This post goes out as an email to our subscribers every day and is posted for free here around 2 PM ET. To get your real-time copy, sign up for the free or premium version here: Opening Print Subscribe.

Day One Of The Fed’s Two-Day Meeting

Follow @MrTopStep on Twitter and please share if you find our work valuable!

Our View

S&P 500 Daily Moves Greater Than ± 2% Since Trump’s Election Victory (Nov 6, 2024-Dec 8, 2025)

I asked Grok to make a list of the jump in volatility since Trump took office in his second term, and it’s my guess that this list will get bigger and bigger.

One of my best calls since Trump took office was that there would be increased volatility, and that it would continue right into the end of his term.

Since Donald Trump’s second term began, U.S. stock market volatility has increased compared to the Biden years. The $VIX has repeatedly spiked above 30, peaking near 55 in early April, driven by aggressive tariff announcements, trade wars, and policy uncertainty.

While the S&P 500 is still up around 16.81%, and the Nasdaq is up 22.10% year-to-date as of December 8, I’ve seen a lot of years with sell-offs late in the year — but this year has been far bumpier, with multiple sharp sell-offs and a six-fold increase in 2%+ daily drops versus 2023–2024.

Trump’s policies have brought back the higher volatility environment seen in his first term.

Our Lean

The PitBull said it again last night — that after December 15th (or mid-month) is when the markets typically start the year-end rally. But we still have this week to get through.

I had a feeling there could be some selling going into Tuesday’s Fed rate decision, and we could see more of that today.

The yield on the 10-year note has increased from a November low of 3.97% to 4.14% on December 5. Bond futures (ZBH26) made a high at 117.31 on 11/25 and a low at 114.27 yesterday, and have been down in 5 of the last 7 sessions, with one of the up days only gaining 4 ticks. Not exactly a ringing endorsement for further rate cuts — despite the market leaning toward 2 to 3 more cuts in 2026.

Our lean: If the Fed turns hawkish, we could see a 1% to 2% drop. If the Fed is dovish, the ES will likely go back to 6900 or higher — fast.

I don’t think the rally is over, but yesterday’s price action before the $NVDA news was weak. I expect another very volatile session, which I think could see some further weakness.

@HandelStats Study: Day 1 of the Fed’s Two-Day Meeting

December 9th Market Performance: 1980–Present

A study of S&P 500 daily performance since 1980 shows that December 9th has been a slightly bearish day overall.

Historical Stats (1980–2024):

-

Total occurrences: 33

-

Up days: 15

-

Down days: 18

-

Up probability: 45.45%

-

Down probability: 54.55%

While the edge is modest, the day has leaned slightly negative over the past four decades.

A Stronger Signal: When December 9th Falls on a Tuesday

The most striking pattern emerges when we isolate only those years in which December 9th landed on a Tuesday.

Across all such occurrences since 1980:

-

Up days: 0

-

Down days: 100%

In other words:

Every single December 9th that fell on a Tuesday was a down day.

That’s a small sample, but a perfect historical streak is worth noting, especially when combined with broader seasonal tendencies.

FOMC preview – Published Dec. 5

At the conclusion of next week’s FOMC meeting, we expect that the Committee

will lower the target range for the fed funds rate by 25bp to 3.50-3.75%. We look

for at least two dissents in favor of no action and one in favor of a larger cut. The

interest rate forecast “dots” will also reflect unease about cutting, as we expect only

a slim majority of the nineteen Committee participants will have penciled in next

week’s cut as an appropriate action. As was the case in September, we think the

median participant will pencil in one more cut in each of the next two years.

Likewise, we don’t see reason to look for large changes to the economic forecasts.

We look for the forward guidance in the statement to reference “the extent and

timing” of additional adjustments, a subtle shift to indicate a cut is less likely at

subsequent meetings. At the press conference, we expect that Powell will stress

that with policy rates close to neutral, the time for risk management cuts is past and

that further cuts would only come with a material deterioration in the labor market.

With markets only pricing in a roughly one-in-three chance of a cut at the January

meeting, Powell will not have to use the same trenchant language used in October

to push back against market expectations.

Next week there are almost equally compelling reasons to cut and to hold. In such

instances, it comes down to vote counting. Most governors appear to favor cutting,

and most reserve bank presidents appear to favor holding. The most decisive news

to tilt the balance was NY Fed President Williams’ remarks two weeks ago that

there is room for another cut “in the near term.” We believe he was speaking for

the rest of the leadership (Powell and Jefferson), and this should weigh the votes

firmly toward a cut. We expect Musalem will join Schmid in dissenting against in

favor of holding. If they had their druthers, we think Collins and Goolsbee would

not cut next week either, though we guess they aren’t so firmly opposed as to cast

a dissent. Miran seems likely to dissent again for a 50bp cut.

Given that next week’s move is a close call, there is a widely held view that it will

be a “hawkish cut.” We generally agree with this view. One way this could be

conveyed would be for the statement to mimic last year’s forward guidance. Last

November’s statement referenced “In considering additional adjustments…”

which was followed by a cut in December. The December statement referenced “In

considering the extent and timing of additional adjustments…” which was

followed by a pause at the January ’25 meeting. By mirroring that change in

language, the Committee could hint at a pause in the coming January meeting. We

don’t see any other material changes in the statement language. At the press

conference, we think Powell will characterize policy as close to neutral. We don’t

expect him to comment directly on January, but instead to highlight that there is a

lot of data to be released between now and the January meeting and that will guide

their decision.

For the economic projections, we think the GDP projections for this year will be

revised up two tenths to 1.8%, and the core PCE will be revised down three tenths

to 2.8%, with no change in the unemployment rate projection. We don’t look for

major changes to GDP or unemployment in the out years, while core PCE could

be revised down a tick or two. In the dots for this year, we see at least seven and

potentially nine participants penciling in no cut for next week’s meeting.

Looking further afield, with little change in the economic outlook, we see the median dot continuing to point to one cut in ’26 followed by a final cut in ’27. We think we could see the median longer run dot move up from 3.0% to 3.125% (though admittedly we expected that in September whereas they left it unchanged).

We’re not looking for significant balance sheet announcements. If the desk needs to conduct open market operations around year-end, the implementation note from the recent meetings is flexible enough to permit policy to respond to market developments.

Guest Post: Tom Incorvia – Blue Tree Strategies

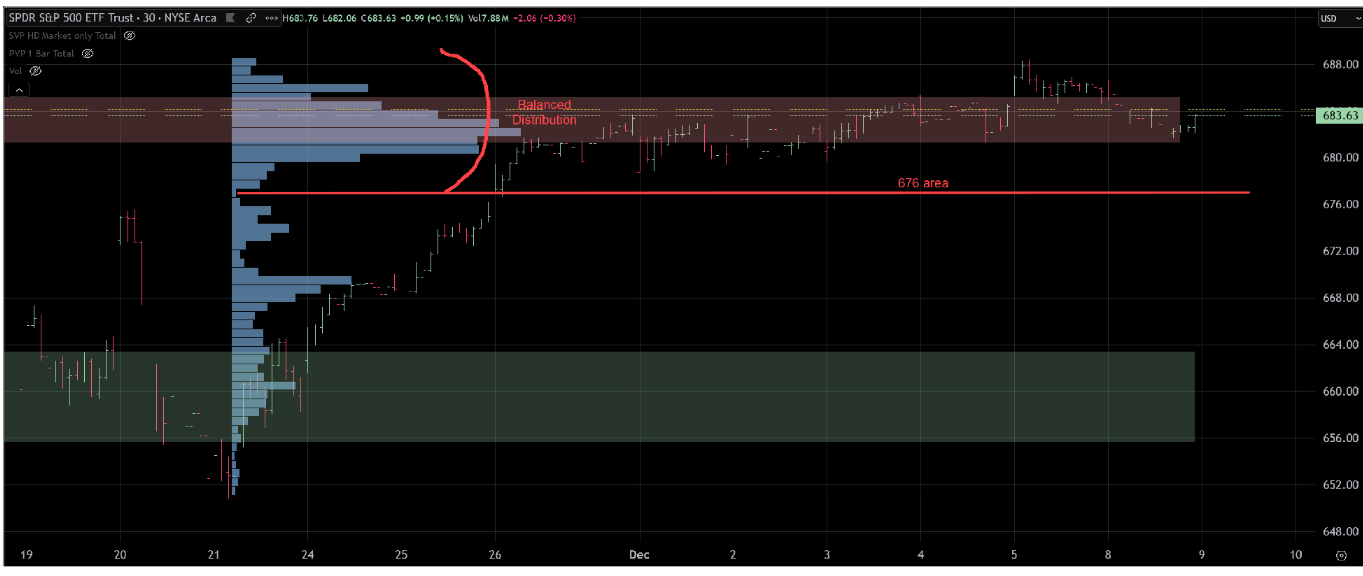

Since November 26, the SPY has remained in a narrow consolidation band, with price action showing limited directional conviction. Such tight ranges typically reflect market indecision regarding the next potential swing move. From an analytical standpoint, a decisive break outside this consolidation zone is needed to establish directional clarity. Until then, market participants face a choice between exercising patience or applying short-duration, mean-reversion strategies within the range.

Friday’s session briefly improved the outlook, with trading sustained above the long-term balance area. However, Monday’s subsequent rejection of those higher levels diminished that constructive signal. The low-volume area near 676 remains a critical reference point. Maintaining trade above this zone would preserve the current balance structure, while a breakdown below it would increase the probability of a move toward the 660 region.

Tom Incorvia began his career in financial services in 1987 and has amassed over three decades of experience navigating the complexities of the markets. His career spans both the buy-side and sell-side of the trading desks, having served as Vice President of Equity Trading and later as General Partner of a hedge fund. This dual perspective has provided him with a unique and well-rounded understanding of market behavior.

You can purchase Tom’s Course on Volume Profile here.

Market Recap

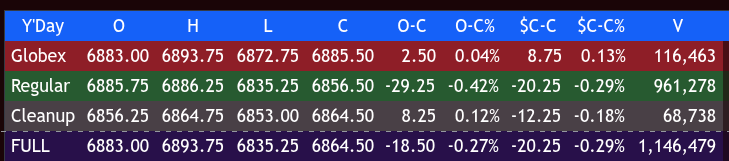

In true fashion, the ES rallied up to 6893.75 on Globex and opened Monday — day one of the Fed’s two-day meeting — at 6885.75, up 9 points or +0.13%.

After the open, the ES rallied up to 6993.25 and then reversed as the NQ tumbled. After some flatline price action above the VWAP, it started getting hit by sell programs, pushing the ES down to 6848.50 at 11:00. It then rallied up to 6860.75 before dropping to a new low at 6841.00 at 12:25.

The ES popped up to 6863.75 at 1:00, sold off down to a new low at 6835.25 at 2:55, traded up to 6847.75 at 2:50, then down to 6840.00 at 3:35. It traded 6845.00 as the 3:50 cash imbalance showed $1.2 billion to buy, shot up to 6867.00, and settled at 6864.50, down 20.25 points or -0.29% from the previous close.

The NQ settled at 25,664.00, down 68 points or -0.26% on the day.

While much of the tech sector got pounded early, most of the losses were erased after a report that the Trump administration was going to give $NVDA the green light to sell the H200 chips to China. The late MiM buy imbalance also caught the shorts off guard.

In the end, it was a pre-Fed spook job.

In terms of the ES’s overall tone, the brunt of the selling was on the tech and AI side until after the 3:50 cash imbalance. In terms of the ES’s overall trade, volume was on the low side at 1.17 million contracts traded.

MiM

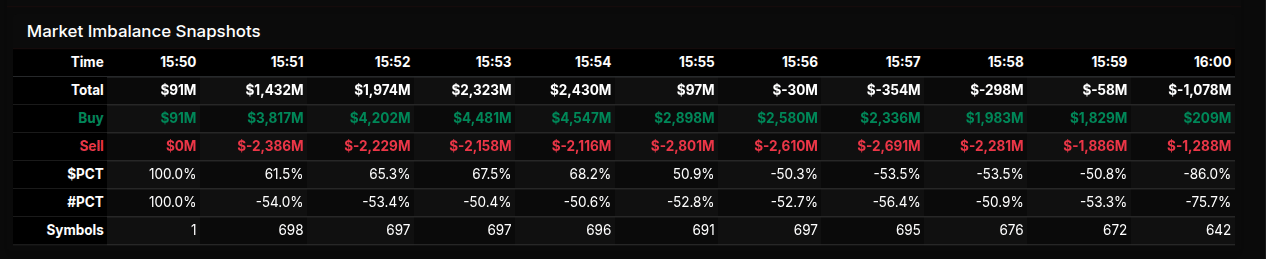

Market-on-Close Recap – MiM

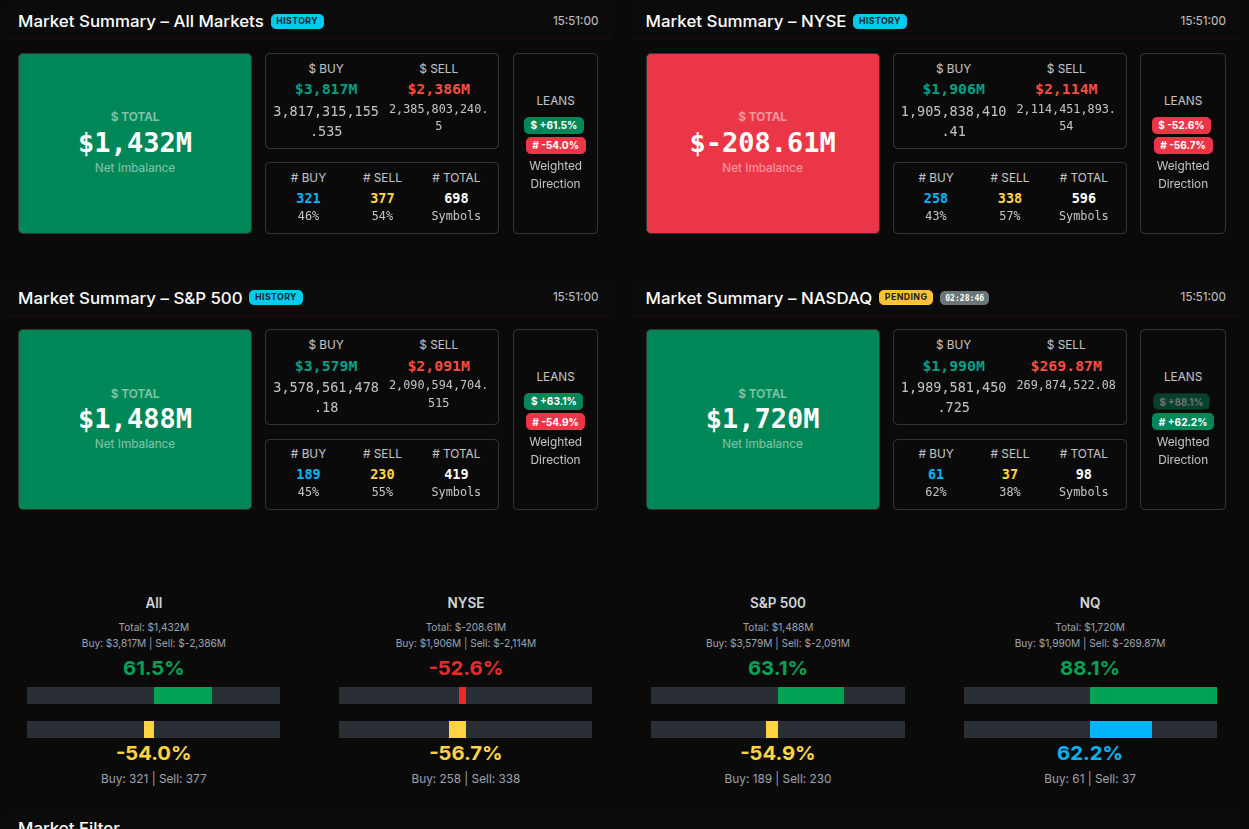

The MOC auction opened at 15:51 with a strong $1.43B buy imbalance, driven largely by tech, communication services, and consumer cyclicals. The early surge showed a 61.5% positive dollar lean, but the symbol lean ran -54%, signaling that while dollars were concentrated in fewer, larger names, most symbols were actually skewed to the sell side — a classic sign of rotation underneath a headline buy imbalance.

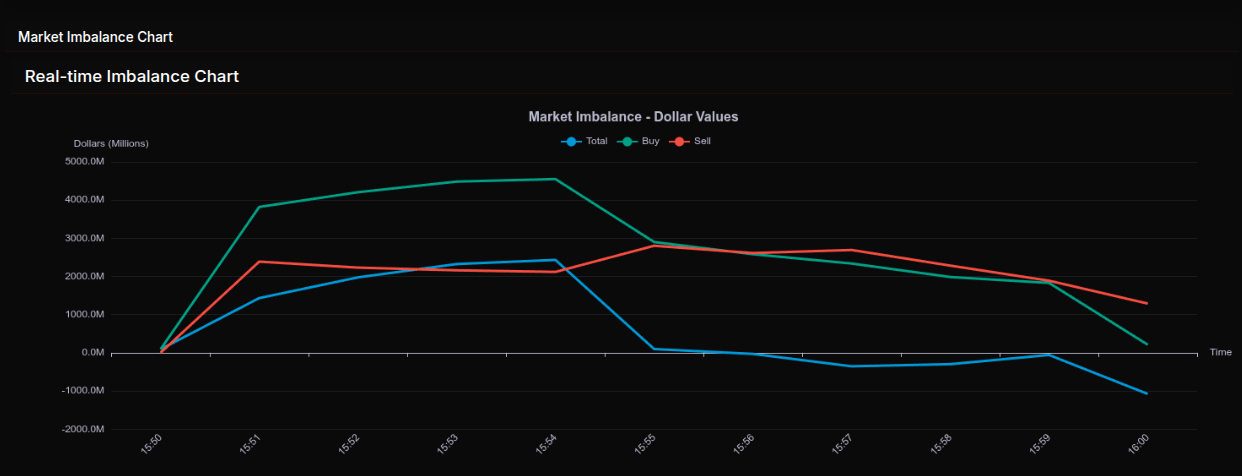

From 15:51 to 15:54, buy pressure climbed steadily, peaking near $4.5B, while sell flows held between $2.1B–$2.3B, keeping the net imbalance solidly positive. But by 15:55 the auction tone shifted. The net collapsed to just $97M, and by 15:56 the imbalance flipped negative (-$30M) as sell pressure widened. This transition continued: at 15:57 the net hit -$354M, and into the final print it deteriorated to -$1.07B, ending the auction decisively on the sell side.

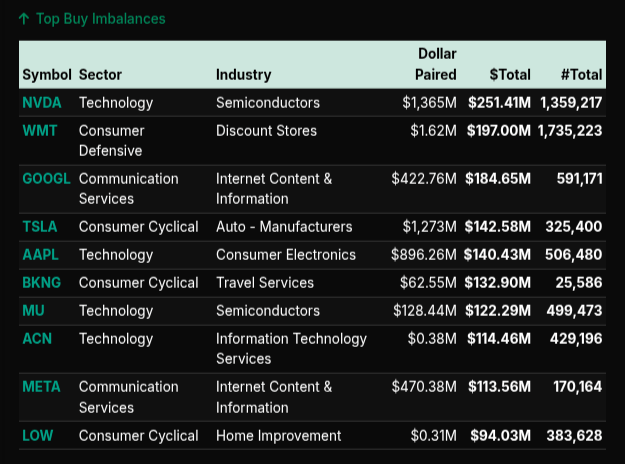

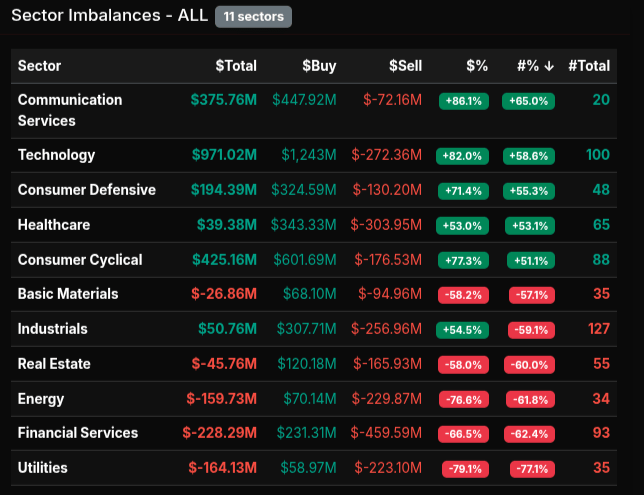

Sector flows showed where the rotation occurred. Communication Services (+86%), Technology (+82%), and Consumer Cyclical (+77%) carried the buy side. Heavy dollar inflows went into NVDA ($251M), GOOGL ($184M), TSLA ($142M), and AAPL ($140M). But Basic Materials (-58%), Energy (-67%), Financials (-66%), and Utilities (-79%) leaned sharply negative, indicating broad distribution outside of growth.

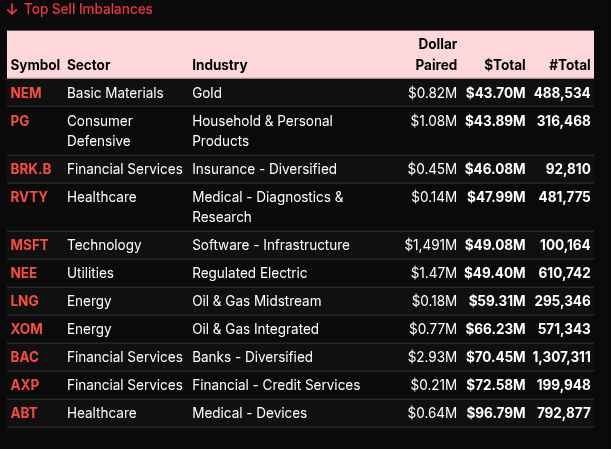

The sell side was led by NEM, PG, BRK.B, RVTY, MSFT, NEE, and XOM, each showing meaningful negative imbalances despite the early buy surge. The contrast between large-cap tech inflows and persistent selling in defensives and cyclicals reinforced the rotational character: dollars chased megacap growth, but symbol breadth pointed to a broader sell program.

By the close, NASDAQ still held a strong 88% buy dollar lean, but NYSE was firmly negative (-52.6%). The imbalance curve clearly showed buyers losing control after 15:54, with sellers dominating the final minutes.

Technical Edge

Fair Values for December 8, 2025:

-

SP: 6.88

-

NQ: 30.05

-

Dow: 45.31

Daily Market Recap 📊

For Monday, December 8, 2025

• NYSE Breadth: 38.56%

• Nasdaq Breadth: 59.79%

• Total Breadth: 57.26%

• NYSE Advance/Decline: 33.97%

• Nasdaq Advance/Decline: 44.79%

• Total Advance/Decline: 40.82%

• NYSE New Highs/New Lows: 86 / 39

• Nasdaq New Highs/New Lows: 200 / 100

• NYSE TRIN: 0.80

• Nasdaq TRIN: 0.54

Weekly Breadth Data 📈

For Week Ending Friday, December 5, 2025

• NYSE Breadth: 50.53%

• Nasdaq Breadth: 53.62%

• Total Breadth: 52.44%

• NYSE Advance/Decline: 48.46%

• Nasdaq Advance/Decline: 52.40%

• Total Advance/Decline: 50.97%

• NYSE New Highs/New Lows: 273 / 72

• Nasdaq New Highs/New Lows: 441 / 297

• NYSE TRIN: 0.90

• Nasdaq TRIN: 0.93

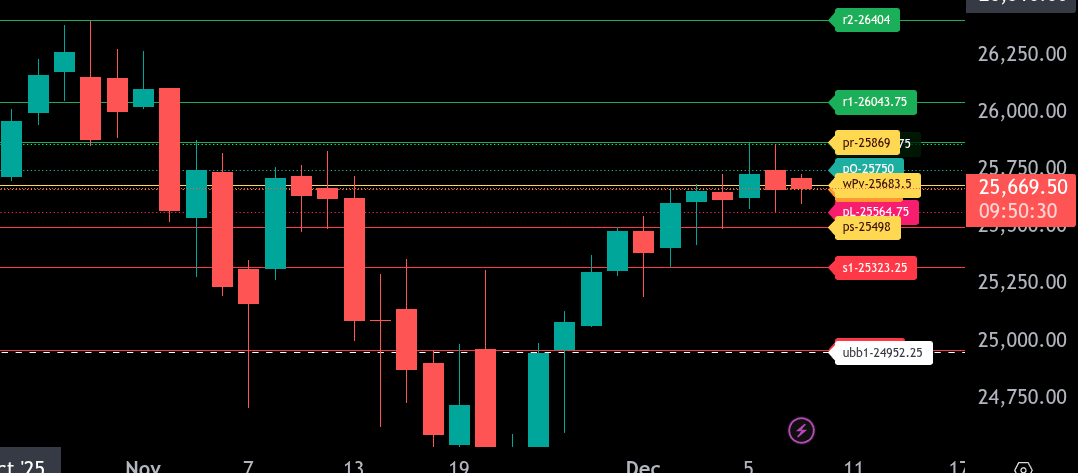

ES & NQ Levels (Premium only)

ES – Z Levels

The bull/bear line for ES is at 6859.25. ES is trading near 6860.50, holding just above this key pivot. Staying above 6859.25 keeps a short-term bullish tone; losing it shifts momentum back to sellers.

The upper range target is 6894.50. If ES can firm above 6883.00 and push through 6894.50, upside extension toward 6927.50 becomes likely.

The lower range target is 6824.00. A break back below 6859.25 opens the door to 6855.25, then 6835.25, and into 6824.00. Losing 6824.00 exposes 6791.00.

Overall: Holding above 6859.25 favors rotation back toward 6894.50. Failure under 6859.25 puts sellers in control with 6824.00 as the main downside magnet.

NQ – Z – Levels

The bull/bear line for the NQ is at 25,683.50. Price is currently trading just below at 25,669.50, signaling early-session weakness. A sustained move back above 25,683.50 is needed to shift intraday momentum upward.

If price fails to reclaim the bull/bear line, downside pressure favors a move into the lower range target at 25,498. Additional support sits at 25,664, then 25,564.75. A break under these zones opens the path toward 25,323.25.

If buyers regain control above 25,683.50, resistance comes in at 25,750 and then the upper range target at 25,869. Above that, the next resistance level is 26,043.

Overall, below 25,683.50 keeps the tone defensive, while reclaiming it invites a test of the upper areas.

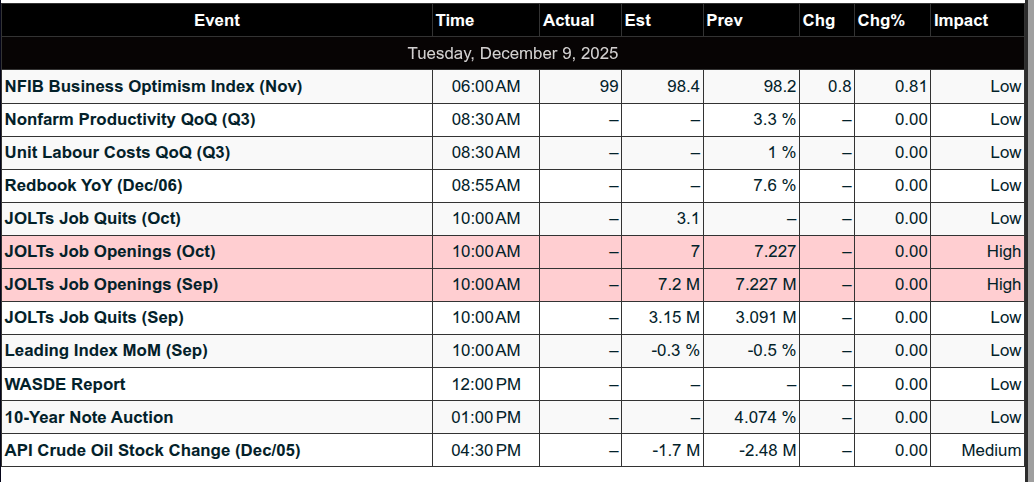

Calendars

Economic Calendar

Today

Important Upcoming

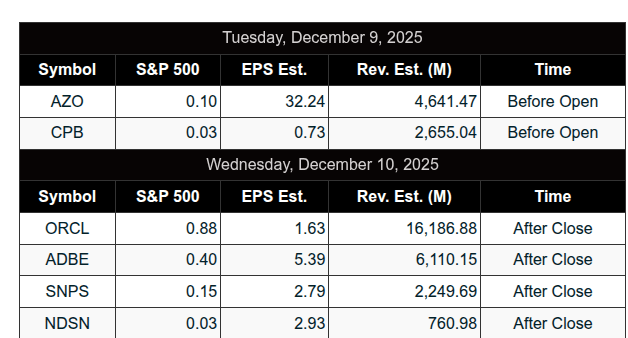

Earnings

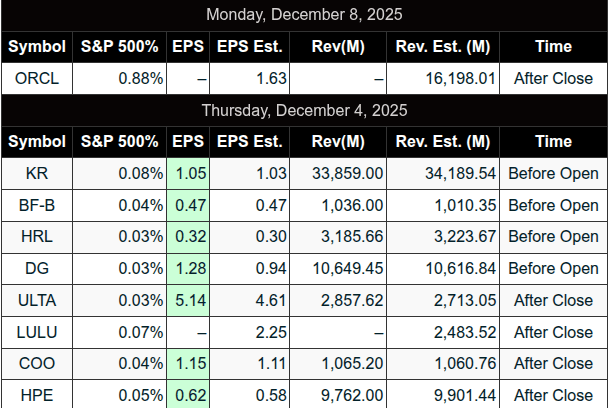

Trading Room Summaries

Polaris Trading Group Summary – Monday, December 8, 2025

The trading day opened with cautious optimism but quickly turned into a grind marked by indecision, choppy action, and persistent bearish pressure. Despite early hopes for increased volatility and range expansion, Monday unfolded as a day of patience, selectivity, and important lessons.

Morning Session: Choppy Start, Caution Advised

-

PTGDavid and the team opened the day with key links, charts, and strategy guidance. Manny highlighted early that vol might not be suppressed and hinted at potential range expansion, favoring setup #4.

-

A long trade idea around 6880.75 was offered by Manny, and Bosier planned longs above 81, with adds at 87 and 89, but nothing materialized cleanly early.

-

David reminded the room that bulls must reclaim the 6870 handle, otherwise momentum may falter — which it eventually did.

Lesson: Both Manny and David stressed caution on Mondays — never go full size early, avoid “attacking” the open, and let the market settle. This mindset helped keep traders defensive and protected from early whipsaws.

Midday: Bear Pressure Intensifies

-

Bulls lost control after giving up 6870; David noted “it was toast for da bulls.”

-

Manny salvaged a solid +7pt short on a textbook “lay-up” trade, offsetting his earlier -4pt scratch on Setup #3.

-

Multiple levels from the PTG Daily Range Calculator and Cycle Day projections were fulfilled:

-

CD1 low hit at 6836.25

-

Cycle Day 3 violation level and MoneyBoz confluence all tagged in the 6835-6838 zone.

-

-

Market chopped around these levels with no meaningful bullish response. David called out “no conviction” and “uninspiring rhythms.”

Lesson: Respect key zones. The confluence of multiple technical levels around 6835 created a magnet for price action. When bulls failed to reclaim broken support, the door opened for deeper value shifts lower.

Afternoon: News-Driven Bounce, Quickly Faded

-

Brief NVDA-related news spike (export chips to China) gave bulls a short squeeze attempt, reclaiming 6856, but it was short-lived.

-

David noted the move was “just another trap set to lure in the bait.”

-

Both NQ and CL Open Range short targets were hit. CL hit TGT1; NQ hit all.

-

Manny waited all afternoon for a Setup #4 entry, which never came, echoing David’s reminder: “Hope is NOT a strategy!”

Lesson: Stay tactical, not emotional. Manny’s patience and discipline to not force trades was a standout decision. The NVDA pop reminded everyone to be cautious with news-based volatility — traps can be swift.

End of Day: Bears Dominate, Bulls Absorb

-

Despite a $2.4B MOC buy imbalance, the late-day rally lacked teeth and was absorbed quickly. Price returned to VWAP, ending the session with no meaningful upside progress.

-

David emphasized: “Wait all day for a decent move and all you get is the closing move @ the final bell… That is no way to trade.”

Highlights & Takeaways

-

Best Trade of the Day: Manny’s +7pt short on a clean setup after early scratch.

-

Key Level Respect: 6870 and 6835 zones provided major structure for the day.

-

Biggest Lesson: Mondays require patience and smaller size. Forcing trades or chasing early moves often leads to regret.

-

Discipline Wins: Staying out was sometimes the best trade — as David said, “You basically got paid sitting on the sidelines today.”

Market Mood Summary:

-

Bias: Bearish

-

Volatility: Gradually increased, particularly after NVDA news.

-

Structure: Key breakdowns followed by rejection of key reclaim levels.

-

Conviction: Low from bulls; bears had ball control throughout.

Solid read and adaptation by the room yesterday — with cautious, risk-aware trading prevailing over forced entries. Today’s setups will be clearer thanks to yesterday’s groundwork.

Discovery Trading Group Room Preview – December 9, 2025

Macro & Political Highlights:

-

China/Nvidia Deal: Futures steady after Trump approves Nvidia (NVDA) to resume H200 AI chip sales to “approved” Chinese customers. The U.S. will receive 25% of NVDA’s China sales under the deal.

-

Fed Decision Looms: FedWatch shows 89.4% probability of a rate cut at tomorrow’s FOMC meeting. Market reaction remains uncertain amid unclear future policy path.

-

Trade & Tariffs:

-

Trump unveils $12B farmer aid package, funded by tariff revenues, to offset trade war effects.

-

Threats of an additional 5% tariff on Mexico over water treaty violations.

-

USMCA exit is reportedly under consideration by the Trump administration.

-

Despite a 29% drop in U.S.-bound shipments, China posts record $1T+ trade surplus.

-

Economic Sentiment & Legal Watch:

-

Trump to hit the road amid poor poll numbers on inflation handling (CBS: 36% approve on economy, 32% on inflation).

-

White House investigating price fixing in the supply chain.

-

Justice Kavanaugh voices concern over FTC independence, warning of potential implications for the Fed.

Market & Technical Outlook:

-

Volatility remains moderate ahead of the Fed. ES 5-day average range: 51.75 points.

-

Whale bias: Short into the U.S. open on light overnight volume.

-

Trendline levels:

-

Resistance: 7278/83, 7408/13

-

Support: 6768/63, 6602/07, 6444/39

-

-

ES grinding higher, holding above 50-day MA (6781.50); trendlines remain in play.

Earnings & Data Watch:

-

Premarket: AutoZone (AZO). After-hours: Casey’s (CASY), GameStop (GME). Wednesday AM: Chewy (CHWY).

-

Key data today:

-

JOLTS (delayed) @ 10:00am ET

-

CB Leading Index (delayed) @ 10:00am ET

-

Tentative: ADP Weekly Employment @ 8:15am ET

-

Affiliate Disclosure: This newsletter may contain affiliate links, which means we may earn a commission if you click through and make a purchase. This comes at no additional cost to you and helps us continue providing valuable content. We only recommend products or services we genuinely believe in. Thank you for your support!

Disclaimer: Charts and analysis are for discussion and education purposes only. I am not a financial advisor, do not give financial advice and am not recommending the buying or selling of any security.

Remember: Not all setups will trigger. Not all setups will be profitable. Not all setups should be taken. These are simply the setups that I have put together for years on my own and what I watch as part of my own “game plan” coming into each day. Good luck!

This post goes out as an email to our subscribers every day and is posted for free here around 2 PM ET. To get your real-time copy, sign up for the free or premium version here: Opening Print Subscribe.

Comments are closed