TODAY’S GAME PLAN: from the trading

desk, this is not research

DATA/HEADLINES 9:45ET S&P Global US Manufacturing, Services PMI, Canada June Retail Sales; 10:00ET New Home Sales;

1:00ET 20-year bond auction

US new home sales probably rose 1% last month, rebounding from June’s 2.5% decline. The August manufacturing PMI is expected to hold at 49, while the services gauge may have dipped slightly.

TODAY’S HIGHLIGHTS:

- Putin, at BRICS: We seek a justifiable settlement by peaceful means

- US Mortgage Rates Jump to 7.31%, Highest Level Since Late 2000

- Tens of millions of Americans to swelter in triple-digit temps this week

Global stock markets edged higher as weak European economic data sent the euro lower and sparked a bounce in bond and equity markets. Investors are also awaiting

results from tech darling Nvidia later to see if the sector’s lofty valuations still look justified. German business activity saw its fastest contraction in over three years and had traders scurrying to firm up bets that the European Central Bank could now

pause what has been a record-breaking run of interest rate hikes. Japan’s factory activity shrank for a third straight month in August amid higher oil prices and uncertainty over the global economic outlook.

EQUITIES:

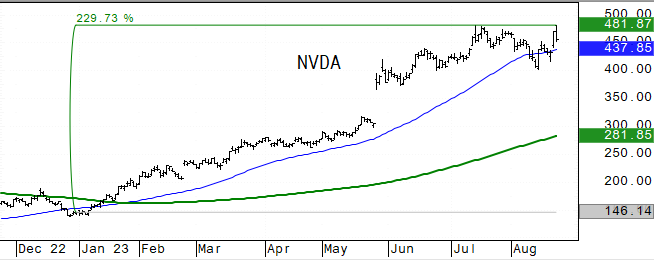

US equity futures pared gains after disappointing earnings updates weighed on investor sentiment ahead of results from chipmaker Nvidia. Futures are still pointing to a bounce having

been pressured on Tuesday by higher bond yields, which hit 16-year highs. US PMI figures measuring August activity will be in focus this morning as investors assess the strength of the economy before Powell’s remarks on Friday. US mortgage rates rose to 7.3%

last week, the highest level since late 2000, sending a key measure of demand down to the lowest in nearly three decades. Home-purchase applications fell for a sixth week to the lowest level since 1995. Chip bellwether NVIDIA is higher in premarket trading

before its results due aftermarket tonight – options market implying a 10% move on earnings. Shares fell on Tuesday, pulling back from an intraday record high.

Futures ahead of the bell: E-Mini S&P +0.1%, Nasdaq +0.2%, Russell 2000 -0.05%, Dow +0.05%.

In pre-market trading, AMC Entertainment (AMC) tumbles 18% with shares on track to suffer a third day of double-digit losses following a Delaware Supreme Court’s ruling that the company’s

stock conversion can proceed. Apellis Pharmaceuticals (APLS) jumped 27% after the biopharmaceutical company provided an update. Arcus Biosciences (RCUS) and iTeos Therapeutics (ITOS) jumped over 35% after competitor Roche AG said data from a critical study

of its new cancer medicine was accidentally released. Foot Locker (FL) tumbles 32% after cutting its adjusted earnings per share guidance for the full year. Peloton sank 27% after forecasting revenue for the first quarter that missed estimates. Urban Outfitters

(URBN) shares are up 4.9% after the clothing retailer reported second-quarter earnings that beat estimates.

European indices were mixed midday as traders weighed weak economic data, marginally waning interest rates, softer oil prices, and took positions ahead of earnings results from US chipmaker

Nvidia. Today’s German ‘flash’ PMIs showed a big drop in services PMI which fell to 47.3, down from 52.3 previously. German manufacturing PMI was little changed at 39.1 (prior 38.8). UK services PMI fell to 48.7, down from 51.5 in August, and manufacturing

PMI also saw a large decline falling to 42.5, down from 45.3, and the lowest reading since the early stages of the pandemic. Eurozone composite PMI dropped to 47.0 in August from July’s 48.6, its lowest since November 2020 and well below the 50 mark separating

growth from contraction. France services PMI slipped further into contractionary territory. Sthe Stoxx 600 erased morning gains but holding slightly higher on the day. Utilities and REITs lead gainers while retail and energy sectors underperform. Stoxx 600

+0.3%, DAX +0.1%, CAC +0.1%, FTSE 100 +0.75%. Utilities +1.7%, REITs +1.2%, Healthcare +1%. Retail -1.5%, Energy -0.8%, Technology -0.6%.

Gauges in Asia were mixed. Asian markets saw more focus on the weakness in China’s economy and yuan, as well some gloomy factory readings from Japan, which also dented sentiment. The

MSCI Asia-Pacific Index advanced 0.4% for a two-day gain of 1.5%. Key gauges advanced in Taiwan, India, Australia and Hong Kong. In China, blue chips failed to hold onto Tuesday’s gains, falling 1.3%. Tech hardware stocks including TSMC extended climbs ahead

of a key earnings report from US chipmaker Nvidia. Baidu, Kuaishou and Anta Sports all rallied in Hong Kong after results. Taiwan +0.85%, Topix +0.5%, ASX 200 +0.4%, Sensex +0.3%, Hang Seng Index +0.3%. Kospi -0.4%, Vietnam -0.7%, CSI 300 -1.6%.

FIXED INCOME:

Treasuries advance, boosted by wider gains across bunds after soft PMI data. Europe led a rally in global bonds as signs of a quickening downturn in the euro area

prompted traders to trim interest-rate hike bets on an ECB September hike and now price in a roughly 40% chance of a 25 basis point move. Outperformance of core European rates drags Treasury yields lower by 5bp to 7bp across the curve with gains on the day

led by intermediates. US focus is on manufacturing PMI, while Treasury auctions resume with 20-year bond sale later in the session. US 10-year yields drop to around 4.26%, remain near lows of the day and richer by 6.5bp versus Tuesday’s close.

METALS:

Precious metal prices rose, with gold extending gains for a fourth straight session, while investors looked forward to comments from Federal Reserve officials at

the Jackson Hole symposium, to gauge the possibility of more interest-rate increases. Gains, however, were limited, as the US dollar index held strong. Spot gold +0.3%, silver +1.5%.

ENERGY:

Oil fell for a third day as a hastening downturn in the euro area added to wider worries about economic growth in top importer China. WTI fell below $79, hitting

the lowest level intraday in almost a month as the contraction in euro-area private sector activity intensified in August. US crude stockpiles fell by 2.4 million barrels last week, with supplies at Cushing declining by more than 2 million, the API reported.

That would take total holdings to the lowest this year if confirmed by the EIA today. Gasoline inventories rose. Turkey and Iraq failed to reach a breakthrough in talks to restart a crucial oil pipeline whose closure has cut off nearly half a million barrels

of crude from global markets. WTI -1.5%, Brent -1.4%, US Nat Gas -0.1%, RBOB -1.9%.

CURRENCIES:

The euro fell to a more than two-month low against the dollar and the pound fell sharply after survey data showed weak business activity in August. The yuan rises

after another strong currency fixing by the PBOC and dollar sales from state-owned banks before trimming gains as the greenback edges higher. The US Dollar Index holds above its key 200 day moving average. US$ Index +0.3%, GBPUSD -0.9%, EURUSD -0.35%, USDJPY

-0.2%, EURJPY -0.6%, EURGBP +0.5%, AUDUSD -0.05%, USDNOK +0.7%.

Bitcoin +0.3%, Ethereum +0.9%.

TECHNICAL LEVELS:

|

ESU23 |

10 Year Yield |

Dec Gold |

Sept WTI |

Spot $ Index |

|

|

Resistance |

4573.00 |

5.325% |

2029.0 |

89.20 |

108.000 |

|

|

4525.00 |

4.710% |

2007.0 |

87.50 |

107.180 |

|

|

4493.00 |

4.500% |

1987.0 |

85.00 |

106.000 |

|

|

4488.00 |

4.375% |

1957.9 |

82.97 |

105.380 |

|

|

4458.00 |

4.355% |

1951.0 |

82.05 |

103.750 |

|

Settlement |

4399.25 |

1926.0 |

79.64 |

||

|

|

4384.00 |

3.930% |

1913.3* |

78.60 |

103.200 |

|

|

4350.00 |

3.700% |

1907.0* |

76.68 |

102.800 |

|

|

4325/30 |

3.590% |

1866.0 |

76.47 |

102.050 |

|

|

4310.00* |

3.265% |

1842.0 |

74.37 |

101.590 |

|

Support |

4265.00 |

3.000% |

1796.7* |

72.06 |

101.100 |

Colors within the report:

Green is always the 200 period (day, week).

Red is always 21,

Blue = 50,

Brown =

100 *Stars have added importance

UPGRADES:

- Brown-Forman (BF/B) raised to overweight at Morgan Stanley; PT $75

- Dollar General (DG) raised to buy at Edward Jones

- Fulcrum Therapeutics (FULC) raised to buy at HC Wainwright; PT $14

- Louisiana-Pacific (LPX) raised to buy at DA Davidson; PT $76

- Petrobras ADRs (PETR4 BZ) raised to buy at Banco BTG Pactual; PT $16

- Petrobras ADRs (PETR4 BZ) raised to buy at BofA

- ScanSource (SCSC) raised to buy at Northcoast; PT $36

- Suncor Energy (SU CN) raised to overweight at Wells Fargo; PT C$54

- TPVG US (TPVG) raised to neutral at Compass Point; PT $9.75

DOWNGRADES:

- Dick’s Sporting (DKS) cut to neutral at Wedbush; PT $115

- Lufax ADRs (LU) cut to add at Huatai Research; PT $1.73

- PhenomeX Inc (CELL) cut to market perform at Cowen; PT $1

- Premier (PINC) cut to neutral at Piper Sandler; PT $25

- Urban Outfitters (URBN) cut to sell at CFRA; PT $29

INITIATIONS:

- AES Corp (AES) rated new overweight at Barclays; PT $25

- American Electric Power (AEP) rated new overweight at Barclays; PT $88

- Atmos Energy (ATO) rated new equal-weight at Barclays; PT $122

- CMS Energy (CMS) rated new equal-weight at Barclays; PT $58

- CenterPoint Energy (CNP) rated new underweight at Barclays; PT $28

- Con Edison (ED) rated new equal-weight at Barclays; PT $88

- DTE Energy (DTE) rated new overweight at Barclays; PT $117

- Dominion Energy (D) rated new equal-weight at Barclays; PT $52

- Duke Energy (DUK) rated new overweight at Barclays; PT $96

- Edison International (EIX) rated new equal-weight at Barclays; PT $68

- Entergy (ETR) rated new equal-weight at Barclays; PT $98

- Evergy (EVRG) rated new equal-weight at Barclays; PT $56

- Eversource (ES) rated new equal-weight at Barclays; PT $72

- Exelon (EXC) rated new overweight at Barclays; PT $43

- FirstEnergy (FE) rated new equal-weight at Barclays; PT $37

- GMS (GMS) rated new buy at DA Davidson; PT $82

- Hammerhead Energy (HHRS CN) rated new outperform at BMO; PT C$22

- Legacy Housing (LEGH) rated new outperform at Wedbush; PT $30

- Marine Products (MPX) rated new neutral at DA Davidson; PT $16

- NorthWestern (NWE) rated new underweight at Barclays; PT $48

- OGE Energy (OGE) rated new overweight at Barclays; PT $36

- PG&E (PCG) rated new overweight at Barclays; PT $19

- PPL (PPL) reinstated equal-weight at Barclays; PT $26

- PSEG (PEG) rated new overweight at Barclays; PT $64

- Pinnacle West Capital (PNW) rated new overweight at Barclays; PT $81

- Portland General (POR) rated new equal-weight at Barclays; PT $43

- Sempra (SRE) rated new overweight at Barclays; PT $156

- Southern Co (SO) rated new equal-weight at Barclays; PT $68

- WEC Energy (WEC) rated new underweight at Barclays; PT $83

Data sources: Bloomberg, Reuters, CQG

No responses yet