TODAY’S GAME PLAN: from the trading

desk, this is not research

DATA/HEADLINES 7:00ET Challenger Job Cuts; 8:30ET Weekly Jobless Claims, Trade Balance; 9:00ET Fed’s Mester speaks;

10:40ET Fed’s Kashkari speaks; 11:30ET Fed’s Barkin speaks; 12:00ET Fed’s Daly speaks; 12:15ET Fed’s Barr speaks

TODAY’S HIGHLIGHTS:

- Biden announces $9 billion more in student debt relief; total approved debt cancellation $127B

- Joe Biden sent his German shepherd to an unspecified location following about a dozen biting incidents

- Former European Commission President Juncker: Ukraine is “corrupt at all levels of society”

- Biden Administration to Resume Border Wall Construction in Policy Reversal

Global markets steadied, after a plunge in oil prices and softer US labor data late on Wednesday helped bring US Treasury yields back down from 16-year highs. The

MSCI world equity index was up 0.3%, after hitting its lowest level since late March yesterday. Investor sentiment remains fragile after wild moves across markets this week driven by soaring US bond yields. Barclays analysts wrote in a note that global bonds

are doomed to keep falling unless a sustained slump in equities revives the appeal of fixed-income assets. All eyes will now be on Friday’s US employment figures for clues on the health of the world’s biggest economy and the US Federal Reserve’s monetary policy

outlook.

EQUITIES:

US equities futures fluctuated overnight as investors mulled the outlook for monetary policy and braced for key jobs data. Traders are now looking to tomorrow’s US jobs data for clues

as to whether the bonds sell-off will continue. The recent selloff in US stocks has been widespread, with just 11% of the S&P 500 members now trading above their 50-day moving average. Several times over the past 18 months, stocks have bounced when the breadth

reached similar levels.

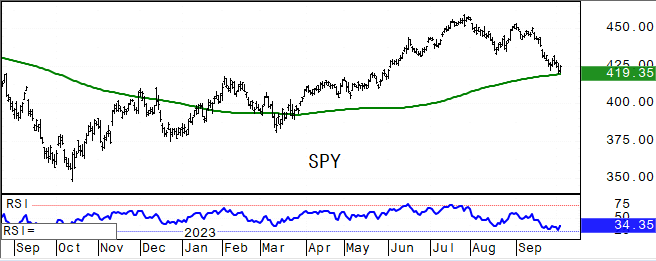

Futures ahead of the bell: E-Mini S&P +0.05%, Nasdaq +0.1%, Russell 2000 -0.1%, Dow -0.1%. A 10% decline in SPX from the July highs would be around 4148 area. 200 day moving average held

as support in SPY.

In pre-market trading, Rivian Automotive (RIVN) falls as much as 9% after the electric-vehicle maker announced plans to issue $1.5 billion in convertible debt and reported preliminary

third-quarter revenue. Clorox (CLX) – reeling from a cyberattack that disrupted production — falls over 4% after saying preliminary net sales dropped by 23%-28% in the latest quarter. MaxCyte (MXCT), owner of a platform used in the cell therapy market, slumps

22% after the company posted preliminary third-quarter revenue that disappointed. BioXcel Therapeutics (BTAI) falls 6.4% after Truist Securities downgraded the biotech firm to hold from buy. Cambium Networks’ (CMBM) shares are plummeting 32% after the wireless

networking infrastructure company reported preliminary third-quarter revenue that prompted at least two analyst downgrades. Nanobiotix ADRs (NBTX) sink 20% after the company said 10 deaths occurred within 180 days of enrollment of a trial for its investigational

treatment for patients with advanced head and neck cancer.

Growth stocks remain attractive in an uncertain economic outlook, Citi quants said.

European gauges tracked slightly higher midday as traders weighed cooling interest rates and slipping oil prices, and bargain-hunted after recent declines. ECB’s Kasimir indicated “core

inflation data confirmed ECB’s expectations that the last rate hike is the last one.” Among individual movers in Europe, Alstom SA shares plunged 35% after the French train maker slashed its financial guidance due to delays on UK contracts and a rise in inventories.

Imperial Brands gained ~4% in London, after announcing a further £1.1 billion share buyback on profit growth. Stoxx 600 +0.5%, DAX +0.2%, CAC +0.2%, FTSE 100 +0.6%. Travel & Leisure +2.2%, Media +1%, Retail +1%, Financial Services +1%. Energy -0.7%.

Asian shares rebounded from 11-month lows overnight, following gains on Wall Street. The MSCI Asia Pacific Index climbed 1.1%, driven by gains in the financial and technology sectors.

Japanese stocks led the relief rally in the region with Topix recording its best day in 11 months. Philippine and Vietnamese stocks bucked the region-wide positive trend. Philippine’s stock benchmark slid after inflation jumped to a four-month high. Vietnam’s

Ho Chi Minh Index dropped led by selloff in banks. Hong Kong ended marginally higher, while markets in mainland China were shut for a week-long holiday. South Korean inflation rose 3.7% from a year ago in September, while consumer prices in the Philippines

climbed 6.1%, both above forecasts. In Thailand, price gains slowed. India’s services activity strengthened month on month. Taiwan’s inflation rate rose more than expected. Topix +2%, Taiwan +1.1%, Sensex +0.6%, ASX 200 +0.5%, Hang Seng +0.1%. Philippines

-1.9%, Vietnam -1.3%, Kospi -0.1%.

FIXED INCOME:

Treasuries are mixed in early US trading with the yield curve steepening further as front-end outperforms. Similar price action in core European rate markets as crude

oil extends its slide. US 5s30s spread exceeds 17bp, widest since May, while 2s10s inversion lessens further to -31bps, nearing the March high.10 year yield ~4.725%, 2 year ~5.03%.

METALS:

Gold steadied near its lowest level since March after benchmark Treasury yields eased from a 16-year high following weak jobs data from the US. Bullion remains vulnerable to further investor

selling prompted by the Federal Reserve signaling monetary policy would remain tighter for longer. Markets may get a clearer picture of the labor market from Friday’s nonfarm payrolls figures, which are forecast to show a slight slowdown in hiring. Spot gold

is flat, silver +0.5%.

ENERGY:

Oil prices remain under pressure this morning after suffering the biggest one-day drop in over a year, as an uncertain demand outlook held off any boost from OPEC+

maintaining oil output cuts to keep a tight supply. Concerns over the dent to oil demand from higher interest rates and a global slowdown, along with weak US seasonal gasoline demand, drove WTI down by 5%-plus, the largest amount since 2022. The reversal of

crude’s recent rally probably pushed OPEC+ to stay the course on output cuts, Citi said. JPMorgan analysts expect crude demand to decline this quarter following the recent rally. Australian LNG workers will meet today after raising complaints over the terms

of a deal to end strikes at Chevron facilities. WTI -1.5%, Brent -1.3%, US Nat Gas +1.9%, RBOB +0.5% after testing its key 200 week moving average.

CURRENCIES:

The dollar inched lower amid relatively thin flows with traders focused on Friday’s US jobs report, but strategists say the pullback may just be temporary. The dollar

has strengthened against all of its Group-of-10 peers in the past six months, with the yen and New Zealand dollar leading losses. Authorities from Japan to South Korea have been seeking to bolster their currencies as the surging greenback threatens to fan

inflationary pressures. Earlier this week, analysts speculated that Japanese authorities may have intervened to support the currency, but Bank of Japan money market data showed on Wednesday that they most likely had not intervened. US $Index -0.1%, GBPUSD

is flat, USDJPY -0.15%, EURUSD +0.1%, AUDUSD +0.3%, USDCAD +0.2%, NZDUSD +0.5%.

Bitcoin +0.4%, Ethereum -0.2%.

TECHNICAL LEVELS:

|

ESZ23 |

10 Year Yield |

Dec Gold |

Nov WTI |

Spot $ Index |

|

|

Resistance |

4399.00 |

|

1982.5 |

93.71 |

111.525 |

|

|

4371/74 |

5.500% |

1936.5 |

92.25 |

110.000 |

|

|

4342.00 |

5.325% |

1913.5 |

90.90 |

108.970 |

|

|

4319.50 |

5.000% |

1900.0 |

88.30 |

107.990 |

|

|

4304.00 |

4.810% |

1865.0 |

85.00 |

107.350 |

|

Settlement |

4297.75 |

1834.8 |

84.22 |

||

|

|

4277.00 |

4.700% |

1831.0 |

83.22 |

105.380 |

|

|

4261.50 |

4.500% |

1821.0 |

81.50 |

104.420 |

|

|

4231.00 |

4.250% |

1800.0 |

80.00 |

103.800 |

|

|

4200/01* |

4.000% |

1796.7* |

77.54 |

103.100 |

|

Support |

4165/75 |

3.800% |

1776.5 |

75.92 |

102.920 |

Colors within the report:

Green is always the 200 period (day, week).

Red is always 21,

Blue = 50,

Brown =

100 *Stars have added importance

- Upgrades

- (AMXB MM) America Movil ADRs Raised to Buy at BofA

- (BECN) Beacon Roofing Raised to Outperform at RBC; PT $94

- (CCL) Carnival Raised to Hold at Shore Capital

- (CMS) CMS Energy Raised to Overweight at KeyBanc; PT $57

- (CNP) CenterPoint Energy Raised to Overweight at KeyBanc; PT $29

- (DTE) DTE Energy Raised to Overweight at KeyBanc; PT $106

- (ETR) Entergy Raised to Overweight at KeyBanc; PT $97

- (ISTR) Investar Holding Raised to Overweight at Piper Sandler

- (LOB) Live Oak Banc Raised to Overweight at JPMorgan; PT $40

- (ORLY) O’Reilly Automotive Raised to Buy at Citi; PT $1,040

- (PB) Prosperity Banc Raised to Strong Buy at Raymond James

- (PNW) Pinnacle West Capital Raised to Sector Weight at KeyBanc

- (TLEVICPO MM) Televisa ADRs Raised to Buy at BofA; PT $4.70

- (UWMC) UWM Holdings Raised to Buy at BTIG; PT $6

- Downgrades

- (AYI) Acuity Brands Cut to Sell at CFRA; PT $174

- (BTAI) Bioxcel Therapeutics Cut to Hold at Truist Secs

- (CLX) Clorox Cut to Market Perform at Raymond James

- (CMA) Comerica Cut to Outperform at Raymond James; PT $53

- (CMBM) Cambium Networks Cut to Market Perform at JMP

- (CMBM) Cut to Market Perform at Oppenheimer

- (FND) Floor & Decor Cut to Neutral at Citi; PT $90

- (HEO CN) H2O Innovation Cut to Hold at Canaccord; PT C$4.25

- (KZR) Kezar Life Sciences Cut to Hold at JonesTrading

- (NEE) NextEra Energy Cut to Sector Weight at KeyBanc

- (NU) Nubank Cut to Neutral at New Street Research; PT $8.10

- (PAY) Paymentus Cut to Neutral at Citi; PT $17

- (SLGC) SomaLogic Cut to Hold at Jefferies; PT $2.30

- (TSCO) Tractor Supply Cut to Neutral at Citi; PT $207

- (VAC) Marriott Vacations Cut to Hold at Jefferies; PT $112

- Initiations

- (ACGL) Arch Capital Reinstated Buy at Deutsche Bank; PT $103

- (AIG) AIG Reinstated Buy at Deutsche Bank; PT $79

- (AJG) Arthur J Gallagher Reinstated Buy at Deutsche Bank; PT $277

- (ALPN) Alpine Immune Rated New Outperform at RBC; PT $19

- (AME) Ametek Rated New Neutral at BNPP Exane; PT $159

- (AON) Aon PLC Reinstated Hold at Deutsche Bank; PT $361

- (APH) Amphenol Rated New Outperform at BNPP Exane; PT $93

- (ARES) Ares Management Rated New Outperform at Wolfe; PT $133

- (BX) Blackstone Rated New Peerperform at Wolfe

- (CART) Instacart Rated New Market Perform at Bernstein; PT $30

- (CB) Chubb Reinstated Buy at Deutsche Bank; PT $269

- (CG) Carlyle Group Rated New Peerperform at Wolfe

- (CGNX) Cognex Rated New Outperform at BNPP Exane; PT $55

- (CRBG) Corebridge Financial Rated New Hold at Deutsche Bank; PT $24

- (CSLR) Complete Solaria Rated New Buy at Janney Montgomery; PT $7

- (DINO) HF Sinclair Rated New Outperform at BMO; PT $65

- (EQH) Equitable Holdings Reinstated Hold at Deutsche Bank; PT $31

- (FCNCA) First Citizens Rated New Outperform at Wedbush; PT $1,700

- (FHN) First Horizon Rated New Neutral at Wedbush; PT $12

- (FTV) Fortive Rated New Outperform at BNPP Exane; PT $91

- (GGG) Graco Rated New Neutral at BNPP Exane; PT $73

- (HIG) Hartford Financial Reinstated Hold at Deutsche Bank; PT $85

- (HWM) Howmet Aerospace Rated New Neutral at Northcoast

- (IEX) Idex Rated New Neutral at BNPP Exane; PT $200

- (JNJ) J&J Rated New Outperform at RBC; PT $178

- (KEY CN) Keyera Rated New Buy at Citi; PT C$35

- (KKR) KKR & Co. Rated New Outperform at Wolfe; PT $75

- (LTH CN) Lithium Ionic Rated New Buy at Desjardins; PT C$5.25

- (MET) MetLife Reinstated Hold at Deutsche Bank; PT $71

- (MMC) Marsh & McLennan Reinstated Buy at Deutsche Bank; PT $226

- (NDSN) Nordson Rated New Outperform at BNPP Exane; PT $275

- (OCS) Oculis Holding Rated New Buy at Stifel; PT $35

- (OWL) Blue Owl Capital Rated New Outperform at Wolfe; PT $16

- (PBF) PBF Energy Rated New Outperform at BMO; PT $60

- (PPL CN) Pembina Pipeline Rated New Neutral at Citi; PT C$42

- (PRU) Prudential Financial Reinstated Hold at Deutsche Bank; PT $99

- (REXR) Rexford Industrial Rated New Buy at Colliers; PT $60

- (TDY) Teledyne Rated New Outperform at BNPP Exane; PT $530

- (TRV) Travelers Reinstated Hold at Deutsche Bank; PT $186

- (VSTS) Vestis Rated New Buy at Redburn; PT $29

- (ZBRA) Zebra Tech Rated New Underperform at BNPP Exane; PT $183

Data sources: Bloomberg, Reuters, CQG

No responses yet