TODAY’S GAME PLAN: from the trading

desk, this is not research

DATA/HEADLINES 9:15ET Fed’s Powell speaks; 10:00ET Wholesale Inventories; 1:00ET US $40B 10-year auction; 1:40ET

Fed’s Williams speaks; 2:00ET Fed’s Barr speaks; 4:45ET Fed’s Jefferson speaks

TODAY’S HIGHLIGHTS:

- According to a new NCRI report, at least 200 American colleges and universities illegally withheld information

on approximately $13 billion in undisclosed contributions from foreign regimes

link - Virginia Democrats sweep legislative elections after campaigning on abortion rights

- Miami hosts the third GOP presidential debate tonight

- US 30-Year Mortgage Rate Tumbles by Most in More Than a Year

Global stocks edged lower as investors awaited clues on the path of interest rates from a raft of central bank officials including Federal Reserve Chair Jerome Powell.

Up today are US policymakers including Powell, New York Fed President John Williams and three other policy makers, as well as Bank of England Governor Andrew Bailey and officials from the European Central Bank. Traders are waiting to see if Powell will push

back against rate-cut talk. If the Fed pivots its monetary policy and allows the economy to avoid a recession, global equities could be poised for a double-digit rally in 2024, according to HSBC strategists. President Biden and Xi Jinping are expected to meet

Nov. 15 in San Francisco for the Asia-Pacific Economic Cooperation summit.

EQUITIES:

US equity futures fluctuated as traders await Fed Chair Jerome Powell and other Fed speakers. They are widely expected to follow other policymakers in downplaying

the likelihood of policy easing. The Fed’s Neel Kashkari said policymakers have yet to win the fight against inflation and they will consider more tightening if needed. Austan Goolsbee said officials don’t want to “pre-commit” decisions on rates.

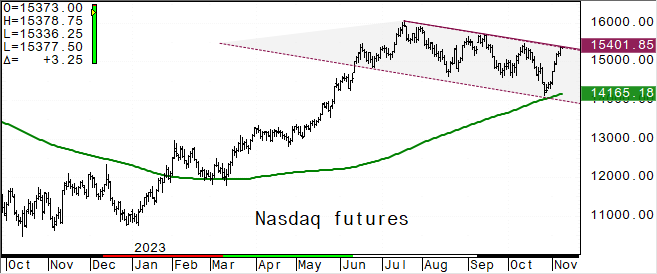

Futures ahead of the bell: E-Mini S&P +0.1%, Nasdaq +0.1%, Russell 2000 .0.0%, Dow +0.1%. Nasdaq testing the top of the descending trend channel. S&P has some room before testing key

.618 Fibonacci retrace.

In pre-market trading, Array (ARRY) shares fall 11% as the maker of renewable energy equipment cut its revenue guidance for the full year. Coupang (CPNG) falls 6% as the online retailer’s

3Q profit missed analysts’ estimates. EBay (EBAY) shares fall 7% after lowering Q4 guidance. Lucid (LCID) fell 5% after the electric-vehicle startup lowered its full-year production forecast. Nerdy (NRDY) tumbled 25% after the online learning company cut its

projection for revenue. Rivian (RIVN) rose 7% after the electric-vehicle startup boosted its production guidance and ended an exclusivity agreement to sell battery-electric vans to Amazon.com. Robinhood (HOOD) dropped 8% after the online brokerage’s results

fell short. Sleep Number (SNBR) plummeted 33% after cutting its outlook for the full year. Take-Two (TTWO) rose 8.5% on a report of plans to announce the next highly anticipated Grand Theft Auto game as early as this week. Upstart (UPST) shares fall 23% after

the AI lending marketplace firm reported third-quarter results that missed expectations. Upwork (UPWK) jumped 20% as the online-recruitment company boosted its revenue guidance for the full year. Bumble (BMBL) falls 6% after giving a worse-than-expected revenue

outlook. Enovix (ENVX) gains 16% after the company reported a third-quarter loss that was narrower than expected. Toast (TOST) falls 17% after the restaurant-software company gave a disappointing outlook. Vroom (VRM) falls 17% after the automotive retailer

reported third-quarter revenue that missed expectations.

European gauges were little changed, while companies reported mixed results at the tail end of the earnings season. Euro-area inflation consumer expectations for the year ahead rose to

4% from 3.5% in September, the ECB said. The BOE’s Andrew Bailey reiterated it’s too early to start talking about rate cuts, He sees inflation back at its 2% target within two years. Europe is headed for a soft landing, according to the IMF. The Stoxx Europe

600 Index erased early losses to trade slightly higher with autos and retail shares outperforming while utilities underperform. Marks & Spencer Group soared 10% after profit surged and it reinstated a dividend. Bayer said it may separate its consumer-health

or crop-science operations after results missed. Vestas surged 8% after raising its full-year earnings outlook following a flood of turbine orders. Stoxx 600 +0.1%, DAX +0.1%, CAC +0.2%, FTSE 100 is flat. Autos +0.9%, Healthcare +0.8%, Travel and Retail +0.8%.

Utilities -1.4%, Chemicals -0.3%.

Shares in Asia were mixed to lower with the MSCI Asia Pacific Index falling 0.5%, taking its two-day loss to over 2%. Financials the biggest drag. China shares failed to hold on to early

gains but Chinese property developers surged in the afternoon following a report that China has asked Ping An Insurance Group to take a controlling stake in developer Country Garden Holdings. While Ping An denied the report, Country Garden jumped more than

10%. Stocks in Japan and Singapore were among the worst performers in the region. Stocks in Vietnam jumped as investor sentiment got a boost from a weaker US dollar. Singapore -1.4%, Topix -1.2%, Kospi -0.9%, Hang Seng Index -0.6%, CSI 300 -0.25%. Vietnam

+3%, Philippines +0.4%, Taiwan +0.3%, ASX 200 +0.25%, Sensex +0.05%.

FIXED INCOME:

Treasury yields hovered above multi-week lows while waiting on comments from Federal Reserve Chair Jerome Powell. Fed Governor Christopher Waller said on Tuesday

that the economy bears watching after “blowout” third-quarter GDP figures, while the usually hawkish Fed governor Michelle Bowman said she still expects higher rates will be needed. Meanwhile, Fed Governor Lisa Cook said geopolitical tensions could trigger

negative spillovers, including higher inflation. US yields cheaper by 1bp-2bp on the day across front-end and belly of the curve with long-end yields little changed to lower on the day, flattening 2s10s by 1bp, 5s30s by more than 3bp. Treasury auction cycle

resumes with $40b 10-year note sale, following good reception for 3-year note Tuesday. 10 year yield ~4.58%.

METALS:

Gold prices declined for a third day amid diminishing worries about geopolitical tensions in the Middle East. US dollar strength has reduced bullions appeal causing a 2% drop from its

recent high above $2,000 per ounce. Traders are also keeping a close eye on whether the Federal Reserve has finished raising interest rates, which would benefit the non-yielding asset. Spot gold -0.3%, silver -1%.

ENERGY:

Oil extended its slump to a three-month low as a forecast drop in US gasoline consumption added to a growing batch of indicators suggesting the demand outlook is

worsening. Crude oil production in the United States this year will rise by slightly less than previously expected but demand will fall, the EIA said on Tuesday. China, the world’s biggest importer, is also seeing dimming oil demand as winter approaches. Crude

prices have now plunged more than 15% in less than three weeks, dragging US pump prices down to levels not seen since March. US stockpiles jumped by 12 million barrels last week, the API reported. That’d be the biggest rise in about nine months if confirmed

by the EIA. The EIA will delay the release of weekly inventory data until the week of Nov. 13 to complete a planned systems upgrade. WTI -1.5%, Brent -1.4%, US Nat Gas -1.1%, RBOB -0.8%.

CURRENCIES:

The dollar rises for a third day as traders keep their focus on upcoming speeches by Federal Reserve officials. Sterling slips despite BOE Governor Bailey arguing

that it is too early to talk about rate cuts. ECB chief economist Philip Lane said the central bank “shouldn’t take a lot of comfort” from recent decline in euro-area inflation. Hedging costs for one week, which account for inflation data from the US and

the UK, remain low, suggesting stability in major currency ranges. US$ Index +0.2%, GBPUSD -0.3%, USDJPY +0.3%, EURUSD -0.2%, AUDUSD -0.2%, NZDUSD -0.2%.

Bitcoin -0.4%, Ethereum -0.5%.

TECHNICAL LEVELS:

|

ESZ23 |

10 Year Yield |

Dec Gold |

Dec WTI |

Spot $ Index |

|

|

Resistance |

4566.00 |

5.750% |

2056.0 |

86.41 |

108.970 |

|

|

4500/05 |

5.500% |

2029.4 |

85.55 |

107.990 |

|

|

4470.00 |

5.325% |

2019.7 |

83.60 |

107.350 |

|

|

4439.00* |

5.000% |

1998.0 |

80.00 |

106.785 |

|

|

4403.00 |

4.810% |

1983.0 |

78.26 |

105.765 |

|

Settlement |

4396.00 |

1973.5 |

77.37 |

||

|

|

4364.00 |

4.555% |

1964.0 |

76.70 |

104.850 |

|

|

4325.00 |

4.350% |

1948.1 |

75.63* |

104.380 |

|

|

4296.00 |

3.930% |

1921.5 |

74.25 |

103.800 |

|

|

4277.00 |

3.650% |

1898.4 |

73.84 |

103.420 |

|

Support |

4230.00 |

3.265% |

1865.5 |

70.00 |

102.550 |

Colors within the report:

Green is always the 200 period (day, week).

Red is always 21,

Blue = 50,

Brown =

100 *Stars have added importance

- Upgrades

- Datadog (DDOG) Raised to Overweight at JPMorgan

- European Residential REIT (ERE-U CN) Raised to Sector Outperform at Scotiabank; PT C$3.50

- Fidelity National (FIS) Raised to Outperform at Wolfe; PT $65

- Glaukos (GKOS) Raised to Overweight at Wells Fargo; PT $83

- ProQR Therapeutics (PRQR) Raised to Buy at Chardan Capital Markets

- Quanta Services (PWR) Raised to Buy at Goldman; PT $211

- Rexford Industrial (REXR) Raised to Sector Outperform at Scotiabank

- Wish (WISH) Raised to Hold at Loop Capital; PT $4

- Downgrades

- Air Transport (ATSG) Cut to Neutral at Susquehanna; PT $15

- AquaBounty (AQB) Cut to Neutral at HC Wainwright

- Arcutis Biotherapeutics (ARQT) Cut to Hold at JonesTrading

- BRP Group (BRP) Cut to Equal-Weight at Wells Fargo; PT $24

- Credicorp (BAP) Cut to Neutral at Bradesco BBI; PT $140

- Datadog (DDOG) Cut to Neutral at Mizuho Securities; PT $108

- Durect (DRRX) Cut to Neutral at HC Wainwright

- Entergy (ETR) Cut to Sector Perform at RBC; PT $117

- Estee Lauder (EL) Cut to Market Perform at Cowen; PT $120

- First Guaranty Bancshares (FGBI) Cut to Underweight at Piper Sandler

- Imperial Oil (IMO CN) Cut to Neutral at Goldman; PT C$85

- Lucid (LCID) Cut to Neutral at Cantor; PT $6

- Masimo (MASI) Cut to Market Perform at Raymond James

- MasTec (MTZ) Cut to Neutral at Goldman; PT $54

- Nextdoor (KIND) Cut to Inline at Evercore ISI; PT $3

- Nuwellis Inc (NUWE) Cut to Neutral at Ladenburg Thalmann

- NXP Semi (NXPI) Cut to Sell at Citi; PT $150

- Cut to Buy at CFRA

- Spartan Delta Corp (SDE CN) Cut to Sector Perform at ATB Capital; PT C$5

- Tanger (SKT) Cut to Neutral at Compass Point; PT $26

- Zentalis (ZNTL) Cut to Neutral at Wedbush; PT $12

- Initiations

- Applied Opto (AAOI) Rated New Buy at Northeast Securities

- Caribou Biosciences (CRBU) Rated New Neutral at Cantor

- Fair Isaac (FICO) Reinstated Overweight at Wells Fargo; PT $1,120

- Hubbell (HUBB) Rated New Buy at Seaport Global Securities; PT $325

- Marqeta (MQ) Rated New Positive at Susquehanna; PT $9

- Trane Technologies (TT) Reinstated Buy at William O’Neil

Data sources: Bloomberg, Reuters, CQG

No responses yet