TODAY’S GAME PLAN: from

the trading desk, this is not research

DATA/HEADLINES ET: 10:00 a.m: US Oct. New Home Sales, 10:30 a.m: US Nov. Dallas Fed Manufacturing

Activity,11:30 a.m: US to sell $68 billion 26-week bills and $54 billion 2-year notes,1:00 pm: US to sell $75 billion 13-week bills and $55 billion 5-year notes

TODAY’S HIGHLIGHTS:

- NASA warns of solar storm hitting Earth amid increased activity, fiery eruptions on Sun

- Black Friday shoppers sent a record $9.8 billion online in the US, Adobe Analytics reported

- Michigan returned to No. 2 and received 10 first-place votes after beating Ohio State 30-24 in Ann Arbor on Saturday.

World stocks were a touch lower on Monday following a weak session out of Asia where news that profits of China’s industrial companies increased by just 2.7% for the year to

October raised concerns about deflation in the world’s second biggest economy, damping sentiment across the region. Meanwhile, Israel and Hamas signaled that a temporary cease-fire in Gaza could be extended beyond Monday. Treasury yields gained, touching the

highest in a week. The dollar weakened with oil, while gold advanced to the highest since May.

EQUITIES:

US equity futures edged lower and set to pause their recent rally on Monday, influenced by a slowdown in Chinese industrial profits that tempered optimism for the global economic

recovery. Crown Castle rose 4.9% on reports of activist investor Elliott Investment Management planning changes. Foot Locker shares fell 3.9% after a downgrade by Citi, anticipating weaker Q3 earnings. Shopify shares surged 3.1% as the e-commerce company reported

a record $4.1 billion in Black Friday sales. Conversely, GE HealthCare Technologies dropped 2.7% after receiving a sell rating from UBS, citing unappealing risk/reward in the near term. Notable premarket movers: Crown Castle (CCI US) +3.7%, Kenvue (KVUE US)

+2.0%, Newmont Corp (NEM US) +1.0%, Nubank (NU US) +0.9%. Halliburton (HAL US) -1.2%, Coinbase (COIN US) -1.9%, GE Healthcare (GEHC US) -2.7%.

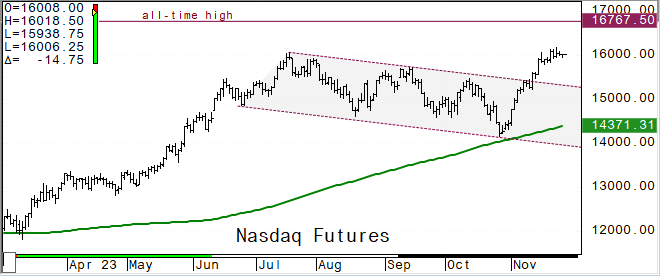

Futures ahead of the bell: E-Mini S&P -0.1%, Nasdaq -0.03%, Russell 2000 -0.3%, Dow -0.1%.

European stocks were slightly lower after a second-week rally as traders evaluated monetary policy paths and anticipated upcoming inflation data. The Stoxx Europe 600 Index dipped

slightly, with energy stocks lagging due to falling oil prices. Individual movements included BASF SE declining after a rating cut and Julius Baer Group Ltd. shares dropping amid a review of its private debt business. Inflation gauges in the US and Eurozone

are expected to show modest annual increases, supporting the belief that interest rates won’t rise soon. European stocks are poised for the best month since January, but warning signals, like elevated bond volatility, raise caution as the rally enters December.

Investors are cautious ahead of significant inflation data influencing the ECB policy meeting on December 14. Notably, European oil and gas stocks are watched closely amid falling oil prices and the delayed OPEC+ meeting this week. Stoxx 600 -0.1%, DAX -0.1%,

CAC was flat, FTSE 100 -0.2%.

Asian stocks declined, driven by concerns about China’s economic health, but losses narrowed following reports that President Xi Jinping will meet tech companies in Shanghai. The MSCI

Asia Pacific Index fell up to 0.5%, with TSMC and Toyota Motor as major drags. China’s CSI 300 Index dropped as industrial profit growth slowed, signaling fragility despite policy efforts. Xi’s reported visit to tech firms, including semiconductor stocks,

prompted a rally. Despite the losses, the Asian equity benchmark is set to break a three-month losing streak, boosted by a less hawkish Federal Reserve and China’s policy support. Notably, Malaysia’s tourism-related stocks gained after announcing the removal

of entry visa requirements for Chinese and Indian citizens starting December 1. Key events this week include China’s PMI and the Fed’s inflation gauge. Singapore -0.1%, Topix -0.4%, Vietnam -0.7%, Sensex -0.1%, Kospi -0.04%, ASX 200 -0.7%, Taiwan -0.9%, Thailand

-0.1%, Indonesia +1%, CSI 300 –0.7%.

FIXED INCOME:

Treasuries were little changed with yields within 1bp of Friday’s closing levels. Core European bonds outperform, led by gilts after dovish comments from BOE Governor Andrew Bailey, who

said recent inflation figures were “very good news.” Main focal point of US session is supply as two coupon auctions are slated — 2-year and 5-year notes. US 10-year yields were around 4.465%, trailing bunds and gilts outperforming by 4bp and 2.5bp in the

sector; curve spreads are also within 1bp of Friday close levels

METALS:

Gold prices climbed to the highest since May, as the dollar continued to weaken ahead of Treasury auctions that are expected to indicate whether the US bond market is set for a meaningful

revival. Gold +0.6%, Silver +1.5%.

ENERGY:

Oil prices dipped below $80 a barrel as investors brace for a pivotal OPEC+ meeting on November 30, postponed from Sunday. Concerns about global crude supplies arise, as African

oil producers aim for higher caps in 2024. Reports hint at the possibility of Saudi Arabia extending its voluntary 1 million bpd production cut beyond December, contributing to market uncertainty. WTI -0.8%, Brent -0.8%

CURRENCIES:

In currency markets, the US dollar index slipped as much as 0.2% and was headed for a monthly loss of more than 3%, its worst performance in a year. Elsewhere, the

pound rose against the weaker dollar to a more than two-month high, extending its gains from last week following data showing that British companies unexpectedly reported a marginal return to growth in November after three months of contraction. The Australian

dollar climbed to a more than three-month high, while the kiwi edged 0.3% higher before the RBNZ interest rate decision on Wednesday, where the central bank is seen keeping rates unchanged at 5.5%, as they have been since the last adjustment in May.US$ Index

-0.2%, GBPUSD +0.3%, USDJPY +0.4%, EURUSD +0.1%, AUDUSD +0.3%, USDNOK +0.6%.

Bitcoin and other cryptocurrencies slipped back on Monday, with recent 18-month highs for digital assets proving hard to hold. Bitcoin -1.6%, Ethereum -2.6%.

TECHNICAL LEVELS:

|

ESZ23 |

10 Year Yield |

Dec Gold |

Jan WTI |

Spot $ Index |

|

|

Resistance |

4652.00 |

5.500% |

2100.0 |

86.29 |

107.990 |

|

|

4624.00 |

5.325% |

2085.4 |

84.57 |

107.350 |

|

|

4611.00 |

5.000% |

2056.0 |

80.90 |

106.450 |

|

|

4597.50 |

4.775% |

2029.4 |

80.10 |

105.800 |

|

|

4571.00 |

4.620% |

2019.7 |

78.18 |

104.750 |

|

Settlement |

4568.25 |

2003.0 |

75.54 |

||

|

|

4540/41 |

4.350% |

1981.5 |

75.00 |

103.620 |

|

|

4518.00 |

3.990% |

1963.9 |

72.16 |

102.550 |

|

|

4500.00 |

3.640% |

1950.6 |

70.16w |

101.240 |

|

|

4470.00 |

3.245% |

1944.0 |

66.80 |

100.000 |

|

Support |

4439.00 |

3.000% |

1921.5 |

65.00 |

99.580 |

Colors within the report:

Green is always the 200 period (day, week).

Red is always 21,

Blue = 50,

Brown =

100 *Stars have added importance

Upgrades

- ARC Resources (ARX

CN) Raised to Buy at Stifel Canada; PT C$26.25 - Carnival (CCL)

Raised to Buy at Melius; PT $19 - Cathedral

Energy Services (CET CN) Raised to Outperform at ATB Capital - HUTCHMED

China (HCM LN) ADRs Raised to Buy at Deutsche Bank; PT $22.10 - Mondelez (MDLZ)

Raised to Outperform at RBC; PT $83 - Roku (ROKU)

Raised to Buy at Cannonball Research; PT $116 - YPF (YPFD

AR) ADRs Raised to Neutral at Goldman; PT $17.10

Downgrades

- Afya (AFYA)

Cut to Neutral at JPMorgan; PT $23 - Ametek (AME)

Cut to Market Perform at Cowen; PT $160 - Canadian

National (CNR CN) Cut to Hold at Deutsche Bank - Canadian

Net Real Estate (NET-U CN) Cut to Hold at Desjardins; PT C$5.25 - Canadian

Pacific Kansas (CP CN) Cut to Hold at Deutsche Bank - Charge Enterprises (CRGE)

Cut to Hold at Maxim - Corteva (CTVA)

Cut to Hold at Berenberg; PT $52 - Deveron (FARM

CN) Cut to Market Perform at Raymond James - Empire Co (EMP/A

CN) Cut to Sector Perform at National Bank; PT C$44 - Firm Capital

Apartment R (FCA/U CN) Cut to Hold at Laurentian Bank - Foot Locker (FL)

Cut to Sell at Citi; PT $18 - Gaotu Techedu (GOTU)

ADRs Cut to Hold at China Renaissance; PT $2.30 - GE Healthcare (GEHC)

Cut to Sell at UBS; PT $66 - Graphic

Packaging (GPK) Cut to Market Perform at Raymond James - LexinFintech (LX)

ADRs Cut to Neutral at Citi; PT $2.12 - Lucid (LCID)

Cut to Hold at Needham - NanoString (NSTG)

Cut to Neutral at JPMorgan - Okta (OKTA)

Cut to Market Perform at JMP - Old Dominion (ODFL)

Cut to Hold at Deutsche Bank; PT $386 - Pioneer

Natural (PXD) Cut to Sell at Argus - Potlatch (PCH)

Cut to Market Perform at Raymond James - Rock Tech

Lithium (RCK CN) Cut to Speculative Buy at Cantor; PT C$2.50 - Southern

Copper (SCCO) Cut to Underweight at Morgan Stanley; PT $68 - Splunk (SPLK)

Cut to Hold at Jefferies; PT $157 - TD Bank (TD

CN) Cut to Market Perform at Cormark Securities; PT C$92 - Telecom

Argentina (TECO2 AR) ADRs Cut to Sector Underperform at Scotiabank - Urban Outfitters (URBN)

Cut to Equal-Weight at Morgan Stanley - Weyerhaeuser (WY)

Cut to Market Perform at Raymond James - Initiations

- Amkor Technology (AMKR)

Rated New Buy at Melius; PT $35 - Arista Networks (ANET)

Rated New Outperform at Haitong Intl; PT $240 - Casella

Waste (CWST) Rated New Overweight at Wells Fargo; PT $95 - D.R. Horton (DHI)

Rated New Hold at Jefferies; PT $119 - Gaotu Techedu (GOTU)

ADRs Reinstated Neutral at Goldman; PT $2.60 - Genelux (GNLX)

Rated New Buy at HC Wainwright; PT $35 - GFL Environmental (GFL

CN) Rated New Equal-Weight at Wells Fargo - Lancaster

Colony (LANC) Rated New Hold at Jefferies; PT $166 - Lennar (LEN)

Rated New Hold at Jefferies; PT $117 - Lifezone

Metals (LZM) Rated New Buy at Roth MKM; PT $14 - Luckin Coffee (LKNCY)

ADRs Rated New Overweight at Guotai Junan Sec - New Oriental

Education (EDU) ADRs Reinstated Buy at Goldman; PT $85 - Pinterest (PINS)

Rated New Buy at New Street Research; PT $48 - PulteGroup (PHM)

Rated New Buy at Jefferies; PT $107 - Republic

Services (RSG) Rated New Overweight at Wells Fargo; PT $180 - Sonnet BioTherapeutics

H (SONN) Rated New Buy at Ladenburg Thalmann - Tal Education (TAL)

ADRs Reinstated Buy at Goldman; PT $11.70 - TECSYS (TCS

CN) Rated New Buy at Echelon Wealth; PT C$45 - Vital Energy

Inc (VTLE) Rated New Buy at Truist Secs; PT $70 - Waste Connections (WCN

CN) Rated New Overweight at Wells Fargo - Wingstop (WING)

Reinstated Buy at William O’Neil - WM (WM)

Rated New Equal-Weight at Wells Fargo; PT $175 - Zepp Health (ZEPP)

ADRs Rated New Buy at Fundamental Research; PT $5.08

Data sources: Bloomberg, Reuters, CQG

No responses yet