TODAY’S GAME PLAN: from the trading

desk, this is not research

DATA/HEADLINES 8:30ET Philly Fed; 10:00ET Existing Home Sales, Richmond Fed Mfg Index; 2:30ET Fed’s Goolsbee speaks

TODAY’S HIGHLIGHTS:

- Biden sparked outrage during his visit to Maui after making a joke comparing the deadly wildfires with almost

losing his ’67 Corvette – Newsweek - US Federal Aviation Administration holding runway safety meetings at 90 airports after series of close calls

Global stocks extended their comeback rally with the MSCI All Country stock index climbing 0.4% in a second straight session of gains. Markets are awaiting more hints

on the outlook for interest rates from policy makers when Fed officials and policy makers from the European Central Bank, the Bank of England and the Bank of Japan head to Jackson Hole, Wyoming, for their annual central bank conference later this week.

EQUITIES:

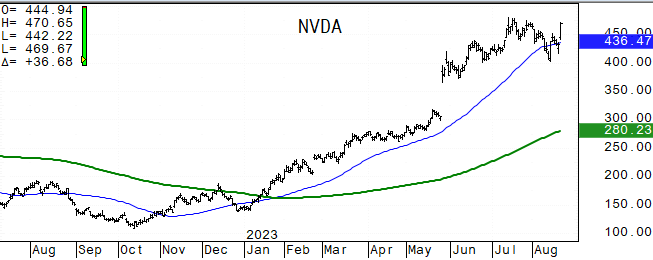

US equity futures are higher, with tech in focus as Nvidia signaled further gains before its earnings report this week. Activision Blizzard rallies 1% ahead of the bell as Microsoft’s

$69 billion acquisition of the firm got a fresh chance at winning approval from UK regulators after the tech giant submitted a substantially different deal. SoftBank Group’s semiconductor unit Arm filed for what is set to be this year’s largest US initial

public offering. Focus was also on US banking stocks, after S&P Global late on Monday cut credit ratings and revised its outlook for multiple lenders, warning that funding risks and weaker profitability will likely test the sector’s credit strength.

Futures ahead of the bell: E-Mini S&P +0.5%, Nasdaq +0.8%, Russell 2000 +0.7%, Dow +0.3%.

In premarket trading, Nvidia (NVDA) added another 1.6% after a more than 8% jump on Monday in a buildup in expectations over the quarterly results of the chip designer that has been the

biggest beneficiary of a boom in artificial intelligence. AppLovin (APP) shares rose 4% as Jefferies upgraded the stock to buy from hold and boosted its PT by 150% to $50. Baidu (BIDU) gained 4.4% after its revenue rose the most in more than a year. Miniso

(MNSO) jumped 7% after the Chinese variety store chain reported fourth-quarter net profit that beat estimates. Tesla (TSLA) rose 4%, on track to extend gains after snapping its longest losing streak of the year on Monday. Zoom (ZM) advanced 4% after the company

raised its full-year forecast for both adjusted earnings and revenue. Coinbase (COIN) gains 2.6% alongside crypto-related peers, after the crypto exchange operator took a stake in stablecoin issuer Circle. Dick’s Sporting Goods (DKS) sinks 19% after the retailer’s

adjusted earnings per share missed analysts’ expectations and management cut its annual EPS guidance. Republic First Bancorp’s stock (FRBK) tanked 29% after it said Nasdaq has informed it its stock will be delisted on Wednesday.

European indices are broadly higher, driven by a 2.7% jump in the tech sector on optimism surrounding the world’s most valuable chipmaker Nvidia, ahead of its quarterly results on Wednesday.

Europe’s Stoxx 600 Index is on track for its biggest gain in nearly a month. In the UK, the FTSE 100 Index is looking to snap its longest losing streak since July 2019. Ubisoft Entertainment SA jumped 8% after signing a cloud streaming deal for Activision

Blizzard Inc. games. Stoxx 600 +1.2%, DAX +1.1%, CAC +1.2%, FTSE 100 +0.6%. Basic Resources +2.7%, REITs +2.1%, Construction +1.5%, Travel +1.4%. All sectors are in the green.

Equities in Asia rose, boosted by a late rally in Chinese stocks, while the Hang Seng Index snapped a seven-day losing streak to end up ~1%. The mainland’s CSI 300 Index closed 0.8% higher

after erasing a loss of as much as 0.7%. The MSCI Asia Pacific Index gained 1%, led by technology and financial shares. Gauges in Korea and Taiwan advanced as chip-related stocks climbed on optimism over Nvidia Corp.’s upcoming earnings report. Thailand stocks

were among the biggest winners in the region as the country was set to appoint a prime minister after months of political gridlock. Japanese lenders led gains on the Topix index after the nation’s benchmark bond yield hit a nine-year high, boosting optimism

the sector’s profitability will improve. Hang Seng Tech +2%, Thailand +1.3%, Topix +1.1%, Shanghai Composite +0.9%, Taiwan +0.3%, Kospi +0.3%, Sensex was flat.

FIXED INCOME:

Treasury futures are higher on the day, paring a portion of Monday’s losses which saw 10-year yields push to new multiyear highs. The persistently resilient economy

has seen investors position for monetary policy to remain tight in the long term, pushing the yields on benchmark Treasuries to the highest since 2007. US 10-year yields climbed to 4.36% – and up almost 40 bps month-to-date. Yields are richer by 1.5bp to

3bp across the curve with the 2s10s spread flatter by as much as 2bp on the day. 10 year yield is down 2bps around 4.31%. 2 year yield ~5.0%.

METALS:

Gold rose for a second day, extending a climb from a five-month low, as the dollar weakened, and traders awaited signals on the US Federal Reserve’s monetary policy.

Later in the week a speech by Fed Chair Jerome Powell will be monitored for clues on the outlook for US interest rates. Spot gold added 0.4%, silver +0.5%.

ENERGY:

Oil prices were weaker as investors stay sour on China’s economic prospects and demand from the world’s top crude importer over the rest of the year. Meanwhile, the

US is expected to continue to draw down stocks. A preliminary Reuters poll showed crude oil and gasoline inventories were expected to have fallen last week, with data from API due later today. However, a possible easing of supply may be in the cards. Observed

exports from Iran have surged to 2.2 million barrels a day this month, and there has been a sudden flurry of talks between Turkey and Iraq as those countries seek to restart a major oil pipeline. European gas prices have been rising as strikes loom at Australian

liquefied natural gas facilities. Benchmark Dutch gas is up nearly 50% for August. WTI -0.4%, Brent -0.6%, US Nat Gas -2%, RBOB -0.05%.

CURRENCIES:

The US Dollar Index continues to fluctuate around its key 200 day moving average. China’s yuan edged back down to around 7.30 per dollar, having shown signs of stabilization

after state banks had earlier used the offshore forwards market to defend it. The yen was also on intervention watch and caught a small boost from a meeting between Bank of Japan chief Kazuo Ueda and the Prime Minister. USDJPY slips as much as 0.4% as Japan’s

10-year yield climbed to a new nine-year high. US $ Index +0.02%, GBPUSD +0.05%, USDJPY -0.3%, EURUSD -0.1%, AUDUSD +0.4%, NZDUSD +0.5%.

Bitcoin -0.3%, Ethereum -0.7%.

TECHNICAL LEVELS:

|

ESU23 |

10 Year Yield |

Dec Gold |

Sept WTI |

Spot $ Index |

|

|

Resistance |

4573.00 |

5.325% |

2029.0 |

89.20 |

108.000 |

|

|

4525.00 |

4.710% |

2007.0 |

87.50 |

107.180 |

|

|

4493.00 |

4.500% |

1987.0 |

85.00 |

106.000 |

|

|

4488.00 |

4.375% |

1957.9 |

82.97 |

105.380 |

|

|

4458.00 |

4.355% |

1951.0 |

82.05 |

103.600 |

|

Settlement |

4412.50 |

1923.0 |

80.12 |

||

|

|

4372.00 |

3.930% |

1912.0* |

78.60 |

103.200 |

|

|

4350.00 |

3.700% |

1907.0* |

76.68 |

102.800 |

|

|

4325/30 |

3.590% |

1866.0 |

76.52 |

102.050 |

|

|

4310.00* |

3.265% |

1842.0 |

74.37 |

101.590 |

|

Support |

4265.00 |

3.000% |

1796.7* |

72.06 |

101.100 |

Colors within the report:

Green is always the 200 period (day, week).

Red is always 21,

Blue = 50,

Brown =

100 *Stars have added importance

UPGRADES:

- AppLovin (APP) raised to buy at Jefferies; PT $50

- Aramark (ARMK) raised to buy at UBS

- Cognizant (CTSH) raised to neutral at JPMorgan; PT $77

- Edison International (EIX) raised to buy at Mizuho Securities; PT $75

- Emerson Electric (EMR) raised to overweight at JPMorgan; PT $107

- Iron Mountain (IRM) raised to outperform at RBC; PT $68

- Jefferies (JEF) raised to buy at Goldman; PT $40

- Pinnacle West Capital (PNW) raised to buy at Mizuho Securities; PT $85

- Provident Financial (PFS) raised to overweight at Piper Sandler

- Restaurant Brands (QSR CN) raised to buy at Northcoast; PT C$116.35

- Shift4 Payments (FOUR) raised to outperform at Raymond James; PT $74

- Trinity Capital (TRIN) raised to buy at Compass Point; PT $15.50

DOWNGRADES:

- Aravive (ARAV) cut to neutral at Cantor; PT 25 cents

- Certara (CERT) cut to hold at Jefferies; PT $17

- Estee Lauder (EL) cut to neutral at President Capital Management

- Evercore (EVR) cut to neutral at Goldman; PT $140

- Genpact (G) cut to underweight at JPMorgan; PT $40

- PhenomeX Inc (CELL) cut to hold at Berenberg; PT $1

- Target (TGT) cut to neutral at Daiwa; PT $134

INITIATIONS:

- Alphabet (GOOGL) rated new outperform at Wedbush; PT $160

- Axon (AXON) rated new equal-weight at Morgan Stanley; PT $230

- Celldex (CLDX) rated new underweight at Wells Fargo; PT $21

- Karuna Therapeutics (KRTX) rated new overweight at Wells Fargo; PT $225

- Light & Wonder (LNW) rated new buy at Redburn; PT $104

- MercadoLibre (MELI) rated new outperform at Wedbush; PT $1,500

- Meta Platforms (META) rated new outperform at Wedbush; PT $350

- Pinterest (PINS) rated new neutral at Wedbush; PT $30

- Sea Ltd ADRs (SE) rated new outperform at Wedbush; PT $48

- Shopify (SHOP CN) rated new outperform at Wedbush; PT $62

- TripAdvisor (TRIP) rated new neutral at Wedbush; PT $17

Data sources: Bloomberg, Reuters, CQG

No responses yet