This post goes out as an email to our subscribers every day and is posted for free here around 2 PM ET. To get your real-time copy, sign up for the free or premium version here: Opening Print Subscribe.

Weekly Survey:2nd Week in June

Weekly Breadthalyzer – Friday, June 9th, 2025

Market breadth continued to show broad improvement heading into June. For the week ending June 6, the NYSE recorded 1,897 advancers versus 929 decliners, while the Nasdaq saw 3,215 advancers against 1,511 decliners. Upside volume dominated, with 58% of total NYSE volume and 61% of Nasdaq volume on the advancing side. Notably, new highs expanded: NYSE marked 188 versus 83 new lows, and Nasdaq logged 411 versus 191. This improvement suggests a firming of broader participation, though sentiment remains slightly cautious given the still-elevated number of new lows.

Compared to the prior week, breadth was stronger. Total upside volume rose from 59% to 60% overall. The advance/decline ratio remained firmly positive, with NYSE at 67% advancing issues and Nasdaq at 68%. However, block trade data showed some uptick in large-lot selling activity. The TRIN reading for NYSE declined from 1.73 to 1.44, and Nasdaq TRIN came in at 1.32, suggesting less stress under the surface while remaining in neutral territory. Overall, the breadth data suggests constructive underpinnings, with momentum tentatively broadening out beyond megacaps.

Breadth Stats:

-

NYSE Breadth: 58% Upside Volume

-

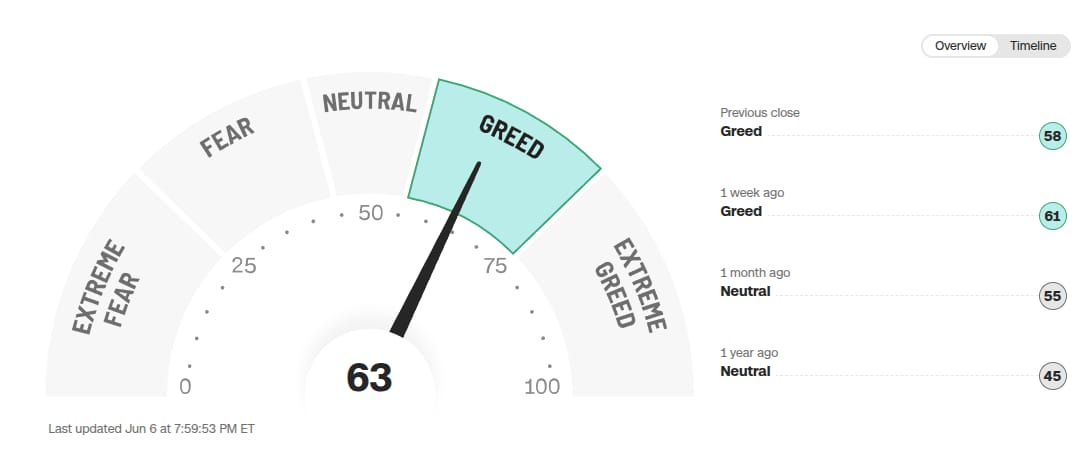

CNN Fear & Greed Index: 63 (Greed)

-

Previous Close: 58 (Greed)

-

1 Week Ago: 61 (Greed)

-

1 Month Ago: 55 (Neutral)

-

1 Year Ago: 45 (Neutral)

-

-

Nasdaq Breadth: 61% Upside Volume

-

Total Breadth: 60% Upside Volume

-

NYSE Advance/Decline: 67% Advance

-

Nasdaq Advance/Decline: 68% Advance

-

Total Advance/Decline: 69% Advance

-

NYSE New Highs/New Lows: 188 / 83

-

Nasdaq New Highs/New Lows: 411 / 191

-

NYSE TRIN: 1.44

-

Nasdaq TRIN: 1.32

Key Economic Events

Wednesday, June 11 – U.S. Consumer Price Index (CPI) May’s CPI report will be a key inflation gauge ahead of the Fed’s June policy meeting. April’s CPI came in slightly above expectations, showing a 3.4% annual rise. Any upside surprise in May could reignite concerns about inflation persistence and delay rate-cut expectations.

Why it matters: Sticky inflation, particularly in shelter and services, could undermine hopes for a September rate cut and weigh on equity valuations.

Thursday, June 12 – U.S. Producer Price Index (PPI) The May PPI will provide insight into inflation at the wholesale level. April’s PPI rose more than expected at 0.5% MoM. Analysts will closely examine core PPI for signs of pipeline inflation that could affect future consumer prices.

Why it matters: Elevated PPI could pressure margins and lead to CPI spillover, complicating the Fed’s path.

Sunday–Monday, June 9–10 – US-China Trade Talks (London) A new round of U.S.–China trade negotiations will take place on the sidelines of an international economic forum. While major breakthroughs aren’t expected, any tone shift or hint at future tariffs could influence risk appetite.

Why it matters: Trade tensions remain a macro overhang. Markets will react to rhetoric and policy cues from both sides.

Corporate Earnings to Watch

Tuesday, June 10 – J.M. Smucker (SJM) Q4 Earnings

J.M. Smucker is expected to report fourth-quarter earnings with projected EPS of $2.24 on revenue of $2.18 billion. Investors will focus on demand trends for its packaged food brands and the impact of input cost pressures. Updates on margins and FY2026 guidance could sway sentiment, especially as consumer staples continue to underperform broader indexes.

Tuesday, June 10 – GameStop (GME) Q1 Earnings

GameStop is projected to post EPS of $0.04 on $754 million in revenue for the first quarter. After sharp volatility tied to executive turnover and capital raises, traders are watching closely for updates on the company’s turnaround plan and digital strategy. Any guidance will be key, particularly in the context of ongoing cost management and store performance.

Wednesday, June 11 – Oracle (ORCL) Q4 Earnings

Oracle is set to report fourth-quarter earnings, with expectations of $1.64 EPS on $15.58 billion in revenue. This will be a key tech report for the week, as investors assess cloud infrastructure performance and AI-linked growth. Strong performance in cloud services, database demand, and bookings could support bullish sentiment. Forward guidance on AI integration will be closely parsed.

Wednesday, June 11 – Oxford Industries (OXM) Q1 Earnings

Oxford Industries, parent of Tommy Bahama and other apparel brands, is forecasted to post EPS of $1.98 on revenue of $383 million. Investors will watch for any signs of consumer spending fatigue, particularly at the premium retail tier. Commentary on inventory levels, promotional activity, and spring/summer outlook will be closely monitored.

Thursday, June 12 – Adobe (ADBE) Q2 Earnings

Adobe will report Q2 earnings with consensus expectations of $4.97 EPS on $5.8 billion in revenue. This is a key tech bellwether for gauging software spending, with particular focus on AI-driven Creative Cloud and Firefly tools. Analysts are looking for signals on growth sustainability in digital media and enterprise cloud subscriptions.

Thursday, June 12 – Restoration Hardware (RH) Q1 Earnings

RH is expected to report a Q1 loss of $0.07 per share on $818 million in revenue. High-end furniture and home goods retailers have struggled with discretionary spending pullbacks. Investors will look for signals of stabilization or further weakness in luxury housing demand and the company’s new gallery openings strategy.

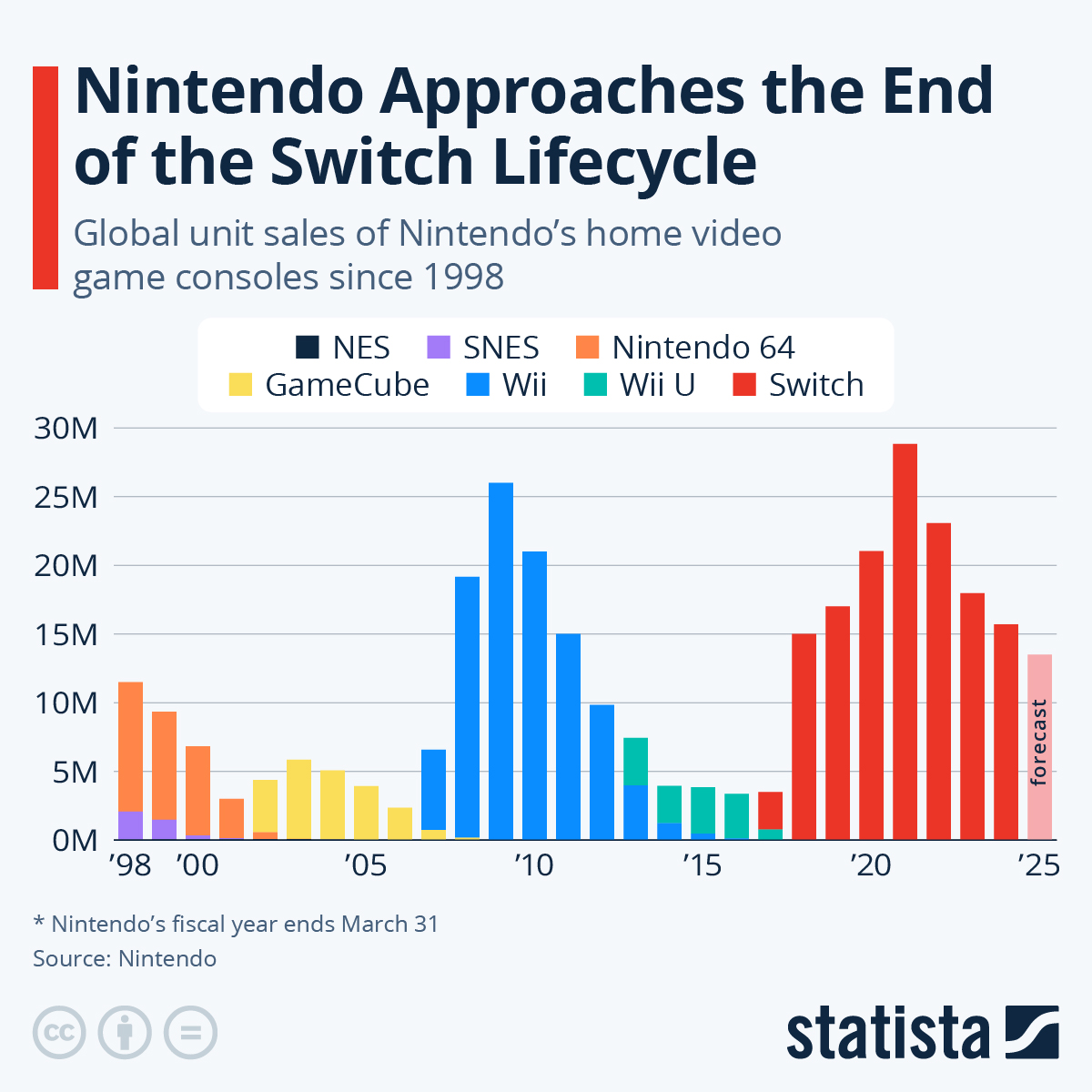

Chart of the Week:

You will find more infographics at Statista

You will find more infographics at StatistaOn Thursday, Nintendo finally released the Switch 2, the long-awaited successor of the Switch, which made its debut in 2017. Despite Nintendo’s reputation for taking big risks and making bold moves – think the motion-controlled Wii in 2006 or succeeding the successful Wii with an entirely new concept in the Wii U – the Japanese company is playing it relatively safe this time. The Switch 2 clearly builds on the proven and highly popular foundation laid by the original Switch, keeping the basic concept alive and just making refinements that bring the ageing device to 2025 and beyond.

Geopolitical Events

China’s Economic Indicators:

-

China’s inflation and trade data, expected this week, will shed light on its economic health amid sluggish domestic growth and U.S. tariff pressures. These metrics are critical for assessing global demand, given China’s role in trade and manufacturing.

U.S.–China Trade Talks (London) – June 9–10, 2025

High-level talks to de-escalate the trade war were scheduled to begin on Monday, June 9 in London between U.S. Treasury/Commerce officials and China’s Vice Premier He Lifeng.

Levels We Are Watching

S&P 500 Index (SPX)

Current: 5,928.48 (+0.28%)

Support: 5,866

Resistance: 6,000

Commentary: SPX is testing psychological resistance at 6,000. A breakout could fuel follow-through buying.

Nasdaq-100 (NDX)

Current: 21,412.03 (+0.33%)

Support: 21,206

Resistance: 21,578

Commentary: Momentum remains tech-driven. The 21,578 level is critical to maintain upside pressure.

Dow Jones Industrial Average (DJI)

Current: 41,335.81 (+0.16%)

Support: 41,100

Resistance: 42,735

Commentary: The Dow continues to lag. Watch for rotation catalysts.

Crude Oil (USO)

Current: 68.12 (+1.44%)

Support: 65.75

Resistance: 69.80

Commentary: Oil rebounded strongly last week. Focus is on OPEC+ supply commentary.

Bitcoin (BTC-USD)

Current: 106,880 (+1.71%)

Support: 100,928

Resistance: 107,867

Commentary: BTC is holding a narrow range. Regulatory clarity remains key.

Gold (GC=F)

Current: $2,351.40 (+0.62%)

Support: $2,310

Resistance: $2,398

Commentary: Gold is consolidating near all-time highs. Real yields and dollar direction will be decisive.

Yield Curves

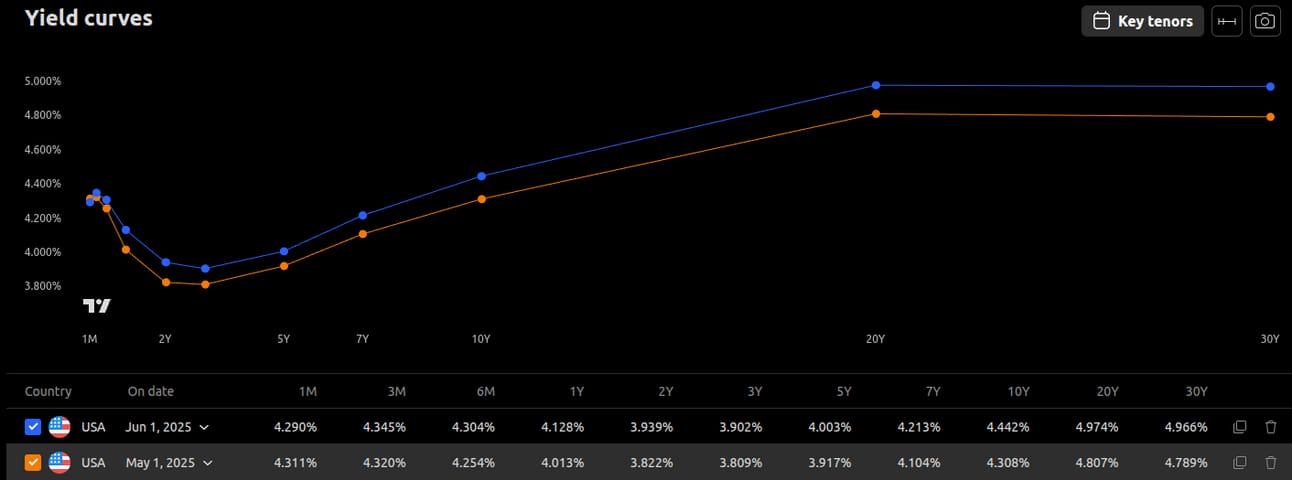

Based on the yield curve for June 8, 2025, the overall shape remains upward sloping from the 2-year to 30-year maturities, similar to last week, indicating a “normal” yield curve and expectations of economic expansion. The 1-month yield (4.290%) is slightly lower than the 3-month yield (4.345%), with a dip to the 6-month (4.304%) and 1-year (4.128%) yields, before rising again at the 2-year (3.939%) and beyond. This continues to show a slight initial “hump” or inversion at the short end, followed by a consistent upward slope.

Compared to last week (June 1, 2025), the yields have shifted slightly upward across most maturities, with the 30-year yield increasing from 4.789% to 4.969%. The short-term “hump” persists, suggesting ongoing near-term uncertainty or market dynamics, potentially tied to Federal Reserve policy expectations. The slight rise in yields across the curve might reflect growing confidence in long-term growth or adjustments in inflation expectations.

Conclusion:

Last week’s market setup played out largely as expected. Key economic data—especially ISM PMIs and Friday’s jobs report—showed a cooling but resilient economy. Job creation came in slightly below expectations, which initially raised hopes for a September rate cut, though sticky wage data kept the Fed’s trajectory uncertain. Breadth metrics improved meaningfully, supporting the idea of a more inclusive rally, while the CNN Fear & Greed Index moved up from 61 to 63, reflecting growing bullish sentiment without tipping into euphoric extremes.

Our focus on Dollar General, Dollar Tree, and Broadcom delivered insight across both consumer resilience and the AI narrative. Broadcom’s strong results reinforced the tech-led leadership in equities, while the dollar-store chains confirmed trade-down behaviors remain a tailwind amid high living costs.

Looking ahead, the setup remains highly event-driven. With CPI, PPI, and the FOMC all landing midweek, the market is poised for sharp moves. The S&P 500 is within striking distance of the psychologically significant 6,000 level. If inflation comes in soft and the Fed signals a possible policy pivot, that resistance could break. But hawkish commentary or hot prints could stall momentum and revive volatility.

The upcoming week will be pivotal for macro strategy. With CPI, PPI, and the Fed decision on deck, volatility is likely to rise midweek. Breadth improvements have been encouraging, but follow-through hinges on how markets interpret inflation and central bank messaging. A breakout above SPX 6,000 could mark the next leg up—if the data cooperates.

Stay alert, stay nimble.

This post goes out as an email to our subscribers every day and is posted for free here around 2 PM ET. To get your real-time copy, sign up for the free or premium version here: Opening Print Subscribe.

Comments are closed