TODAY’S GAME PLAN: from

the trading desk, this is not research

DATA/HEADLINES ET 8:30 a.m: US Initial Jobless Claims, 10:00 a.m.: Fed’s Harker speaks, 11:00

a.m: EIA US crude oil inventories, 11:45 a.m: Fed’s Goolsbee speaks.

TODAY’S HIGHLIGHTS:

- Bruce Springsteen Postpones All September Tour Dates Due to Peptic Ulcer Disease

- Travis Kelce to test knee in Thursday morning workout

Global equities were mostly lower, with US stock futures slipping while European stocks remained flat, erasing an earlier decline. Nasdaq futures slid due to a report

stating that China plans to expand its ban on the use of iPhones to state firms and agencies. In Asia, equities closed lower, with Chinese stocks among the worst performers, weighed down by property developers. Meanwhile, the US and European Union are working

on an agreement that would introduce new tariffs aimed at excess steel production from China and other countries. In currency markets, China’s onshore yuan dropped to its lowest level against the greenback since late 2007, even after the PBOC set its daily

reference rate at a stronger-than-expected level for the 54th straight day. Two-year Treasury yields edged back below 5%, while oil and most metals declined.

EQUITIES:

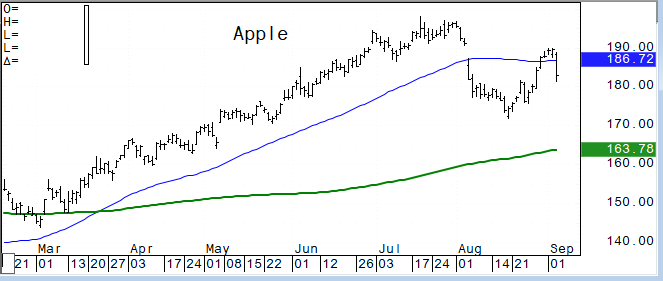

US stock futures dropped as investors ramped up bets on further Federal Reserve policy tightening. Apple slid as much as 2.6% in premarket trading on China’s plans

to ban iPhones in some government agencies. Nvidia fell as much as 2.7% in US premarket trading, putting the stock on track for a second session of losses, as a weak start to September is making for the worst monthly decline since last December. C3.ai (AI

US) shares fell 9.6% after the artificial intelligence software company gave a tepid revenue forecast and said that profitability will take longer than expected. UiPath (PATH US) shares rose 4.8% after the robotic process automation software company reported

second-quarter results that beat expectations and gave an outlook. Yext (YEXT US) shares slumped 15% after the infrastructure-software company’s third-quarter revenue forecast came in below the average analyst estimate at the midpoint. NEE +1.2%, MCD +1.2%,

STLA +1%, MRNA +0.6%, LMT +0.5%, GME +6%, PATH +4%, IP +1.7%, CROX -2.1%, STX -2.8%.

Futures ahead of the bell: E-Mini S&P -0.5%, Nasdaq -0.9%, Russell 2000 -0.3%, Dow -0.1%.

European stocks were flat, erasing an earlier decline. Utilities and drug makers rose, while miners and technology stocks were the biggest decliners among sectors. In Germany, industrial output fell

again in July, further holding back the biggest economy in Europe and casting a pall over the beginning of the third quarter. Luxury-goods makers, including Swatch Group AG, Burberry Group AG, and Hermes International SA, rose after a slump on Wednesday, triggered

by a warning from Richemont that inflation is starting to hit demand. The sector was also boosted by earnings beat from luxury shoemaker Tod’s SpA. Among single stocks, Direct Line Insurance Group Plc soared after the insurer agreed to sell its brokered commercial

insurance business lines to RSA, while Smurfit Kappa Group Plc fell after confirming that it was in talks with WestRock Co. to merge. Stoxx 600 -0.1%, DAX -0.2%, CAC +0.04%, FTSE 100 +0.2%.

Asian stocks were lower as Chinese property developers slipped, following their sharp rally in the previous session. The MSCI Asia Pacific Index slid by as much as 0.8%, setting it up for a third

day of losses. The tech sector was the worst performing, as solid US data overnight spurred bets for further Federal Reserve tightening. Almost all equity benchmarks were in the red, except in India; Indian stocks were lifted by gains in power producers. China’s

export slump eased in August, adding to early signals that the worst may be over for some parts of the world’s second-largest economy as it tries to regain momentum. Chinese chipmaker companies dropped on Thursday after a US lawmaker called for an investigation

into the reported SMIC chip related to Huawei’s new phone model. Elsewhere, Malaysia’s central bank kept rates on hold at 3%. Hang Seng Index -1.3%, Kospi -0.6%, ASX 200 -1.2%, Vietnam -0.2%, Nikkei 225 -0.7%, Sensex +0.1%, Philippines +0.2%, Taiwan -0.7%.

FIXED INCOME:

Treasuries are slightly richer across the curve, with gains led by the front-end as 2-year yields edge back below 5%, following a wider bull-steepening rally in gilts. Front-end yields

are richer by 2bp-3bp, with 2s10s and 5s30s steeper by 1bp-2bp; US 10-year around 4.27%, about 1bp richer on the day, with bunds and gilts outperforming by 1.5bp and 6bp in the sector. Focal points today include weekly initial jobless claims and six scheduled

Fed speakers.

METALS:

Gold was steady as stronger-than-expected US economic data bolstered bets that the Federal Reserve could hike interest rates again this year. Meanwhile, Gold investment

has risen over the past year, driven by central bank purchases, with overall implied allocations by non-bank investors at the highest since the end of 2012. Gold +0.2%, silver -0.3%.

ENERGY:

Oil prices weakened after capping the longest run of gains in more than four years as OPEC+ leaders extended supply cuts to the end of 2023. Elsewhere, European natural

gas prices rose as uncertainties lingered over the possibility of strikes at Chevron Corp.’s LNG facilities in Australia. WTI -0.6%, Brent -0.5%.

CURRENCIES:

The US Dollar strengthened, supported by a strong reading of US services ISM data on Wednesday, nudging up market pricing for a 25 basis-point Federal Reserve rate hike in November to around 55%

from around 50%. China’s onshore yuan dropped to a 16-year low against the dollar as pessimism grew toward China’s economy and financial markets. The yen slid to a 10-month low; Bank of Japan Board Member Junko Nakagawa said it’s appropriate to continue with

monetary easing for the time being as the inflation target hasn’t been achieved yet. Elsewhere, the Aussie dollar earlier slipped after the nation reported a smaller trade surplus for July. US$ Index +0.1%, GBPUSD -0.3%, USDJPY +0.1%, EURUSD -0.1%, AUDUSD

+0.05%, NZDUSD +0.2%, USDCAD -0.1%

Bitcoin +0.08%, Ethereum +0.02%.

Colors within the report:

Green is always the 200 period (day, week).

Red is always 21,

Blue = 50,

Brown =

100 *Stars have added importance

UPGRADES:

-

First Quantum Minerals (FM CN) raised to outperform at BMO; PT C$40

-

McDonald’s (MCD) raised to overweight at Wells Fargo; PT $310

-

Owens Corning (OC) raised to neutral at Goldman; PT $150

-

Tri Pointe Homes (TPH) raised to outperform at Oppenheimer; PT $36

-

Vail Resorts (MTN) raised to buy at Truist Secs; PT $290

DOWNGRADES:

-

Crocs (CROX) cut to neutral at B Riley; PT $101

-

Dave & Buster’s (PLAY) cut to outperform at Raymond James; PT $55

-

Dell Technologies (DELL) cut to underweight at Barclays; PT $53

-

Greenbrier (GBX) cut to equal-weight at Wells Fargo; PT $40

-

NCR (NCR) cut to neutral at Northcoast

-

Pampa Energia ADRs (PAMP AR) cut to reduce at HSBC; PT $30

-

Polestar ADRs (PSNY) cut to underweight at Barclays; PT $3

-

Roku (ROKU) cut to hold at Loop Capital; PT $85

-

Seagate (STX) cut to equal-weight at Barclays; PT $65

-

Torrid (CURV) cut to neutral at Baird; PT $2.50

-

Verint (VRNT) cut to market perform at Oppenheimer

INITIATIONS:

-

American Financial (AFG) rated new hold at Jefferies; PT $120

-

Ardelyx (ARDX) rated new buy at HC Wainwright; PT $9

-

Bank of America (BAC) reinstated buy at HSBC; PT $35

-

Citigroup (C) reinstated hold at HSBC; PT $43

-

CyberArk (CYBR) rated new buy at Guggenheim; PT $200

-

CytoSorbents (CTSO) reinstated buy at B Riley; PT $4

-

Flex (FLEX) rated new overweight at Barclays; PT $35

-

Floor & Decor (FND) rated new buy at Stifel; PT $120

-

Goldman Sachs (GS) reinstated buy at HSBC; PT $403

-

Harmony Biosciences (HRMY) rated new buy at Berenberg; PT $59

-

Home Depot (HD) rated new hold at Stifel; PT $350

-

JPMorgan (JPM) reinstated hold at HSBC; PT $159

-

Jabil (JBL) rated new overweight at Barclays; PT $134

-

Kenvue (KVUE) rated new buy at Canaccord; PT $28

-

Koru Medical Systems (KRMD) rated new buy at B Riley; PT $4.50

-

Krystal Biotech (KRYS) rated new buy at Berenberg; PT $154

-

Lowe’s (LOW) rated new buy at Stifel; PT $270

-

Markel Group Inc (MKL) rated new buy at Jefferies; PT $1,750

-

Monro (MNRO) rated new equal-weight at Wells Fargo; PT $35

-

Morgan Stanley (MS) reinstated buy at HSBC; PT $99

-

Oil States (OIS) rated new outperform at Raymond James; PT $10

-

PNC Financial (PNC) rated new reduce at HSBC; PT $110

-

PlayAGS (AGS) rated new market outperform at JMP; PT $11

-

RLI (RLI) rated new buy at Jefferies; PT $155

-

Sportradar (SRAD) rated new market perform at JMP

-

Terawulf (WULF) rated new buy at Compass Point; PT $3

-

Truist Financial (TFC) rated new hold at HSBC; PT $29

-

U.S. Bancorp (USB) rated new hold at HSBC; PT $39

-

Valvoline (VVV) rated new overweight at Wells Fargo; PT $42

-

Wells Fargo (WFC) rated new hold at HSBC; PT $45

Data sources: Bloomberg, Reuters, CQG

No responses yet