TODAY’S GAME PLAN: from the trading

desk, this is not research

DATA/HEADLINES 8:30ET 10:30ET Fed’s Harker speaks; 4:30ET Fed’s Harker speaks

TODAY’S HIGHLIGHTS:

- Iran’s Foreign Ministry says that Hamas is potentially ready to release the nearly 200 hostages if Israel

stops its airstrikes on the Gaza Strip - Iran said Palestinian militants have the means to fight long term

- Egypt says that Israel is not cooperating with delivery of aid into Gaza

- Suzanne Somers, known for playing Chrissy on Three’s Company, died at 76

Global markets were broadly calmer today after last week’s rush into haven assets, as investors await further developments in the Middle East. US officials rushed

to speak with Middle Eastern nations, including back-channel talks with Iran to contain the violence. US Secretary of State Antony Blinken landed back in Tel Aviv, after meeting Arab leaders to discuss the conflict and efforts to provide humanitarian assistance

to people in Gaza. Iran warned on Saturday that if Israel’s “war crimes and genocide” were not stopped then the situation could spiral out of control with “far-reaching consequences.” Meanwhile, headwinds in China’s markets are growing. The US said it will

tighten sweeping measures that restrict China’s access to advanced semi-conductors and chip-making gear in a bid to prevent it from getting a military edge. Key updates on the state of the global economy due this week include Chinese growth figures and inflation

readings in Japan, the UK and the euro zone.

EQUITIES:

US equity futures nudged higher, and Treasuries dropped as caution prevailed amid diplomatic efforts to contain the Israel-Hamas conflict, just as the latest earnings reporting season

gets into full swing. Wall Street strategists warned that the outlook for corporate profits is weakening. Morgan Stanley’s Michael Wilson said earnings revisions breadth for the S&P 500 has fallen sharply over the past couple of weeks. Citigroup’s index of

earnings revisions shows downgrades have outpaced upgrades for four straight weeks ahead of the reporting season. Democrats are said to be holding informal talks with Republicans about a potential bipartisan solution to finding a House speaker. The House

GOP nominated Jim Jordan, and a vote is planned for tomorrow.

Futures ahead of the data: E-Mini S&P %, Nasdaq %, Russell 2000 %, Dow %.

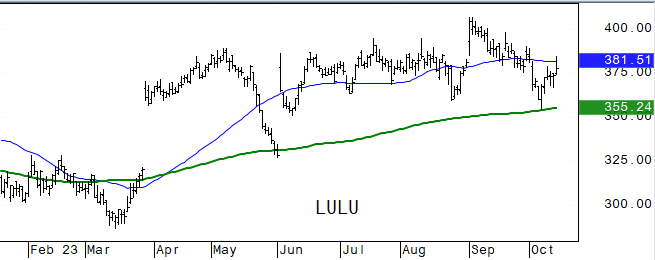

In pre-market trading, Lululemon (LULU) advances 4.6% putting the athletic-apparel brand on track for a seventh-straight day of gains, after S&P Dow Jones Indices announced on Friday

that the company would replace Activision Blizzard in the S&P 500. Pfizer fell 2.5% after the pharmaceutical giant slashed its revenue and earnings forecasts and agreed to take back nearly 8 million Paxlovid doses from the US government. Apple dropped 1%

after a study pointed to disappointing sales of the new iPhone. Manchester United slumped as much as 22% after a report that a Qatari group of investors had withdrawn its bid to buy the English football club. Ambrx Biopharma (AMAM) jumps as much as 47% after

the firm released data abstract from a trial of its investigational drug for prostate cancer. Enphase Energy (ENPH) drops as much as 2.2% after BMO Capital Markets downgrades the solar energy equipment maker to market perform from outperform. coverage on

the online grocery delivery firm with buy-equivalent recommendations. Novavax (NVAX) falls as much as 4.7% after the Financial Times reported that EU regulators have delayed a decision to approve the company’s revised Covid-19 vaccine.

European gauges steadied after last week’s volatility at the start of the Israel-Hamas conflict. Germany’s GDP declined 0.2% in the quarter and is seen contracting 0.1% in the final three

months of the year. Energy stocks were boosted by recent gains in oil prices, with Shell Plc hitting a record high. Technology shares underperform in Europe after Bloomberg News reported that the US is considering further restrictions to curb China’s access

to advanced semiconductors. Telecom Italia SpA fell over 5% after saying it received a binding offer for its phone network, without disclosing details of a price. Polish equities jumped the most since May 2022 as a bloc of pro-European opposition parties appeared

on track to unseat the nationalist government. Stoxx 600 +0.2%, DAX +0.1%, CAC +0.15%, FTSE 100 +0.3%. Basic Resources +1.3%, Retail +1%, Banks +1%, Energy +0.8%. Technology -0.2%.

Asian shares declined as a selloff in the region’s semiconductor stocks weighed on sentiment already hit by the conflict in the Middle East. The MSCI Asia Pacific Index fell nearly1%,

with Taiwan Semiconductor and Samsung among the biggest drags. A gauge of the region’s chipmakers slid 2% after a Bloomberg News report that the US is considering further restrictions to curb China’s access to advance semiconductors. Continued weakness in

China’s property shares saw the mainland and Hong Kong benchmarks end lower. Equities dropped in mainland China despite the central bank making the biggest medium-term liquidity injection since 2020. Thailand stocks were among the worst performers in the region

after a selloff in the nation’s property stocks, which fell to their lowest level in 15 months. Nikkei 225 -2%, Thailand’s SET -1.6%, Vietnam -1.1%, Philippines -1%, CSI 300 -1%, Hang Seng Index -1%, Kospi -0.8%, ASX 200 -0.3%, Sensex -0.2%.

FIXED INCOME:

Treasuries are lower, led by the long end as flight-to-quality bid eases. US yields are cheaper by 1.5bp-10bp across the curve with long-end-led losses steepening

2s10s, 5s30s spreads by ~7bp and ~5bp on the day. 10-year yield rises ~7bps, clawing back some of last week’s 19 basis-point drop and 30-year yields are up 10bp on the day. Beyond Middle East conflict, focal points this week include a packed Fed speaker slate

headed by Chair Powell at the Economic Club of New York on Thursday.

METALS:

Gold slipped, following the biggest daily advance in seven months on Friday. Metal prices are heading for more turbulence in the coming 12 months as global demand falters, Citi said after

gauging the mood at the annual LME Week. Spot gold -0.8%, silver -0.6%.

ENERGY:

Crude oil nudged lower after climbing nearly 6% on Friday, as investors waited to see if the Israel-Hamas conflict draws in other countries. Oil rose sharply on Friday,

with traders appearing reluctant to hold short positions ahead of the weekend as Israel prepared for an expected ground incursion into Gaza. Fears the Israel-Hamas war could spill over, perhaps involving Iran and threatening supplies from the Mideast saw traders

rebuild a risk premium after an initial spike last Monday was mostly erased in subsequent sessions. WTI -0.2%, Brent -0.3%, US Nat Gas -3%, RBOB +0.2%.

CURRENCIES:

The dollar slipped, while New Zealand’s dollar led gains in the Group-of-10 currencies after the opposition National Party won the general election. Israel’s shekel

fell to its weakest level since 2015. The zloty outperformed most other currencies as Poland’s pro-European opposition parties headed for an election majority, raising hopes of pro-market policies and access to EU recovery funds. Zloty gains as much as 1.8%

against euro, before trimming gains TO 1.2%. US$ Index -0.2%, GBPUSD +0.3%, EURUSD +0.3%, USDJPY -0.1%, AUDUSD +0.5%, NZDUSD +0.6%, USDSEK -1%.

Bitcoin +2%, Ethereum +1.2%. Crypto stocks gain pre-market as Bitcoin touches one week highs.

TECHNICAL LEVELS:

|

ESZ23 |

10 Year Yield |

Dec Gold |

Nov WTI |

Spot $ Index |

|

|

Resistance |

4461.00 |

5.750% |

2029.0 |

95.03 |

110.000 |

|

|

4431.00 |

5.500% |

2010.9 |

93.10 |

108.970 |

|

|

4407.00 |

5.325% |

2000.0 |

92.13 |

107.990 |

|

|

4396.00 |

5.000% |

1981/85 |

89.86 |

107.350 |

|

|

4375.00 |

4.885% |

1976.5 |

88.30 |

106.175 |

|

Settlement |

4357.25 |

1941.5 |

87.69 |

||

|

|

4333.00 |

4.500% |

1939.6 |

85.40 |

105.535 |

|

|

4310.00 |

4.350% |

1897/98 |

83.92 |

104.725 |

|

|

4277.00 |

4.000% |

1869.5 |

81.50 |

104.380* |

|

|

4246.00 |

3.835% |

1821/23 |

79.35 |

103.800 |

|

Support |

4235.00 |

3.500% |

1800.0 |

77.75 |

103.180 |

Colors within the report:

Green is always the 200 period (day, week).

Red is always 21,

Blue = 50,

Brown =

100 *Stars have added importance

- Upgrades

- (ALHC) Alignment Healthcare Raised to Strong Buy at Raymond James

- (ALSN) Allison Transmission Raised to Neutral at JPMorgan; PT $70

- (AOI CN) Africa Oil Raised to Buy at SpareBank; PT C$3.72

- (AR) Antero Resources Raised to Buy at SWS; PT $35

- (CHKP) Check Point Software Raised to Equal-Weight at Morgan Stanley

- (CL) Colgate-Palmolive Raised to Buy at Stifel; PT $81

- (CPK) Chesapeake Utilities Raised to Equal-Weight at Wells Fargo

- (DHI) D.R. Horton Raised to Buy at Goldman; PT $131

- (EH) EHang Holdings ADRs Raised to Buy at Goldman; PT $30.50

- (EMBR3 BZ) Embraer ADRs Raised to Buy at Citi; PT $16

- (GBX) Greenbrier Raised to Positive at Susquehanna; PT $50

- (LNT) Alliant Energy Raised to Sector Outperform at Scotiabank; PT $59

- (LPG) Dorian LPG Raised to Buy at Pareto Securities; PT $35

- (NICE IT) Nice Ltd ADRs Raised to Overweight at Morgan Stanley; PT $220

- (NUE) Nucor Raised to Neutral at JPMorgan; PT $151

- (PFE) Pfizer Raised to Buy at Jefferies; PT $39

- (PTEN) Patterson-UTI Raised to Buy at BofA; PT $16

- (SBRA) Sabra Health Raised to Equal-Weight at Wells Fargo; PT $15

- (SO) Southern Co Raised to Sector Outperform at Scotiabank; PT $78

- (TAL) Tal Education ADRs Raised to Buy at UBS; PT $11.60

- (TRN) Trinity Industries Raised to Positive at Susquehanna; PT $32

- (UNH) UnitedHealth Raised to Buy at UBS; PT $640

- (VRNS) Varonis Systems Raised to Overweight at Morgan Stanley; PT $39

- (W) Wayfair Raised to Hold at Loop Capital

- Downgrades

- (BCC) Boise Cascade Cut to Underperform at BofA

- (BNTX) BioNTech ADRs Cut to Hold at HSBC; PT $111

- (CCI) Crown Castle Cut to Sector Perform at RBC; PT $100

- (CHK) Chesapeake Energy Cut to Hold at SWS; PT $99

- (CMI) Cummins Cut to Underweight at JPMorgan; PT $255

- (D) Dominion Energy Cut to Sector Perform at Scotiabank; PT $46

- (ENPH) Enphase Energy Cut to Market Perform at BMO; PT $148

- (ES) Eversource Cut to Sector Perform at Scotiabank; PT $60

- (JD) JD.com ADRs Cut to Market Perform at Bernstein; PT $31

- (KBH) KB Home Cut to Neutral at Goldman; PT $48

- (MAXN) Maxeon Solar Cut to Neutral at BofA

- (MPW) Medical Properties Cut to Underweight at Wells Fargo; PT $4

- (O) Realty Income Cut to Sector Perform at Scotiabank; PT $54

- (PXD) Pioneer Natural Cut to Market Perform at BMO; PT $267

- (TWNK) Hostess Brands Cut to Neutral at Citi; PT $34

- (WHD) Cactus Cut to Underperform at BofA

- Initiations

- (AMX CN) Amex Exploration Rated New Outperform at National Bank

- (BAP) Credicorp Rated New Buy at Jefferies; PT $161.20

- (BBDC4 BZ) Bradesco ADRs Rated New Buy at Jefferies; PT $3.50

- (BCOLO CB) Bancolombia ADRs Rated New Hold at Jefferies; PT $28.60

- (BLX) Bladex Rated New Buy at Jefferies; PT $37

- (BSAN CI) Santander Chile ADRs Rated New Hold at Jefferies; PT $18.90

- (CART) Instacart Rated New Overweight at JPMorgan; PT $33

- (CART) Rated New Market Outperform at JMP; PT $33

- (CART) Rated New Buy at Citi; PT $34

- (CART) Rated New Buy at Stifel; PT $48

- (CART) Rated New Overweight at Barclays; PT $40

- (CART) Rated New Neutral at Wedbush; PT $28

- (CART) Rated New Buy at Goldman; PT $48

- (CART) Rated New Overweight at Piper Sandler; PT $36

- (CART) Rated New Outperform at Oppenheimer; PT $36

- (CHILE CI) Banco de Chile ADRs Rated New Hold at Jefferies; PT $21

- (GCT) GigaCloud Technology Rated New Buy at CMB International

- (HLF CN) High Liner Foods Reinstated Market Perform at BMO; PT C$12

- (IFS) Intercorp Finl Rated New Buy at Jefferies; PT $34.90

- (ITUB4 BZ) Itau ADRs Rated New Hold at Jefferies; PT $6.10

- (KVYO) Klaviyo Rated New Buy at Mizuho Securities; PT $40

- (KVYO) Rated New Outperform at Cowen; PT $42

- (KVYO) Rated New Buy at Canaccord; PT $37

- (KVYO) Rated New Buy at Needham; PT $40

- (KVYO) Rated New Outperform at William Blair

- (KVYO) Rated New Outperform at Baird; PT $40

- (KVYO) Rated New Equal-Weight at Morgan Stanley; PT $38

- (KVYO) Rated New Equal-Weight at Barclays; PT $37

- (KVYO) Rated New Neutral at Citi; PT $38

- (KVYO) Rated New Buy at Truist Secs; PT $42

- (KVYO) Rated New Neutral at Goldman; PT $36

- (KVYO) Rated New Overweight at Piper Sandler; PT $38

- (LNGE CN) LNG Energy Group Rated New Buy at Canaccord; PT C$1

- (ME CN) Moneta Gold Inc Rated New Outperform at National Bank; PT C$3

- (NFG CN) New Found Gold Rated New Outperform at National Bank; PT C$8.50

- (NU) Nubank Rated New Buy at Jefferies; PT $10.80

- (NXT) NEXTracker Rated New Buy at Janney Montgomery; PT $43

- (PRTHU) Priority Technology Hold Rated New Market Perform at KBW

- (RADL3 BZ) Raia Drogasil ADRs Rated New Buy at Jefferies; PT $6.60

- (SAN SM) Santander Brasil ADRs Rated New Hold at Jefferies; PT $5.70

- (VSTS) Vestis Rated New Overweight at JPMorgan; PT $20

- (VTS) Vitesse Energy Rated New Buy at Roth MKM; PT $30.50

- (ZYXI) Zynex Rated New Outperform at RBC; PT $13

Data sources: Bloomberg, Reuters, CQG

No responses yet