TODAY’S GAME PLAN: from the trading

desk, this is not research

DATA/HEADLINES 8:30ET PPI; 2;00ET FOMC Rate Decision

ECB, BOE, SNB policy meetings Thursday – PPI 0.0% MoM, Exp. 0.0%; PPI Core 0.0% MoM, Exp. 0.2%

TODAY’S HIGHLIGHTS:

- ~90 Percent of Moscow’s Pre-War Army Lost to Death or Injury, US Intelligence Estimate Says

- The United Nations passed a resolution calling for a ceasefire in Gaza

- Rates on US 30-year fixed mortgages were down last week to 7.07% from 7.9% in October

- FCC Rejects $900 Million Subsidy For SpaceX Amid Concerns Of Gov’t Weaponization

- U.S Warship Shoots Down Suspected Houthi Drone In Red Sea – ABC

Global stocks are mixed with today’s focus on the conclusion of the Fed’s final policy meeting of the year. Meanwhile, the United Nations passed a resolution calling

for a ceasefire in Gaza and nearly 200 nations reached a historic deal to begin reducing the global consumption of fossil fuels at the COP28 climate summit. In Poland, new Prime Minister Donald Tusk’s government was sworn in, raising hopes of smoother relations

with the rest of the European Union. The Asian Development Bank raised its 2023 growth forecast for developing Asia and China.

EQUITIES:

US equity futures posted small moves in cautious trading as investors looked ahead to the Federal Reserve’s interest-rate decision, bracing for any warnings that

market expectations of policy easing are overdone. The Fed is widely expected to hold, but the latest US inflation data raised doubts about the likelihood of an aggressive pivot toward policy easing. S&P 500 futures edge higher after Tuesday’s cash closed

at the highest level since January 2022 while tracking its longest weekly winning streak in six years.

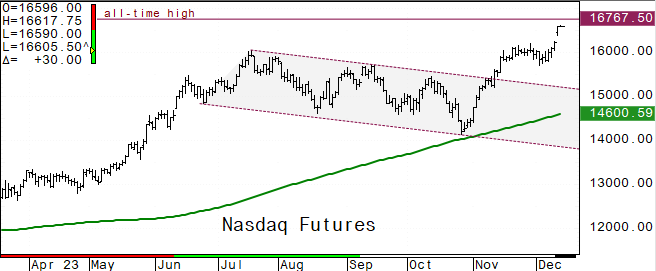

Futures ahead of the bell: E-Mini S&P +0.1%, Nasdaq +0.2%, Russell 2000 -0.05%, Dow +0.1%.

In pre-market trading, Tesla dropped 1.4% after recalling more than 2 million vehicles to fix autopilot safety flaws. Pfizer shares tumbled 8% after the drugmaker forecast revenue for

next year lower than analysts’ projections even after the purchase of a cancer drugmaker that’s producing some of the hottest treatments in the oncology market. Coherent (COHR) falls 2% as Morgan Stanley cuts the semiconductor device company’s stock recommendation

to equal-weight from overweight. Take-Two (TTWO) shares rise 4% as Nasdaq said the Grand Theft Auto VI owner’s stock will be added to the Nasdaq-100 Index, with Seagen set to leave. Xponential Fitness (XPOF) gained over 6% after Stifel upgrades to buy from

hold. Hertz Global Holdings (HTZ) is down 4% after Oppenheimer cut the recommendation to perform from outperform. Vertex Pharmaceuticals (VRTX) rallies 7.5% after the firm announced positive results from a mid-stage study of a non-opioid drug to treat painful

diabetic peripheral neuropathy.

European stocks are on track to hit a February 2022 high once again as chemicals supported gains, after BASF SE and Arkema received upgrades from UBS. Telecoms lagged with Telefonica

SA hit by its exposure to Argentina following the country’s devaluation of its currency. Meanwhile, Britain’s economy shrank more than expected in October, raising the risk of a recession. Gross domestic product fell by 0.3% from September, versus expectations

of no change. The BOE is widely expected to keep its Bank Rate at 5.25% on Thursday. Strategists at Goldman Sachs have adopted an overweight stance on the European stocks while Citigroup’s outlook is also upbeat, with markets being too pessimistic on earnings

growth. Stoxx 600 +0.2%, DAX +0.1%, CAC +0.2%, FTSE 100 +0.3%. Chemicals +1.4%, Healthcare +0.8%. Telecom -1.2%, Retail -0.3%.

Shares in Asia declined, with Chinese equities leading the retreat on disappointment over lack of more stimulus from a key economic leadership meeting. The losses came after China’s annual

economic work conference this week prioritized industrial policy and indicated little desire for large-scale stimulus. MSCI’s Asia Pacific Index dipped 0.3%, with Tencent and Alibaba among the biggest drags. Chinese AI and robot stocks rose after policymakers

vow to put greater emphasis on developing artificial intelligence and Elon Musk introduces Optimus. Country Garden surprised creditors Wednesday night with full yuan bond repayment. China’s CSI 300 -1.7%, Vietnam -1.2%, Thailand -1.2%, Kospi -1%, Hang Seng

Index -0.9%, Philippines -0.6%. Sensex +0.05%, Singapore +0.05%, Taiwan +0.1%, Nikkei 225 +0.25%, ASX 200 +0.3%.

FIXED INCOME:

Treasuries edge higher, with yields richer by 1bp-3bp across the curve at the start of US session that includes Fed rate decision at 2ET and Powell’s press conference

a half hour later. US 10-year yields around 4.18%, richer by 2bp on the day with gilts outperforming. UK 10yr yields were lower by 9bps, to its lowest since May due to weaker UK GDP report. Market positioning appears to be long in the front-end of the US curve,

suggesting that a bear-flattening reaction to today’s Fed communications is the pain trade.

METALS:

Gold was slightly higher as investors anticipated remarks from Federal Reserve Chair Jerome Powell, expected to shed light on the central bank’s interest rate trajectory

for the upcoming year. Spot gold +0.1%, silver -0.5%.

ENERGY:

Oil prices reversed early losses overnight, after falling by more than 3% yesterday to six-month lows on oversupply and demand concerns. OPEC+ left its expectations

for global oil demand unchanged for this year and next and raised its 2023 global economic growth forecast, against a backdrop of falling oil prices the cartel has been unable to halt. The cartel cited China’s economic rebound as a major driver of demand growth

next year together with higher-than-expected growth in the Americas. Meanwhile, weekly average Russian crude exports jumped to the highest since July, compounding oversupply concerns and throwing doubt on the recent output cut agreement by OPEC+. The cost

of shipping through the Red Sea is also rising as the Iran-aligned Houthis in Yemen have stepped up attacks on ships. WTI +0.5%, Brent +0.4%, US Nat Gas +0.8%, RBOB +0.6%.

CURRENCIES:

The dollar inched higher ahead of the Federal Reserve decision, recovering from Tuesday’s decline. Sterling dropped due to weaker UK data, prompting traders to ramp

up bets on Bank of England interest-rate cuts next year. New Zealand dollar led G-10 losses, hitting its lowest since late November, after a set of data triggered cuts in some economists’ inflation forecasts. Elsewhere, Argentina devalued the peso by 54%

after the close of local markets and announced a swath of spending cuts, in the first steps of President Milei’s shock-therapy program to revive the nation’s troubled economy. US$ Index +0.05%, GBPUSD -0.3%, EURUSD -0.05%, USDJPY +0.15%, NZDUSD -0.65%, AUDUSD

-0.1%.

Bitcoin +0.5%, Ethereum +0.6%.

TECHNICAL LEVELS:

|

ESH23 |

10 Year Yield |

Feb Gold |

Jan WTI |

Spot $ Index |

|

|

Resistance |

4782.00 |

5.500% |

2117.0 |

81.00 |

|

|

|

4761.00 |

5.325% |

2089.5 |

79.00 |

107.350 |

|

|

4738.50 |

5.000% |

2051.0 |

77.90 |

106.300 |

|

|

4720.50 |

4.725% |

2027.0 |

76.60 |

105.100 |

|

|

4700.00 |

4.570% |

2006.8 |

72.15 |

104.350 |

|

Settlement |

4697.25 |

1993.2 |

68.61 |

||

|

|

4661/65 |

4.020% |

1986.5 |

66.90 |

103.550 |

|

|

4637/39 |

3.640% |

1973.9 |

65.00 |

102.540* |

|

|

4620.00 |

3.245% |

1963.5 |

63.64 |

101.240 |

|

|

4599.00 |

3.000% |

1960.8* |

61.75 |

100.000 |

|

Support |

4539.00 |

|

1935.5 |

60.00 |

99.580 |

Colors within the report:

Green is always the 200 period (day, week).

Red is always 21,

Blue = 50,

Brown =

100 *Stars have added importance

- Upgrades

- Ally Financial (ALLY) Raised to Equal-Weight at Morgan Stanley; PT $31

- C4 Therapeutics (CCCC) Raised to Buy at Stifel; PT $12

- Capital One (COF) Raised to Equal-Weight at Morgan Stanley; PT $120

- Cogeco Communications (CCA CN) Raised to Buy at Veritas Investment Research Co; PT C$70

- D.R. Horton (DHI) Raised to Outperform at KBW; PT $164

- Gogoro (GGR) Raised to Neutral at JPMorgan; PT $2.20

- Health Catalyst (HCAT) Raised to Overweight at JPMorgan; PT $11

- Incyte (INCY) Raised to Outperform at Leerink; PT $78

- MFA Financial (MFA) Raised to Outperform at KBW; PT $12

- Mohawk Industries (MHK) Raised to Equal-Weight at Barclays; PT $100

- MSCI (MSCI) Raised to Overweight at Morgan Stanley; PT $600

- Opendoor Technologies (OPEN) Raised to Market Perform at KBW; PT $3.50

- Pentair (PNR) Raised to Overweight at KeyBanc; PT $82

- Q2 Holdings (QTWO) Raised to Neutral at Piper Sandler; PT $41

- Radian (RDN) Raised to Outperform at KBW; PT $29

- RxSight (RXST) Raised to Overweight at Wells Fargo; PT $42

- Xponential (XPOF) Raised to Buy at Stifel; PT $18

- Downgrades

- Aveanna Healthcare (AVAH) Cut to Underweight at JPMorgan

- Bread Financial Holdings (BFH) Cut to Underweight at Morgan Stanley

- Church & Dwight (CHD) Cut to Sell at Citi; PT $90

- Coherent Corp (COHR) Cut to Equal-Weight at Morgan Stanley; PT $45

- Evofem Biosciences (EVFM) Cut to Hold at Laidlaw

- Ferrari (RACE) Cut to Hold at HSBC

- Ford (F) Cut to Neutral at BNPP Exane

- Hertz (HTZ) Cut to Perform at Oppenheimer

- Hillman Solutions (HLMN) Cut to Equal-Weight at Barclays; PT $9

- Icosavax (ICVX) Cut to Hold at Jefferies; PT $15.50

- Inspire Medical (INSP) Cut to Equal-Weight at Wells Fargo; PT $187

- Johnson & Johnson (JNJ) Cut to Equal-Weight at Wells Fargo; PT $163

- Johnson Controls (JCI) Cut to Hold at Vertical Research; PT $55

- LyondellBasell (LYB) Cut to Neutral at Citi; PT $98

- Model N (MODN) Cut to Neutral at JPMorgan; PT $25

- Nexpoint Real Estate Finance (NREF) Cut to Market Perform at KBW

- RCM (RCM) Cut to Neutral at JPMorgan; PT $11

- Trex (TREX) Cut to Underweight at Barclays; PT $74

- Visteon (VC) Cut to Neutral at BNPP Exane; PT $130

- Walker & Dunlop (WD) Cut to Market Perform at KBW; PT $105

- Zurn Elkay Water (ZWS) Cut to Sector Weight at KeyBanc

- Initiations

- Acadia Pharma (ACAD) Rated New Buy at Citi; PT $38

- Acelyrin (SLRN) Rated New Equal-Weight at Wells Fargo; PT $11

- Arcturus Therapeutics (ARCT) Rated New Buy at Canaccord; PT $90

- Aris Water Solutions Inc (ARIS) US Rated New Buy at Seaport Global Securities; PT $15

- Arrowroot Acquisition (ARRW) Rated New Buy at Benchmark; PT $18

- Axsome Therapeutics (AXSM) Rated New Buy at Citi; PT $125

- Bruker Corp (BRKR) Rated New Outperform at Wolfe

- Camping World (CWH) Rated New Buy at Roth MKM; PT $30

- Cava Group (CAVA) Rated New Outperform at Cowen; PT $46

- Danaher (DHR) Reinstated Peerperform at Wolfe

- Denali Therapeutics (DNLI) Rated New Buy at Citi; PT $32

- DoubleVerify (DV) Rated New Overweight at Morgan Stanley; PT $40

- HilleVax (HLVX) Rated New Buy at HC Wainwright; PT $28

- Impinj (PI) Rated New Positive at Susquehanna; PT $100

- Ironwood (IRWD) Rated New Buy at Intron Health; PT $18

- Karuna Therapeutics (KRTX) Reinstated Buy at Citi; PT $291

- Microsoft (MSFT) Rated New Buy at Truist Secs; PT $600

- Neurocrine Bio (NBIX) Reinstated Buy at William O’Neil

- Rated New Neutral at Citi; PT $127

- ON Semi (ON) Rated New Buy at President Capital Management; PT $95

- Opera (OPRA) ADRs Rated New Buy at Goldman; PT $16.50

- Roblox (RBLX) Rated New Overweight at Wells Fargo; PT $49

- Sarepta (SRPT) Reinstated Buy at Citi; PT $113

- Standex (SXI) Rated New Buy at DA Davidson; PT $165

- Veralto (VLTO) Rated New Peerperform at Wolfe

- Vizio Holding (VZIO) Rated New Buy at B Riley; PT $11

- Xylem (XYL) Rated New Outperform at Wolfe; PT $127

Data sources: Bloomberg, Reuters, CQG

No responses yet