TODAY’S GAME PLAN: from the trading

desk, this is not research

DATA/HEADLINES 8:30ET Philadelphia Fed Non-Manufacturing Activity; 9:45ET S&P Global US Manufacturing PMI; 10:00ET

Richmond Fed Manufacturing Index; 1:00ET 2-year auction

TODAY’S HIGHLIGHTS:

- “We have to deport people more often and faster” – German Prime Minister Olaf Scholz

- Intelligence shows Iranian-backed militias are ready to ramp up attacks against US forces in the Middle East

– CNN

Global stocks steadied on Tuesday as a flicker of investor risk appetite lifted equities and commodities, although trading was cautious given the war in the Middle

East. Israel’s military, meanwhile, said there are “long weeks of fighting ahead,” though it wouldn’t say if a ground invasion of Gaza is imminent. There are growing calls in Israel to rethink the scope of any such action, amid concern over the fate of hostages

and the threat of a full-on Hezbollah attack from the north. Monthly surveys of business activity showed a decline in the euro zone and the UK in early October, ahead of a separate report due out later for the United States.

EQUITIES:

US equity futures rebounded as investors await key tech earnings. Investor attention will be split this week between the earnings of high-profile companies, such

as Microsoft, Meta Platforms and Amazon, as well as a slew of economic data ahead of the Fed’s meeting from Oct. 31 to Nov. 1. Third-quarter gross domestic product on Thursday, along with the Personal Consumption Expenditures (PCE) report, the Fed’s preferred

inflation gauge, on Friday, could help shape medium-term expectations for US rates. Verizon +1.8%, reported strong 3Q results momentum, raises free cash flow guidance. Coca Cola +1.6%, EPS $0.74 Beats $0.65 Estimate, Revenues $12.00B Beat $10.79B Estimate.

Cadence Design Systems (CDNS) shares fell 3.3% pre-bell after the computer software firm provided a downbeat earnings outlook for the current three-month period. Logitech International

(LOGI) jumped 9.5% as the computer products manufacturer lifted its fiscal 2024 sales outlook. Several other pre-market movers included Agilysys, Arm, Cleveland-Cliffs, Coinbase, Li-Cycle Holdings and Redfin.

Futures ahead of the bell: E-Mini S&P +0.6%, Nasdaq +0.7%, Russell 2000 +0.8%, Dow +0.4%.

European shares edged higher ,with the banking sector weighing on the FTSE 100. Barclays fell 6.8% as it hinted at major cost-cutting and warned of increased competition

for savers’ money. Lloyds and NatWest also saw declines, dragging down the banking sector. Economic concerns were exacerbated by a Eurozone Composite Purchasing Managers’ Index at a near three-year low and a fourth straight month of business activity contraction

in Germany, raising fears of a recession. Investors do not expect the European Central Bank to raise interest rates when it meets this week but are still prepared for borrowing costs to remain high for a long time. Hermes, Puma, and Logitech International

saw stock increases due to strong performance, while miners benefited from higher base metal prices. On the downside, IT services firm Softcat’s shares slumped due to decreased full-year revenue, and industrial firms like Bunzl saw declines after warning of

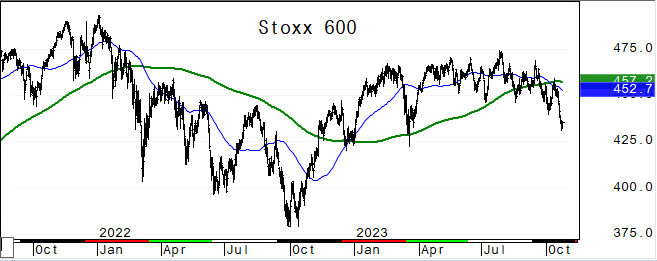

a drop in full-year revenue. Stoxx 600 +0.2%, DAX +0.3%, CAC +0.6%, FTSE 100 -0.05%.

Asian stocks reversed early losses as bond yields dropped, while most Chinese gauges rose after the nation’s sovereign wealth fund bought exchange-traded funds to shore up prices. Xi

Jinping made his first known visit to the nation’s central bank since he became Chinese president a decade ago, underscoring the government’s increased focus on shoring up the economy and financial markets. The MSCI Asia Pacific Index climbed 0.2% to end a

four-day slide that took it to an 11-month low. Benchmarks in Japan, South Korea and Taiwan finished higher, while Hong Kong’s Hang Seng Index fell to its lowest level since last November as trading resumed after a holiday. India was closed for a holiday.

Vietnam +1.1%, Kospi +1.1%, Singapore +1%, Indonesia +1%, Shanghai Composite +0.8%, CSI 300 +0.4%, Taiwan +0.35%, Nikkei 225 +0.2%. Hang Seng Index -1%, Philippines -0.8%, Thailand -0.6%.

FIXED INCOME:

Treasury 10-year yields slipped as much as five basis points to a one-week low after reaching the highest since 2007 yesterday. Treasuries are recovering after some of the market’s most

prominent bears warned of an economic slowdown, stoking bets the declines have overshot and that the Federal Reserve will need to lower interest rates. Billionaire investor Bill Ackman wrote in a social media post Monday that he unwound his bet against US

government bonds amid rising global risks, while Bill Gross wrote that he’s buying short-dated interest-rate futures in anticipation of a recession by year-end.

METALS:

Gold prices have fallen slightly from a five-month high due to several factors, including a surge in Treasury yields, which makes gold, a non-interest-bearing asset,

less attractive. The market is also closely watching US economic data and Federal Reserve Chairman Jerome Powell’s upcoming speech for indications on monetary policy. Gold -0.7%. Silver -0.8%.

ENERGY:

Oil prices recovered some of the previous day’s losses as markets worried that the Israel-Hamas war could escalate into a wider conflict in the oil-exporting region.

Brent crude snapped two days of losses to climb above $90 per barrel. There are growing calls in Israel to rethink the scope of any ground invasion of Gaza as talks to free hostages taken by Hamas intensified and French President Macron becomes the latest

world leader to visit. WTI +0.4%, Crude +0.4%.

CURRENCIES:

In the currency market, the dollar edged higher against a basket of currencies, after Monday’s 0.5% drop. The euro swung to a loss against the dollar as data showed

the French and German economies struggling. USD/JPY dropped as much as 0.3% to a one-week low of 149.32. The Bank of Japan announced unscheduled bond-purchase operations to curb the recent increase in bond yields. AUD/USD rallied as much as 0.7% to a day high

as leveraged funds bought the Aussie before a speech by Reserve Bank Governor Bullock. US$ Index +0.4%. GBPUSD -0.2%, USDJPY +0.1%, EURUSD -0.4%, AUDUSD flat & NZDUSD flat.

Bitcoin +9%, Ethereum +7%. Bitcoin hit the highest level since May 2022 as the possible approval in the coming weeks of the first US spot Bitcoin ETFs stoked appetite.

TECHNICAL LEVELS:

|

ESZ23 |

10 Year Yield |

Dec Gold |

Dec WTI |

Spot $ Index |

|

|

Resistance |

4384.00 |

|

2100.0 |

95.03 |

110.000 |

|

|

4348.00 |

5.750% |

2081.0 |

93.10 |

108.970 |

|

|

4322.00 |

5.500% |

2056.0 |

92.13 |

107.990 |

|

|

4285.00 |

5.325% |

2028.6 |

89.85 |

107.350 |

|

|

4262.00 |

5.000% |

2012.7 |

88.13 |

106.785 |

|

Settlement |

4241.75 |

1987.8 |

85.49 |

||

|

|

4235.50 |

4.800% |

1956.0 |

84.70 |

105.200 |

|

|

4216.00 |

4.455% |

1943.0 |

81.50 |

104.380* |

|

|

4202.00* |

3.925% |

1921.2 |

79.35 |

103.800 |

|

|

4185.00 |

3.870% |

1894.0 |

78.02 |

103.330 |

|

Support |

4150.00 |

3.500% |

1863.0 |

75.63 |

|

Colors within the report:

Green is always the 200 period (day, week).

Red is always 21,

Blue = 50,

Brown =

100 *Stars have added importance

Upgrades

(ARE CN) Aecon Group Raised to Buy at Canaccord; PT C$14

(AXP) American Express Raised to Neutral at Piper Sandler; PT $151

(BLDP CN) Ballard Power Systems Raised to Buy at HSBC; PT C$6.15

(BRZE) Braze Raised to Buy at DA Davidson

(EDIT) Editas Raised to Buy at Citi; PT $11

(ERO CN) ERO Copper Raised to Buy at Paradigm Capital; PT C$30

(FM CN) First Quantum Minerals Raised to Buy at Paradigm Capital

(GEI CN) Gibson Energy Raised to Sector Outperform at Scotiabank; PT C$25

(IR) Ingersoll Rand Raised to Buy at Stifel; PT $73

(IVN CN) Ivanhoe Mines Raised to Buy at Paradigm Capital; PT C$15

(LUN CN) Lundin Mining Raised to Buy at Paradigm Capital; PT C$12.50

(MEDP) Medpace Holdings Raised to Outperform at Baird; PT $289

(SILK) Silk Road Medical Raised to Peerperform at Wolfe

Downgrades

(CUBE) CubeSmart Cut to Equal-Weight at Wells Fargo; PT $37

(ENPH) Enphase Energy Cut to Neutral at Daiwa; PT $100

(ESMT) EngageSmart Cut to Market Perform at Raymond James

(ESMT) Cut to Hold at Needham

(ESMT) Cut to Sector Weight at KeyBanc

(FMC) FMC Corp Cut to Equal-Weight at Morgan Stanley; PT $70

(FMC) Cut to Neutral at Goldman; PT $59

(FMC) Cut to Neutral at BofA; PT $63

(GATO) Gatos Silver Cut to Hold at Canaccord; PT $5.50

(HES) Hess Cut to Equal-Weight at Wells Fargo; PT $171

(LICY) Li-Cycle Cut to Hold at Cantor; PT $3

(MKFG) Markforged Holding Cut to Market Perform at William Blair

(MNST) Monster Beverage Cut to Neutral at Piper Sandler; PT $50

(OKTA) Okta Cut to Neutral at President Capital Management; PT $78

(PNT) Point Biopharma Cut to Neutral at Piper Sandler; PT $12.50

(RF) Regions Financial Cut to Neutral at UBS; PT $15

(SEE) Sealed Air Cut to Market Perform at William Blair

(TNT-U CN) TRUE North Commercial Cut to Underperform at National Bank

Initiations

(AIRC) Apartment Income REIT Rated New Outperform at Raymond James

(AMZN) Amazon Rated New Buy at Seaport Global Securities; PT $145

(ANL) Adlai Nortye ADRs Rated New Overweight at Cantor; PT $30

(CABA) Cabaletta Bio Rated New Overweight at Cantor; PT $40

(CLPT) ClearPoint Neuro Inc Rated New Buy at Stifel; PT $8

(CRTO) Criteo ADRs Reinstated Overweight at KeyBanc; PT $40

(EXR) Extra Space Rated New Underweight at Wells Fargo; PT $115

(EXRO CN) Exro Technologies Rated New Sector Perform at National Bank

(FDMT) 4D Molecular Rated New Overweight at Cantor; PT $32

(KRYS) Krystal Biotech Reinstated Overweight at Cantor; PT $160

(LSCC) Lattice Semi Rated New Buy at Needham; PT $90

(MIRM) Mirum Pharma Rated New Overweight at Cantor; PT $50

(ONON) On Holding Rated New Buy at Redburn; PT $33

(PSA) Public Storage Reinstated Overweight at Wells Fargo; PT $270

(RCKT) Rocket Pharma Rated New Overweight at Cantor; PT $65

Data sources: Bloomberg, Reuters, CQG

No responses yet