TODAY’S GAME PLAN:

from the trading desk, this is not research

DATA/HEADLINES 9:45ET S&P Global US Manufacturing PMI; 10:00ET Construction Spending

Happy 2024–the year of dragon represents authority, prosperity, and good fortune

TODAY’S HIGHLIGHTS and News:

- California’s population declined by 573k (rounded), Illinois’ by 264k, New York’s by 631k – census

- Drugmakers set to raise US prices on at least 500 drugs in January

- Passengers and crew escape a devastating fire on Japan Airlines plane after collision at Tokyo airport

- DoorDash plans to diversify beyond food delivery

- Iran said it’s open to fresh talks around its nuclear program

- $842 million Powerball jackpot was won by someone in Michigan, the first time that’s happened on New Year’s Day since the game’s start

World shares opened the year on cautious footing amid rising tension in the Red Sea and weak Chinese data that weighed on Asian shares. A slew of factory purchasing

managers’ indexes published around the world today showed a persistent slowdown and suggested any turnaround this year would take time. Switzerland, Japan and NZ remained closed. Japan markets are yet to trade after an earthquake and tsunami on January 1st.

Iran dispatched a warship to the Red Sea after the US Navy destroyed three Houthi boats after an attack on a Maersk container vessel. Maersk suspended all transit through the route.

EQUITIES:

US equity futures dropped as investors weighed bets on monetary easing against elevated valuations, mounting tension in the Middle East and weak Chinese data. Futures on the tech-heavy

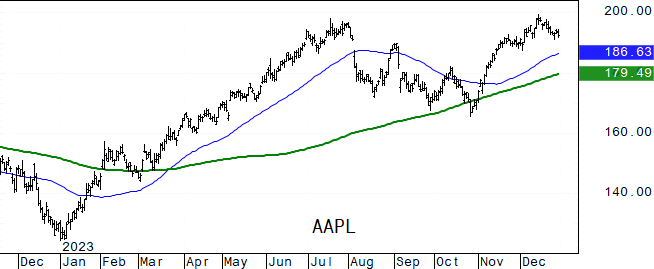

Nasdaq index lead losses as shares of Apple fell in US pre-market trading after a downgrade by Barclays. Market attention is now focused on economic data due later in the week, including the US non-farm payrolls report on Friday which could provide clues

as to the Federal Reserve’s next move. This week also includes ISM manufacturing, JOLTS. FOMC minutes, ADP employment change, factory orders and ISM services index.

Futures ahead of the bell: E-Mini S&P -0.85%, Nasdaq -1.2%, Russell 2000 -0.9%, Dow -0.7%.

In pre-market trading, Apple (AAPL) shares fall 1.6% after Barclays cuts its rating to underweight from equal-weight, citing that channel checks show weakness in iPhone volumes. Unity

Software (U) drops 3.3% after Piper Sandler downgrades the graphic-tools provider to underweight from neutral. Chinese electric-vehicle makers listed in the US drop after China’s BYD posted a record sales quarter thanks to aggressive discounting amid an industry

price war, stoking worries over rising competition. Li Auto (LI) -4.3%, Nio (NIO) -1.1%, XPeng (XPEV) -1%. Cryptocurrency-linked stocks rally as Bitcoin rises past the $45,000 mark to touch its highest level since April 2022. TeraWulf (WULF) +19%, Cleanspark

(CLSK) +13%, Marathon Digital (MARA) +13%%, Riot Platforms (RIOT) +10%, Coinbase Global (COIN) +5.4%.

European indices reversed early gains although Euro zone bank stocks held onto gains after rising to their highest since 2018. The Stoxx Europe 600 erased gains of as much as 0.7% to

trade lower as technology and consumer products stocks lead losses. Among individual movers, AP Moller-Maersk A/S rose after halting transit through the Red Sea following an attack on one of its ships by Houthi rebels. ASML Holding NV fell after Bloomberg

reported it canceled shipments of some of its machines to China. Eurozone inflation figures due later this week will provide clues about monetary policy. Signs of economic woes were underscored by a survey showing euro zone factories ended 2023 on the back

foot, with activity contracting in December for the 18th straight month. Stoxx 600 -0.5%, DAX -0.5%, CAC -0.7%, FTSE 100 -0.5%. Banks +0.8%, Telecom +0.7%, Energy +0.5%. Technology -1.5%, Chemicals and Retail -1.1%.

Asian equities were mixed after key markets returned from the New Year holiday, while sentiment soured after weak economic data from China. China’s Manufacturing PMI came in at 49 versus

49.6 estimate and business confidence for 2024 remained subdued, a survey showed. Chinese chipmakers dropped as ASML canceled some shipments to China following a request from the Biden administration. Across Asia, PMI data largely signaled a slowdown in

new orders and production volumes. Input costs also rose and supply chain performance worsened. South Korea’s Kospi Index closed at its highest level in 19 months amid foreign investor demand for chipmakers. Stocks also rose in Australia, driven by gains

in banking and minerals shares. Hang Seng Index -1.5%, CSI 300 -1.3%, Sensex -0.5%, Taiwan -0.4%, Singapore -0.3%. Vietnam +0.2%, ASX 200 +0.5%, Kospi +0.5%, Thailand +1.25%, Philippines +1.6%.

FIXED INCOME:

US Treasury yields climb 5bp to 7bp across the curve with futures near lows of the day heading into early US session, following wider bear steepening move seen in

gilts where UK long-end yields are cheaper by up to 13bp on the day. Yields on 10-year US bonds and German bunds added more than five basis points as money markets wagered on fewer than 150 basis points of easing by the Federal Reserve in 2024. The prospect

of heavy new issuance is also likely weighing on bonds, particularly after their strong performance ahead of year-end. 10-year yields rise to around 3.95%, 2-year yield ~4.32%. Treasury supply resumes next week with 3, 10 and 30-year auctions.

METALS:

Gold rose, after notching up its first annual gain in three years as investors increased bets that the Federal Reserve will start to cut interest rates in the months

ahead. Bullion ended 2023 up 13%. Traders will look to US data releases later this week, including employment figures, that may influence the Fed’s monetary policy stance. Spot gold +0.2%, silver +0.4%.

ENERGY:

Oil prices jumped due to an escalation in tensions in the Red Sea as well as hopes for strong demand from China, where investors are expecting fresh stimulus measures.

Brent crude surged more than 2% after Iran dispatched a warship in response to the US Navy’s sinking of three Houthi boats over the weekend. The head of energy firm E.ON (EONGn.DE) said that instability in the Middle East could send energy prices soaring.

WTI +2%, Brent +1.8%, US Nat Gas +5.7%, RBOB +2.2%.

CURRENCIES:

In currency markets, the yen weakened in thin trading as investors monitored conditions after an earthquake in Japan on Monday. At least 48 people were killed after

a powerful earthquake hit Japan’s northwest coast. The dollar strengthened for the third consecutive session after data showed China’s factory activity shrank in December to the lowest level in six months. The euro dipped due to data showing prolonged contraction

in euro-area manufacturing. US$ Index +0.8%, GBPUSD -0.7%, EURUSD -0.8%, USDJPY +0.8%, AUDUSD -0.4%, USDCAD +0.5%, NZDUSD -0.9%, USDCHF +1%.

Bitcoin %, Ethereum %. Bitcoin jumped above $45,000 for the first time since April 2022, buoyed by optimism around the possible approval of exchange-traded spot

bitcoin funds. There have been increasing signs regulators are prepared to sign off on at least some of the 13 proposed spot bitcoin ETFs, with expectations the decision will likely come in early January.

TECHNICAL LEVELS:

|

ESH24 |

10 Year Yield |

Feb Gold |

Feb WTI |

Spot $ Index |

|

|

Resistance |

4925.00 |

5.000% |

2200.0 |

81.37 |

107.350 |

|

|

4900.00 |

4.600% |

2180.0 |

78.15 |

106.600 |

|

|

4873.00 |

4.500% |

2152.3 |

77.71 |

104.780 |

|

|

4841.50 |

4.340% |

2117.0 |

76.40 |

104.000 |

|

|

4824.50 |

4.025% |

2100.0 |

72.23 |

103.400 |

|

Settlement |

4820.00 |

2071.8 |

71.65 |

||

|

|

4803.00 |

3.840% |

2063.0 |

72.12 |

100.550 |

|

|

4780.00 |

3.640% |

2026.7 |

69.73 |

100.000 |

|

|

4746.00 |

3.245% |

2016.6 |

67.98 |

99.580 |

|

|

4717.00 |

3.000% |

1987.9 |

66.25 |

98.940 |

|

Support |

4688.00 |

2.700% |

1975.2 |

65.00 |

98.000 |

Colors within the report:

Green is always the 200 period (day, week).

Red is always 21,

Blue = 50,

Brown =

100 *Stars have added importance

- Upgrades

- Acadia Realty (AKR) Raised to Buy at Jefferies; PT $20

- Alpha & Omega Semi (AOSL) Raised to Buy at B Riley; PT $34

- American Homes (AMH) Raised to Buy at Jefferies; PT $41

- Booking (BKNG) Raised to Equal-Weight at Wells Fargo; PT $3,459

- Boston Properties (BXP) Raised to Buy at Jefferies; PT $80

- Centene (CNC) Raised to Overweight at Wells Fargo; PT $90

- CubeSmart (CUBE) Raised to Buy at Jefferies; PT $53

- Douglas Emmett (DEI) Raised to Hold at Jefferies; PT $15

- Equinix (EQIX) Raised to Peerperform at Wolfe

- Essex Property (ESS) Raised to Buy at Jefferies; PT $281

- Evergy (EVRG) Raised to Overweight at Barclays; PT $56

- Exact Sciences (EXAS) Raised to Buy at Benchmark; PT $91

- Expedia (EXPE) Raised to Equal-Weight at Wells Fargo; PT $159

- Hilton Grand Vacations (HGV) Raised to Buy at Jefferies; PT $50

- Hudson Pacific (HPP) Raised to Buy at Jefferies; PT $12

- Huntington Bancshares (HBAN) Raised to Equal-Weight at Barclays; PT $15

- Invitation Homes (INVH) Raised to Buy at Jefferies; PT $41

- Ionis Pharma (IONS) Raised to Buy at BofA; PT $62

- Moderna (MRNA) Raised to Outperform at Oppenheimer; PT $142

- nCino (NCNO) Raised to Overweight at Piper Sandler

- Netstreit (NTST) Raised to Outperform at Wolfe; PT $22

- Park Hotels (PK) Raised to Buy at Jefferies; PT $21

- Sprout Social (SPT) Raised to Overweight at Cantor; PT $74

- Thoughtworks (TWKS) Raised to Outperform at Baird; PT $6

- Travel + Leisure Co (TNL) Travel + Leisure Co Raised to Buy at Jefferies; PT $57

- Universal Health (UHS) Raised to Overweight at Wells Fargo; PT $177

- Weave (WEAV) Raised to Overweight at Piper Sandler

- Downgrades

- Alliant Energy (LNT) Cut to Equal-Weight at Barclays; PT $53

- Apple (AAPL) Cut to Underweight at Barclays; PT $160

- AvalonBay (AVB) Cut to Peerperform at Wolfe

- AvidXchange (AVDX) Cut to Neutral at Piper Sandler

- Birchcliff Energy (BIR CN) Cut to Sector Perform at ATB Capital; PT C$8

- BlackLine Inc (BL) Cut to Underweight at Piper Sandler

- Brunswick (BC) Cut to Neutral at B Riley; PT $106

- Choice Hotels (CHH) Cut to Underperform at Jefferies; PT $96

- Citizens Financial (CFG) Cut to Equal-Weight at Barclays; PT $40

- Estee Lauder (EL) Cut to Hold at Deutsche Bank; PT $146

- Hasbro (HAS) Cut to Neutral at DA Davidson; PT $53

- Helmerich & Payne (HP) Cut to Neutral at Seaport Global Securities

- Icosavax (ICVX) Cut to Neutral at Guggenheim

- Inspire Medical (INSP) Cut to Hold at Stifel; PT $210

- Jackson Financial (JXN) Cut to Hold at Jefferies; PT $55

- Mid-America (MAA) Cut to Hold at Jefferies; PT $136

- ProFrac Holding (ACDC) Cut to Neutral at Seaport Global Securities

- Regions Financial (RF) Cut to Underweight at Barclays; PT $22

- Ryanair (RYA ID) ADRs Cut to Inline at Evercore ISI; PT $140

- Simply Good Foods (SMPL) Cut to Hold at Deutsche Bank; PT $42

- Southwest Air (LUV) Cut to Inline at Evercore ISI; PT $35

- Unity Software (U) Cut to Underweight at Piper Sandler

- Initiations

- Nike (NKE) Rated New Outperform at Haitong Intl; PT $118.70

- Rollins (ROL) Rated New Buy at Goldman; PT $49

Data sources: Bloomberg, Reuters, CQG

Comments are closed