

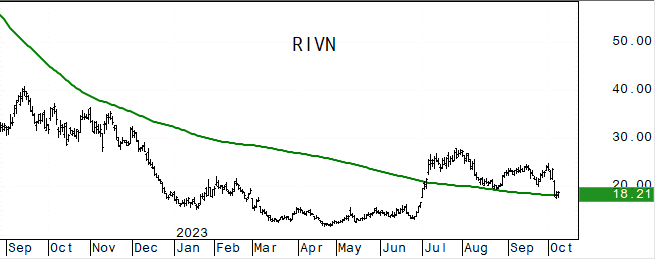

Hyatt Hotels (H) rises as much as 6% after the hotel chain was named by S&P Dow Jones Indices to replace National Instruments Corp. in the S&P MidCap 400 Index, effective Thursday. Rivian Automotive (RIVN) rises 3.5% as UBS upgrades the electric-vehicle startup

to buy from neutral. US-listed Chinese stocks gain after Bloomberg News reported that Beijing is preparing to unleash a new round of stimulus measures.

The Stoxx Europe 600 index climbed 1.5%, heading for its best day this year, with all industry sectors in the green. Miners led the advance as copper and nickel prices rose after Bloomberg

reported that China is preparing to unleash a new round of measures to support its economy. Anglo American Plc advanced more than 5%, while Glencore Plc, Rio Tinto Plc and ArcelorMittal added more than 3% each. Carmakers rose the most in four months, led by

Volvo Car AB-B. Bank of America strategists see nearly 15% downside to earnings-per-share projections for the next 12 months in Europe, as the boost from banks and energy companies fades and the global economy slows further. DAX +1.4%, CAC +1.3%, FTSE 100

+1.5%. Travel & Leisure +2.25%, Basic Resources +2.25%, Autos +2%, Utilities +2%.

Shares in Asia had their biggest daily gain since July. The MSCI Asia Pacific Index climbed 1.2%, with all sub-sectors except real estate in the green. Japanese benchmarks led gains in

the region after returning from holiday. Mainland Chinese stocks fell amid concerns about the strength of economic recovery. China’s largest private property developer Country Garden Holdings warned that it might not be able to meet all of its offshore payment

obligations. China is considering raising its budget deficit for 2023 to help the economy meet the government’s annual growth target. Taiwan’s market was closed for a holiday. Nikkei 225 +2.4%, Hang Seng Tech +1.3%, Singapore +1%, ASX 200 +1%, Sensex +0.9%,

Hang Seng Index +0.8%, Vietnam +0.6%. Kospi -0.25%, China’s CSI 300 -0.75%.

FIXED INCOME:

Treasuries jumped, catching up with Monday’s global government bond rally, when cash trading in the US was closed for a holiday. The yield on the policy-sensitive

two-year Treasury dropped by the most since the end of August, while the benchmark 10-year had its best day since March. Meanwhile, there’s been a clear change of tone from Fed officials regarding interest rates. Fed Vice Chair Philip Jefferson said officials

could “proceed carefully” following the recent rise in Treasury yields, and Fed Bank of Dallas President Lorie Logan said the surge in long-term rates may mean less need for further tightening. Another slate of Fed speakers today may add to the picture. In

Europe, ECB’s Villeroy indicated “interest rates are at a good level and not desirable to hike rates further.” US yields remain lower after paring some of their gap lower move, with 10 year yield ~4.7%, down 9 bps. Treasury auction cycle begins with $46b

3-year note sale, followed by 10- and 30-year reopenings Wednesday and Thursday.

METALS:

Gold dipped slightly as ongoing conflicts in the Middle East continued to disrupt markets. Investors were also contemplating whether the era of tightening financial conditions might be

reaching its peak, spurred by dovish comments from Federal Reserve officials. The IMF boosted its global inflation forecast for next year to 5.8% from the 5.2% predicted three months ago. In most countries, the institution sees CPI remaining above central

bank targets until 2025. Gold -0.3%, silver -0.7%.

ENERGY:

Oil prices eased after surging the most in more than six months yesterday, with traders cautious as they watched for potential supply disruptions amid military clashes

between Israel and Hamas. Reports of Iran’s involvement are being investigated globally, which if true would likely provide another boost to prices. While Israel produces very little crude oil, markets worried that if the conflict escalates it could hurt Middle

East supply and worsen an expected deficit for the rest of the year. In a more positive sign for supply, Venezuela and the US have progressed in talks that could provide sanctions relief. The IMF lifted its global inflation forecast for next year and called

for central banks to keep policy tight until there’s a durable easing in price pressures. WTI -0.15%, Brent -0.2%, US Nat Gas +1%, RBOB +0.7%.

CURRENCIES:

In currency markets, the dollar is slightly lower, after reversing intraday losses as traders braced for another day of tension due to the Israel-Hamas conflict.

Attention will then shift to upcoming events like the release of the Federal Reserve minutes and US CPI data later in the week. Norway’s krone leads losses among Group-of-10 peers after data showed that the country’s inflation slowed more than expected last

month. USDJPY briefly erased gains after a Kyodo report that the Bank of Japan is considering raising its fiscal 2023 price outlook to near 3% from the 2.5% it announced in July. US$ Index -0.05%, GBPUSD +0.1%, EURUSD +0.1%, USDJPY +0.4%, AUDUSD -0.25%, USDNOK

+0.7%.

Bitcoin -0.2%, Ethereum +0.3%.

TECHNICAL LEVELS:

|

ESZ23 |

10 Year Yield |

Dec Gold |

Nov WTI |

Spot $ Index |

|

|

Resistance |

4515.00 |

|

1981/85 |

95.03 |

111.525 |

|

|

4482.00 |

5.500% |

1937.5 |

92.13 |

110.000 |

|

|

4446.00 |

5.325% |

1923.5 |

89.86 |

108.970 |

|

|

4407.00 |

5.000% |

1900.0 |

88.30 |

107.990 |

|

|

4388.00 |

4.885% |

1882.0 |

87.25 |

107.350 |

|

Settlement |

4368.75 |

1864.3 |

86.38 |

||

|

|

4358.50 |

4.700% |

1856.7 |

84.57 |

106.050tl |

|

|

4322.00 |

4.500% |

1844.0 |

83.70 |

104.420 |

|

|

4305.00 |

4.300% |

1821.0 |

81.50 |

103.800 |

|

|

4289.00 |

4.000% |

1800.0 |

77.62 |

103.180 |

|

Support |

4235.00 |

3.800% |

1796.7* |

76.03 |

102.920 |

Colors within the report:

Green is always the 200 period (day, week).

Red is always 21,

Blue = 50,

Brown =

100 *Stars have added importance

- Upgrades

- (ABCB) Ameris Bancorp Raised to Buy at DA Davidson; PT $44

- (ACAD) Acadia Pharma Raised to Overweight at JPMorgan; PT $32

- (BZH) Beazer Homes Raised to Outperform at Wedbush; PT $32

- (EA) Electronic Arts Raised to Buy at BofA

- (EXAS) Exact Sciences Raised to Overweight at Piper Sandler; PT $90

- (MEG CN) MEG Energy Raised to Outperform at RBC; PT C$31

- (MTL CN) Mullen Group Raised to Buy at TD; PT C$18.50

- (OHI) Omega Healthcare Raised to Buy at BofA; PT $36

- (PNFP) Pinnacle Financial Raised to Hold at Jefferies; PT $71

- (RIVN) Rivian Raised to Buy at UBS; PT $24

- (SBRA) Sabra Health Raised to Buy at BofA

- (SJ CN) Stella-Jones Raised to Outperform at National Bank; PT C$83

- Downgrades

- (GLW) Corning Cut to Neutral at JPMorgan

- (JNPR) Juniper Cut to Neutral at JPMorgan; PT $29

- (MRTX) Mirati Therapeutics Cut to Market Perform at Cowen

- (MRTX) Cut to Neutral at Piper Sandler; PT $58

- (NTST) Netstreit Cut to Underperform at BofA

- (O) Realty Income Cut to Neutral at BofA; PT $52

- (QRVO) Qorvo Cut to Sell at Citi

- (SPLK) Splunk Cut to Neutral at Daiwa; PT $157

- (SRC) Spirit Realty Cut to Underperform at BofA

- (STWD) Starwood Property Cut to Market Perform at KBW; PT $20

- (SWKS) Skyworks Cut to Sell at Citi; PT $87

- Initiations

- (AAP) Advance Auto Rated New Market Perform at Cowen; PT $55

- (ARM) ARM Holdings PLC ADRs Rated New Buy at Daiwa; PT $63

- (ARM) ADRs Rated New Outperform at Oddo BHF; PT $70

- (AZO) AutoZone Rated New Outperform at Cowen; PT $2,975

- (BXSL) Blackstone Secured Lending Fund Rated New Buy at Truist Secs

- (COTY) Coty Rated New Hold at Kepler Cheuvreux; PT $11.66

- (DG) Dollar General Rated New Neutral at BNPP Exane; PT $116

- (DLTR) Dollar Tree Rated New Outperform at BNPP Exane; PT $139

- (ELS) Equity LifeStyle Rated New Neutral at Compass Point; PT $65

- (MDB) MongoDB Rated New Sector Perform at Scotiabank; PT $335

- (MNKD) MannKind Rated New Outperform at Wedbush; PT $10

- (NMRA) Neumora Therapeutics Rated New Buy at BofA; PT $18

- (NMRA) Rated New Outperform at William Blair

- (NMRA) Rated New Outperform at RBC; PT $24

- (NMRA) Rated New Overweight at JPMorgan; PT $21

- (NMRA) Rated New Buy at Stifel; PT $26

- (NMRA) Rated New Buy at Guggenheim; PT $22

- (NTRS) Northern Trust Reinstated Buy at BofA; PT $90

- (ORLY) O’Reilly Automotive Rated New Outperform at Cowen; PT $1,100

- (RYZB) RayzeBio Rated New Buy at Truist Secs; PT $29

- (RYZB) Rated New Buy at Jefferies; PT $35

- (RYZB) Rated New Overweight at JPMorgan; PT $30

- (SCR CN) Strathcona Resources Rated New Sector Perform at RBC; PT C$35

- (SUI) Sun Communities Rated New Neutral at Compass Point; PT $125

- (VFS) Vinfast Auto Ltd Rated New Buy at Chardan Capital Markets

- (ZURA) Zura Bio Rated New Buy at Ladenburg Thalmann; PT $10

Data sources: Bloomberg, Reuters, CQG

No responses yet