TODAY’S GAME PLAN: from the trading

desk, this is not research

DATA/HEADLINES 8:30ET Weekly Jobless Claims, Durable Goods Orders, Chicago Fed Nat Activity Index, Cap Goods Orders;

10:00ET Fed’s Harker speaks; 11:00ET Kansas City Fed Manufacturing Activity; 11:15ET Fed’s Collins speaks; 1:00ET $8 billion 30-year TIPS auction

TODAY’S HIGHLIGHTS:

- According to a report by AP, the only road out of Lahaina was barricaded during deadly Maui fires

- Trump is due to surrender in Atlanta today

- US says stolen COVID relief funds seized so far top $1.4 billion

Global shares rose after blockbuster results from tech darling Nvidia boosted Wall Street, while a retreat in government bond yields eased pressure on borrowing costs,

further boosting sentiment. The MSCI Emerging Markets Index jumped 1.5%, the biggest gain in a month. Investors were also taking bullish cues from news that leaders from Brazil, Russia, India, China and South Africa agreed to expand their BRICS group to give

it more economic clout. Meanwhile, bond markets were broadly higher as investors looked ahead to the gathering of top central bankers at Jackson Hole. The Kremlin is yet to comment on a plane crash in which Wagner chief Yevgeny Prigozhin, his deputy and eight

others are believed to have died. Beijing suspended all seafood imports from Japan after treated wastewater from the Fukushima plant was released into the Pacific Ocean.

EQUITIES:

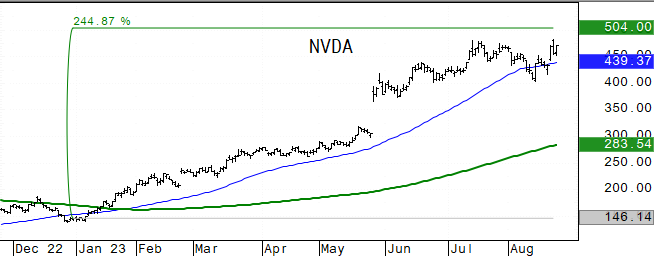

US equity futures are higher as Nasdaq outperforms after a strong outlook from Nvidia Corp. gave fresh impetus to the artificial intelligence hype that’s boosting tech stocks this year.

Nvidia’s results, along with the AI stock frenzy, are punctuating a week that’s seen broad equity-market gains and renewed risk taking by investors. While worries about rising bond yields dominated the conversation last week, the tone has quickly shifted back

to mega-cap tech and whether their earnings can power a stock market that’s been treading water for the past month.

Futures ahead of the bell: E-Mini S&P +0.5%, Nasdaq +1%, Russell 2000 -0.2%, Dow -0.15%. E-mini S&P is nearing initial key resistance at its

50 day mvg avg.

In premarket trading, Nvidia advanced over 8% after the chipmaker delivered a third straight sales forecast that beat analysts’ estimates, while tech giants such as Apple and Microsoft

also rose. Meta, Google and X will need to adhere to strict new content moderation rules under the EU’s Digital Services Act from tomorrow. Boeing fell 2% after it confirmed that its largest supplier improperly drilled holes in a component of the 737 Max.

Guess (GES) shares surged 15% after the apparel retailer’s adjusted earnings per share and net revenue beat expectations. Snowflake (SNOW) rose 4% after the software company reported 2Q results that beat expectations. Splunk (SPLK) shares jumped 13% after

the infrastructure-software company reported an earnings beat and raised full-year guidance. US Steel (X) fell as much as 3% after Esmark said it’s no longer pursuing a takeover. Cassava Sciences (SAVA) gains 7% on news of insider buying. Dollar Tree (DLTR)

falls 6.5% after the retailer provided a 3Q profit forecast that widely missed expectations. The company said it is positioned to bring in wealthier shoppers.

European indices are only marginally higher after paring early gains from Nvidia’s bumper earnings report and falling bond yields faded. Europe’s Stoxx 600 is on track for a four-day

winning streak with the financial services and real estate subgroups leading advancers while the basic resources sub-index lagged. UBS Group AG led financial services stocks higher after the Zurich-based lender was reported to have set a target of winding

down Credit Suisse Group AG’s domestic bank as soon as the end of this month. Stoxx 600 +0.1%, DAX +0.2%, CAC +0.2%, FTSE 100 +0.25%. Financial Services +0.8%, Chemicals +0.7%, Energy +0.4%, REITs +0.4%. Basic Resources -0.6%, Construction -0.4%.

Asian equities advanced, boosted by a rally in semiconductor stocks and Chinese technology firms on the back of Nvidia’s blowout earnings. The MSCI Asia Pacific Index climbed 1%, notching

a third straight day of gains. Chinese stocks listed in Hong Kong were among the best performers in Asia, led by gains in technology companies on optimism over their earnings strength despite the overall malaise in the country’s economy. Chinese seafood stocks

rallied after the Chinese customs authority said the nation will “comprehensively” suspend imports of aquatic products from Japan effective today. Hang Seng Tech +3.7%, Hang Seng Index +2%, Vietnam +1.4%, Kospi +1.3%, Taiwan +1.2%, Nikkei 225 +0.9%CSI 300

+0.7%, Sensex -0.3%.

FIXED INCOME:

Treasuries were rangebound overnight with cash yields slightly cheaper across the curve heading into the US session. US 10-year yields around 4.21%, 2-year yield

~4.97%. TIPs demand will be tested with a $8 billion auction of 30-year securities later, follows a solid 20-year bond sale on Wednesday.

METALS:

Gold edged higher after its biggest jump in five weeks, which was triggered by economic reports that reignited optimism policymakers are nearing the end of monetary-tightening

cycles. Elsewhere, the Polish central bank bought the most gold in four years in July, boosting the share of bullion to more than a tenth of its reserves. Gold +0.1%, silver -0.6%.

ENERGY:

Oil fluctuated as an improving supply outlook hit a market grappling with sluggish demand. Oil futures ticked higher, attempting to find their footing after a three-day

drop that sent the US benchmark to its lowest close in nearly a month. A round of weak purchasing managers index readings on Wednesday from Japan to the eurozone to the US added to economic jitters, analysts said. On the supply front, Reuters reported Wednesday

that US officials were drafting a proposal that would ease sanctions on Venezuela’s oil exports if the country moves toward a free and fair presidential election. That comes on top of a surge in exports from Iran this month. European natural gas prices tumbled

as much as 21% on signs that a labor dispute at Australia’s biggest liquefied natural gas export plant will be resolved, easing fears about one of three possible strikes. WTI +0.2%, Brent +0.3%, US Nat Gas -1.5%, RBOB +1.1%.

CURRENCIES:

In currency markets, the dollar index reversed early overnight losses to trade marginally into the US session. Yen slipped from its strongest in more than a week

while keeping to a tight range before the Jackson Hole meeting of central bankers The Chinese yuan inched higher as the central bank continued to fix the daily mid-point at stronger-than-expected levels. The yuan trimmed its advance as offshore funding costs

eased after surging earlier in the day. The IMF will allow Argentina to intervene in currency markets within a range that won’t be made public to avoid speculation. US$ Index +0.1%, GBPUSD -0.3%, USDJPY +0.4%, EURUSD -0.1%, AUDUSD -0.4%, NZDUSD -0.6%.

Bitcoin -0.3%, Ethereum -0.7%.

TECHNICAL LEVELS:

|

ESU23 |

10 Year Yield |

Dec Gold |

Oct WTI |

Spot $ Index |

|

|

Resistance |

4600.00 |

5.325% |

2029.0 |

89.20 |

107.180 |

|

|

4573.00 |

4.710% |

2007.0 |

87.50 |

106.000 |

|

|

4525.00 |

4.500% |

1987.0 |

85.00 |

105.380 |

|

|

4493.00 |

4.375% |

1957.9 |

82.97 |

104.700 |

|

|

4489.00* |

4.355% |

1951.0 |

82.05 |

104.000 |

|

Settlement |

4447.00 |

1948.1 |

78.89 |

||

|

|

4434.00 |

3.950% |

1913.3* |

76.77 |

103.200 |

|

|

4401.00 |

3.700% |

1907.0* |

76.41 |

102.800 |

|

|

4379.00 |

3.590% |

1866.0 |

74.27 |

102.300 |

|

|

4350.00 |

3.265% |

1842.0 |

71.80/72.00 |

101.780 |

|

Support |

4310.00 |

3.000% |

1796.7* |

68.20 |

101.250 |

Colors within the report:

Green is always the 200 period (day, week).

Red is always 21,

Blue = 50,

Brown =

100 *Stars have added importance

UPGRADES:

- AMC Entertainment (AMC) raised to neutral at Wedbush; PT $19

- Dynatrace (DT) raised to buy at President Capital Management; PT $57

- Kenvue (KVUE) raised to buy at Goldman; PT $29

- NeuroPace (NPCE) raised to equal-weight at Morgan Stanley; PT $6

- Nvidia (NVDA) raised to buy at Stifel; PT $600

- Nvidia (NVDA) raised to buy at WestPark Capital; PT $690

- Nvidia (NVDA) raised to outperform at BNPP Exane; PT $745

- Prudential Financial (PRU) raised to strong buy at Raymond James

- TIXT CN (TIXT CN) raised to sector outperform at Scotiabank; PT C$20.29

- Williams-Sonoma (WSM) raised to neutral at BofA; PT $146

DOWNGRADES:

- Agiliti (AGTI) cut to underweight at Morgan Stanley; PT $10

- Ally Financial (ALLY) cut to peerperform at Wolfe

- Analog Devices (ADI) cut to neutral at Piper Sandler

- Estee Lauder (EL) cut to market perform at Bernstein; PT $160

- Integra LifeSciences (IART) cut to underweight at Morgan Stanley

- International Flavors (IFF) cut to equal-weight at Morgan Stanley

- Mawson Infrastructure Group (MIGI) cut to neutral at Cantor; PT $1

- Peloton (PTON) cut to hold at Needham

- Sea Ltd ADRs (SE) cut to neutral at KGI Securities; PT $42

- Sight Sciences (SGHT) cut to equal-weight at Morgan Stanley; PT $8.40

- Stevanato Group (STVN) cut to equal-weight at Morgan Stanley; PT $34

INITIATIONS:

- Civitas Resources Inc (CIVI) rated new buy at Jefferies; PT $87

- Concentrix (CNXC) rated new sector outperform at Scotiabank; PT $120

- EFFECTOR Therapeutics (EFTR) rated new buy at HC Wainwright; PT $5

- Epam Systems (EPAM) rated new sector perform at Scotiabank; PT $265

- Fifth Third (FITB) rated new market perform at Raymond James

- Genmab ADRs (GMAB DC) rated new buy at BTIG; PT $44

- Globant (GLOB) rated new sector outperform at Scotiabank; PT $210

- Werewolf (HOWL) rated new outperform at Wedbush; PT $9

- Xcel Energy (XEL) rated new equal-weight at Barclays; PT $60

Data sources: Bloomberg, Reuters, CQG

No responses yet