TODAY’S GAME PLAN: from the trading

desk, this is not research

DATA/HEADLINES 8:30ET Weekly Jobless Claims, Advance Good Trade Balance, Wholesale Inventories; 10:00ET Pending

Home Sales; 1:00ET 7 Year Note Auction

TODAY’S HIGHLIGHTS and News:

-

The world’s debt market is set to post its biggest two-month gain on record

-

Apple resumed US store sales of its latest smartwatches after winning a court reprieve in patent fight

-

The US proposed that G-7 groups explore ways to seize $300 billion in frozen Russian assets

-

Even as EV sales increased, the global oil industry sold more gasoline than ever this year

World shares are higher as consensus builds that rates in developed countries are heading lower next year. The MSCI ACWI Index of global equities is on pace for

its highest close since February 2022, up more than 15% from its October low. The world’s debt market is on track to post its biggest two-month gain on record as traders ramp up expectations that global central banks will have to aggressively cut interest

rates next year to bolster growth. Swaps traders are pricing about 150 basis points of rate cuts in the US and UK next year, and almost 175bps in the euro zone. North Korea leader Kim Jong Un has ordered his country’s military, munitions industry and nuclear

weapons sector to accelerate war preparations to counter what he called unprecedented confrontational moves by the US, state media said.

EQUITIES:

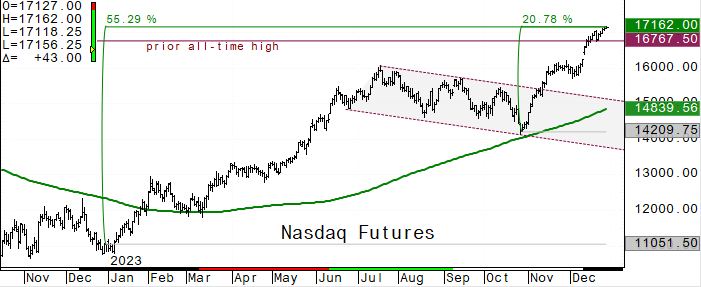

US equity futures are mixed with tech companies outperforming the broader market and heading for their best year in almost a quarter century. Nasdaq 100 index futures edged higher, with

the tech-heavy gauge on track for its best year since the 1999 dotcom bubble burst. With the year winding down, most S&P sectors are staring at big yearly gains, led by semiconductors +61% and tech +55%.

Futures ahead of the bell: E-Mini S&P +0.02%, Nasdaq +0.25%, Russell 2000 -0.3%, Dow -0.1%.

In pre-market trading, Altice USA (ATUS) gains ~9%, adding to Wednesday’s rally that was spurred by a report billionaire Xavier Niel has interest in buying Altice Portugal. CytoSorbents

(CTSO) falls 26% after a trial of its medical device missed the primary effectiveness goal. Microsoft (MSFT) shares are up 0.3% after Wedbush raised its price target on the software company to $450, maintaining an outperform rating.

European stocks fluctuated, hovering around their highest level since January 2022. The Stoxx Europe 600 index was slightly lower after erasing an early advance in thin holiday trading,

with trading volumes 54% below the 30-day average. Health care and food & beverage sectors led gains, while energy and telecoms stocks lagged. The benchmark is set to end 2023 up about 13% after a two-month rally that’s been fueled by slowing inflation, economies

avoiding major contractions and hopes for central-bank pivots. Stoxx 600 -0.15%, DAX -0.2%, CAC -0.4%, FTSE 100 is flat. Healthcare +0.3%, Food & Bev +0.2%. Energy, banks and telecom are down ~0.5%.

Asian stocks advanced for a fourth day, led by a rally in Chinese shares, boosted by a rotation into some of 2023’s worst-performing sectors. The MSCI Asia Pacific Index rose 1.2% as

Australian and Indonesian stocks climbed toward all-time highs. Chinese benchmarks led regional gains, with the CSI 300 Index extending a rebound from last week, even as investors remain concerned about the nation’s weak economy. Shares in Japan bucked the

trend and fell as a stronger yen and ex-dividend payouts weighed. Hang Seng Tech +3.4%, Hang Seng Index +2.5%, CSI 300 +2.3%, Kospi +1.6%, Singapore +1.4%, Philippines +0.9%, ASX 200 +0.7%, Sensex +0.5%. Nikkei 225 -0.4%, Topix -0.1%.

FIXED INCOME:

Treasuries are under mild pressure in early US trading, surrendering a portion of Wednesday’s gains that sent benchmark yields to new multi-month lows after a well-bid

5-year auction. Yields are higher by 1bp-2bp across the curve; 2s10s wider by 0.5bps. Supply cycle concludes with $40b 7-year auction at 1pm EST, poised to draw a yield more than 55bps lower than last month’s. Investors are betting on an 88% chance of a rate

cut as early as March, according to the CME FedWatch tool, a huge swing from a month ago when the probability was just 21%. 10 year yield 3.815%, 2 year yield 4.25%.

METALS:

Gold prices steadied after hitting a more than three-week peak. Investors await the US initial jobless claims data for further cues on Fed monetary policy. On the

physical front, China’s net gold imports via Hong Kong rose about 37% in November from the previous month, data showed. Spot gold -0.1%, silver +0.2%.

ENERGY:

Oil retreated on signs the US stockpile keeps building amid thin holiday volumes. WTI slipped briefly below $73 a barrel after declining by 1.9% on Wednesday as concerns

eased about shipping disruptions along the Red Sea route. Danish shipping company Maersk said it has scheduled several dozen container vessels to travel via the Suez Canal and Red Sea in the coming weeks. However, a US-led coalition to quell tensions in the

Red Sea has not so far yielded coordinated action as hoped. Israeli forces pummeled central Gaza by land, sea and air on Wednesday, a day after Israel’s chief of staff told reporters the war would go on “for many months”. The American Petroleum Institute reported

nationwide inventories rose by 1.8 million barrels. Official prints on US reserves, as well as gauges of output and demand, are due later today from the Energy Information Administration. Even as EV sales increased, the global oil industry sold more gasoline

than ever this year. WTI -1.1%, Brent -1%, US Nat Gas +2%, RBOB -0.7%.

CURRENCIES:

In currency markets, the dollar hit a new five-month low as markets continued to price in expectations for the Federal Reserve to cut rates next year. The Swiss franc

strengthened against the dollar for a sixth day, extending the rally that has taken it to the strongest point since January 2015. The yen got a boost from expectations that the Bank of Japan will raise interest rates for the first time since 2007, with Governor

Ueda further building the case for a move in the spring. “It’s possible to make some decisions even if the bank doesn’t have the full results of spring wage negotiations from small- and middle-sized businesses,” the governor said.

US$ Index -0.2%, GBPUSD -0.25%, EURUSD +0.05%, USDJPY -0.7%, AUDUSD -0.1%, UNDNOK +0.3%, USDCHF -0.8%.

Bitcoin -1.5%, Ethereum +0.6%.

TECHNICAL LEVELS:

|

ESH24 |

10 Year Yield |

Feb Gold |

Feb WTI |

Spot $ Index |

|

|

Resistance |

4950.00 |

5.000% |

2200.0 |

81.37 |

107.350 |

|

|

4925.00 |

4.600% |

2180.0 |

77.71 |

106.280 |

|

|

4900.00 |

4.500% |

2152.3 |

77.04 |

105.000 |

|

|

4873.00 |

4.340% |

2117.0 |

76.25 |

104.350 |

|

|

4851.00 |

4.020% |

2100.0 |

75.71 |

103.400 |

|

Settlement |

4833.50 |

2093.1 |

74.11 |

||

|

|

4804.00 |

3.840% |

2026.7 |

73.05 |

101.240 |

|

|

4781.00 |

3.640% |

2012.8 |

72.08 |

100.000 |

|

|

4746.00 |

3.245% |

2008.6 |

71.11 |

99.580 |

|

|

4717.00 |

3.000% |

1973.5 |

69.73 |

98.940 |

|

Support |

4688.00 |

2.700% |

1960.8* |

67.98 |

98.000 |

Colors within the report:

Green is always the 200 period (day, week).

Red is always 21,

Blue = 50,

Brown =

100 *Stars have added importance

- Downgrades

- Karuna Therapeutics (KRTX) Cut to Neutral at JPMorgan; PT $330

- RayzeBio (RYZB) Cut to Neutral at JPMorgan; PT $62.50

- Cut to Hold at Truist Secs; PT $62.50

- Initiations

- AIG (AIG) Rated New Buy at HSBC; PT $86

- Allstate (ALL) Rated New Hold at HSBC; PT $145

- Canadian Solar (CSIQ) Rated New Overweight at Guotai Junan Sec

- Chubb (CB) Rated New Buy at HSBC; PT $263

- LanzaTech Global (LNZA) Rated New Buy at Janney Montgomery; PT $10

- LM Funding America (LMFA) Rated New Neutral at HC Wainwright

- Progressive (PGR) Rated New Hold at HSBC; PT $164

- Sato Technologies Corp (SATO CN) Rated New Neutral at HC Wainwright

- Sphere 3D (ANY) Rated New Buy at HC Wainwright; PT $5

- Spotify (SPOT) Rated New Outperform at CICC; PT $210

- Travelers (TRV) Rated New Hold at HSBC; PT $203

Data sources: Bloomberg, Reuters, CQG

Comments are closed