TODAY’S GAME PLAN: from the trading

desk, this is not research

DATA/HEADLINES 8:00ET Fed’s Barr speaks; 8:30ET *Employment Report; 9:45ET S&P Global US Services PMI; 10:00ET

ISM Services Index, Fed’s Barkin speaks; 12:45ET Fed’s Kashkari speaks; 3:30ET Fed’s Bostic speaks, Fed’s Barr speaks

TODAY’S HIGHLIGHTS:

- Elon Musk says AI will eventually create a situation where ‘no job is needed’

- Israeli troops have surrounded Hamas stronghold of Gaza City

- FTX founder Sam Bankman-Fried found guilty, faces a maximum sentence of 115 years in prison

Global stocks rose and are on track for their biggest weekly rise in a year, with the MSCI World index +4.3% for the week. Bets are mounting that central banks are

preparing to close the chapter on the steepest rate hikes since the early 1980s, reinforced by signs that economic growth and inflation are slowing. Investors pumped a net $1.79 billion into global equity funds in the week leading to November 1, the first

weekly inflow in seven, thanks to a surge in demand in Asia. US Secretary of State Antony Blinken arrived in Tel Aviv for talks as Israeli troops encircled Gaza City amid intense aerial bombardment. Israel says a cease-fire with Hamas isn’t on the table after

calls from the US for a pause.

EQUITIES:

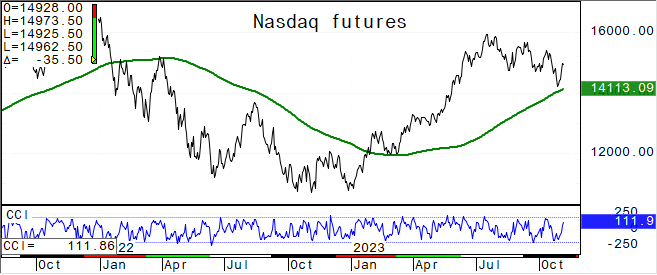

US equity futures fluctuated in subdued trading overnight as investors awaited key employment figures after data on Thursday suggested the US economy might finally

be cooling. Economists expect the US economy added 180,000 jobs in October, after the blockbuster 336,000 increase in September. Nasdaq futures underperform after Apple delivered a sales forecast for the holiday quarter that missed Wall Street expectations.

China’s commerce minister told Micron Technology’s president Beijing would welcome the US semiconductor company deepening its footprint in the Chinese market.

Futures ahead of the bell: E-Mini S&P -0.1%, Nasdaq -0.3%, Russell 2000 +0.3%, Dow -0.02%.

In premarket trading, Apple fell ~3% after revenue from the greater China region disappointed investors. Bill Holdings (BILL) shares tumble 35% after the financial software company cut

its annual revenue forecast. Block Inc. (SQ) jumped 17% after the digital payments firm posted third-quarter results that beat and boosted its full-year outlook. Coinbase (COIN) trades 4% lower after third-quarter retail trading volume fell short of estimates.

Confluent (CFLT) shares gain 3% after Guggenheim Securities raised the recommendation on the software company to buy from neutral. Expedia (EXPE) rose 9% after reporting third-quarter earnings that beat estimates and announced a $5 billion share buyback.

Fortinet (FTNT) shares tumbled 24% as the cybersecurity firm cut its billings forecast for the year while at least four brokerages downgraded their rating on the stock after the company’s weak results and guidance. Nio ADRs (NIO) rose 3% as the Chinese EV

maker said it is cutting jobs and may spin off non-core businesses to reduce costs and improve efficiency.

European stocks posted modest gains, rounding off a weekly rally powered by a series of solid earnings and a perceived dovish tilt by central banks. Eurozone unemployment came in at 6.5%,

estimate was 6.4%. The Stoxx 600 added about 0.2% to its strongest week since March, with Real Estate and Autos leading gains. BMW AG rose over 3.5% after increased sales of fully electric vehicles boosted margins. A.P. Moller-Maersk A/S, a bellwether for

global trade, slumped more than 15% after saying it’s cutting at least 10,000 jobs to shield its profitability. Shipping stocks slide in Europe, as Maersk warns of subdued demand, noting that overcapacity is triggering price drops. Stoxx 600 +0.1%, DAX +0.2%,

CAC -0.1%, FTSE 100 -0.1%. REITs +1.8%, Autos +1.5%, Retail +1.1%, Banks +1%.

Shares in Asia were broadly higher as risk sentiment improved on bets that the Federal Reserve may be done with its most aggressive interest rate hikes in decades. The MSCI Asia Pacific

Excluding Japan Index rose 1.7%, with Tencent, AIA Group and Alibaba among the biggest contributors. All major markets in the region were in the green, while Japan was closed for a holiday. Apple suppliers in Asia were mixed after the iPhone maker projected

fiscal first-quarter revenue that fell short of expectations. A private sector survey showed China’s services activity expanded at a slightly faster pace in October, but sales

grew at the softest rate in 10 months. Hang Seng Index +2.5%, Singapore +2%, ASX 200 +1.1%, Kospi +1.1%, China’s CSI 300 +0.8%, Taiwan +0.7%, Sensex +0.4%, Vietnam +0.1%.

FIXED INCOME:

Treasuries are narrowly mixed ahead of the jobs data, with the curve slightly steeper as long-end yields trade cheaper by around 2bp on the day. Four Fed speakers

are also scheduled for today, who may offer additional policy outlook. US 10-year yields around 4.65%, 2 year yield ~4.99%. The long-end lags slightly, re-steepening 5s30s spread by 2.5bp to ~19bp and unwinding a small portion of Thursday’s aggressive flattening

move. 2s10s slightly flatter around 33bps. UBS anticipates the 10-year yield will fall to 3.5% by June next year, as the Fed shifts its attention from rate hikes to rate cuts.

METALS:

Gold fluctuated overnight and is headed for its first weekly decline in four, with haven demand easing as the Israel-Hamas war remained contained. Spot gold +0.1%, silver -0.5%.

ENERGY:

Oil futures rose but remained on track for a second straight weekly fall after fears of a widening of the Israel-Hamas war faded and investors renewed their focus

on the outlook for demand. Crude has mostly given up its war premium as the conflict hasn’t endangered supplies from the region, the source of about a third of the world’s oil. US refining margins rebounded to their highest level in about a month. WTI +0.8%,

Brent +0.6%, US Nat Gas +0.3%, RBOB +0.1%.

CURRENCIES:

In currency markets, the dollar is lower for a third straight day, dragged lower by US treasury yields. USDJPY heads for a third day of losses for the first time

in three months. The Swedish krona leads G-10 gains; USD/SEK down as much as 0.5%. US$ Index -0.2%, GBPUSD +0.2%, EURUSD +0.2%, AUDUSD +0.15%, USDJPY -0.2%, NZDUSD +0.4%.

Bitcoin %, Ethereum %. Bankman-Fried, founder of the collapsed crypto exchange FTX, was found guilty of seven counts of fraud and conspiracy after jurors in Manhattan

deliberated for less than five hours Thursday. The verdict came just shy of one year after FTX filed for bankruptcy in a swift corporate meltdown that shocked financial markets and erased his estimated $26 billion personal fortune. Cathie Wood said Bitcoin

is “digital gold” as a deflation hedge.

TECHNICAL LEVELS:

|

ESZ23 |

10 Year Yield |

Dec Gold |

Dec WTI |

Spot $ Index |

|

|

Resistance |

4470.00 |

6.000% |

2100.0 |

92.13 |

110.000 |

|

|

4438.00 |

5.750% |

2081.0 |

89.85 |

108.970 |

|

|

4403.00 |

5.500% |

2056.0 |

88.13 |

107.990 |

|

|

4376.00 |

5.325% |

2029.4 |

86.32 |

107.350 |

|

|

4337/38 |

5.000% |

2019.7 |

85.88 |

106.785 |

|

Settlement |

4335.75 |

1993.5 |

82.46 |

||

|

|

4312.00 |

4.545% |

1983.6 |

80.20 |

105.660 |

|

|

4270.00 |

4.350% |

1964.0 |

78.31 |

104.380 |

|

|

4255.00 |

3.930% |

1947.1 |

76.70 |

103.800 |

|

|

4186.00 |

3.650% |

1921.5 |

75.60 |

103.420 |

|

Support |

4158.00 |

3.265% |

1898.4 |

74.25 |

102.550 |

Colors within the report:

Green is always the 200 period (day, week).

Red is always 21,

Blue = 50,

Brown =

100 *Stars have added importance

- Upgrades

- Airbnb (ABNB) Raised to Buy at Phillip Secs; PT $157

- Aptiv (APTV) Raised to Neutral at Piper Sandler

- Baytex Energy (BTE CN) Raised to Outperform at National Bank; PT C$9.25

- BioCryst (BCRX) Raised to Buy at Jefferies; PT $10

- Confluent (CFLT) Raised to Buy at Guggenheim; PT $23

- Raised to Outperform at Wolfe; PT $21

- East West Bancorp (EWBC) Raised to Outperform at Wedbush; PT $69

- Epam Systems (EPAM) Raised to Overweight at Piper Sandler; PT $265

- Essential Utilities (WTRG) Raised to Buy at Edward Jones

- First Horizon (FHN) Raised to Outperform at Wedbush; PT $14

- Generac (GNRC) Raised to Buy at Guggenheim; PT $142

- Lundin Mining (LUN CN) Raised to Outperform at National Bank

- Moderna (MRNA) Raised to Hold at HSBC; PT $69

- Molson Coors (TAP) Raised to Hold at Deutsche Bank; PT $58

- Omnicell (OMCL) Raised to Equal-Weight at Wells Fargo; PT $28

- Raised to Overweight at Piper Sandler; PT $39

- Outlook Therapeutics Inc (OTLK) Raised to Buy at HC Wainwright; PT $2

- PayPal (PYPL) Raised to Outperform at KGI Securities; PT $70

- Rapid7 (RPD) Raised to Outperform at Wolfe; PT $56

- Regeneron (REGN) Raised to Outperform at Raymond James; PT $950

- Uber (UBER) Raised to Overweight at KeyBanc; PT $60

- Zillow (ZG) Raised to Strong Buy at CFRA; PT $47

- Downgrades

- AMN Healthcare (AMN) Cut to Hold at Benchmark

- Cut to Hold at Jefferies; PT $70

- Apple (AAPL) Cut to Neutral at Fubon; PT $190

- BILL Holdings Inc (BILL) Cut to Sector Weight at KeyBanc

- Cheniere Energy Partners (CQP) Cut to Sell at Stifel; PT $53

- Comerica (CMA) Cut to Neutral at Wedbush; PT $45

- Cross Country Health (CCRN) Cut to Hold at Jefferies; PT $21

- Estee Lauder (EL) Cut to Hold at Berenberg; PT $118

- First Foundation (FFWM) Cut to Neutral at Wedbush; PT $6

- Fortinet (FTNT) Cut to Market Perform at William Blair

- Cut to Neutral at JPMorgan; PT $52

- Cut to Inline at Evercore ISI; PT $51

- Cut to Hold at Stifel; PT $52

- Cut to Neutral at Cantor; PT $50

- Cut to Market Perform at Oppenheimer

- Fox Corp (FOXA) Cut to Neutral at JPMorgan; PT $36

- Fox Factory (FOXF) Cut to Neutral at B Riley; PT $80

- Cut to Hold at Stifel; PT $80

- Holley (HLLY) Cut to Market Perform at Telsey; PT $9

- JPMorgan (JPM) Cut to Hold at Odeon Capital; PT $140

- New York Community Bancorp (NYCB) Cut to Neutral at Wedbush; PT $11

- Omnicell (OMCL) Cut to Neutral at BTIG

- Papa John’s (PZZA) Cut to Hold at Stifel; PT $65

- Sangamo (SGMO) Cut to Sector Perform at RBC; PT $2

- Schneider National (SNDR) Cut to Neutral at Susquehanna; PT $23

- Skyworks (SWKS) Cut to Hold at Summit Insights

- SolarEdge (SEDG) Cut to Peerperform at Wolfe

- Southern Co (SO) Cut to Sector Perform at Scotiabank; PT $78

- Stag Industrial (STAG) Cut to Sector Perform at RBC; PT $39

- Stem Inc (STEM) Cut to Neutral at Guggenheim

- Initiations

- Allied Gold (AAUC CN) Rated New Outperform at CIBC; PT C$8

- Amazon (AMZN) Rated New Buy at William O’Neil

- Crane Co. (CR) Rated New Buy at William O’Neil

- Microsoft (MSFT) Rated New Buy at Cinda Securities

- Netflix (NFLX) Rated New Buy at CMB International; PT $512

- Pinterest (PINS) Reinstated Buy at William O’Neil

- Veralto (VLTO) Rated New Sector Perform at RBC; PT $78

Data sources: Bloomberg, Reuters, CQG

No responses yet