This post goes out as an email to our subscribers every day and is posted for free here around 2 PM ET. To get your real-time copy, sign up for the free or premium version here: Opening Print Subscribe.

Inflation nation. What will the fed do?

Follow @MrTopStep on Twitter and please share if you find our work valuable!

Our View

Going into today’s CPI release, Oracle fell another 6.7%, while Micron dropped 4.64%. It’s been a tough stretch for tech and high-growth names, especially with inflation concerns looming over the market.

One crazy stat from Bespoke caught my attention—while I’ve always appreciated their insights, this one is truly remarkable: all 26 Russell 1,000 stocks that had gained more than 100% year-to-date as of last Friday were down today, and they were down an average of more than 5%. At the same time, the 25 worst-performing stocks in the Russell 1,000 YTD through last Friday were up an average of more than 3% yesterday.

Our Lean

According to Goldman Sachs, the Consumer Price Index (CPI) for November is expected to reflect a 2.7% 12-month inflation rate, an increase of one-tenth of a percentage point from October. Core CPI is forecast to remain steady at 3.3%, unchanged from October.

I know the markets have been bullish, but it’s clear that the Fed won’t be thrilled with a high inflation print, especially as they approach their next decision-making window. Beyond today’s CPI report, we also have the Producer Price Index (PPI) on Thursday and the PitBull’s low the day before the December options expiration on Friday.

From Stock Traders Almanac:

December’s Quarterly Options Expiration Week Historically Bullish

December’s quarterly options expiration week and the week after have the most bullish record of all quarterly option expirations (page 108, Stock Trader’s Almanac 2023 & 2024 Almanac). Since 1982, DJIA has advanced 30 times during December’s options expiration week with an average gain of 0.46%. In the following week, DJIA advanced 75.6% of the time with an average gain of 0.80%. S&P 500 has a similar, although slightly softer record.

However, the record is not pristine. In 2021, accelerating inflation metrics triggered concerns that the Fed was behind the curve with monetary policy and last year there was a growing concern the Fed was going too far, too fast. In 2018, DJIA and S&P 500 suffered their worst weekly loss as the Fed remained hawkish and determined to raise interest rates even as economic growth was slowing and Treasury bond yields were falling. In 2011, Europe’s debt crisis derailed the market. In 2012, the threat of going over the fiscal cliff triggered a nearly 2% loss the week after.

Going into next week, the market’s bullish historical trends will be tested by the Fed, CPI and PPI. The Fed is widely anticipated to hold rates steady, but everyone is still searching for clarity on whether the Fed is done along with any indication as to when rates may be cut. Today’s better than expected November employment report raises the stakes slightly, but the trend employment has been toward softer.

MiM and Daily Recap

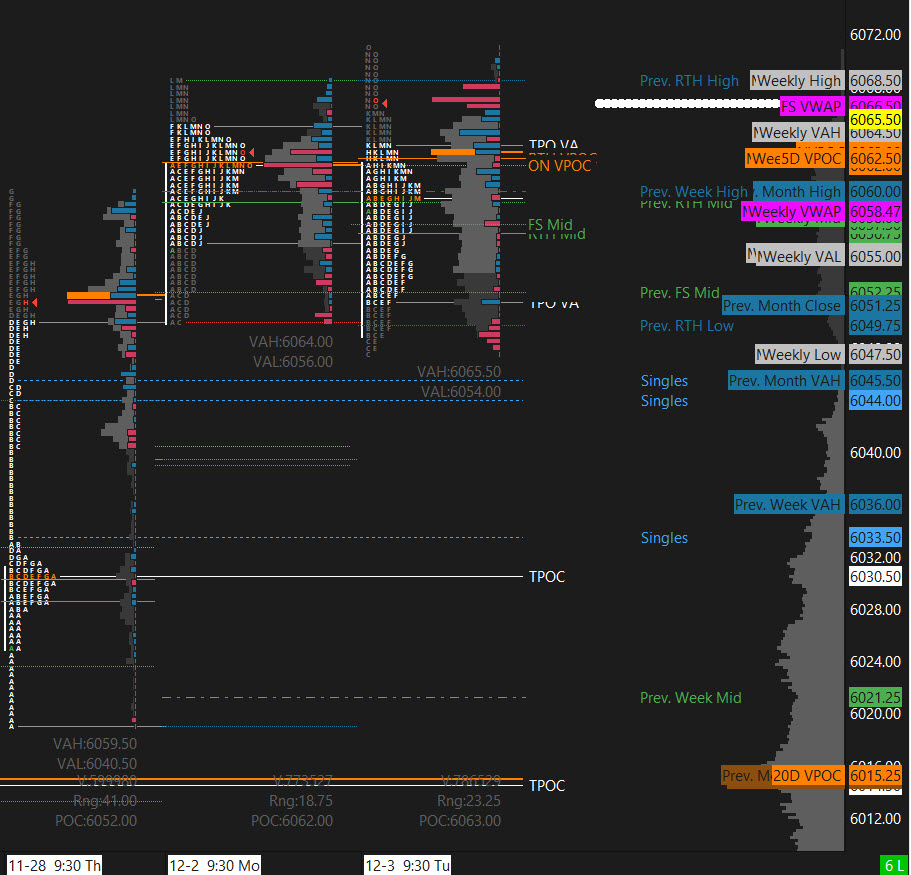

The ES traded in a tight range during the Globex session, setting an overnight low of 6057.50 at 4:44 AM. A rally from this level pushed prices up to the overnight high of 6072.75, establishing the first-half-of-the-day range.

The regular session opened at 6071.75, followed by a quick dip to 6061 before prices rallied, dipped again, and then whipsawed up to the day’s high of 6075.25 at 10:45 AM. This proved to be a false breakout as a lower high reversal, led by NQ and the Mag.7, dragged the market back below the open and attracted sellers back in for the remainder of the day.

While the rest of the morning drifted lower, eventually printing a regular session low of 6060 at 12:18 PM, we did get a little profit-taking move back up to 6068.50 at 12:34 PM. From there it was a steady distribution grind lower over the next three hours, where every rally could be sold without much reaction, printing the session low of 6039.75 at 3:32 PM.

A 10-point bounce on short-covering yielded to another downdraft just before the 3:50 PM MIM, which initially showed $464 million to sell but quickly grew to $1.75 billion by the 3:55 PM update. The market absorbed it all and short-covered some more ahead of today’s CPI report, ultimately settling at 6052.75, down 13 points (-0.21%).

The NQ settled at 21,434.75, down 49 points (-0.23%). The session saw slightly higher volumes, with 1.27 million contracts traded in ES and 530K in NQ. While the selling over the past two days has been notable, yesterday’s volume and volatility do not suggest much large position adjustment out of yesterday’s action, likely due to anticipation of today’s CPI report. If the number is a surprise in either direction, be ready for a much bigger range and heightened volatility, possibly until next week’s Fed meeting.

Technical Edge

MrTopStep Levels:

Fair Values for December 11, 2024:

-

SP: 12.64

-

NQ: 46.02

-

Dow: 97.84

VIX: 14.36

Daily Market Recap 📊

-

NYSE Breadth: 31% Upside Volume

-

Nasdaq Breadth: 44% Upside Volume

-

Total Breadth: 42% Upside Volume

-

NYSE Advance/Decline: 38% Advances

-

Nasdaq Advance/Decline: 39% Advances

-

Total Advance/Decline: 39% Advances

-

NYSE New Highs/New Lows: 64 / 30

-

Nasdaq New Highs/New Lows: 130 / 97

-

NYSE TRIN: 1.21

-

Nasdaq TRIN: 0.81

Weekly Market 📈

-

NYSE Breadth: 45% Upside Volume

-

Nasdaq Breadth: 60% Upside Volume

-

Total Breadth: 55% Upside Volume

-

NYSE Advance/Decline: 37% Advances

-

Nasdaq Advance/Decline: 47% Advances

-

Total Advance/Decline: 43% Advances

-

NYSE New Highs/New Lows: 339 / 96

-

Nasdaq New Highs/New Lows: 604 / 285

-

NYSE TRIN: 1.21

-

Nasdaq TRIN: 0.81

Guest Posts

PTG David: Polaris Trading Group

Prior Session: Cycle Day 2 Recap

-

Market Activity: The expected MATD rhythms unfolded during the AM session with a “Rock’em Sock’em” two-way auction. Sellers maintained pressure throughout.

-

Afternoon Session: At 2 PM, the “Shake n Bake” saw bulls losing traction, ultimately capitulating into the closing bell.

-

Session Stats:

-

Range: 35 handles

-

Volume: 1.241M contracts exchanged

-

-

Detailed Recap: Trading Room RECAP 12.10.24

Transition: Cycle Day 2 to

-

Current Price Action:

-

Price is below the Cycle Day 1 Low (6060).

-

Odds: 92.59% favor recovery back above 6060 during this session.

-

Key Market Drivers for Today

-

Event: Final CPI reading of the year.

-

Market Expectation:

-

85% chance of a 25 bps rate cut at the December 18th FED meeting.

-

Current target rate: 4.50% – 4.75%.

-

-

Volatility Alert: CPI releases can trigger unpredictable price volatility. Maintain vigilance for potential two-way activity.

PTG’s Primary Directive (PD):

ALWAYS STAY IN ALIGNMENT WITH THE DOMINANT FORCE.

Scenarios for Today

-

Bull Scenario:

-

Price sustains a bid above 6050.

-

Initial targets: 6060 – 6065 zone.

-

-

Bear Scenario:

-

Price sustains an offer below 6050.

-

Initial targets: 6040 – 6035 zone.

-

Key Levels

-

PVA High Edge: 6073

-

PVA Low Edge: 6055

-

Prior POC: 6062

ES (Profile)

Thanks for reading, PTGDavid

Trading Room Summaries

Polaris Trading Group Summary – Tuesday, December 10, 2024

The day began with PTGDavid sharing essential resources, disclaimers, and a link to the Zoom room for the trading session. Key insights were communicated early, with expectations for rhythmic market activity (MATD) and initial target zones outlined for both Nasdaq (NQ) and S&P 500 (ES) futures.

Key Highlights:

-

Morning Session:

-

Early strength in NQ was noted, with targets in the 21540–21560 range.

-

ES achieved initial targets around 6075–6080, fulfilling the Daily Trade Strategy (DTS) early expectations.

-

Discussion of tools like the D-Level Money Box (DLMB) emphasized flexibility across different timeframes.

-

-

Midday Observations:

-

Price returned to critical zones like the “Line in the Sand,” signifying key decision points.

-

Adjustments to tools and configurations were discussed, demonstrating the importance of precise settings for accurate readings.

-

-

Afternoon Activity:

-

A power surge caused a brief disruption, quickly resolved by PTGDavid.

-

Volatility triggers and setups like the “Peek-a-Boo” (PKB) pattern were actively monitored.

-

The “2 PM Shake n Bake” highlighted predictable market behavior during this time.

-

-

Late Session:

-

Short trades became prominent as targets in the 6050–6045 range were met, with continued management via stop trails.

-

Lower-level zones between 6042–6036 were identified and fulfilled, aligning with rotational CD2 day characteristics.

-

A minor MOC (Market On Close) sell imbalance of $445M was noted.

-

A late buy response emerged from the lower Money Box Zone, emphasizing market participants’ reactions at strategic levels.

-

Lessons and Positive Takeaways:

-

Precision in Targets: The session underscored the value of predefined levels and tools like the DLMB for structured trade management.

-

Adaptability: Adjusting to real-time developments, such as power surges or shifting market rhythms, was seamlessly handled.

-

Patterns and Rhythms: Identifying consistent setups (e.g., PKB and volatility triggers) provided actionable trade opportunities.

-

Community Engagement: Collaborative troubleshooting and strategy discussions enriched learning for all participants.

The day ended with strategic zones met, disciplined trade management, and valuable insights into both market behavior and the effective use of PTG tools.

Discovery Trading Group Room Preview – December 11, 2024

-

Key Event: The primary focus today is the release of the Consumer Price Index (CPI) at 8:30 AM ET. This critical inflation data may influence the Fed’s anticipated rate cut next week. Current market conditions favor a “soft-landing” narrative, with equities thriving under falling inflation, economic resilience, and rate cut expectations. Any shift could trigger significant volatility or sell-offs.

-

Market Performance:

-

U.S. stock indexes dipped ~0.3% on Tuesday.

-

Alphabet (GOOG) surged 5% after announcing quantum computing breakthroughs with its Willow quantum chip. This innovation significantly reduces computation times for complex problems compared to classical supercomputers.

-

Oracle (ORCL) fell 7% following disappointing quarterly revenue and intensified competition in the cloud sector.

-

-

Geopolitical & Policy Developments:

-

China commenced a 2-day policy planning session, signaling potential monetary stimulus and “moderately loose” fiscal measures amid economic challenges and U.S. trade concerns.

-

-

Corporate Earnings: Adobe (ADBE) and Nordson (NDSN) report earnings after the market close.

-

Economic Data Calendar:

-

8:30 AM ET: CPI numbers (critical focus for today).

-

10:30 AM ET: Crude Oil Inventories.

-

2:00 PM ET: Federal Budget Balance.

-

-

Market Insights:

-

Elevated volatility continues as markets await CPI data. Bullish sentiment from large traders persists into the release, with light overnight trading volumes.

-

The ES Index approached the 6011/14 support zone of its short-term uptrend channel. A higher-than-expected CPI reading could breach this support, while a favorable outcome provides room for potential all-time highs. Key technical levels to monitor: Resistance at 6143/46; Support at 6011/14 and 5884/87.

-

Stay tuned for updates post-CPI release as markets react to the inflation data.

ES -Week to Week

ES 6100 starting to seem like a long time ago. We are retracing here a bit, we like the 6045 for a tag and a hold. Upside 6100, of course, and then a break there above we have a target set to 6168.

NQ – Week to Week

Is NQ charging up or stalling? Some inflation news to get through this week. There should be plenty of weak shorts in the market right now to fuel up to the 21,740 area and set new highs. If inflation comes in hot, expect profit triggering to drive the markets lower in which case that 21,200 area will be calling.

Calendars

Today

Important Upcoming

Earnings

Affiliate Disclosure: This newsletter may contain affiliate links, which means we may earn a commission if you click through and make a purchase. This comes at no additional cost to you and helps us continue providing valuable content. We only recommend products or services we genuinely believe in. Thank you for your support!

Disclaimer: Charts and analysis are for discussion and education purposes only. I am not a financial advisor, do not give financial advice and am not recommending the buying or selling of any security.

Remember: Not all setups will trigger. Not all setups will be profitable. Not all setups should be taken. These are simply the setups that I have put together for years on my own and what I watch as part of my own “game plan” coming into each day. Good luck!

This post goes out as an email to our subscribers every day and is posted for free here around 2 PM ET. To get your real-time copy, sign up for the free or premium version here: Opening Print Subscribe.

Comments are closed