This post goes out as an email to our subscribers every day and is posted for free here around 2 PM ET. To get your real-time copy, sign up for the free or premium version here: Opening Print Subscribe.

Trump’s Victory, Fed Moves, and the Market Sell-Off: What’s Next?

Follow @MrTopStep on Twitter and please share if you find our work valuable!

Our View

It seems like the fun never stops in the S&P 500. On November 5, 2024, Trump won both the Electoral College and the popular vote, becoming only the second Republican to win the popular vote since 1988 but the stock market has been going down ever since. The main question is: why? After a full year of rallying, the S&P has fallen 5%, the Dow has dropped 7%, and the Nasdaq has fallen 7%. In the grand scheme of the last two years, it’s not that much, but it’s the timing of the sell-off that threw a monkey wrench into what most people were looking for, an end-of-the-year push. Santa Claus didn’t just fail to show up, he got shoved off the roof.

I hate to keep going over and over the same things but I was talking to Jeff Hirsch from the Stock Trader’s Almanac, and he agreed with my assessment: the Fed didn’t need to cut by 0.50% in December. Based on the data, the Fed never should have cut. That decision marked one of the best “sell-the-news” events in a long time. Inflation was already rising, yields were climbing, and Trump was threatening just about everyone with increased tariffs, all while the geopolitical situation grew increasingly volatile. Yesterday, the Nasdaq fell for the fifth straight session, while YM closed up almost 0.50% higher, and the S&P closed essentially flat, just a tad higher.

Heading into today’s CPI number, the yield on the 10-year note settled at 4.787%, down from Monday’s 4.802%, its highest closing level since October 2023. I think this moment is ground zero, and today’s CPI number could be pivotal. Additionally, Citigroup, Goldman Sachs, JPMorgan, and Wells Fargo are all set to report their quarterly results, which could further impact market sentiment.

-DR

Our Lean

Q1 earnings are going to be important, but today’s CPI number should be market-moving. I anticipate a volatile, two-way trade. While I’ve said that the ES didn’t act all that badly yesterday, the strategy remains to sell into 50- to 70-point rips and keep a close eye on the 10-year yield. The bond market will play a crucial role in determining the direction of equities, so monitoring these levels is key,

-DR

MiM and Daily Recap

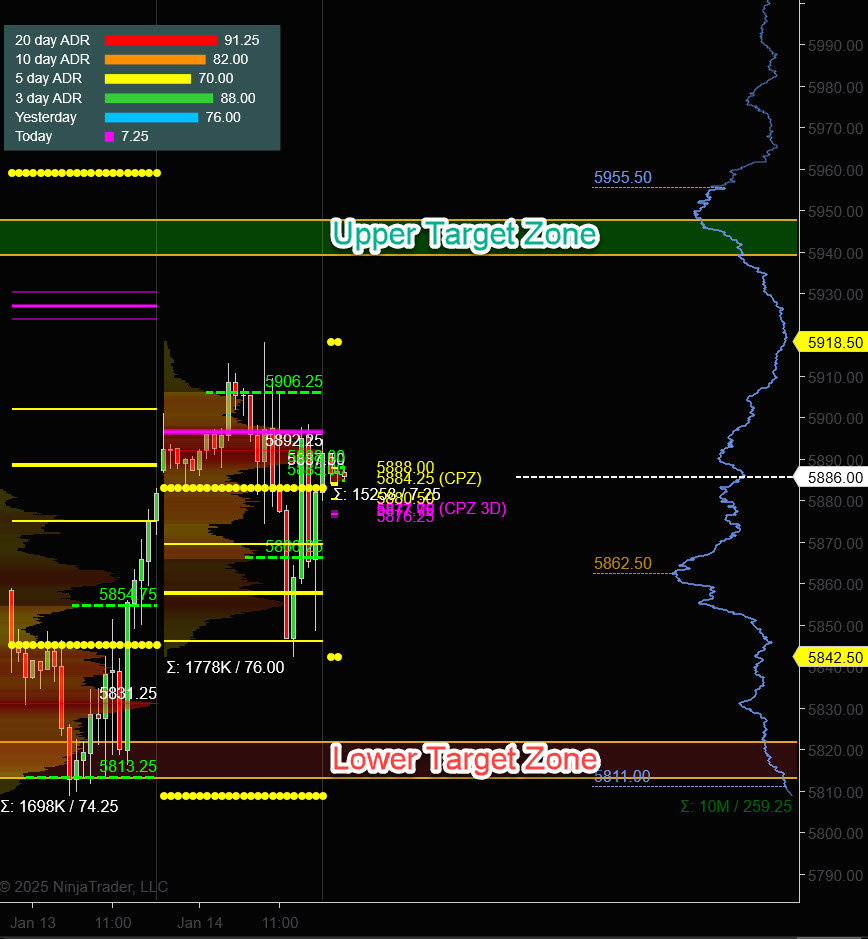

The ES put in a Globex high of 5913.50 overnight before leading to some selling ahead of the PPI release, sliding down to a low of 5874.50 just before the announcement. After the data release, the market rallied straight up to take out the high, printing 5918.50 which turned out to be the day’s high.

After some initial choppiness following the regular session open at 5902.75, sellers gained control in the morning, driving the ES down to 5878.75 just before 10:00 AM. A subsequent bounce led to a test of the open level at 10:14 AM, but a false breakout above the open and ensuing reversal gave the market fuel to take out downside stops. This triggered a steady decline to the morning low of 5844.75 at 11:58 AM.

A little chop around the 5850-5860 zone led to one more stop run to our low of the day at 5842.50 at 12:34 PM. However, this move proved to be a false breakdown, and the market reversed higher. Buyers stepped back in and steadily pushed the ES back up through the range to print 5898 by 1:58 PM.

The afternoon featured thirty minutes of sideways trading in a tight 10-point range before the bulls yielded again as a strong sell program emerged, driving the market from 5896 at 2:42 PM down to 5848.75 by 3:00 PM. Proving to be a water-in-the-bathtub day, this was it for the bears as the last hour of trading was a face-ripper in the other direction, rallying ahead of the 3:50 PM MiM release which was essentially a flat imbalance.

From here there were still shorts to cover into the cash close settlement at 5882.75. Post-market buying pushed the exchange closing price for the ES to 5891.50, ending the day up 9.75 points (+0.17%). The NQ closed at 20,977.50, down 14.75 points (-0.07%). Volume picked up ahead of today’s CPI report, with the ES trading 1.77 million contracts and the NQ trading 664,000 contracts.

In the end, the markets keep a movin’. In terms of the ES’s overall tone, I don’t think it acted all that bad. In terms of the ES’s overall trade, volume was in line with what we have been seeing.

Technical Edge

MrTopStep Levels:

Fair Values for January 15, 2025:

-

SP: 37.49

-

NQ: 150.81

-

Dow: 218.40

Daily Market Recap 📊

-

NYSE Breadth: 72% Upside Volume

-

Nasdaq Breadth: 55% Upside Volume

-

Total Breadth: 57% Upside Volume

-

NYSE Advance/Decline: 74% Advances

-

Nasdaq Advance/Decline: 56% Advances

-

Total Advance/Decline: 61% Advances

-

NYSE New Highs/New Lows: 42 / 50

-

Nasdaq New Highs/New Lows: 58 / 173

-

NYSE TRIN: 1.26

-

Nasdaq TRIN: 1.12

Weekly Market 📈

-

NYSE Breadth: 43% Upside Volume

-

Nasdaq Breadth: 54% Upside Volume

-

Total Breadth: 50% Upside Volume

-

NYSE Advance/Decline: 23% Advances

-

Nasdaq Advance/Decline: 23% Advances

-

Total Advance/Decline: 23% Advances

-

NYSE New Highs/New Lows: 107 / 257

-

Nasdaq New Highs/New Lows: 265 / 360

-

NYSE TRIN: 1.31

-

Nasdaq TRIN: 0.91

Good Reads:

Bank of America makes surprising pivot on interest rates

US Daily: December CPI Preview (Rindels/Walker)

We expect a 0.25% increase in December core CPI (vs. 0.2% consensus),corresponding to a year-over-year rate of 3.27% (vs. 3.3% consensus). We expect a 0.40% increase in December headline CPI (vs. 0.3% consensus), reflecting 0.35% higher food prices and 2.3% higher energy prices. Our forecast is consistent with a 0.21% increase in CPI core services excluding rent and owners’ equivalent rent and with a 0.18% increase in core PCE in December.

We highlight three key component-level trends we expect to see in this month’s report. First, we expect used car prices to increase 1.0%, reflecting an increase in auction prices. Second, we expect another increase in airfares of 1.0%, reflecting a boost from seasonal distortions. Third, we expect a slight acceleration in the car insurance category (+0.3%) based on continued, albeit decelerating, increases in premiums in our online dataset.

Going forward, we see further disinflation in the pipeline over the next year from rebalancing in the auto, housing rental, and labor markets, but an offset from an escalation in tariff policy. We forecast year-over-year core CPI inflation of 2.7% and core PCE inflation of 2.4% in December 2025.

We expect a 0.25% increase in December core CPI—above consensus of 0.2% but below the 0.30% average of the last three months—corresponding to a year-over-year rate of 3.27% (vs. 3.3% consensus). We expect a 0.40% increase in December headline CPI (vs. 0.3% consensus), reflecting 0.35% higher food prices and 2.3% higher energy prices. Our forecast is consistent with a 0.21% increase in CPI core services excluding rent and owners’ equivalent rent and with a 0.18% increase in core PCE in December.

Exhibit 1 provides a component-level summary of our forecast.

Core 100% 0.30% 0.31% 0.25%

Apparel 3% 0.0% 0.2% 0.2%

New cars 4% 0.2% 0.6% 0.3%

Used cars 2% 1.7% 2.0% 1.0%

Motor vehicle parts 1% 0.1% -0.6% 0.1%

Medical care commodities 2% -0.3% -0.1% -0.1%

Tobacco 1% 0.5% 1.0% 0.3%

Rent of primary residence 10% 0.26% 0.21% 0.25%

Lodging away from home 2% 0.5% 3.2% 0.0%

Medical care services 8% 0.48% 0.37% 0.34%

Public transportation 1% 1.6% 0.0% 0.6%

Transportation services ex-public 7% 0.4% 0.0% 0.3%

Pets 1% 0.1% 0.5% 0.2%

Recreation ex-pets 6% 0.1% 0.2% 0.0%

Education 3% 0.5% 0.4% 0.3%

Communication 4% -0.7% -1.0% 0.0%

Household furnishings and ops. 5% 0.3% 0.6% 0.0%

Personal care 3% 0.3% 0.4% 0.2%

Alcoholic beverages 1% 0.2% 0.1% 0.1%

Owners’ equivalent rent 34% 0.32% 0.23% 0.30%

Residual (implicit) 2% 0.3%

Core Goods 23% 0.18% 0.31% 0.24%

Core Services 77% 0.33% 0.28% 0.25%

Core Services Ex-Rent and OER 33% 0.35% 0.34% 0.21%

Guest Posts

PTG David: Polaris Trading Group

Prior Session was Cycle Day 1: Early rally faded against the initial target zone 5895 – 5905 as outlined in prior DTS Briefing 1.14.25. Selling rotation lower fulfilled the initial downside target zone between 5860 – 5855, finding stronger buy response at the IB TGT 2 (5848) level paired with the prior VWAP.

Two more rotational rhythmic range swings played during the afternoon session, closing mid-range. Clearly a session whereby traders vying for positioning ahead of the CPI print. Range for this session was 76 handles on 1.778M contracts exchanged.

FREE TRIAL link to PTG/Taylor Three Day Cycle

For a more detailed recap of the trading session, click on this link: Trading Room RECAP 1.14.25

…Transition from Cycle Day 1 to Cycle Day 2

Transition into Cycle Day 2: As outlined in the recap above, the prior session was a notable rotational day as traders vying for positioning ahead of today’s CPI print.

Nothing changes for PTG…Simply follow your plan.

PTG’s Primary Directive (PD) is to ALWAYS STAY IN ALIGNMENT with the DOMINANT FORCE.

As such, scenarios to consider for today’s trading.

Bull Scenario: Price sustains a bid above 5875+-, initially targets 5895 – 5905 zone.

Bear Scenario: Price sustains an offer below 5875+-, initially targets 5855 – 5850 zone.

PVA High Edge = 5906 PVA Low Edge = 5866 Prior POC = 5892

ES (Profile)

Thanks for reading, PTGDavid

Trading Room Summaries

Polaris Trading Group Summary – Tuesday, January 14, 2025

Morning Session:

-

The session opened strong, with prices pushing higher overnight, hitting initial targets, and reversing at the “Money Box Zone.” Early trades benefited from this movement as the market reacted positively to the PPI release (3.3% vs. 3.5% forecast), sparking an initial rally.

-

PTGDavid emphasized alignment with dominant market forces, stating, “Deference is to long side plays early on until there is a bearish structural shift.”

-

Key trades included the fulfillment of Cycle Day 1 upper penetration targets and profits from long call positions carried over from the previous session.

-

The session later saw a “sell side shift” (9:58 AM), marking a turning point to bearish momentum.

Midday Action:

-

Bears dominated the market by mid-morning, fulfilling lower initial targets (5860–5855) outlined in the Daily Trade Strategy.

-

Significant opportunities arose from the market’s decline, with traders noting successful short positions, particularly around the Central Pivot Zone and other key levels.

-

PTGDavid reinforced the importance of following the market’s dominant force, referring to the “Simply Simon Strategy.”

Afternoon Session:

-

After a steep selloff, buyers emerged, triggering a reversal in the afternoon. A “Victory Bottom Pattern” hinted at bullish potential, but the market struggled to sustain upward momentum.

-

PTGDavid highlighted another successful PKB (Peek-a-Boo) long trade from a test of IB target 2 low, demonstrating the adaptability of this strategy at various levels.

-

Despite an afternoon rally attempt, the market experienced a sharp “rug pull” late in the session, leading to a bearish close.

-

The day ended with a “bear flag” formation and focus shifted to the CPI print set for the next morning, anticipated to create further volatility.

Key Lessons and Takeaways:

-

Adaptability and Alignment: Staying aligned with the dominant force was critical to success today. Early strength transitioned to a bearish trend, requiring traders to shift strategies mid-session.

-

Patience and Precision: The day offered significant opportunities for both bulls and bears, highlighting the importance of waiting for high-probability setups, like the PKB strategy.

-

Market Insights: The concept of “spillover” from prior sessions was explained, reinforcing the importance of context in day-to-day market behavior.

Highlights:

-

Fulfillment of multiple target zones for both bullish and bearish scenarios.

-

Profitability from long call positions carried over and intraday short trades.

-

Valuable educational moments, including strategy explanations and glossary references.

Outlook:

-

Attention now turns to tomorrow’s CPI print at 8:30 AM, which is expected to bring heightened volatility. Traders are advised to prepare for rapid market movements and ensure alignment with the dominant trend.

Discovery Trading Group Room Preview – January 15, 2025

-

Morning Insights:

-

CPI Focus: Markets are bracing for the 8:30 AM ET Consumer Price Index (CPI) report. Persistent inflation above the Fed’s 2% target is delaying potential rate cuts, which is bullish for Treasury yields but bearish for stocks.

-

Inflation Drivers: Core CPI is expected to rise by 3.3% year-over-year, driven by climbing gas and food prices, along with shelter, medical care, airfares, and lodging costs.

Policy and Fed Updates:

-

Economic Uncertainty: Analysts highlight significant policy uncertainties with the incoming Trump administration. The Fed’s December minutes express concerns over the impact of policy changes on trade and immigration.

-

Interest Rate Outlook: Bank of America predicts no rate cuts in 2025, with a possibility of a return to tighter monetary policy.

Sector News:

-

Semiconductors: Chip manufacturers are challenging new export controls, warning of significant economic and international impacts. The rules could hurt U.S. semiconductor revenue.

-

Earnings Season: Major banks reporting today include JP Morgan Chase (JPM), Wells Fargo (WFC), Goldman Sachs (GS), BlackRock (BLK), Citigroup (C), and Bank of New York Mellon (BK). Synovus Financial Corp (SNV) reports after the bell.

Key Events and Calendar:

-

Economic Data: CPI and Empire State Index at 8:30 AM ET, Oil Inventory at 10:30 AM ET, Fed Beige Book at 2:00 PM ET.

-

Fed Speakers: Barkin (9:20 AM), Kashkari (10:00 AM), Williams (11:00 AM), and Goolsbee (12:00 PM).

Market Dynamics:

-

Volatility: While volatility eased on Tuesday, CPI results are expected to drive directional movement today.

-

Trader Sentiment: Whales remain bullish heading into CPI despite light overnight large trader volume.

-

Technical Trends: S&P 500 futures (ES) remain within a downtrend channel. Key resistance levels are at 6015/12s and 6345/50s, with support at 5825/28s and 5782/79s.

Stay alert for updates as data releases and earnings reports shape today’s market.

-

ES -Week to Week

Still expecting a multi-day bounce from Monday’s drop. Support at the 5882 level needs to hold today. If we do fall based on CPI or other news (JPM is before the open today) 5883 is a marker and then a stop at 5785. For the bulls today they have a job to get to 5931 but a lot of resistance before there in the 5910 and 5918 area. We remain in sell-the-rally mode with the bull/bear line now at 6082.

NQ – Week to Week

The bull/bear line for the NQ is down to 21,932. Above that we are more interested in buying intraday dips. For the bears, 20,947 is a deep resistance line. If we trade below that, 20,922 would be a target. If that breaks, we are putting in lower lows. Upside, bulls need to work this week up to 21,374. To get there 21,124 needs to be tackled.

Calendars

Today

Important Upcoming

Earnings

Affiliate Disclosure: This newsletter may contain affiliate links, which means we may earn a commission if you click through and make a purchase. This comes at no additional cost to you and helps us continue providing valuable content. We only recommend products or services we genuinely believe in. Thank you for your support!

Disclaimer: Charts and analysis are for discussion and education purposes only. I am not a financial advisor, do not give financial advice and am not recommending the buying or selling of any security.

Remember: Not all setups will trigger. Not all setups will be profitable. Not all setups should be taken. These are simply the setups that I have put together for years on my own and what I watch as part of my own “game plan” coming into each day. Good luck!

This post goes out as an email to our subscribers every day and is posted for free here around 2 PM ET. To get your real-time copy, sign up for the free or premium version here: Opening Print Subscribe.

Comments are closed