TODAY’S GAME PLAN: from the trading

desk, this is not research

DATA/HEADLINES 8:30ET GDP, Personal Consumption, Core PCE Price Index, Weekly Jobless Claims; 9:00ET Fed’s Goolsbee

speaks; 10:00ET Pending Home Sales; 11:00ET Kansas City Fed Mfg. Activity; 1:00ET Fed’s Cook speaks; 3:00ET Mexico Rate Decision; 3:30ET Fed’s Barkin speaks; 4:00ET Fed’s Powell host town hall meeting

US 2Q GDP PRICE INDEX RISES AT A 1.7% ANNUAL RATE: EST. 2.0%. US FINAL Q2 CONSUMER SPENDING +0.8%. US FINAL Q2 GDP DEFLATOR +1.7% (CONSENSUS +2.0%).

TODAY’S HIGHLIGHTS:

- JPMorgan ‘Options Whale’ Worries Resurface as Stocks Extend Drop

link - GameStop names billionaire Ryan Cohen as CEO

Global shares were on the defensive, with the MSCI’s all-country index at its lowest since May and on course for its 10th straight daily loss. Oil prices pushed closer

to $100 a barrel, stoking expectations interest rates will stay higher for longer and keeping pressure on global markets. Nervousness about the deepening Chinese property sector bust and another suspension of shares in the ailing real estate giant Evergrande

today added to a messy picture. German inflation is likely to ease significantly in September based on data from five key German states on Thursday, signaling what could be the beginning of the end for high inflation that has weighed heavily on Europe’s largest

economy. Investor focus will turn to US GDP and employment data due this morning as well as the start of China’s Golden Week, which may provide clues on a recovery in consumer spending.

EQUITIES:

US equity futures struggled for direction as bond yields rose ahead of the early data. With the third quarter ending tomorrow, it’s the first negative three-month stretch of the year

for equities and the S&P500 is now down almost 4% since mid-year. In corporate news, Micron Technology was down ~5% overnight after it forecast a wider than expected first-quarter loss even as it prepares to ramp up production of new product lines and works

to become a supplier to Nvidia. Stocks face the risk of further selling linked to a large options position held by a JPMorgan Chase equity fund. Tens of thousands of protective put contracts held by the fund will expire Friday at a strike price not far below

the current level of the S&P 500. Trend-chasing systematic funds are at risk of being forced to unwind equity holdings, according to Goldman Sachs, as short gamma has reached the most extreme level since Goldman began tracking the data in 2019.

Futures ahead of the data: E-Mini S&P +0.1%, Nasdaq is flat, Russell 2000 +0.2%, Dow +0.2%.

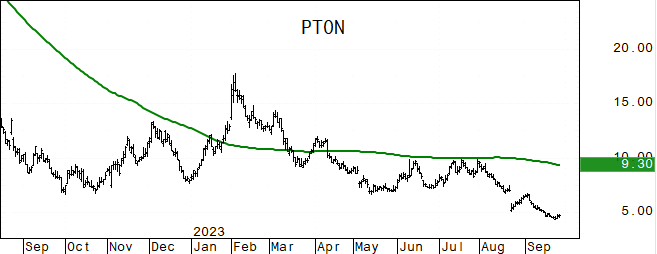

In premarket trading, Peloton Interactive rose 13% after the maker of exercise bikes agreed to a deal with Lululemon Athletica to tap its online workouts and team up on apparel. Micron

Technology tumbled 5% as its mixed outlook for the November quarter weighed on investor sentiment. CarMax fell 10% after posting a lower quarterly profit amid tepid demand for preowned vehicles. Workday (WDAY) plunged 11% on lowered growth targets. Accenture

(ACN) shares are down 4.5% after the IT services company reported its fourth-quarter results and gave a weaker than expected outlook. Gritstone (GRTS) gains 39% after the biotechnology company said it will receive as much as $433 million from the US government

to conduct a trial of its next-generation Covid-19 vaccine.

European gauges are trying to break their downward trend amid weakness in sectors sensitive to higher interest rates, as rising oil prices added to concerns over cost pressures. The Stoxx

Europe 600 benchmark has fallen for six consecutive days, making a six month low. Stoxx 600 reversed early losses as technology and travel shares weigh, while miners outperform. In individual stock moves, Schott Pharma AG shares surged on their first day of

trading after the drug-industry supplier raised €813 million ($854 million) in an initial public offering, the biggest in Germany this year. AMS-Osram AG slumped as much as 23% after the Swiss chipmaker announced a rights issue. Stoxx 600 -0.1%, DAX +0.2%,

CAC +0.4%, FTSE 100 -0.3%, Basic Resources +1.4%, Banks +0.6%, Energy +0.5%. Travel -1.2%, Technology -1%.

Asian gauges were mostly lower as concerns over China’s property market and worries over inflation stoked by oil’s rally inhibited risk taking. The MSCI Asia Pacific Index declined 0.9%,

with Tencent Holdings, Alibaba Group and Toyota among the biggest drags. Hong Kong stocks ended at their lowest level in 10 months after Evergrande’s shares were suspended from trading, further weakening sentiment on China’s real estate sector ahead of upcoming

Golden Week holidays. Japanese stocks were among the worst performers in Asia amid rising interest rates and as more than 1,000 stocks in the Topix traded without rights to the next dividend. Markets were closed for holidays in South Korea, Indonesia and Malaysia.

Nikkei 225 -1.5%, Hang Seng Index -1.4%, Sensex -0.9%, CSI 300 -0.3%, Vietnam -0.1%, ASX 200 -0.1%. Taiwan +0.3%, Philippines +0.2%, Shanghai Composite +0.1%.

FIXED INCOME:

Treasuries are cheaper by up to 4bp across long-end of the curve as Wednesday’s bear-steepening move is extended into early US session. The 2s10s curve is inverted

by less than 50bp for first time since May. The 10-year yield is around 4.6%, the highest since 2007. The US Treasury completes more than $130 billion of new debt sales this week with a 7-year note auction later today. Wednesday’ 5-year note auction stopped

1.2bp through, indicating strong demand. Fed Chair Jerome Powell and a handful of other central bank officials are set to speak later today, and investors will be monitoring GDP data this morning ahead of the personal consumption expenditures price on Friday,

the Fed’s preferred inflation gauge.

METALS:

Gold stabilized after being hit in the previous session by a surging US dollar. Meanwhile, gold in China dropped the most in three years after Beijing permitted more imports. Gold flat,

silver +0.2%.

ENERGY:

Oil prices nudged lower after jumping to their highest in more than a year as a drop in crude stocks in the United States added to worries over tight global supplies

from OPEC+ output cuts. Stockpiles at Cushing have been falling to near historic lows due to strong refining and export demand, prompting concerns about quality of the remaining oil at the hub and whether it will fall below minimum operating levels. Russia’s

ban on fuel exports will not be lifted soon and will remain in place until the domestic market stabilizes, the state-run TASS news agency reported today, citing the Russian energy minister. After 7 weeks of additions, the Biden admin reverted to draining the

SPR last week (-250k barrels). Nearing “tank bottoms”, or the effective minimum, as they always need to hold some oil for operational reasons. WTI -0.5%, Brent -0.4%, US Nat Gas +1.3%, RBOB -1%.

CURRENCIES:

The Dollar edged lower while the yen rose first day in five as repeated verbal warnings by Japanese authorities over the currency’s weakness spurred intervention

speculation. US$ Index -0.3%, GBPUSD +0.6%, EURUSD +0.3%, USDJPY -0.2%, AUDUSD +0.6%, NZDUSD +0.5%.

Bitcoin +0.8%, Ethereum +1.8%.

TECHNICAL LEVELS:

|

ESZ23 |

10 Year Yield |

Dec Gold |

Nov WTI |

Spot $ Index |

|

|

Resistance |

4437.00 |

5.500% |

2022.0 |

100.00 |

111.525 |

|

|

4400.00 |

5.325% |

1996.0 |

98.00 |

110.000 |

|

|

4383.50 |

5.000% |

1982.4 |

97.07 |

108.970 |

|

|

4365.00 |

4.710% |

1935.3 |

95.00 |

107.990 |

|

|

4342.50 |

4.565% |

1913.5 |

94.17 |

107.180 |

|

Settlement |

4313.50 |

1890.9 |

93.68 |

||

|

|

4291.00 |

4.180% |

1866/71 |

92.43 |

105.350 |

|

|

4267.00 |

4.000% |

1842.0 |

88.37 |

104.420 |

|

|

4245.00 |

3.750% |

1821.0 |

86.30 |

103.460 |

|

|

4225.00 |

3.530% |

1800.0 |

83.92 |

103.100 |

|

Support |

4200.00 |

3.265% |

1776.5 |

83.05 |

102.920 |

Colors within the report:

Green is always the 200 period (day, week).

Red is always 21,

Blue = 50,

Brown =

100 *Stars have added importance

- Upgrades

- (DBRG) DigitalBridge Group Inc Raised to Overweight at JPMorgan; PT $25

- (HII) Huntington Ingalls Raised to Overweight at JPMorgan; PT $247

- (NEE) NextEra Energy Raised to Buy at CFRA

- (RDFN) Redfin Raised to Neutral at DA Davidson; PT $8

- (TSCO) Tractor Supply Raised to Buy at DA Davidson; PT $280

- (WTRG) Essential Utilities Raised to Buy at Northcoast; PT $42

- Downgrades

- (API) Agora ADRs Cut to Equal-Weight at Morgan Stanley; PT $3.20

- (GLTO) Galecto Cut to Neutral at HC Wainwright

- (NEP) NextEra Energy Partners Cut to Neutral at JPMorgan; PT $40

- (NEP) Cut to Market Perform at Oppenheimer

- (OSK) Oshkosh Cut to Sector Weight at KeyBanc

- (TEX) Terex Cut to Sector Weight at KeyBanc

- Initiations

- (A) Agilent Rated New Market Perform at Bernstein; PT $123

- (ABI BB) AB InBev ADRs Rated New Outperform at Cowen; PT $67

- (APLE) Apple Hospitality Rated New Peerperform at Wolfe

- (AVTR) Avantor Rated New Market Perform at Bernstein; PT $22

- (BATS LN) BAT ADRs Rated New Market Perform at Cowen; PT $33

- (BMRN) BioMarin Rated New Market Perform at Raymond James

- (BWXT) BWX Technologies Rated New Buy at Deutsche Bank; PT $86

- (CEMARGOS CB) Cementos Argos ADRs Rated New Buy at Jefferies; PT $8.35

- (CERE) Cerevel Therapeutics Rated New Overweight at Piper Sandler

- (CIEN) Ciena Rated New Buy at Stifel; PT $62

- (CPTN) Cepton Rated New Buy at WestPark Capital; PT $10

- (CR) Crane Co. Rated New Buy at Deutsche Bank; PT $118

- (DGE LN) Diageo ADRs Rated New Market Perform at Cowen; PT $152

- (DNTH) Dianthus Therapeutics Inc Rated New Outperform at Raymond James

- (DV) DoubleVerify Rated New Neutral at Macquarie; PT $30

- (EXAS) Exact Sciences Rated New Outperform at Bernstein; PT $83

- (FLYW) Flywire Rated New Buy at BTIG; PT $37

- (FROG) JFrog Rated New Sector Perform at Scotiabank; PT $29

- (GD) General Dynamics Rated New Buy at Deutsche Bank

- (GE) GE Rated New Buy at Deutsche Bank

- (GH) Guardant Health Rated New Outperform at Bernstein; PT $34

- (HEI) Heico Reinstated Buy at Deutsche Bank; PT $192

- (HST) Host Hotels Rated New Outperform at Wolfe; PT $22

- (HWM) Howmet Aerospace Reinstated Buy at Deutsche Bank; PT $59

- (IAS) Integral Ad Science Rated New Outperform at Macquarie; PT $16

- (ILMN) Illumina Rated New Underperform at Bernstein; PT $111

- (IMB LN) Imperial Brands ADRs Rated New Market Perform at Cowen; PT $25

- (INFN) Infinera Rated New Buy at Stifel; PT $7

- (IOBT) IO Biotech Rated New Overweight at Piper Sandler; PT $10

- (IRWD) Ironwood Rated New Market Outperform at JMP; PT $22

- (LHX) L3Harris Rated New Hold at Deutsche Bank; PT $192

- (MRVL) Marvell Technology Rated New Buy at Fubon; PT $63

- (MVIS) MicroVision Rated New Hold at WestPark Capital

- (NTRA) Natera Rated New Market Perform at Bernstein; PT $48

- (PACB) Pacific Bio Rated New Outperform at Bernstein; PT $11

- (PEB) Pebblebrook Rated New Peerperform at Wolfe

- (PK) Park Hotels Rated New Outperform at Wolfe; PT $16

- (RHP) Ryman Hospitality Rated New Outperform at Wolfe; PT $98

- (RTX) RTX Corp Reinstated Sell at Deutsche Bank; PT $70

- (RVTY) Revvity Inc Rated New Outperform at Bernstein; PT $133

- (SHO) Sunstone Hotel Rated New Peerperform at Wolfe

- (TMO) Thermo Fisher Rated New Outperform at Bernstein; PT $603

- (TTI) Tetra Technologies Rated New Buy at Benchmark; PT $8

- (WAT) Waters Rated New Market Perform at Bernstein; PT $280

- (WWD) Woodward Rated New Buy at Deutsche Bank; PT $152

Data sources: Bloomberg, Reuters, CQG

No responses yet