TODAY’S GAME PLAN: from the trading

desk, this is not research

DATA/HEADLINES 8:30ET Chicago Fed National Activity Index,

Philadelphia Fed Non-Manufacturing Activity; 10:00ET Existing Home Sales; 1:00ET $15 billion 10-year TIPS auction; 2:00ET FOMC Meeting Minutes

TODAY’S HIGHLIGHTS:

- ISRAEL-HAMAS DEAL ON 50 HOSTAGES CAN BE ANNOUNCED TODAY: CNN

World stocks were subdued as investors awaited the Federal Reserve’s policy minutes and after the Bank of England warned that rates may have to rise again. Emerging-market

stocks and currencies extended gains as the weakening dollar spurred demand for risk assets. MSCI’s index of developing-nation stocks climbed to the highest level in almost three months, led by technology companies. Hamas said they are close to reaching a

“truce agreement” with Israel in rare public comments that suggest talks over freeing some hostages are progressing and could lead to a limited pause in fighting. Qatar, which hosts some of Hamas’s political leaders, is helping broker the talks. Hamas has

agreed in principle for more than 50 women and children to be released, Axios reported. In return, Israel would pause its military attacks for a specified time each day and release some Palestinians in Israeli jails.

EQUITIES:

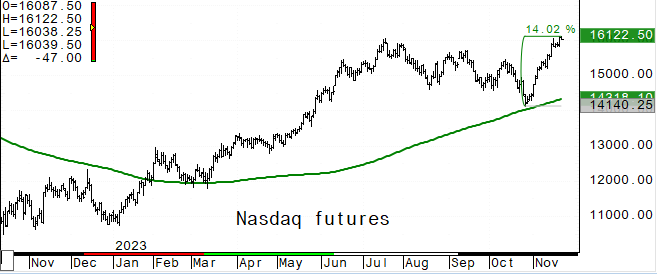

US equity futures are slightly lower after the Nasdaq 100 hit a 22-month high on Monday, driven by Nvidia. With big tech driving this year’s rally, the focus will

also be on the earnings from chipmaker Nvidia, whose shares rose 2.3% on Monday to a record. Options prices indicate the stock could move as much as 8% in either direction. The company looks set to post another sales surge when it reports post-market. Goldman

Sachs strategists said there is a risk of “disappointment in the near term” amid lingering concerns about economic growth and inflation. By contrast, Bank of America technical strategists wrote that US stocks might have “much more upside potential” as they

approach decisive bullish breakouts. The VIX Index of US stock-market volatility held near this year’s lows.

Futures ahead of the bell: E-Mini S&P -0.2%, Nasdaq -0.3%, Russell 2000 -0.6%, Dow -0.2%.

In pre-market trading, Lowe’s fell 6% after cutting its full-year revenue forecast again. Same-store sales fell 7.4% in the third quarter, the fourth consecutive decline. Agilent Technologies

(A) jumped more than 6% after an earnings beat, while Gen Digital gained 3.5% after Morgan Stanley lifted its rating on the cybersecurity company’s stock. CRH (CRH) rose 3% after agreeing to buy a portfolio of concrete assets in Texas from Martin Marietta

Materials. Kohl’s (KSS) fell over 4%, set for a second day of declines, after the department store operator announced that President and COO Dave Alves departed the company. Symbotic (SYM) shares jump 25% after the warehouse automation company reported fourth-quarter

revenue that beat estimates and raised guidance. Zoom (ZM) shares were down 1% after third-quarter earnings beat expectations and it raised its full-year forecast. But brokers, however, are looking for more signs of stabilization, especially given the tough

macroeconomic backdrop. Best Buy (BBY) slips 4.8% after same-store sales fell by more than expected in the third quarter. Dick’s Sporting Goods

(DKS) rises 8.4% after the retailer reported an unexpected increase in third-quarter comparable sales and boosted its annual forecasts. Hibbett Inc. (HIBB) rises 14% after the sporting goods retailer reported EPS and sales that topped consensus estimates.

European shares were muted with the economic calendar bare in Europe. ECB’s Simkus indicated “markets expectations of rate cuts are too optimistic.” The Stoxx 600 is slightly lower as

losses in REITs outweigh gains in the retail sector. Among individual movers, Banca Monte dei Paschi di Siena SpA dropped 8% after Italy sold about 25% of its stake for approximately €920 million ($1 billion) as part of its plan to divest from the bailed out

lender. MorphoSys AG plunged 25% after the German biotech firm announced mixed results in a trial for a drug to treat myelofibrosis. Swiss medical devices firm Sonova Holding AG jumped over 6% after reporting results. Stoxx 600 -0.1%, DAX +0.05%, CAC -0.3%,

FTSE 100 -0.5%. Retail +0.8%, Construction +0.5%, Food & Bev +0.4%. REITs -1.3%, Autos -0.9%, Energy -0.9%, Banks -0.8%.

Shares in Asia advanced, led by Taiwan, as technology shares rose amid the dollar’s fall and the continued improvement in risk sentiment. The MSCI Asia Pacific Index rose 0.6% to its

highest close in about two months and artificial intelligence-related companies climbed ahead of Nvidia’s earnings results. After the close, Baidu’s results beat on its expansion into new businesses such as AI. Chinese developers gained after authorities began

drafting a list of 50 real estate firms that would be eligible for a range of financing as Beijing sought to support the property sector. The PBOC encouraged lenders to cap the amount of new loans they issue in early 2024 and shift some forward to this year.

Taiwan +1.55%, Kospi +0.8%, Vietnam +0.6%, Sensex +0.4%, ASX 200 +0.3%, CSI 300 +0.1%, Topix -0.2%, Hang Seng Index -0.25%, Singapore -0.5%.

FIXED INCOME:

Treasury yields edged lower after a strong 20-year auction in the previous session that suggested the market still anticipates inflation will decelerate and the Fed

will cut rates next year. Treasuries are slightly cheaper across the curve with long-end continuing Monday’s outperformance. Markets are pricing in about a 30% chance of a Fed rate cut in March. Minutes of the last rate-setting meeting, due to be published

later today, may provide more insights into policy makers’ thinking. 10-year yield around 4.41%, 2 year yield ~4.9%, curve slightly flatter.

METALS:

Gold rose to a two-week high as the dollar extended a slide on bets that the Federal Reserve will pivot to interest-rate cuts next year. The leader of Hamas said

his group was close to reaching a “truce agreement” with Israel, suggesting talks over freeing some hostages held by the Gaza-based group are progressing. That could further unwind gold’s war-risk premium. Spot gold +0.5%, silver +0.5%.

ENERGY:

Oil pared a two-day gain that was driven by speculation OPEC+ may deepen supply cuts at a meeting this weekend. Russia cut back its seaborne crude exports to the

lowest since August before a meeting of OPEC+ oil minsters this weekend when compliance with production cuts will be in sharp focus. Ahead of the weekend meeting, fresh US data on crude and product stockpiles will be released, while indications of expanding

non-OPEC crude supplies have countered OPEC+ production cuts. Italy boosted its crude oil imports from the US in September to the highest level in at least four years, in a sign of how European refiners have increasingly turned to American supply. WTI -0.2%,

Brent -0.2%, US Nat Gas -0.2%, RBOB -0.4%.

CURRENCIES:

The dollar is down for a fourth day due to risk-on flows, reports on Chinese stimulus, and a potential truce agreement in Gaza. The Aussi Dollar rose after the Reserve

Bank of Australia’s November policy meeting minutes showed the central bank’s projections were based on one to two more rate hikes. The Japanese yen strengthened, lifting further away from the one-year low it touched last week. China’s yuan rose to its highest

since July in both the offshore and onshore markets, gaining from a much stronger midpoint fixing. US$ Index -0.1%, GBPUSD +0.2%, USDJPY -0.5%, EURUSD +0.05%, AUDUSD +0.3%, NZDUSD +0.6%.

Bitcoin -0.6%, Ethereum -0.9%.

TECHNICAL LEVELS:

|

ESZ23 |

10 Year Yield |

Dec Gold |

Jan WTI |

Spot $ Index |

|

|

Resistance |

4652.00 |

5.500% |

|

86.29 |

107.990 |

|

|

4624.00 |

5.325% |

2056.0 |

84.57 |

107.350 |

|

|

4611.00 |

5.000% |

2029.4 |

80.90 |

106.450 |

|

|

4597.50 |

4.775% |

2019.7 |

80.10 |

105.800 |

|

|

4571.00 |

4.615% |

1998.0 |

78.19 |

104.750 |

|

Settlement |

4562.25 |

1980.3 |

77.83 |

||

|

|

4540/41 |

4.350% |

1958.8 |

72.16 |

103.620 |

|

|

4518.00 |

3.930% |

1949.9 |

70.04w |

102.550 |

|

|

4500.00 |

3.640% |

1941.1 |

66.80 |

101.240 |

|

|

4470.00 |

3.245% |

1921.5 |

65.00 |

100.000 |

|

Support |

4439.00 |

3.000% |

1898.4 |

63.64 |

99.580 |

Colors within the report:

Green is always the 200 period (day, week).

Red is always 21,

Blue = 50,

Brown =

100 *Stars have added importance

- Upgrades

- Black Hills (BKH) Raised to Neutral at Mizuho Securities; PT $53

- C3.ai (AI) Raised to Outperform at Oppenheimer; PT $40

- Celanese (CE) Raised to Neutral at Piper Sandler; PT $135

- Cloudflare (NET) Raised to Outperform at Oppenheimer; PT $85

- DigitalOcean (DOCN) Raised to Outperform at Oppenheimer; PT $37

- Equinix (EQIX) Raised to Outperform at Oppenheimer; PT $875

- Farmers Edge (FDGE CN) Raised to Market Perform at Raymond James

- Gen Digital (GEN) Raised to Overweight at Morgan Stanley; PT $26

- Nova Cannabis Inc (NOVC CN) Raised to Outperform at ATB Capital; PT C$3.50

- Playtika (PLTK) Raised to Buy at Citi

- Vale (VALE3 BZ) ADRs Raised to Buy at Goldman; PT $19.50

- Xylem (XYL) Raised to Buy at Deutsche Bank; PT $120

- Downgrades

- 4Front Ventures Corp (FFNT CN) Cut to Hold at Canaccord

- Agilon Health (AGL) Cut to Hold at Deutsche Bank; PT $12

- CES Energy (CEU CN) Cut to Sector Perform at National Bank; PT C$4.75

- Exelon (EXC) Cut to Neutral at Mizuho Securities; PT $40

- Foot Locker (FL) Cut to Neutral at BTIG

- Hershey (HSY) Cut to Sector Perform at RBC; PT $213

- Incyte (INCY) Cut to Neutral at Goldman; PT $65

- Mainz Biomed (MYNZ) Cut to Neutral at Cantor

- NanoString (NSTG) Cut to Neutral at Baird; PT 75 cents

- National Bank of Canada (NA CN) Cut to Sector Perform at Scotiabank

- Pason Systems (PSI CN) Cut to Sector Perform at National Bank; PT C$20

- Precision Drilling (PD CN) Cut to Sector Perform at National Bank

- Roku (ROKU) Cut to Sell at CFRA; PT $75

- Trican Well Service (TCW CN) Cut to Sector Perform at National Bank

- Waste Connections (WCN CN) Cut to Peerperform at Wolfe

- Zions (ZION) Cut to Neutral at Citi; PT $37

- Initiations

- ACI Worldwide (ACIW) Rated New Buy at Seaport Global Securities; PT $31

- Advanced Energy (AEIS) Rated New Equal-Weight at Wells Fargo; PT $100

- Array (ARRY) Rated New Neutral at Mizuho Securities; PT $19

- Boot Barn (BOOT) Rated New Buy at B Riley; PT $92

- Boyd Group Services (BYD CN) Reinstated Buy at Stifel Canada; PT C$295

- CCL Industries (CCL/B CN) Reinstated Hold at Stifel Canada; PT C$65

- Colliers International (CIGI CN) Rated New Buy at Stifel Canada

- Compass (COMP) Reinstated Hold at Deutsche Bank; PT $2.70

- Enphase Energy (ENPH) Rated New Buy at Mizuho Securities; PT $131

- First Solar (FSLR) Rated New Buy at Mizuho Securities; PT $188

- FirstService (FSV CN) Rated New Buy at Stifel Canada; PT C$240.22

- Hannon Armstrong (HASI) Rated New Buy at Mizuho Securities; PT $30

- Maxeon Solar (MAXN) Rated New Neutral at Mizuho Securities; PT $7

- Newmont Corp (NEM) Rated New Outperform at Macquarie; PT $45

- NFI Group (NFI CN) Reinstated Hold at Stifel Canada; PT C$15

- Opendoor Technologies (OPEN) Rated New Hold at Deutsche Bank; PT $2.80

- Oxford Industries (OXM) Rated New Neutral at BTIG

- Performance Food (PFGC) Reinstated Overweight at Piper Sandler; PT $72

- Premier Financial Corp (PFC) Rated New Market Perform at Hovde Group

- ReNew Energy (RNW) Rated New Buy at Mizuho Securities; PT $8

- Sarepta (SRPT) Reinstated Outperform at Wedbush; PT $224

- Shoals Technologies (SHLS) Rated New Buy at Mizuho Securities; PT $18

- SolarEdge (SEDG) Rated New Buy at Mizuho Securities; PT $108

- Soleno (SLNO) Reinstated Buy at Guggenheim; PT $40

- Strathcona Resources (SCR CN) Rated New Sector Perform at Peters & Co

- Sunnova Energy (NOVA) Rated New Buy at Mizuho Securities; PT $20

- SunPower (SPWR) Rated New Neutral at Mizuho Securities; PT $5

- Sunrun (RUN) Rated New Buy at Mizuho Securities; PT $23

- Superior Plus (SPB CN) Rated New Buy at Stifel Canada; PT C$13

- Sysco (SYY) Reinstated Neutral at Piper Sandler; PT $73

- Talos Energy (TALO) Rated New Buy at Canaccord; PT $24

- US Foods Holding (USFD) Reinstated Neutral at Piper Sandler; PT $45

- Vestis (VSTS) Rated New Buy at Jefferies; PT $20

- Vinfast Auto Ltd (VFS) Rated New Outperform at Wedbush; PT $12

- Zillow (ZG) Rated New Buy at Deutsche Bank; PT $50

Data sources: Bloomberg, Reuters, CQG

No responses yet