TODAY’S GAME PLAN: from the trading

desk, this is not research

DATA/HEADLINES 10:00ET New Home Sales, BOC Rate Decision; 1:00ET 5 year auction; 4:35ET Fed’s Powell speaks

US new homes sales probably rebounded in September after August’s dramatic 8.7% decline

TODAY’S HIGHLIGHTS:

- Hamas says it fired a rocket from Gaza at Israel’s southern Red Sea resort of Eilat

- Israeli airstrikes on Wednesday targeted Syria’s Aleppo Airport

- Qatar said there may be breakthroughs soon in negotiations to release more hostages held by Hamas

- US antisemitic incidents up about 400% since Israel-Hamas war began, report says – Reuters

Global shares are under pressure again as signs of weakening earnings overshadowed optimism about a well-flagged and long-delayed Chinese economic stimulus. Investor

sentiment was initially bolstered after President Xi Jinping stepped up his effort to revive the world’s second-largest economy, including new debt issuance and an unprecedented visit to the central bank. Earnings from some of the euro region’s biggest consumer-facing

companies also stoked concerns that a global economic slowdown is hurting corporate profits. Elevated bond yields continue to weigh on appetite for equities, with major central banks set to hold policy rates high to bring down inflation.

EQUITIES:

US equity futures are lower after Microsoft and Alphabet delivered a mixed picture of big tech earnings. Alphabet fell more than 7% in post-market trading after its

cloud unit reported a smaller than expected profit. Microsoft, on the other hand, climbed ~3% after results in its cloud business beat expectations. Meanwhile, Texas Instruments dropped after a disappointing revenue forecast suggested that demand remains

sluggish for a broad range of electronic components. Meta Platforms is set to report after the bell, with Amazon.com due Thursday. Meanwhile, House Republicans nominated Mike Johnson of Louisiana as their latest choice for speaker, with a floor vote set for

12:00ET.

Futures ahead of the bell: E-Mini S&P -0.25%, Nasdaq -0.45%, Russell 2000 -0.5%, Dow +0.2%.

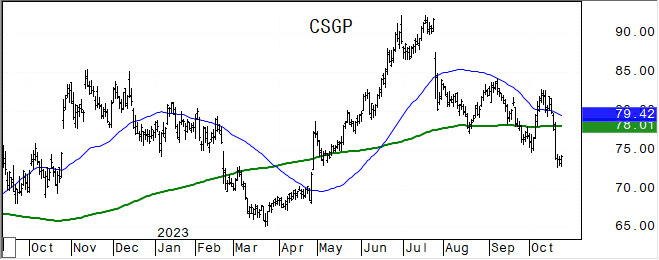

In pre-market trading, CoStar (CSGP) fell 9% after the real estate data company provided a disappointing 4Q forecast. Gap (GPS) shares gain 2.5% after Wells Fargo upgraded the apparel

retailer to overweight from equal-weight. Snap (SNAP) rose 1% after the social media company reported third-quarter results that beat expectations and also gave an outlook that was mixed relative to consensus. Stride (LRN) rose 13% after the online education

company raised guidance. Texas Instruments (TXN) fell 5% as the chipmaker forecast revenue for the fourth quarter that missed estimates. Chewy (CHWY) gains as much as 2.5% after UBS upgrades the online pet supplies retailer to neutral from sell. Teladoc (TDOC)

fell as much as 7.4% after the telehealth platform said it will focus on improving margins over growth. Vertiv Holdings Co. (VRT) jumps as much as 14% after increasing its adjusted earnings per share guidance for the full year.

European gauges reversed their early losses as earnings releases pour in. The Stoxx Europe 600 Index is roughly flat, with real estate, retail and travel & leisure stocks declining the

most while miners and tech outperform. Kering SA slid after the Gucci owner reported a drop in sales amid a global slowdown in luxury, while home products company Reckitt Benckiser Group fell after sales missed expectations. Worldline SA plunged more than

50% after the French fintech company lowered its outlook for this year. Peer Nexi SpA slumped more than 10%. Offsetting those misses, Deutsche bank AG gained as much as 7.5% after saying it plans to accelerate payouts to shareholders as higher income from

its corporate bank and deposit inflows offset weaker trading results in the third quarter. Swedish steelmaker SSAB AB and French software company Dassault Systemes advanced after earnings beats. Germany’s business outlook improved slightly, according to IFO.

Stoxx 600 +0.03%, DAX +0.1%, CAC +0.02%, FTSE +0.25%. Basic Resources +1.2%, Technology +0.8%, Media +0.5%. REITs -1.4%, Retail -1%, Travel -0.8%.

Asian stocks trimmed their earlier gains as an initial rally in Chinese markets eased despite Beijing’s latest steps to support its flagging economy and markets. The MSCI Asia Pacific

Index ended higher by 0.3%, paring an advance of as much as 1.2% with Tencent, Alibaba and Toyota the biggest boosts. The Hang Seng Tech Index opened sharply higher, surging nearly 5%, but those gains were halved as concerns about China’s troubled property

sector lingered. Australian shares erased gains as a faster-than-expected inflation reading supported the case for an interest rate hike next month. South Korean stocks dropped, led lower by EV battery stocks. Hang Seng Tech +2.1%, Topix +0.6%, Hang Seng

Index +0.55%, CSI +0.5%, Taiwan +0.3%. ASX 200 -0.05%, Vietnam -0.4%, Sensex -0.8%, Kospi -0.8%.

FIXED INCOME:

Treasuries are cheaper across the curve, led by the long end, re-steepening the curve with 2s10s paring most of Tuesday’s aggressive flattening move. 10-year yields

near cheapest levels of the day into early US session near 4.86% while 30-year yields re-test 5% level. Treasury auction cycle resumes with $52b 5-year note sale at 1pm, ahead of $38b 7-year on Thursday. Tuesday’s 2-year was solid, stopping in line with WI

yield at bid deadline. Investors will be closely monitoring a speech on Wednesday by US Federal Reserve Chairman Jerome Powell for clues on the path for interest rates.

METALS:

Gold edged higher after two days of losses, with investors continuing to watch for further strength in Treasury yields. The metal reached a five-month high last week in a sharp rally

sparked by the Israel-Hamas war, though haven appetite has since waned as concerns eased over the potential for the conflict to widen to other countries in the Middle East. Gold +0.2%, Silver -0.5%.

ENERGY:

Global benchmark Brent crude was steady after dipping below $88 a barrel and has now erased about half of its gains since Hamas’ attack. Canadian oil prices are weakening

relative to US grades as pipeline bottlenecks restrict shipments to refiners, just months before a massive new export line is scheduled to enter operation. Global demand for fossil fuels is likely to hit a new record next year, amid surging demand from Asia,

according to a new report from the Economist Intelligence Unit. Meanwhile, Russian oil-product exports plunged to the lowest in more than three years. Hurricane Otis made landfall near Acapulco, Mexico, as a category 5. WTI +0.01%, Brent +0.15%, US Nat Gas

+0.25%, RBOB +0.8%.

CURRENCIES:

The dollar extended Tuesday’s gains while the Loonie fell ahead of the Bank of Canada’s policy decision. Bank of Japan officials are likely to monitor bond yield

movements until the last minute before making a decision on whether to adjust the yield curve control program at a policy meeting next week, sources said. The yen was little changed. The Australian dollar initially rose after a strong inflation report but

later lost its gains and is lower on the day as risk aversion gained traction after the London open. Australia’s inflation rate came in hotter than expected, with CPI gaining 5.4% in the third quarter. US$ Index +0.1%, GBPUSD -0.3%, EURUSD -0.2%, USDJPY

flat, AUDUSD -0.2%, NZDUSD -0.4%.

Bitcoin +1.6%, Ethereum +0.7%.

TECHNICAL LEVELS:

|

ESZ23 |

10 Year Yield |

Dec Gold |

Dec WTI |

Spot $ Index |

|

|

Resistance |

4300.00 |

6.000% |

2100.0 |

95.03 |

110.000 |

|

|

4384.00 |

5.750% |

2081.0 |

93.10 |

108.970 |

|

|

4348.00 |

5.500% |

2056.0 |

92.13 |

107.990 |

|

|

4322.00 |

5.325% |

2028.6 |

89.85 |

107.350 |

|

|

4296.00 |

5.000% |

2012.7 |

88.13 |

106.785 |

|

Settlement |

4271.25 |

1986.1 |

83.74 |

||

|

|

4242.50 |

4.800% |

1956.0 |

84.70 |

105.270 |

|

|

4213.00 |

4.470% |

1944.0 |

81.50 |

104.380* |

|

|

4202.00* |

3.925% |

1921.2 |

79.35 |

103.800 |

|

|

4185.00 |

3.870% |

1894.0 |

78.02 |

103.330 |

|

Support |

4150.00 |

3.500% |

1863.0 |

75.63 |

|

Colors within the report:

Green is always the 200 period (day, week).

Red is always 21,

Blue = 50,

Brown =

100 *Stars have added importance

- Upgrades

- (AMRC) Ameresco Raised to Buy at Roth MKM; PT $44

- (AXP) American Express Raised to Neutral at Citi; PT $154

- (CHWY) Chewy Raised to Neutral at UBS; PT $20

- (CSAN3 BZ) Cosan ADRs Raised to Hold at HSBC; PT $13

- (GPS) Gap Raised to Overweight at Wells Fargo; PT $16

- (HXL) Hexcel Raised to Buy at Vertical Research; PT $72

- (LTHM) Livent Raised to Buy at Deutsche Bank; PT $21

- (PCAR) Paccar Raised to Buy at Deutsche Bank; PT $115

- (PGR) Progressive Raised to Outperform at BMO

- (SHOP CN) Shopify Raised to Buy at Veritas Investment Research Co

- (SJW) SJW Raised to Equal-Weight at Wells Fargo; PT $61

- (SRRK) Scholar Rock Raised to Buy at Jefferies; PT $20

- (TECK/B CN) Teck Resources Raised to Strong Buy at CFRA; PT $54

- (TFII CN) TFII CN Raised to Buy at Veritas Investment Research Co

- (TRP CN) TC Energy Raised to Overweight at Wells Fargo; PT C$54

- (VEEV) Veeva Raised to Overweight at Wells Fargo; PT $229

- (VZ) Verizon Raised to Overweight at Barclays

- Downgrades

- (AFRM) Affirm Holdings Cut to Sell at Compass Point; PT $13

- (ALB) Albemarle Cut to Neutral at Piper Sandler; PT $155

- (AMRN) Amarin ADRs Cut to Hold at Jefferies; PT $1

- (BRBR) BellRing Brands Cut to Equal-Weight at Stephens; PT $47

- (CFG) Citizens Financial Cut to Neutral at Piper Sandler; PT $26

- (CWT) California Water Cut to Underweight at Wells Fargo; PT $47

- (ENB CN) Enbridge Cut to Underweight at Wells Fargo; PT C$43

- (ETSY) Etsy Cut to Neutral at Citi; PT $67

- (EVGO) EVgo Cut to Market Perform at Cowen; PT $4

- (FREY) Freyr Battery Cut to Market Perform at Cowen; PT $7

- (FTCH) Farfetch Cut to Sell at SocGen; PT $1.50

- (GLW) Corning Cut to Hold at Deutsche Bank

- (LTHM) Livent Cut to Neutral at Piper Sandler; PT $19

- (NIC) Nicolet Bankshares Cut to Equal-Weight at Stephens; PT $81

- (RF) Regions Financial Cut to Neutral at Piper Sandler; PT $15

- (TRU) TransUnion Cut to Inline at Evercore ISI

- (WNEB) Western New England Cut to Market Perform at Hovde Group

- Initiations

- (ADBE) Adobe Reinstated Hold at KGI Securities; PT $550

- (CHKP) Check Point Software Reinstated Hold at Needham

- (FTNT) Fortinet Reinstated Hold at Needham

- (NFI CN) NFI Group Reinstated Outperform at BMO; PT C$17

- (PANW) Palo Alto Networks Reinstated Buy at Needham; PT $305

- (SN) SharkNinja Rated New Buy at Goldman; PT $52

- (TRML) Tourmaline Bio Inc Rated New Overweight at Piper Sandler; PT $65

- (TSEM IT) Tower Semiconductor Rated New Buy at Benchmark; PT $36

- (UTZ) Utz Brands Rated New Buy at Jefferies; PT $15

- (VZLA CN) Vizsla Silver Rated New Outperform at CIBC; PT C$2.80

Data sources: Bloomberg, Reuters, CQG

No responses yet