This post goes out as an email to our subscribers every day and is posted for free here around 2 PM ET. To get your real-time copy, sign up for the free or premium version here: Opening Print Subscribe.

Shorts Got Steamrolled, Again — Learn or Burn

Follow @MrTopStep on Twitter and please share if you find our work valuable!

Our View

Now that the government is reopening, there’s a huge backlog of economic reports that are going to be released. While there isn’t a Fed meeting in November, there is a two-day meeting scheduled for December 9–10.

I know some people think I’m nuts about the front-running and that the PPT doesn’t want the stock market to fall. You can agree or disagree—but I really believe both. It was happening last night — as of 7:00 PM Sunday night, the ES put in a high at 6795.50 and is trading 6784.50, up 30.75 points. The NQ hit 25,391.50 and is trading 25,330.50, up 168.75 points. At 7:17 PM, the government passed the bill to reopen the government

As for levels, after the YM, ES, and NQ posted two-week lows. The ES at last night’s high was up 140 points off Friday’s 6665.50 low. The NQ, at its Globex high, was up 559.75 points from its 24,709.25 low.

I think the ES is going to 6820, then 6850.

As for the gap up, there could be some selling, but I don’t think either the ES or NQ are going back to the recent lows anytime soon.

Our Lean

I did catch a long ES on Friday, and I have a good enough lead that I’m holding. Over the last few years, I’ve been learning that the news makes a high and makes a low—but it’s how the news is reported that gets people to make extreme decisions. And while it may not be over, the hysteria around the AI bubble stuff remains.

I said last Thursday—and posted it on Twitter and in Friday’s OP—that I heard our dumb-ass elected officials were going to open up the government on Monday, and I was right.

Market Recap

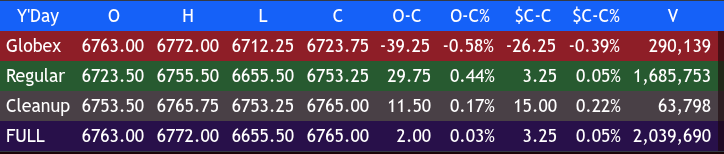

The ESZ25 traded down to 6723.75 on Globex and opened Friday’s regular session (RTH) at 6723.50, down 26.50 points.

After the open, the ES quickly sold off down to 6683.50, rallied back up to a lower high at 6716.50 at 10:15 AM ET, before dropping to 6666.25 and popping up to 6682.00. It then traded back down to 6655.50 and rallied up to 6687.25 around 1:00 PM ET, making a series of dips and rips all the way up to 6705.00 at 1:40 PM ET.

The ES sold off to 6686.00 at 1:50 PM ET and then started plowing higher, trading above VWAP up to 6711.00 at 2:20 PM ET. It pulled back and traded one contract at the exact VWAP price of 6683.75, which triggered an explosive buy program that pushed the ES all the way up to 6744.75 at 3:00 PM ET—an 89.25-point gain off the day’s low.

After reaching the high, the ES pulled back to 6723.25 (one tick below the RTH open) at 3:20 PM ET and traded up to 6745.50 at 3:40 PM ET. It then pulled back to 6731.25 as the 3:50 PM ET cash imbalance showed $2.8 billion to buy. The market ticked down and then ripped up to 6755.50 (exactly 100 points off the low) at 3:55 PM ET, pulled back a few points, then roared up to 6762.50 and settled at 6753.25 on the 4:00 PM ET cash close.

After 4:00 PM ET, the ES ticked down to 6757.00, rallied up to 6765.75, and settled at 6753.75, up 6.25 points or +0.09%.

The NQ made a low at 24,709.25, rallied 518 points up to 25,227.25, and settled at 25,166.25, down 78 points or -0.31% on the day.

In the end, the early selling looked severe, but after the selling dried up and all the options margin calls and rolling lower caught everyone short late in the day, and you can’t tell me the nearly $3 billion bought on the 3:50 imbalance I didn’t add to the late buying spree.

In terms of the ES’s overall tone, I think after the NQ was down over 500 points and immediately started going bid, the ES was already on board. In terms of the ES’s overall trade, volume was the highest of the week at 2.04 million contracts traded.

Last 7 Sessions

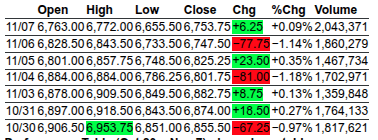

The table above is a very small snippet of the last 7 sessions after the ES traded up to its 10/30 all-time high of 6953.75. There’s no doubt the ES and NQ took a hit, but it isn’t as bad as it looks.

Total over 7 sessions:

On 10/30, the ES made its all-time contract high at 6953.75. Over the 7 trading days from 10/30 to 11/07, the ES fell a total of 226 points on down days and rallied 57 points on up days, resulting in a net point change of 169 down and a −2.4% decline.

The NQ fell 158.75 points on down days and rallied 29.75 points on up days, for a net point change of −129.00 and a −1.89% decline.

The real weakness came from the NQ, which had its worst week since April 4th. I know it was a rough week, but Friday’s late rally saved the FRYday trade. Again, I think what we saw was what a normal pullback looks like after a historic run.

Does that mean the markets can’t go back down? My own opinion is that in most cases, when you have a selloff like we just had and the futures bounce off a low like that, it could be a good low, or similar to how many of the other pullback/declines ended. I believe the positive end-of-year seasonals will carry through into the end of November and the end of the year.

On Tap

-

11:30 AM – Treasury Auction: 13-Week and 26-Week Bills

-

1:00 PM – Treasury Auction: $58 billion in 3-Year Notes (Reopening) & 6-Week Bills

-

After close – Earnings: BigBear.ai (BBAI), CoreWeave (CRWV)

MiM

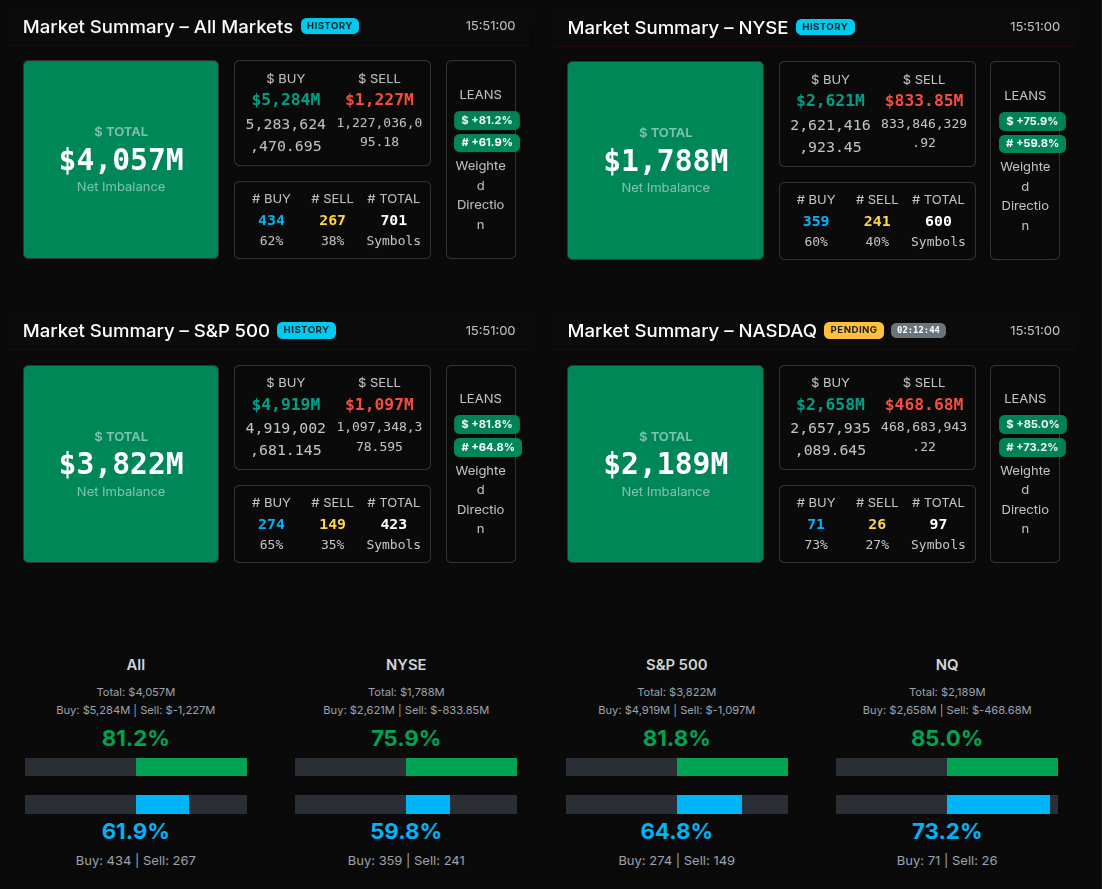

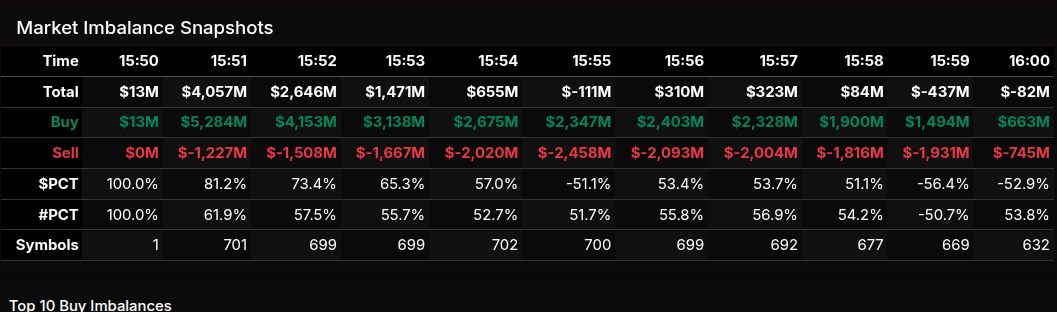

Last Friday’s Market-on-Close (MOC) imbalance opened with a massive buy surge across all markets totaling $4.06B, led by $5.28B in buy orders versus $1.23B in sells, marking a +81% lean—clear institutional accumulation. The S&P 500 showed similar strength at $3.82B net to buy (+81.8%), while the Nasdaq registered an even stronger +85% weighted lean with $2.19B net buy. NYSE flow was also positive at +75.9%, reflecting broad market participation.

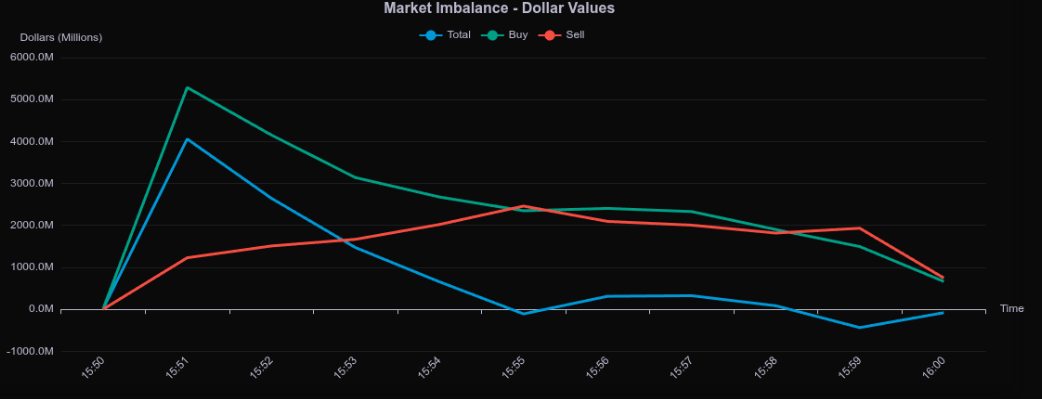

The session’s imbalance curve peaked sharply at 15:51 ET, with total buy interest near $5.3B before moderating steadily through the close as some sell programs entered, trimming the total imbalance to $663M at 16:00. Despite the taper, the close held strongly bid—typical of a session dominated by wholesale market buying rather than rotation.

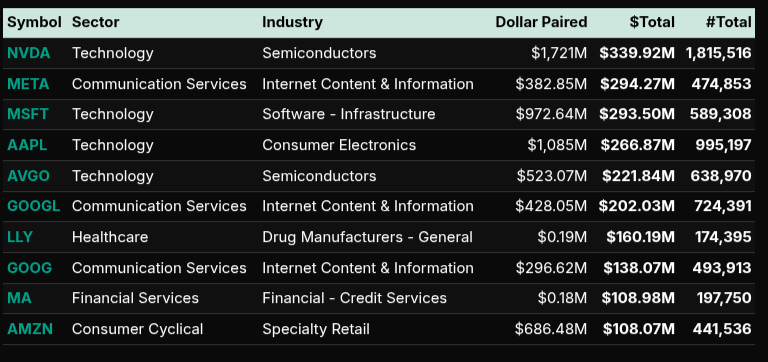

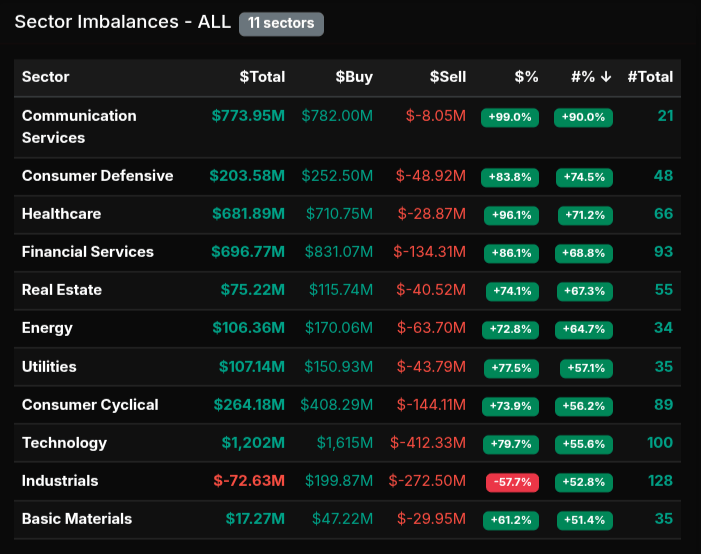

Sector composition reinforced the bullish tone. Technology led with $1.20B in net buying (up +79.7%), anchored by NVDA ($339.9M), MSFT ($293.5M), and AAPL ($266.9M). Communication Services followed with +99% sector strength driven by META (+$294.3M) and GOOGL/GOOG (combined $340M). Healthcare, Financials, and Consumer Defensive also posted strong positive skews, each exceeding +80% buy-weighted. Only Industrials (-57.7%) showed a significant sell lean, as capital rotated out of cyclical exposure.

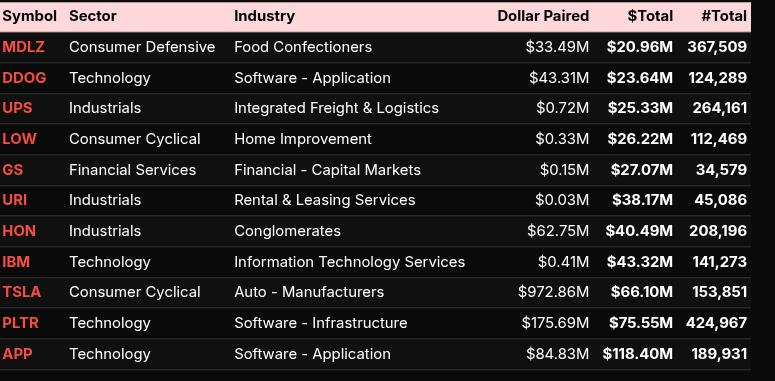

Notable buy symbols included NVDA, META, and MSFT—all heavy semiconductor and software plays—indicating renewed AI and tech accumulation. On the sell side, pressure was concentrated in MDLZ, DDOG, and UPS, each showing modest liquidation relative to overall dollar flow.

By close, symbol participation remained broad: 701 names carried imbalances, with 62% to buy, signaling market-wide demand rather than isolated tech flow. Overall, the MOC profile reflected aggressive end-of-day accumulation in growth and communication names, consistent with fund positioning into mid-November rebalancing.

Technical Edge

Fair Values for November 10, 2025:

-

SP: 23.26

-

NQ: 102.7

-

Dow: 95.4

Daily Breadth Data 📊

For Friday, November 7, 2025

• NYSE Breadth: 72% Upside Volume

• Nasdaq Breadth: 58% Upside Volume

• Total Breadth: 59% Upside Volume

• NYSE Advance/Decline: 61% Advance

• Nasdaq Advance/Decline: 52% Advance

• Total Advance/Decline: 56% Advance

• NYSE New Highs/New Lows: 73 / 126

• Nasdaq New Highs/New Lows: 65 / 388

• NYSE TRIN: 0.67

• Nasdaq TRIN: 0.74

Weekly Breadth Data 📈

For Week Ending November 7, 2025

• NYSE Breadth: 48% Upside Volume

• Nasdaq Breadth: 47% Upside Volume

• Total Breadth: 48% Upside Volume

• NYSE Advance/Decline: 44% Advance

• Nasdaq Advance/Decline: 31% Advance

• Total Advance/Decline: 36% Advance

• NYSE New Highs/New Lows: 223 / 242

• Nasdaq New Highs/New Lows: 345 / 608

• NYSE TRIN: 0.87

• Nasdaq TRIN: 0.65

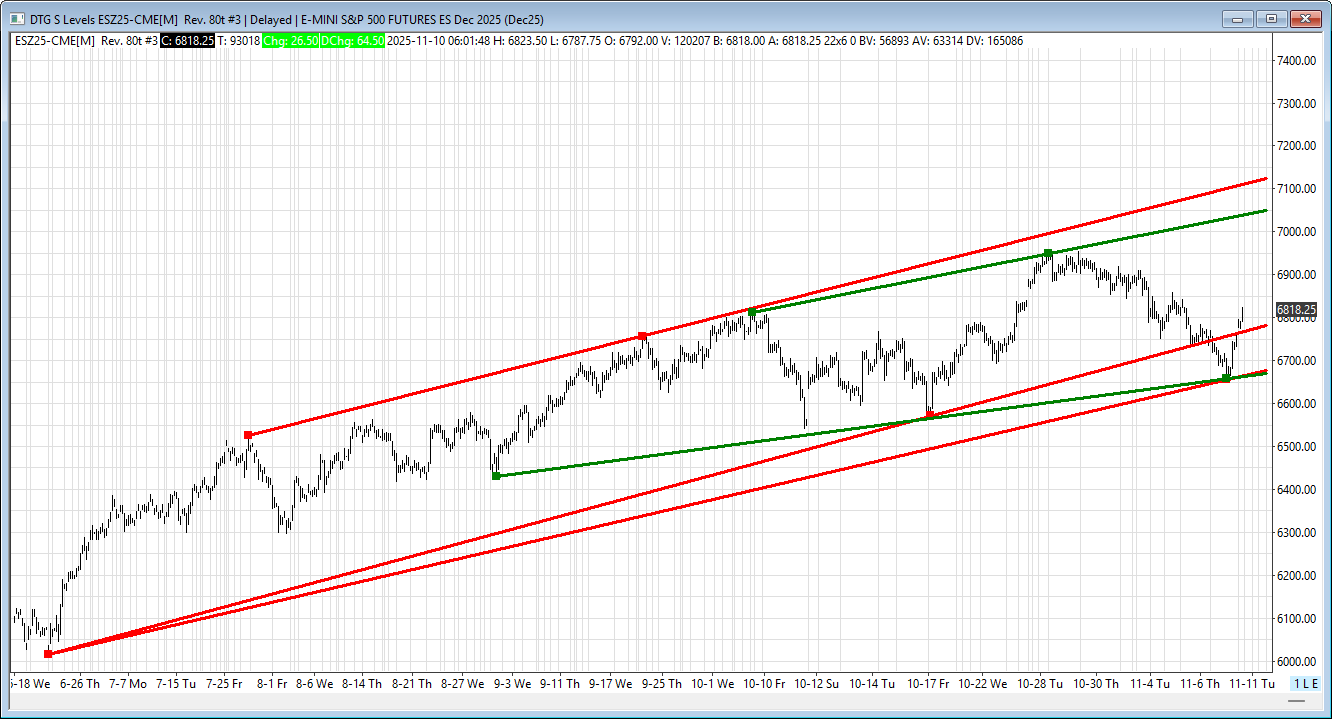

Today’s BTS Levels:

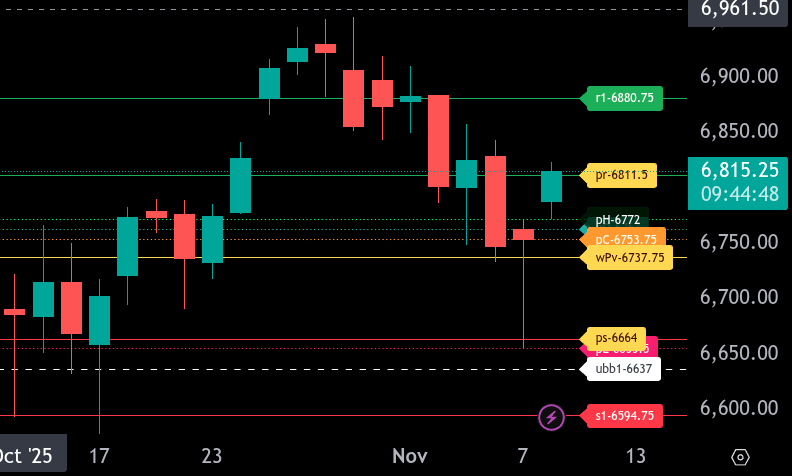

ES Z

The bull/bear line for the ES is at 6737.75. This is the key pivot level that defines today’s directional bias. Trading above this level favors the bulls, while sustained price action below it signals continued weakness.

Currently, ES is trading near 6815.00, showing early strength above the bull/bear line. If momentum holds, the next resistance comes in at 6811.50, followed by 6880.75, which serves as the upper range target. A breakout and hold above 6880.75 would open room for a push toward 6900.00+.

If price fails to hold above 6811.50, watch for a retest of 6772.00 and 6763.00. A sustained move below 6737.75 would turn the tone bearish again, targeting 6664.00 as the lower range level and then 6655.50 as deeper support. A break of 6594.75 could trigger a broader liquidation move.

Overall, the near-term trend leans bullish above 6737.75, but watch for fading strength into resistance levels as the session progresses.

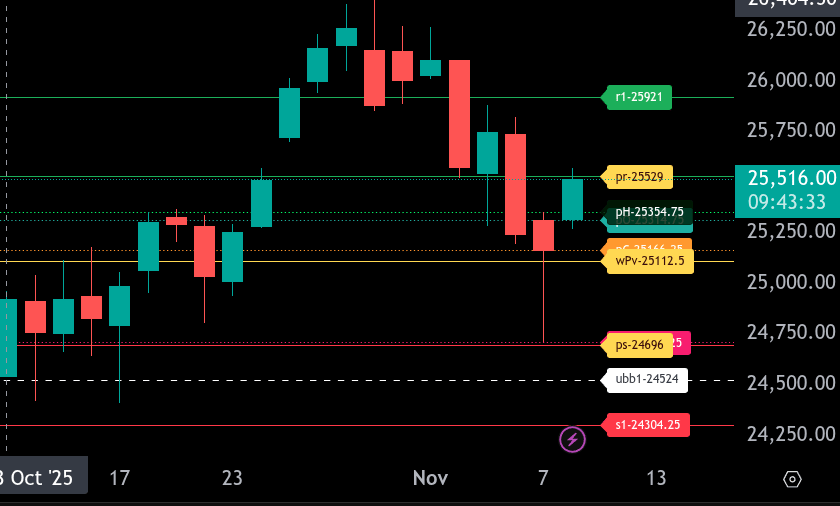

NQ Z

The bull/bear line for the NQ is at 25,112.50. This is the key level that separates bullish and bearish tone today. Currently, NQ is trading around 25,518.00, which keeps the bias tilted to the upside above this level.

If buyers can maintain trade above 25,512.50, the next resistance comes in near 25,529 as the upper range target, with a potential move toward 25,921. Sustained strength above 25,921 could accelerate momentum toward 25,995.

If sellers push price below 25,112.50, look for a test of 24,996 as initial support, with the lower range target down near 24,696. A deeper break opens room toward 24,304.25.

The tone remains constructive above 25,112.50 but turns bearish if that level fails on a sustained basis.

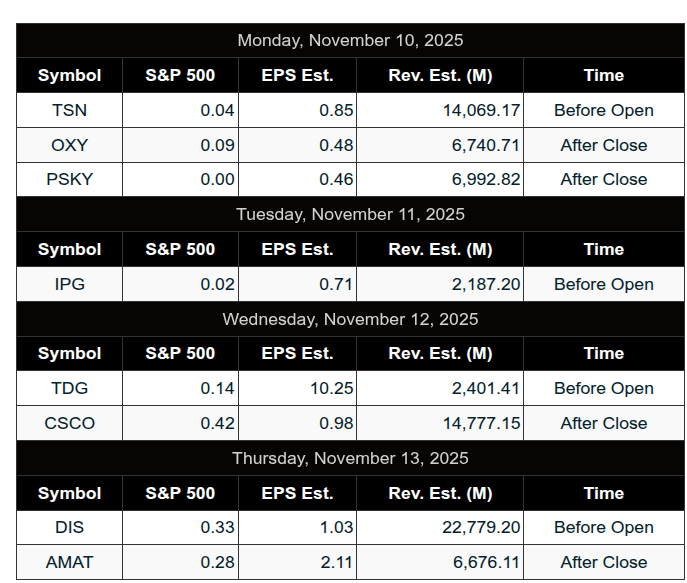

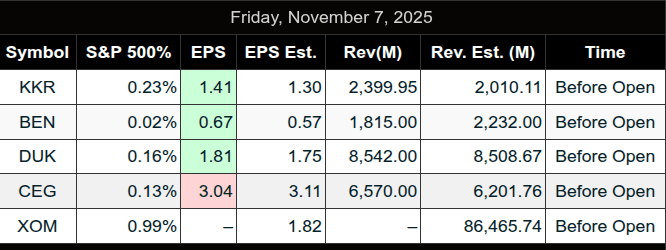

Calendars

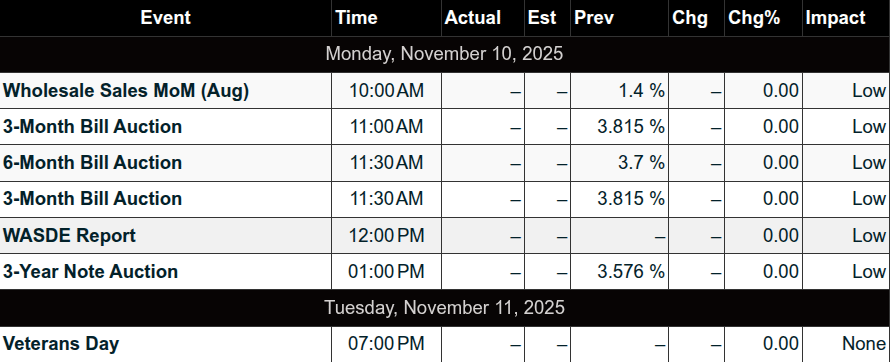

Today’s Economic Calendar

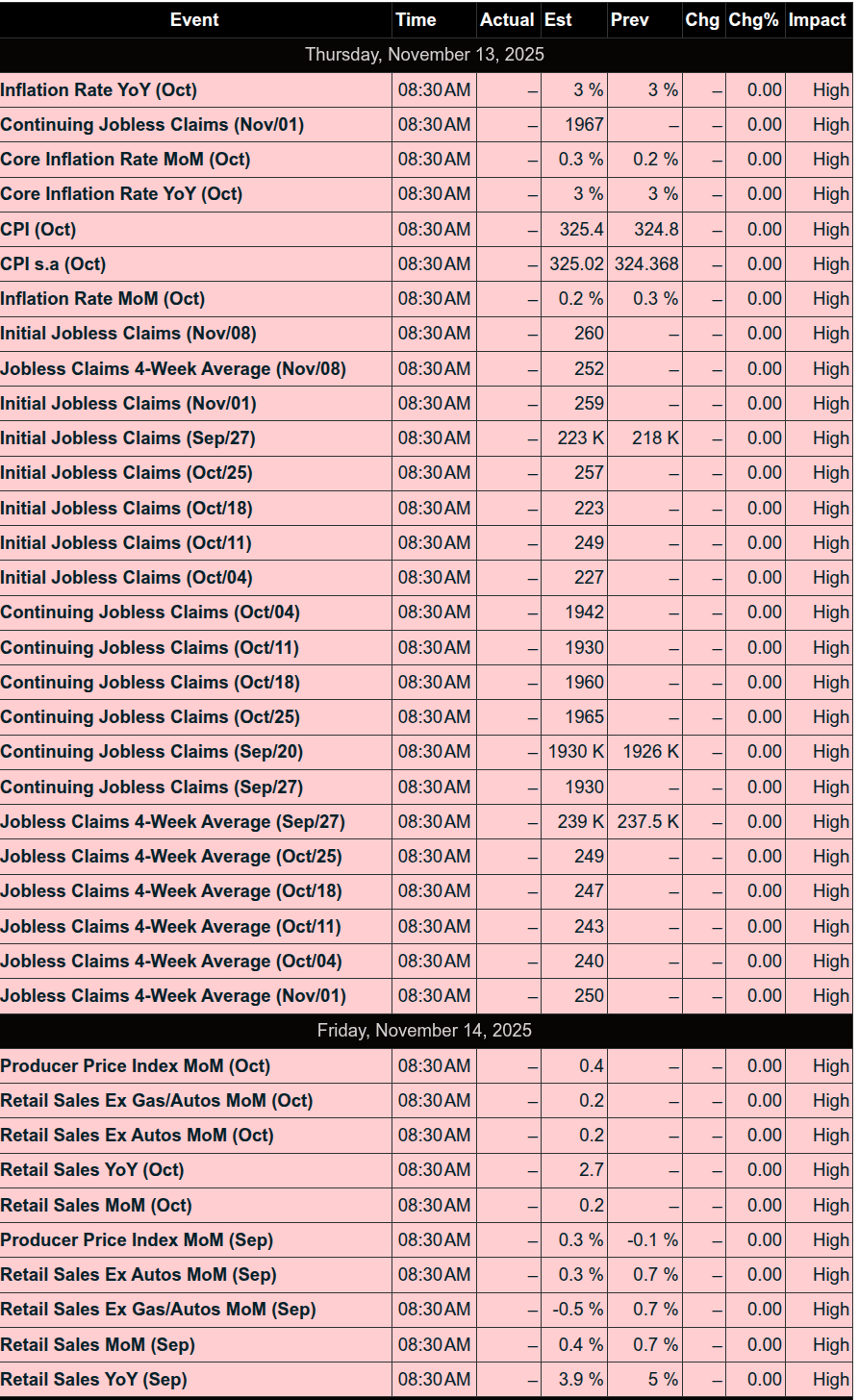

This Week’s Important Economic Events

Upcoming Earnings

Recent Earnings

Room Summaries:

Polaris Trading Group Summary – Friday, November 7, 2025

Friday was a Capital Preservation type day, beginning as Cycle Day 3 and ending with a strong reversal that saw Cycle Day 1 reclaimed by the close. The session was defined by a long-liquidation dip, followed by an aggressive short squeeze recovery into the final hours. Key resistance was identified at the 6760 line-in-the-sand (LIS), which capped price action early. On the downside, critical support levels included 6718.75, which triggered the initial buy response, 6683 which held on a backtest, and the 6666.50 statistical extreme from CD3 that ultimately marked the low and catalyzed the afternoon reversal.

Morning Session:

-

Overnight weakness held below 6760 LIS.

-

Early rejection at lower D-level 6718.75 triggered a precise buy reaction.

-

Manny shared a well-structured trade plan, highlighting buy zones at 6674–78 and 6709–13, and resistance zones at 6754–58 and 6774–78.

-

6683 held on a backtest per David — became a key support marker.

-

Bosier and others engaged in scalps around 6702–6706 area with some small wins.

Midday:

-

Weak chop early, but the wholesale liquidation into the 6666.50 CD3 Extreme triggered the turnaround.

-

Textbook “everything must go” selloff was reversed immediately upon reclaim of 6666.50 — a critical lesson in recognizing statistical extremes and watching for reversals.

Afternoon Power Move:

-

Reversal gained steam with a major short squeeze, culminating in a powerful rally.

-

Price reclaimed CD1 Low (6748.50) — David called it earlier and target was hit.

-

Final push was supported by a $2.8B MOC buy imbalance, reinforcing the late-day strength.

-

Day closed with Cycle Day 1 fully reclaimed, keeping the positive 3-day cycle intact.

Key Wins & Lessons:

-

Buying extremes at 6666.50 (statistical edge) led to a massive rally opportunity.

-

David’s morning call of 6683 holding as support was pivotal.

-

Manny’s zone-based strategy provided clear structure for planning both longs and shorts.

-

Emphasis on capital preservation early, with asymmetrical long setups later, paid off.

Quote of the day:

“Give a little to the bears, let them feel clever… and then take it all back (plus tip) once the selling stops.” – PTGDavid

Outcome: Strong bounce off session lows, bulls reclaim control into weekend.

DTG Room Preview – Monday, November 10, 2025

-

Macro/Policy: Senate advanced a bill to end the government shutdown; House vote likely midweek. The bill extends funding to Jan 30, 2026, with a healthcare vote mandated by end of 2025. Shutdown impact includes airline disruptions and delayed federal pay. SNAP benefits in flux amid legal back-and-forth.

-

Commodities: Gold surging; oil higher on reopening optimism and focus shifting to Fed policy.

-

China: Cracks down on fentanyl precursors with new export license rules for 13 chemicals to US/Canada/Mexico.

-

Earnings: TSMC beat October sales expectations (+16.9%), though pace is slowing. Big Tech plans $400B AI spend in 2026. Premarket earnings: B, TSN, KSPI, KE; After-hours: ASTS, SBS, OXY, RGTI, RKLB.

-

Fed: SF’s Daly speaks 8:30am ET; STL’s Musalem at 9:45am ET.

-

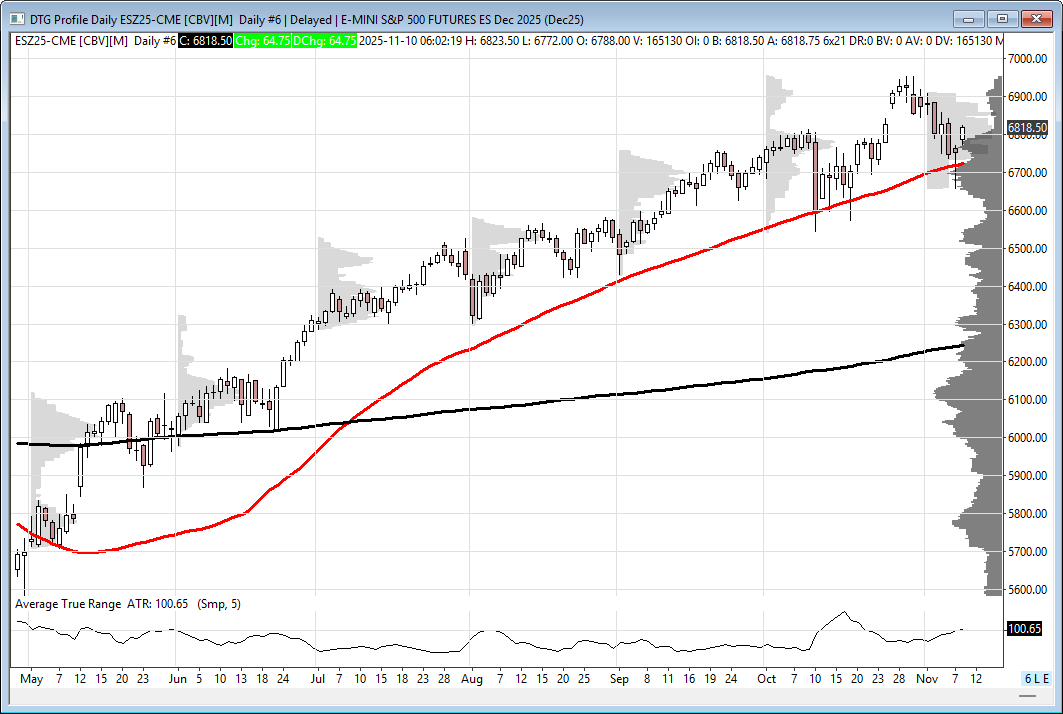

Market Action: Volatility rising; ES 5-day ADR at 98.75. Friday’s bounce off 50-day MA (6724.50) sets 6655.50 as key swing low. Bulls regaining uptrend footing.

-

Levels to Watch:

-

Resistance: 6968/73, 7045/50, 7112/17

-

Support: 6768/73, 6675/80

-

-

Bias: Slightly bullish into US open on light whale volume.

Affiliate Disclosure: This newsletter may contain affiliate links, which means we may earn a commission if you click through and make a purchase. This comes at no additional cost to you and helps us continue providing valuable content. We only recommend products or services we genuinely believe in. Thank you for your support!

Disclaimer: Charts and analysis are for discussion and education purposes only. I am not a financial advisor, do not give financial advice and am not recommending the buying or selling of any security.

Remember: Not all setups will trigger. Not all setups will be profitable. Not all setups should be taken. These are simply the setups that I have put together for years on my own and what I watch as part of my own “game plan” coming into each day. Good luck!

This post goes out as an email to our subscribers every day and is posted for free here around 2 PM ET. To get your real-time copy, sign up for the free or premium version here: Opening Print Subscribe.

Comments are closed