TODAY’S GAME PLAN: from the trading

desk, this is not research

DATA/HEADLINES 8:15ET ADP Employment Change; 8:30ET Treasury quarterly refunding announcement; 9:45ET S&P Global

US Manufacturing PMI; 10:00ET Construction Spending, JOLTS Job Openings, ISM Manufacturing; 2:00ET FOMC Rate Decision; 2:30ET Fed’s Powell speaks

TODAY’S HIGHLIGHTS:

- The Raiders fired coach Josh McDaniels and GM David Ziegler

- Japan Stimulus Package To Include $144 Billion In Spending

- Three people were shot on Halloween night in Bear’s Salem Woods community in Delaware

Global shares fluctuated ahead of a policy decision from the US Federal Reserve, with the central bank widely expected to hold rates steady. Data showed Asia’s manufacturers

faced worsening pressure in October with factory activity in China slipping back into decline, clouding recovery prospects for the region’s major exporters already squeezed by weaker global demand and higher prices. The Bank of Japan intervened in the government

bond market to rein in a jump in yields to fresh decade highs. The Israeli military said it had deployed missile boats in the Red Sea on Wednesday, a day after the Iran-aligned Houthi movement said it had launched missile and drone attacks on Israel and vowed

to carry out more. Some foreigners and wounded Palestinians were allowed to leave Gaza for the first time since Israel began its ground invasion.

EQUITIES:

US equity futures slipped ahead of the Federal Reserve interest-rate decision and the government’s new borrowing plan. The Fed is expected to hold rates steady, while

leaving open the possibility of another hike as soon as December. The market is fully priced for a pause. More than 80% of the stocks in the S&P 500 strengthened yesterday, with a loss of 2.2% for the month. That’s its third straight monthly drop, the longest

losing streak since the COVID pandemic froze the global economy at the start of 2020. Investors have bullish seasonality on their side as the calendar flips to November, historically kicking off the best six months of the year for US equities.

Futures ahead of the bell: E-Mini S&P -0.3%, Nasdaq -0.4%, Russell 2000 -0.6%, Dow -0.3%.

In premarket trading, WeWork plunged 42% after the Wall Street Journal reported that the company plans to file for bankruptcy as early as next week. Canada Goose (GOOS) slides 9.5% after

the apparel company slashed its annual forecasts. First Solar (FSLR) rose 4% amid optimism among analysts of higher shipment volumes. Paycom Software (PAYC) plunged 35% after the employment software company slashed its full-year forecast, with the move weighing

on peers. Advanced Micro Devices (AMD) shares slide 2.4% after the chipmaker gave a revenue forecast that is weaker than expected. Crispr Therapeutics (CRSP) jumped as much as 17% after the company’s potential gene-editing treatment for sickle cell disease

gained support from some advisers to the US FDA. Match Group (MTCH) fell 9% after the dating-app firm provided fourth-quarter revenue guidance that fell short. Estée Lauder (EL) slips 15% after the company lowered its full-year outlook. Lumen Technologies

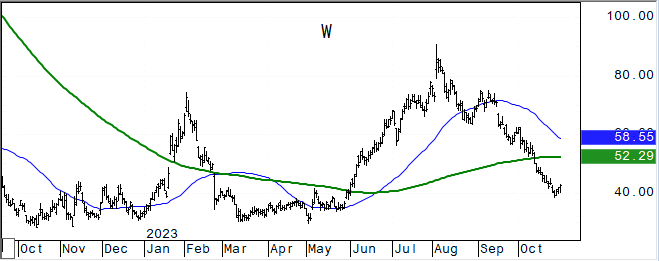

(LUMN) shares are down 5.5% after the wireline telecommunications company reported third-quarter results that are seen as mixed. MasTec (MTZ) tumbles about 16% after the infrastructure construction firm cut its year profit and revenue forecast. Wayfair (W)

drops 13% after posting 3Q results. Yum China (YUMC) drops 12% after the restaurant operator reported third-quarter comparable sales that fell short of estimates.

European gauges were steady as investors awaited a Federal Reserve interest rate decision and assessed a slew of company earnings. European retailers outperformed the broader market,

led by Next Plc as it increased its profit guidance. Orsted A/S plunged 22% after taking a $4 billion hit on abandoned US wind projects. Orsted dropped over 20% after halting the development of two US wind projects and writing down $4 billion. Many European

countries are celebrating “All Saints Day” holiday so flows have been light. Stoxx 600 is flat, DAX flat, CAC -0.05%, FTSE 100 -0.1%. Retail +0.8%, Insurance +0.6%, Healthcare +0.5%. Media underperforms, down 0.7%.

Asian stocks rose, boosted by Japanese shares after the Bank of Japan maintained its negative-rate policy. Purchasing managers’ indexes in China, Japan and South Korea showed activity

shrinking while Vietnam and Malaysia also struggled with the broadening fallout from a Chinese slowdown. China’s Caixin/S&P Global manufacturing PMI fell to 49.5 in October from 50.6 in September, a private sector survey showed. Japan’s factory activity shrank

for a fifth straight month in October. South Korea’s factory activity fell for a 16th straight month while PMIs from Taiwan, Vietnam and Malaysia also showed continued declines in activity. The MSCI Asia Pacific Index climbed 1%, with Toyota Motor Co. and

Mitsubishi Electric Corp. among the biggest contributors. Toyota jumped 4.7% after raising its operating profit forecast 50% and posting record quarterly earnings thanks to a weaker yen. Topix +2.5%, Vietnam +1.1%, Kospi +1%, ASX 200 +0.85%, Taiwan +0.2%,

Shanghai Composite +0.15%, Hang Seng Index -0.05%, Sensex -0.4%, Indonesia -1.6%.

FIXED INCOME:

Treasury yields declined ahead of the Treasury’s quarterly refunding announcement and Fed rate decision, with yields lower by 2bp to 4bp across the curve. The recent

surge in US Treasury yields has contributed to a tightening of financial conditions, leading even hawkish Federal Open Market Committee members to indicate patience over further rate moves. Cleveland Fed Bank President Loretta Mester said ahead of the November

monetary policy meeting that higher bond yields are equivalent to one interest rate hike of 25 basis points. The Fed could use higher Treasury yields as a substitute for further policy tightening. The Fed is poised for a hawkish pause today, though bond traders

are more focused on the Treasury’s borrowing plans. At 8:30ET, the Treasury quarterly refunding is expected to unveil another round of increases to its note and bond auctions. Japanese bond futures pared their losses slightly after the BOJ announced unscheduled

bond-purchase operations as the 10-year bond yield approached 1%. US 10-year yields around 4.90%.

METALS:

Gold steadied ahead of the Federal Reserve’s interest-rate decision; even as high US bond yields weighed. Swaps traders are betting that policymakers will keep rates on hold today but

will scrutinize any forward-looking steer provided by the central bank. Traders are also bracing for a deluge of note and bond supply amid expectations the Treasury will unveil plans for bigger debt sales at a quarterly refunding announcement today. Spot

gold +0.05%, silver -0.7%.

ENERGY:

Oil prices are higher as investors await a Federal Reserve policy decision as they continue to monitor developments around the Israel-Hamas war. Israeli airstrikes

leveled apartment buildings in Gaza and ground troops battled Hamas. Investors were also awaiting the latest round of official US petroleum inventory figures due later in the morning. US oil demand reached its highest level in four years in August, driven

by record seasonal diesel consumption, government data showed. Meanwhile, the Panama Canal’s driest October since 1950 is adding journey times and costs for the shipping of fuels. The number of vessels that can be booked for passage will decline in November

and remain reduced through at least February. WTI +2%, Brent +1.9%, US Nat Gas -2.8%, RBOB +1.4%.

CURRENCIES:

The dollar headed for a second day of gains ahead of the Federal Reserve policy decision while the yen gained against all Group-of-10 peers after Japan’s Ministry

of Finance stepped up its verbal intervention. The yen strengthened after Japan’s foreign exchange chief said he was on standby for intervention. The currency fell sharply on Tuesday after the Bank of Japan’s underwhelming tweak to its cap on bond yields suggested

any move away from ultra-loose policy would be slow and gradual. US$ Index +0.2%, GBPUSD -0.2%, EURUSD -0.3%, EURJPY -0.6%, USDJPY -0.3%, AUDUSD is flat, USDNOK +0.3%.

Bitcoin -0.6%, Ethereum -0.8%.

TECHNICAL LEVELS:

|

ESZ23 |

10 Year Yield |

Dec Gold |

Dec WTI |

Spot $ Index |

|

|

Resistance |

4364.00 |

6.000% |

2100.0 |

93.10 |

110.000 |

|

|

4313.00 |

5.750% |

2081.0 |

92.13 |

108.970 |

|

|

4266.00 |

5.500% |

2056.0 |

89.85 |

107.990 |

|

|

4240.00 |

5.325% |

2029.4 |

88.13 |

107.350 |

|

|

4215.00 |

5.000% |

2019.7 |

86.32 |

106.785 |

|

Settlement |

4212.25 |

1994.3 |

81.02 |

||

|

|

4179.00 |

4.800% |

1983.6 |

80.20 |

105.590 |

|

|

4157.00 |

4.530% |

1964.0 |

78.27 |

104.380 |

|

|

4142.00 |

3.925% |

1945.2 |

76.70 |

103.800 |

|

|

4123.00 |

3.650% |

1921.2 |

75.60 |

103.420 |

|

Support |

4104.00 |

3.255% |

1894.0 |

74.25 |

102.550 |

Colors within the report:

Green is always the 200 period (day, week).

Red is always 21,

Blue = 50,

Brown =

100 *Stars have added importance

- Upgrades

- Cemig (CMIG4 BZ) ADRs Raised to Buy at HSBC; PT $2.90

- Cirrus Logic (CRUS) Raised to Buy at Loop Capital; PT $100

- Context Therapeutics (CNTX) Raised to Buy at HC Wainwright; PT $5

- Eaton Corp (ETN) Raised to Strong Buy at CFRA; PT $245

- Ecolab (ECL) Raised to Buy at CFRA; PT $193

- Ford (F) Raised to Overweight at Barclays; PT $14

- General Motors (GM) Raised to Overweight at Barclays; PT $37

- IPG Photonics (IPGP) Raised to Buy at CFRA; PT $113

- JD.com (JD) ADRs Raised to Buy at UBS; PT $39

- NRG Energy (NRG) Raised to Buy at Guggenheim

- Progressive (PGR) Raised to Equal-Weight at Morgan Stanley; PT $160

- Saia (SAIA) Raised to Buy at Stifel; PT $425

- Shopify (SHOP CN) Raised to Neutral at BNPP Exane; PT C$69.39

- Toromont Industries (TIH CN) Raised to Outperform at BMO; PT C$116

- Trex (TREX) Raised to Strong Buy at CFRA; PT $77

- Downgrades

- Geodrill (GEO CN) Cut to Hold at Beacon Securities; PT C$1.70

- Paycom Software (PAYC) Cut to Neutral at Citi; PT $189

- Cut to Market Perform at Oppenheimer

- Cut to Hold at Deutsche Bank; PT $175

- Cut to Market Perform at Cowen; PT $202

- Cut to Sector Weight at KeyBanc

- Cut to Hold at Stifel; PT $160

- Cut to Neutral at Piper Sandler; PT $185

- Stevanato Group (STVN) Cut to Hold at Jefferies; PT $29

- UFP Packaging (UFPI) Cut to Neutral at DA Davidson; PT $106

- ZoomInfo (ZI) Cut to Neutral at Goldman; PT $17

- Initiations

- BAT (BATS LN) ADRs Rated New Overweight at Morgan Stanley; PT $38

- Decisive Dividend (DE CN) Rated New Buy at Canaccord; PT C$10

- Eyenovia (EYEN) Rated New Outperform at William Blair

- Haleon (HLN LN) ADRs Rated New Overweight at Morgan Stanley; PT $9

- Polestar (PSNY) ADRs Rated New Overweight at Piper Sandler; PT $3

- Regenxbio (RGNX) Rated New Buy at Stifel; PT $35

- Six Flags (SIX) Rated New Underweight at JPMorgan; PT $16

- Tradeweb (TW) Rated New Buy at William O’Neil

- Vinfast Auto Ltd (VFS) Rated New Overweight at Cantor; PT $7

Data sources: Bloomberg, Reuters, CQG

No responses yet