TODAY’S GAME PLAN: from the trading

desk, this is not research

DATA/HEADLINES

TODAY’S HIGHLIGHTS:

- Biden visits Maui today

- The takeover of Credit Suisse is looking more profitable for UBS

- Desperate Californians climb trees to escape floods and mudslides after Hilary brings record rain

- Palm Springs Hit by Biggest Rain Storm in Its Entire History –

Newsweek

Global shares edged higher, even as China delivered smaller rate cuts than investors expected. Confusion over China’s approach to stemming the nation’s property slump

kept the more positive mood in check. Chinese lenders cut their one-year loan prime rate by 10 basis points and kept the five-year prime loan rates unchanged, even after policymakers called for more lending. Traders had expected a 15-basis-point cut on both

rates. There is still some expectation that Chinese authorities will step in with a more generous boost. Meanwhile, in geopolitical news, China’s military said it sent a warning to Taiwan with armed drills. The key event for the week is the US Federal Reserve’s

Jackson Hole conference.

EQUITIES:

US equity futures rose, set to trim three weeks of declines, with the S&P 500 down nearly 5% this month as investors brace for the potential of interest rates remaining higher for longer.

The next clues on the policy outlook will come from this week’s annual gathering of central bankers at Jackson Hole, Wyoming, with Federal Reserve Chairman Jerome Powell due to speak Friday. Goldman Sachs analysts believe there is room for investors to boost

stock exposure if the economy continues on the soft-landing path. Morgan Stanley’s Michael Wilson warned the risk-off “complexion” may last into the fall or winter. On the earnings front, the week’s key event is Wednesday’s report from Nvidia, the chipmaker

whose blowout revenue forecast helped ignite this year’s rally in artificial intelligence-linked stocks.

Futures ahead of the bell: E-Mini S&P +0.4%, Nasdaq +0.7%, Russell 2000 +0.25%, Dow +0.3%.

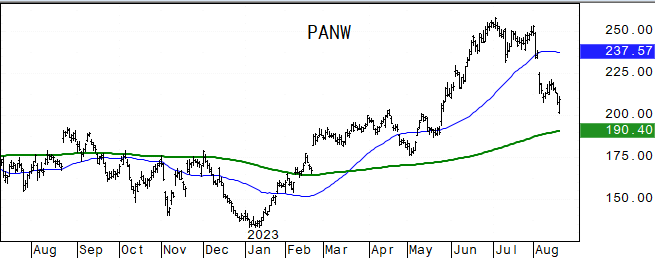

In premarket trading, Palo Alto Networks (PANW) rallied 12% after the cybersecurity company’s billings forecast beat estimates. Kenvue (KVUE) gains 2% after Johnson & Johnson said about

23.8% of tendered J&J shares will likely be swapped for Kenvue shares. Napco Security Technologies (NSSC) falls 35% after the electronic security device maker said it would have to restate three quarters of financial statements. XPeng’s ADRs (XPEV) gain 5.5%

after Bank of America upgrades the Chinese EV maker to buy from neutral.

European indices are higher, helped by disinflation hopes as annual German producer prices fell for the first time in two-and-a-half years. Germany’s Ifo institute reported the downturn

in residential construction deepened in July and UK homebuilder shares hit by a profit warning from Crest Nicholson that whacked the housebuilder’s shares by 15%. Earnings were also in focus with shares in Dutch payments processor Adyen (ADYEN.AS) dropping

another 6%, a 48% drop over the last three sessions, following Thursday’s weak earnings which raised concerns around its valuation. Stoxx 600 +0.6%, DAX +0.6%, CAC +1%, FTSE 100 +0.4%. Autos +1.5%, Energy +1.5%, REITS -1%.

Asian equities head for the longest losing streak since June 2022, led by Chinese stocks, as disappointment persists over the country’s stimulus measures to resuscitate economic activity.

The MSCI Asia Pacific Index fell 0.5%. Stocks slumped in Hong Kong and mainland China after Chinese banks surprised investors by making a smaller-than-expected cut to a key interest rate and keeping another on hold. Benchmarks climbed in Japan and South Korea.

Shares of major property developer Sunac China fell as much as 13% after it flagged a 16 billion yuan ($2.19 billion) net loss for the first half. Some Country Garden bondholders requested full repayment of a local bond due next month after the developer

proposed a three-year extension. Official figures also showed China’s government land sales revenue declined for the 19th consecutive month in July. Hang Seng Index -1.8%, CSI 300 -1.4%, ASX 200 -0.5%, Vietnam +0.1%, Kospi +0.2%, Topix +0.2%, Sensex +0.4%

FIXED INCOME:

Treasury yields resumed their advance, rising across the curve, led by long-end. The 10-year climbed toward the highest level since November 2007, while the 30-year

was near 2011 highs. 2s10s, 5s30s spreads steepen by 2bp and 3bp on the day. A major test comes this week as Treasury investors place their bids for two risky auctions: 20-year bonds and 30-year TIPS, demand for which is notoriously unpredictable. Focus this

week is on the Jackson Hole economic policy symposium, where Fed Chair Powell is scheduled to speak Friday.

METALS:

Gold prices traded modestly higher as the yellow metal aimed for back-to-back gains after a lengthy losing streak. Bullion has fallen for the last four weeks on signs

the US rate-hike cycle still has room to run, with minutes of the Federal Reserve’s July meeting showing concern among policy makers that inflation would fail to ease. Hedge funds have also dialed back their enthusiasm for gold, with net-long positions on

the Comex falling to a five-month low. Spot gold +0.2%, silver +1.9%.

ENERGY:

Oil prices rose with tightening supply from Saudi Arabia offsetting demand concerns. European benchmark gas prices jumped as much as 18% on fears of a strike in Australia.

Prices for liquefied natural gas were underpinned by the risk of a strike at Australian offshore facilities that could affect around 10% of global supply. Russia’s oil-product exports dropped in the first 12 days of August, Vortexa said. Prices of most of

the country’s main products — including diesel, fuel oil and naphtha — breached the G-7 price caps, complicating traders’ access to shipping logistics services and insurance. Separately, Russia’s crude supply to China fell by about 2 million tons to 8 million

month-on-month in July. Hilary came ashore in California late yesterday as its top winds eased to 40 miles per hour, down from 110 mph earlier, making it a tropical storm. WTI +1.2%, Brent +1.1%, US Nat Gas +3%, RBOB +0.5%.

CURRENCIES:

Flows are on the low side in the major currencies. The dollar is slightly lower after touching two month highs on Friday. The kiwi is flat versus the dollar as it

tries to halt a 10th straight daily drop, which would match the record losing streak in the pair. US$ Index -0.2%, GBPUSD +0.2%, AUDUSD +0.2%, USDJPY +0.3%, EURUSD +0.3%, NZDUSD +0.05%, EURJPY +0.6%.

Bitcoin -0.6%, Ethereum -0.8%.

TECHNICAL LEVELS:

|

ESU23 |

10 Year Yield |

Dec Gold |

Sept WTI |

Spot $ Index |

|

|

Resistance |

4548.00 |

5.325% |

2029.0 |

89.20 |

108.000 |

|

|

4522.00 |

4.710% |

2007.0 |

87.50 |

107.180 |

|

|

4497.00 |

4.500% |

1987.0 |

85.00 |

106.000 |

|

|

4484.00 |

4.375% |

1957.9 |

82.65 |

105.380 |

|

|

4410.00 |

4.325% |

1951.0 |

81.28 |

103.600 |

|

Settlement |

4350.00 |

1915.9 |

80.66 |

||

|

|

4325/30 |

3.900% |

1907.0* |

78.70 |

103.270 |

|

|

4310.00* |

3.700% |

1905.0 |

76.77 |

102.800 |

|

|

4265.00 |

3.590% |

1866.0 |

76.63 |

102.050 |

|

|

4202.00* |

3.265% |

1842.0 |

74.27 |

101.590 |

|

Support |

|

3.000% |

1796.7* |

71.76 |

101.100 |

Colors within the report:

Green is always the 200 period (day, week).

Red is always 21,

Blue = 50,

Brown =

100 *Stars have added importance

UPGRADES:

- Acushnet (GOLF) raised to buy at Jefferies; PT $84

- Appfolio (APPF) raised to overweight at Stephens; PT $212

- Cogent Comms (CCOI) raised to neutral at Goldman; PT $64

- Insulet (PODD) raised to buy at Citi; PT $265

- Liberty SiriusXM (LSXMA) raised to buy at Seaport Global Securities

- XPeng ADRs (XPEV) raised to buy at BofA; PT $22

DOWNGRADES:

- Alpha Metallurgical Resources Inc (AMR) cut to market perform at Cowen

- Coca-Cola Femsa ADRs (KOFUBL MM) cut to neutral at Grupo Santander; PT $96

- Embotelladora Andina ADRs (ANDINAA CI) cut to neutral at Grupo Santander

- Insulet (PODD) cut to neutral at Baird; PT $219

- Medical Properties (MPW) cut to underweight at JPMorgan; PT $7

- NSSC US (NSSC) cut to market perform at William Blair

- Sarcos Technology & Robotics (STRC) cut to hold at Jefferies; PT $1.15

- Tracon Pharmaceuticals (TCON) cut to hold at JonesTrading

INITIATIONS:

- Alphabet (GOOGL) rated new overweight at Guotai Junan Sec; PT $150.92

- Atour Lifestyle ADRs (ATAT) rated new buy at Sealand Securities

- Decisive Dividend (DE CN) rated new buy at Echelon Wealth; PT C$10.75

- Expro Group Holdings NV (XPRO) reinstated inline at Evercore ISI

- FMC Corp (FMC) rated new neutral at JPMorgan; PT $90

- GameSquare Holdings Inc (GAME CN) rated new buy at Roth MKM; PT C$9.48

- Grocery Outlet (GO) rated new overweight at Guotai Junan Sec

- Merus BV (MRUS) rated new outperform at Cowen

- Oceaneering (OII) reinstated inline at Evercore ISI; PT $24

- Restaurant Brands (QSR CN) rated new overweight at JPMorgan; PT C$111.05

- Target (TGT) rated new neutral at CTBC Securities; PT $138

Data sources: Bloomberg, Reuters, CQG

No responses yet