TODAY’S GAME PLAN: from the trading

desk, this is not research

DATA/HEADLINES 8:30ET Retail Sales, Weekly Jobless Claims, Import Export Prices; 10:00ET Business Inventories;

2:00ET Mexico Rate Decision

BANK OF ENGLAND MAINTAINS KEY INTEREST RATE AT 5.25%

TODAY’S HIGHLIGHTS:

- Covid Surge Prompts Return of Scanners, Calls for Masks in Asian Cities

- Biden administration may subject 48 new drugs to Medicare rebates

- Poll shows 72% of Palestinians back Oct. 7 attack on Israel, support for Hamas rises – Reuters

- Putin says there will be no peace until his goals in Ukraine are achieved

- Jeffrey Gundlach predicts a drop to the low 3% range in US 10-year yield

Global markets rose on a busy day for policy announcements in Europe, after the Federal Reserve indicated that its interest-rate hike cycle has ended and that lower

borrowing costs are coming in 2024. The SNB kicked off Europe’s central bank announcements by holding rates steady at 1.75%, as expected. The Bank of England also kept rates unchanged but said that “there is still some way to go” in the fight to control

inflation. Brazil’s central bank lowered its benchmark rate by 50 bps as expected and sees more cuts by the same amount. MSCI’s 47-country world stocks index was adding to its impressive 13% gain over the last 1-1/2 months, while bond markets continued to

slide globally. ECB keeps the deposit facility rate unchanged at 4.00%; as expected.

EQUITIES:

US equity futures are higher, a day after the Fed Chair said that the historic tightening of monetary policy is likely over, with a discussion of cuts in borrowing costs coming “into

view”. Policymakers were nearly unanimous in their projections that borrowing costs would fall in 2024, with projections in the “dot plot” showing 75 basis points of reductions.

Futures ahead of the bell: E-Mini S&P +0.3%, Nasdaq +0.3%, Russell 2000 +1.3%, Dow +0.2%.

In pre-market trading, Moderna (MRNA) gains 11% after study results showed that its personalized vaccine developed with Merck helped prevent the recurrence of severe skin cancer. Pagaya

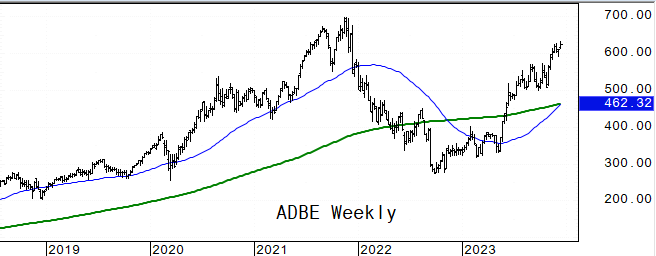

Technologies (PGY) rises as much as 5.8% as Jefferies initiates coverage on the fintech company’s stock with a buy recommendation. Adobe (ADBE) shares are down as much as 5.7%, after giving a full-year forecast that is weaker than expected. The software maker’s

sales outlook signaled it will have to wait longer than expected for a boost from new AI tools. Adobe also said US antitrust regulators are looking into its cancellation rules for subscriptions. Apellis Pharmaceuticals (APLS) falls 13% on news it expects a

European regulator to adopt a negative opinion on Pegcetacoplan at its next meeting.

E-Mini calendar roll: next resistance 54.70, 55.55

European shares jumped after the Federal Reserve pivoted toward reversing its steep interest-rate hikes ahead of a decision by the region’s own central bank. Europe’s Stoxx 600 index

surged as much as 1.7%, led by Real Estate and Miners. Shares in Germany and France hit fresh all-time peaks. Vivendi surged after saying it may split its media and entertainment empire into several entities. Traders are pricing in 161bps and 125bps of rate

cuts by the end of 2024 for the ECB and BOE respectively. Stoxx +1.4%, DAX +0.6%, CAC +1.2%, FTSE 100 +1.6%. REITs +5.9%, Basic Resources +3.3%, Construction +3.1%, Insurance -0.8%.

Shares in Asia jumped after the Federal Reserve green-lighted interest-rate cuts for next year. The MSCI Asia Pacific Index gained 1.6%, with AIA Group, Infosys and TSMC among the biggest

gainers. Key gauges rose more than 1% in Hong Kong, South Korea, India and Australia. Japanese equities fell as the yen strengthened, with investors eying an eventual end to the nation’s negative rates. Chinese tourism-related companies rose after the government

said it will launch a 3-year plan to promote inbound tourism. Philippines +2.5%, ASX 200 +1.6%, Thailand +1.5%, Indonesia +1.4%, Sensex +1.3%, Kospi +1.3%, Hang Seng Index +1.1%, Taiwan +1%, Vietnam -0.4%, China’s CSI 300 -0.5%, Topix -1.4%.

FIXED INCOME:

Treasuries extended the sharp rally that followed the Fed meeting, with the 10-year yield falling below 4% for the first time since August. Policy sensitive 2-year

yield has now plunged 92bps since the October high to 4.33%. Markets are now pricing a more than 85% chance of a rate cut in March, according to CME FedWatch tool, compared with 40% a day before. Treasuries extend Wednesday’s post-Fed surge higher, with yields

another 4bp to 10bp richer on the day in a continued bull-steepening move. Goldman Sachs revised Fed call — now seeing “earlier and faster” cuts. US 2s10s, 5s30s spreads are steeper by 4bp and 5bp on the day.

METALS:

Gold advanced after the Federal Reserve gave the clearest signal yet that its aggressive tightening campaign has ended, forecasting a series of rate cuts next year

in a shift that brightens the metal’s outlook. Bullion rose above $2,035 an ounce after surging 2.4% on Wednesday as Fed policymakers said they expected to lower rates by 75 basis points in 2024. Gold +0.4%, Silver +1%.

ENERGY:

Oil prices are higher for a second straight day, boosted by a weaker dollar following the clearest sign yet that the Federal Reserve’s aggressive hiking campaign

is over. Global oil demand growth is slowing down sharply as economic activity weakens in key countries, the International Energy Agency said as it slashed estimates for this quarter. The IEA sliced nearly 400,000 barrels a day from assessments of consumption

growth for the final three months of 2023, and continues to expect that growth rates will decelerate dramatically next year. WTI +2%, Brent +2%, US Nat Gas +0.9%, RBOB +2%.

CURRENCIES:

The dollar dropped to a fresh four-month low after the Fed’s latest economic projections indicated the interest rate hike cycle has ended and lower borrowing costs

are coming next year. The Norwegian crown strengthened after an unexpected rate hike of 25bps, adding that it would likely stay at that level for some time. The Swiss franc was little changed after the Swiss National Bank held rates. Sterling jumped after

the BOE left its key rate at 5.25%. The yen continued to strengthen in the wake of the dollar’s tumble. Australian dollar, meanwhile, hit over a four-month high versus the dollar after domestic net employment jumped. The kiwi rose over 1% versus the greenback

despite data showing the New Zealand economy unexpectedly contracted in the third quarter.

Bitcoin +0.3%, Ethereum +1.8%.

TECHNICAL LEVELS:

|

ESH23 |

10 Year Yield |

Feb Gold |

Jan WTI |

Spot $ Index |

|

|

Resistance |

4873.00 |

5.325% |

2117.0 |

81.00 |

107.350 |

|

|

4830.00 |

5.000% |

2089.5 |

79.00 |

106.280 |

|

|

4808.00 |

4.600% |

2051.0 |

77.90 |

105.000 |

|

|

4782.00 |

4.540% |

2027.0 |

76.60 |

104.350 |

|

|

4764.00 |

4.340% |

2006.8 |

72.12 |

103.520 |

|

Settlement |

4760.75 |

1997.3 |

69.47 |

||

|

|

4735.00 |

4.020% |

1986.5 |

67.71 |

102.540* |

|

|

4711/12 |

3.935% |

1973.9 |

66.80 |

101.740 |

|

|

4690.00 |

3.640% |

1963.5 |

65.00 |

101.240 |

|

|

4668.00 |

3.245% |

1960.8* |

63.64 |

100.000 |

|

Support |

4639.00 |

3.000% |

1935.5 |

61.75 |

99.580 |

Colors within the report:

Green is always the 200 period (day, week).

Red is always 21,

Blue = 50,

Brown =

100 *Stars have added importance

- Upgrades

- Aclara Resources (ARA CN) Raised to Speculative Buy at Canaccord

- Alector (ALEC) Raised to Buy at Stifel; PT $15

- Beacon Roofing (BECN) Raised to Overweight at JPMorgan; PT $103

- Choice Hotels (CHH) Raised to Neutral at JPMorgan; PT $119

- Cognizant (CTSH) Raised to Equal-Weight at Barclays

- Foot Locker (FL) Raised to Overweight at Piper Sandler; PT $33

- Gibson Energy (GEI CN) Raised to Overweight at Wells Fargo; PT C$23

- Host Hotels (HST) Raised to Neutral at JPMorgan; PT $18

- Installed Building (IBP) Raised to Overweight at JPMorgan; PT $199

- Invesco (IVZ) Raised to Outperform at KBW; PT $20

- Live Nation (LYV) Raised to Overweight at Morgan Stanley; PT $110

- Marathon Petroleum (MPC) Raised to Overweight at Wells Fargo; PT $169

- Park Hotels (PK) Raised to Neutral at JPMorgan; PT $16

- Paychex (PAYX) Raised to Equal-Weight at Barclays

- Ryman Hospitality (RHP) Raised to Neutral at JPMorgan; PT $102

- Six Flags (SIX) Raised to Overweight at Morgan Stanley; PT $32

- Sunstone Hotel (SHO) Raised to Neutral at JPMorgan; PT $10

- TopBuild (BLD) Raised to Overweight at JPMorgan; PT $387

- Trex (TREX) Raised to Neutral at JPMorgan; PT $79

- TripAdvisor (TRIP) Raised to Buy at BTIG; PT $25

- U.S. Steel (X) Raised to Strong Buy at CFRA; PT $46

- Downgrades

- Amtech (ASYS) Cut to Hold at Benchmark

- Cepton (CPTN) Cut to Hold at WestPark Capital; PT $10

- Deckers Outdoor (DECK) Cut to Hold at Stifel; PT $709

- Dollarama (DOL CN) Cut to Hold at TD; PT C$105

- Cut to Hold at Stifel Canada; PT C$100

- Equitrans (ETRN) Cut to Underweight at Wells Fargo; PT $10

- Excelerate Energy (EE) Cut to Equal-Weight at Wells Fargo; PT $18

- FMC Corp (FMC) Cut to Market Perform at BMO; PT $63

- Fortune Brands (FBIN) Cut to Hold at CFRA; PT $76

- Fulton Financial (FULT) Cut to Equal-Weight at Stephens; PT $16

- Gaming and Leisure (GLPI) Cut to Neutral at JPMorgan; PT $48

- Green Dot (GDOT) Cut to Underweight at Barclays

- Harmony (HAR SJ) ADRs Cut to Underweight at JPMorgan; PT $3.10

- Northrop Grumman (NOC) Cut to Underperform at Wolfe; PT $450

- Riskified (RSKD) Cut to Equal-Weight at Barclays

- SeaWorld (SEAS) Cut to Equal-Weight at Morgan Stanley; PT $57

- Sibanye Stillwater (SSW SJ) ADRs Cut to Neutral at JPMorgan; PT $6

- Silicon Labs (SLAB) Cut to Strong Sell at CFRA; PT $80

- Stanley Black & Decker (SWK) Cut to Underweight at JPMorgan; PT $89

- Initiations

- American Financial (AFG) Reinstated Buy at Janney Montgomery; PT $135

- American Tower (AMT) Rated New Buy at HSBC; PT $245

- Arch Capital (ACGL) Reinstated Inline at Evercore ISI; PT $88

- Bitfarms/Canada (BITF CN) Rated New Buy at B Riley; PT C$5.39

- Cardinal Health (CAH) Rated New Underweight at Wells Fargo; PT $96

- Cencora Inc (COR) Reinstated Equal-Weight at Wells Fargo; PT $213

- Cincinnati Financial (CINF) Reinstated Neutral at Janney Montgomery

- Coterra Energy Inc (CTRA) Rated New Hold at Baptista Research

- CRH (CRH) Rated New Buy at Truist Secs; PT $81

- Crown Castle (CCI) Rated New Hold at HSBC; PT $110

- Cytek Biosciences (CTKB) Rated New Overweight at Stephens; PT $9

- Everest Group Ltd (EG) Rated New Inline at Evercore ISI; PT $431

- Exact Sciences (EXAS) Rated New Outperform at Wolfe; PT $95

- Globant (GLOB) Reinstated Buy at William O’Neil

- Illumina (ILMN) Rated New Outperform at Wolfe; PT $175

- Rated New Overweight at Stephens; PT $170

- Ironwood (IRWD) Reinstated Overweight at Wells Fargo; PT $20

- Kenvue (KVUE) Rated New Hold at Baptista Research; PT $23.50

- Keysight (KEYS) Rated New Hold at Baptista Research; PT $163

- McKesson (MCK) Rated New Equal-Weight at Wells Fargo; PT $502

- Metals Acquisition (MTAL) Rated New Outperform at National Bank; PT $14

- Moleculin Biotech (MBRX) Rated New Buy at HC Wainwright; PT $3

- Opera (OPRA) ADRs Reinstated Buy at B Riley; PT $20

- Pacific Bio (PACB) Rated New Overweight at Stephens; PT $11

- Pagaya Technologies (PGY) Rated New Buy at Jefferies; PT $2.50

- PagerDuty Inc (PD) Rated New Buy at BofA; PT $30

- PSQ Holdings (PSQH) Rated New Buy at Roth MKM; PT $8.50

- RenaissanceRe (RNR) Reinstated Underperform at Evercore ISI; PT $200

- Schnitzer Steel (RDUS) Rated New Neutral at Seaport Global Securities

- Shift4 Payments (FOUR) Rated New Buy at Seaport Global Securities

- Talen Energy Corp (TLNE) Rated New Outperform at Oppenheimer; PT $77

- Thermo Fisher (TMO) Rated New Outperform at Wolfe; PT $575

- Waters (WAT) Reinstated Peerperform at Wolfe

- WK Kellogg (KLG) Rated New Equal-Weight at Morgan Stanley; PT $13

- Xylem (XYL) Rated New Hold at Baptista Research; PT $118.80

- Zai Lab (ZLAB) ADRs Rated New Overweight at Morgan Stanley; PT $47.50

Data sources: Bloomberg, Reuters, CQG

No responses yet