TODAY’S GAME PLAN: from the trading

desk, this is not research

DATA/HEADLINES 8:30ET Weekly Jobless Claims, Philly Fed; 9:00ET Fed’s Jefferson speaks; 10:00ET Existing Home

Sales, Leading Index; 12:00ET Fed’s Powell speaks; 1:20ET Fed’s Goolsbee speaks; 1:30ET Fed’s Barr speaks; 4:00ET Fed’s Bostic speaks; 5:30ET Fed’s Harker speaks; 6:40ET Fed’s Logan speaks

TODAY’S HIGHLIGHTS:

- Israeli air strike kills head of Hamas led national security forces

- Hezbollah, in Lebanon, has an estimated 100,000 missiles and rockets at its disposal

Global shares fell again as rising bond yields and weak earnings news sapped appetite for stocks as traders tracked an intensifying diplomatic push to contain the

Israel-Hamas war. UK Prime Minister Rishi Sunak is meeting Israel officials today, as efforts intensify to contain the Israel-Hamas war and push for the entry of vital aid to Gaza. United Nations Secretary-General Antonio Guterres is due in Egypt, while Germany’s

top diplomat will visit Jordan, Israel and Lebanon before the weekend. Israel said it will allow aid into southern Gaza only if none will be diverted to Hamas. Israel’s military struck more sites in Gaza, including tunnel shafts, positions for launching anti-tank

missiles and intelligence infrastructure.

EQUITIES:

US equity futures edged lower as investor attention turns to data for fresh readings on the economy and Chair Jerome Powell rounds off another busy day of speeches by Fed officials. President

Biden is considering a supplemental request to Congress of about $100 billion that would include defense assistance for Israel and Ukraine, along with border security funding and aid to nations in the Indo-Pacific, including Taiwan. As the earnings season

gets into full swing, Goldman Sachs strategists “broadly recommend” buying single-stock call options ahead of upcoming third-quarter reports due to “recent upward estimate revisions, upward price target revisions and our view that calls are underpriced versus

the potential for a relief rally.”

Futures ahead of the bell: E-Mini S&P -0.1%, Nasdaq +0.1%, Russell 2000 -0.3%, Dow -0.1%.

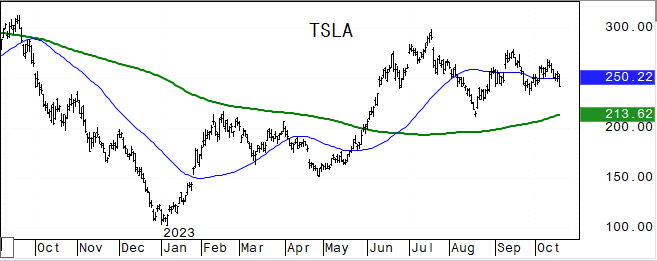

In premarket trading, Tesla slid as much as 5.5% after the electric-vehicle maker’s third-quarter results missed already low expectations. Netflix surged 13% after the streaming-video

company posted its best quarter for subscriber growth in years. Crowdstrike (CRWD) and Zscaler (ZS) rose as Jefferies upgraded their ratings to buy from hold. Lam Research (LRCX) dropped 3% after the chip manufacturing equipment supplier reported a decline

in revenue for a third-straight quarter. Las Vegas Sands (LVS) rose over 5% after the casino operator reported third-quarter adjusted property Ebitda that beat estimates. VMWare (VMW) shares slid 7% after the Financial Times reported Chinese regulators may

hold up its $61 billion acquisition by Broadcom. Blackstone (BX) drops by as much as 4% after the alternative asset manager reported distributable income/share for the third quarter that missed the average analyst estimate. Canada Goose (GOOS) drops 6% as

Cowen and Wells Fargo Securities downgraded the parka retailer to a hold. Equifax (EFX) drops 7.5% after the credit-reporting agency cut its adjusted earnings-per-share guidance for the full year. Peloton Interactive (PTON) drops 6.9% after BofA Global Research

downgraded its rating to underperform from neutral.

European equities fell for a third day as rising Treasury yields put pressure on risk assets across the world, and earnings reports from some of the region’s biggest companies disappointed.

Drugmaker Roche Holding AG dropped the most in almost a year on its cautious outlook. Renault slipped after reporting results that missed consensus estimates. Nestle SA shares declined after reporting the slowest sales growth in almost three years. The Stoxx

Europe 600 Index is down 0.9%, with healthcare, REITs and auto stocks declining the most. Shares in the region have been hit this week, with investors rotating into defensive sectors and value stocks. DAX -0.3%, CAC -0.7%, FTSE 100 -1%. REITs -2%, Autos -1.9%,

Healthcare -1.8%. Technology +1.2%.

Asian stocks plunged, driven by losses in China. The MSCI Asia Pacific Index declined 1.6%, with Tencent, Alibaba and Samsung leading the decline. China’s CSI 300 Index slid the most

in over two months, extending losses from Wednesday, when the country’s latest economic data showed the housing crisis remains a major drag even as growth surpassed expectations. Hong Kong’s heavyweight developers also dropped amid a report home purchase tax

cuts could be smaller than expected. JPMorgan upgraded China’s growth forecast to 5.2% this year and 4.7% in 2024 after the latest GDP beat. Japan’s exports rose more than expected in September and Australian employment came in weaker than expected. South

Korea’s Kospi lost almost 2% as the central bank held interest rates steady and flagged upside risks to inflation. Taiwan’s benchmark erased the day’s losses to close higher after TSMC jumped as projected revenue and capital spending came in ahead of analysts’

expectations, signaling a long awaited chip recovery. Taiwan +0.1%, Hang Seng Index -2.5%, CSI 300 -2.1%, Nikkei 225 -1.9%, Kospi -1.9%, Vietnam -1.4%, ASX 200 -1.4%, Sensex -0.4%.

FIXED INCOME:

Treasuries are cheaper across the curve with losses led by long-end. 10 year yield gained for a fourth day, closing in on 5% while 30 year yield hit its highest level

since 2007. US Treasuries have not been fulfilling their usual safe-haven role in recent days, with strong US data trumping worries about a deepening conflict in the Middle East. Federal Reserve Bank of New York President John Williams said interest rates

would have to stay at restrictive levels “for some time.” US yields cheaper by more than 6bp at long-end, widening 2s10s by 3bps. 10 year yield ~4.97%, 2 year yield 5.25%.

METALS:

Gold is slightly higher on haven demand after delivering gains of almost 7% since the October 7 attack by Hamas on Israel. Still, gold’s rebound from a seven-month low set earlier in

October has yet to draw in significant purchases through exchange-traded funds. Rising Treasury yields are curbing the upside for the metal. Spot gold +0.25%, silver +0.3%.

ENERGY:

Oil prices slipped as traders tracked developments in the Middle East and the US eased crude sanctions against Venezuela, potentially aiding global supply. The move

signals the country is on the brink of being able to pump 200,000 more barrels of crude a day, a roughly 25% jump, according to analysts. Meanwhile, OPEC+ showed no signs of supporting the call of fellow member Iran for an oil embargo on Israel. Japan, the

world’s fourth-largest crude buyer, urged Saudi Arabia and other oil producing nations to increase supplies to stabilize the global oil market. WTI -1%, Brent -1.1%, US Nat Gas -1.5%, RBOB -0.8%.

CURRENCIES:

The dollar fluctuated, while the yen strengthened slightly as Japan’s exports rose more than expected in September. Bank Indonesia raised its key rate to 6% from

5.75%, surprising markets as it aimed to bolster the rupiah amid risks from Middle East tensions. Chinese investors offloaded the most US bonds and stocks in four years in August, fueling speculation the authorities may have moved to beef up their war chest

to defend a weakening yuan. US$ Index -0.1%, GBPUSD -0.1%, EURUSD +0.3%, USDJPY -0.1%, AUDUSD -0.3%, USDNOK +0.3%.

Bitcoin %, Ethereum %.

TECHNICAL LEVELS:

|

ESZ23 |

10 Year Yield |

Dec Gold |

Nov WTI |

Spot $ Index |

|

|

Resistance |

4500/04 |

|

2029.9 |

95.03 |

110.000 |

|

|

4482.00 |

5.750% |

2010.9 |

93.10 |

108.970 |

|

|

4461.00 |

5.500% |

2000.0 |

92.13 |

107.990 |

|

|

4235.00 |

5.325% |

1981/85 |

89.86 |

107.350 |

|

|

4420.00 |

5.000% |

1976.5 |

88.57 |

106.785 |

|

Settlement |

4342.25 |

1968.3 |

87.27 |

||

|

|

4319.50 |

4.500% |

1941.5 |

85.40 |

105.535 |

|

|

4310.00 |

4.350% |

1921.2 |

84.20 |

105.000 |

|

|

4277.00 |

4.000% |

1881.7 |

81.50 |

104.380* |

|

|

4256.00 |

3.835% |

1856.0 |

79.35 |

103.800 |

|

Support |

4235.50 |

3.500% |

1821/23 |

77.75 |

103.180 |

Colors within the report:

Green is always the 200 period (day, week).

Red is always 21,

Blue = 50,

Brown =

100 *Stars have added importance

- Upgrades

- (APTV) Aptiv Raised to Overweight at JPMorgan; PT $145

- (BBY) Best Buy Raised to Buy at Goldman; PT $85

- (CRWD) CrowdStrike Raised to Buy at Jefferies; PT $225

- (FIS) Fidelity National Raised to Overweight at Barclays; PT $69

- (FSLR) First Solar Raised to Overweight at JPMorgan; PT $220

- (JUSH CN) Jushi Holdings Raised to Buy at Canaccord; PT C$1.71

- (KTB) Kontoor Brands Raised to Buy at Goldman; PT $56

- (NFLX) Netflix Raised to Overweight at KeyBanc; PT $510

- (PEY CN) Peyto Exploration Raised to Outperform at CIBC; PT C$18

- (PPL CN) Pembina Pipeline Raised to Outperform at CIBC; PT C$51

- (RCM) RCM Raised to Buy at Truist Secs; PT $18

- (SMTC) Semtech Raised to Buy at Benchmark; PT $30

- (SOFI) SoFi Technologies Raised to Market Perform at KBW; PT $7.50

- (SPR) Spirit Aero Raised to Buy at Deutsche Bank

- (U) Unity Software Raised to Hold at Jefferies; PT $27

- (XYL) Xylem Raised to Outperform at Oppenheimer; PT $118

- (ZS) Zscaler Raised to Buy at Jefferies; PT $225

- Downgrades

- (BBCP) Concrete Pumping Cut to Neutral at Baird; PT $8.50

- (BYD CN) Boyd Group Services Cut to Sell at Goldman; PT C$225

- (DADA) Dada Nexus ADRs Cut to Equal-Weight at Morgan Stanley; PT $4.78

- (DHT) DHT Holdings Cut to Hold at Stifel; PT $11

- (ENPH) Enphase Energy Cut to Sector Perform at Scotiabank; PT $140

- (FL) Foot Locker Cut to Sell at Goldman; PT $18

- (FOXA) Fox Corp Cut to Underweight at Huber Research Partners; PT $32

- (FTNT) Fortinet Cut to Hold at Jefferies; PT $65

- (GBIO) Generation Bio Cut to Market Perform at Cowen

- (GOOS CN) Canada Goose Cut to Market Perform at Cowen

- (GOOS CN) Cut to Equal-Weight at Wells Fargo

- (GPK) Graphic Packaging Cut to Underweight at Wells Fargo; PT $19

- (KEY CN) Keyera Cut to Neutral at CIBC; PT C$33

- (MCRI) Monarch Casino Cut to Hold at Truist Secs; PT $65

- (MXL) MaxLinear Cut to Hold at Deutsche Bank; PT $23

- (NTRS) Northern Trust Cut to Equal-Weight at Wells Fargo; PT $71

- (PTON) Peloton Cut to Underperform at BofA; PT $4.15

- (PXD) Pioneer Natural Cut to Market Perform at Cowen; PT $256

- (TSLA) Tesla Cut to Neutral at Fubon; PT $275

- (UCBI) United Community Banks Cut to Neutral at Piper Sandler; PT $27

- (WBX) Wallbox Cut to Neutral at Chardan Capital Markets; PT $2.25

- Initiations

- (AVTR) Avantor Rated New Buy at Baptista Research; PT $27.70

- (BLMN) Bloomin’ Brands Reinstated Hold at Deutsche Bank; PT $25

- (CABA) Cabaletta Bio Rated New Buy at Stifel; PT $31

- (CAKE) Cheesecake Factory Reinstated Hold at Deutsche Bank; PT $32

- (CHWY) Chewy Reinstated Underperform at BofA; PT $16

- (CMG) Chipotle Reinstated Buy at Deutsche Bank; PT $2,375

- (DPZ) Domino’s Pizza Reinstated Buy at Deutsche Bank; PT $430

- (DRI) Darden Reinstated Buy at Deutsche Bank; PT $159

- (EFC) Ellington Financial Inc Reinstated Buy at B Riley; PT $15

- (FTRE) Fortrea Rated New Neutral at Citi; PT $32

- (GPCR) Structure Therapeutics ADRs Rated New Market Outperform at JMP

- (GRCL) Gracell Biotech ADRs Rated New Buy at Stifel; PT $11

- (INTU) Intuit Rated New Neutral at President Capital Management

- (JACK) Jack in the Box Reinstated Hold at Deutsche Bank; PT $71

- (LAC CN) Lithium Americas Rated New Buy at Eight Capital; PT C$22.65

- (MCD) McDonald’s Reinstated Buy at Deutsche Bank; PT $287

- (NTST) Netstreit Rated New Neutral at Mizuho Securities; PT $15

- (PFGC) Performance Food Rated New Buy at Deutsche Bank; PT $80

- (PZZA) Papa John’s Reinstated Hold at Deutsche Bank; PT $71

- (QSR CN) Restaurant Brands Rated New Buy at Deutsche Bank; PT $75

- (SBUX) Starbucks Reinstated Buy at Deutsche Bank; PT $118

- (SHAK) Shake Shack Reinstated Hold at Deutsche Bank; PT $62

- (SYY) Sysco Reinstated Buy at Deutsche Bank; PT $75

- (TRGP) Targa Resources Rated New Outperform at Haitong Intl; PT $116.95

- (TXRH) Texas Roadhouse Reinstated Buy at Deutsche Bank; PT $111

- (WEN) Wendy’s Reinstated Hold at Deutsche Bank; PT $20

- (YUM) Yum Reinstated Hold at Deutsche Bank; PT $131

Data sources: Bloomberg, Reuters, CQG

No responses yet