TODAY’S GAME PLAN: from the trading

desk, this is not research

DATA/HEADLINES 8:15ET ECB Rate Decision; 8:30ET Advance Goods Trade Balance, GDP, Durable Goods Orders, Weekly

Jobless Claims; Inventories; 10:00ET Pending Home Sales; 11:00ET KC Fed Mfg Activity; 1:00ET 7 year auction;

TODAY’S HIGHLIGHTS:

- Maine police are pursuing a suspect in two Lewiston shootings that left at least 16 people dead

- Hurricane Otis slammed Acapulco — wrecking roads, buildings and hotels

- Redfin Reports Buyers Get Some Relief As New Listings Finally Increase, More Sellers Drop Prices

Global stocks slid as high-profile earnings misses drained risk sentiment. Higher bond yields overnight dragged shares around the world to multi-month lows in the

middle of a busy week for corporate earnings, as investors awaited an ECB meeting and the release of US GDP. Israel said its ground forces pushed into Gaza overnight to attack Hamas targets as Israeli Prime Minister Netanyahu said it was “preparing for a ground

invasion” that could be one of several. Hamas has threatened to kill some of the more than 200 hostages it brought back to Gaza, of whom Israel says more than half hold foreign passports, from 25 countries.

EQUITIES:

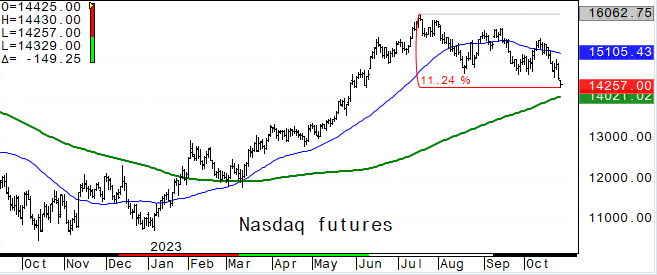

US equity futures are lower again as investors await third quarter GDP data which likely increased at a 4.3% annualized rate, which would be the fastest since the

fourth quarter of 2021. On Wednesday, the Russell 2000 closed at its lowest level since November 6, 2020. Year-to-date, the Russell 2000 is down 6% as the Nasdaq still sits on a hefty 22% gain and the S&P 500 is up 9%. Alphabet shares logged their worst session

since March 2020 overnight, dropping 9.5% as investors were disappointed with stalling growth in its cloud division. Shares in Meta fell 4% on Wednesday and another 3% in after-hours trade after publishing results showing better-than-expected revenue but a

cloudy outlook. Meanwhile, the United Auto Workers reached a tentative labor agreement with Ford Motor Co., putting pressure on the carmaker’s two chief rivals to end a protracted strike that has cost the industry billions of dollars. UAW leadership will

vote on the deal Oct. 29.

Futures ahead of the bell: E-Mini S&P -0.8%, Nasdaq -1.1%, Russell 2000 -0.5%, Dow -0.4%.

In pre-market trading, Align Technology (ALGN) shares slid 24% after the maker of dental aligners cut its net revenue guidance for the full year. Mattel (MAT) dropped 10% after the toy

manufacturing and entertainment company maintained its full-year sales outlook, citing softness in the industry and a weaker global economy. UPS slumped more than 3% after cutting its annual profit forecast. Endeavor Group (EDR), the company behind WWE and

UFC, soared 23% after private equity group Silver Lake Management said it’s considering a takeover bid. Ford (FORD) rose over 2%, set to extend gains to a second session, as the UAW reached a tentative labor agreement with the carmaker. Adobe (ADBE) edged

0.7% higher as Oppenheimer joins DA Davidson in turning bullish on the stock.

European stocks dropped, bringing the benchmark Stoxx 600 close to wiping out its 2023 gains, as glum company results in Europe and the US hit risk appetite before the European Central

Bank’s rate decision. The Stoxx 600 is down ~1% with automakers and banks declining the most. British lender Standard Chartered fell over 9% while setting aside more cash to cover China-related losses, underscoring how a property crash and slowing growth in

the world’s second-largest economy is hitting international banks. Mercedes-Benz Group AG declined 6% after reporting a drop in third-quarter margins from a year ago as car prices declined and inflation fanned the cost of everything from components to labor.

Siemens Energy plummeted 36% after saying it’s seeking about $16.9 billion in guarantees from the German government. DAX -1.5%, CAC -1%, FTSE 100 -0.9%. Autos -2.5%, Banks -1.75%, Retail -1.7%.

Asian stocks slumped the most in three weeks, with technology shares leading the declines following another surge in Treasury yields and weak earnings by some of the sector’s bellwether

companies. The MSCI Asia Pacific Index slid 1.4% with Chinese sportswear maker Li Ning the top loser after it reported lackluster sales for the third quarter. The MSCI Asia gauge is down close to 5% this month, widening its 2023 underperformance versus peers

in the US and Europe. Korean EV battery stocks were sharply lower, as poor earnings from sector bellwethers and a bleak EV sales outlook continue to batter investor sentiment. China’s regional banks dropped after Citi said the local government financing vehicle

debt issue is a risk for the lenders. Vietnam -4.2%, Kospi -2.7%, Nikkei 225 -2.1%, Taiwan -1.7%, Sensex -1.4%, ASX 200 -0.6%, Hang Seng Index -0.25%. China’s CSI 300 +0.3%, Hang Seng Tech +0.3%.

FIXED INCOME:

Treasuries are narrowly mixed with the curve slightly steeper as yields broadly hold within one basis point of Wednesday’s session close. Core European rates outperform

Treasuries ahead of the ECB rate decision. US session focus includes GDP data while this week’s auction’s conclude with $38 billion 7-year note sale. US third quarter GDP is unlikely to provide help for the bond market as it is expected to show the economy

grew at its fastest quarterly pace in two years. Friday’s personal consumption expenditure (PCE) price index, the Fed’s preferred inflation gauge, is also top of mind. US 10-year yields around 4.97%, up 1bp.

METALS:

Gold rose for a second day after Israel’s military said it made a limited ground raid of Gaza, fueling concerns of the conflict spilling over. Bullion has risen more than 8% since the

Oct. 7 attacks by Hamas. Infantry and tanks entered northern Gaza to attack numerous cells before withdrawing, the IDF said. A full invasion of the enclave is currently being prepared, according to Israeli Prime Minister Netanyahu. Attention will turn to US

economic data including third-quarter gross domestic product today for clues on the Fed’s next move. Swaps traders are all but unanimous on the central bank holding rates steady next week. Spot gold +0.2%, silver +0.2%.

ENERGY:

Oil prices declined, paring a portion of the gains seen the previous day, driven by heightened tensions in the Middle East. Global oil inventories — both commercial

and in strategic reserves — have collapsed to a multiyear low as OPEC+ curtails production, reducing the available cushion just as the crisis in the Middle East raises the possibility of supply disruptions. Worldwide stockpiles sank to 3.31 billion barrels

this month, according to intelligence firm Kpler, the lowest since it started tracking the figure in January 2017. WTI -1.9%, Brent -1.8%, US Nat Gas +0.3%, RBOB -1%.

CURRENCIES:

In currency markets, the dollar index hit a two-week high, driven by higher yields, and the yen weakened past 150 per dollar, a level that has put traders on guard

for intervention. The euro stayed under pressure ahead of the European Central Bank policy decision. US$ Index +0.3%, GBPUSD -0.3%, EURUSD -0.3%, USDJPY +0.1%, AUDUSD -0.1%, USDNOK +0.6%.

Bitcoin -1.4%, Ethereum +1.5%. Sam Bankman-Fried is expected to take the stand today

TECHNICAL LEVELS:

|

ESZ23 |

10 Year Yield |

Dec Gold |

Dec WTI |

Spot $ Index |

|

|

Resistance |

4331.00 |

6.000% |

2100.0 |

93.10 |

110.000 |

|

|

4300.00 |

5.750% |

2081.0 |

92.13 |

108.970 |

|

|

4270.00 |

5.500% |

2056.0 |

89.85 |

107.990 |

|

|

4242.00 |

5.325% |

2028.6 |

88.13 |

107.350 |

|

|

4223.00 |

5.000% |

2012.7 |

86.30 |

106.785 |

|

Settlement |

4209.75 |

1994.9 |

85.39 |

||

|

|

4202.00* |

4.800% |

1956.0 |

84.70 |

105.270 |

|

|

4190.00 |

4.490% |

1944.7 |

81.50 |

104.380* |

|

|

4172.00 |

3.925% |

1921.2 |

79.35 |

103.800 |

|

|

4150.00 |

3.870% |

1894.0 |

78.22 |

103.330 |

|

Support |

4114.00 |

3.500% |

1863.0 |

75.63 |

|

Colors within the report:

Green is always the 200 period (day, week).

Red is always 21,

Blue = 50,

Brown =

100 *Stars have added importance

- Upgrades

- (ADBE) Adobe Raised to Outperform at Oppenheimer; PT $660

- (ADBE) Raised to Buy at DA Davidson

- (AKAM) Akamai Raised to Neutral at Guggenheim

- (CNTA) CNTA US Raised to Equal-Weight at Morgan Stanley; PT $8

- (CP CN) Canadian Pacific Kansas Raised to Outperform at Raymond James

- (IBP) Installed Building Raised to Buy at Benchmark; PT $150

- (MSFT) Microsoft Raised to Buy at HSBC; PT $413

- (OKTA) Okta Raised to Buy at Daiwa; PT $87

- (SNAP) Snap Raised to Hold at China Renaissance; PT $9

- (SQM/B CI) SQM ADRs Raised to Sector Outperform at Scotiabank; PT $84

- (UMBF) UMB Financial Raised to Buy at Janney Montgomery; PT $73

- Downgrades

- (ARQT) Arcutis Biotherapeutics Cut to Neutral at Mizuho Securities

- (AY) Atlantica Sustainable Cut to Market Perform at Raymond James

- (BBWI) Bath & Body Works Cut to Hold at Jefferies; PT $30

- (BOKF) BOK Financial Cut to Equal-Weight at Wells Fargo; PT $70

- (FFIV) F5 Inc Cut to Underperform at BofA

- (FM CN) First Quantum Minerals Cut to Sector Perform at RBC; PT C$38

- (FTV) Fortive Cut to Neutral at BofA; PT $70

- (HES) Hess Cut to Neutral at Susquehanna; PT $160

- (MXL) MaxLinear Cut to Neutral at Roth MKM; PT $18

- (PZZA) Papa John’s Cut to Neutral at Wedbush; PT $95

- (TMO) Thermo Fisher Cut to Sector Weight at KeyBanc

- (VMI) Valmont Cut to Neutral at Northcoast

- Initiations

- (AA) Alcoa Rated New Buy at DBS Bank; PT $41

- (ELVA CN) Electrovaya Rated New Buy at Seaport Global Securities; PT $7

- (EVER) EverQuote Resumed Market Perform at Raymond James

- (FDMT) 4D Molecular Rated New Outperform at RBC; PT $25

- (NILI CN) Surge Battery Metals Inc Rated New Buy at Roth MKM; PT C$3

- (PCOR) Procore Technologies Rated New Outperform at BMO; PT $80

- (RKLB) Rocket Lab USA Rated New Overweight at Cantor; PT $6

Data sources: Bloomberg, Reuters, CQG

No responses yet