This post goes out as an email to our subscribers every day and is posted for free here around 2 PM ET. To get your real-time copy, sign up for the free or premium version here: Opening Print Subscribe.

Equities Soar Despite Inflation Risks and Policy Uncertainty

Follow @MrTopStep on Twitter and please share if you find our work valuable!

Our View

These markets are bulletproof. Every lower open is a buy, as is every pullback. I get it—the markets are on a roll, with most of the big banks adjusting their year-end forecasts for the S&P higher. I get over 15 bank reports every day, from CitiBank to UBS; I get them all. They were lowering their year-end projections back in April. I have seen this many times, and it usually doesn’t end with the desired result, but I’m not sure about the last six months of this year. I think the markets are in motion, and despite a laundry list of negatives, the S&P continues to push higher.

Let’s face it—Trump is a market disrupter, and it’s going to be that way for the next 1,286 days. While I feel confident that there is a lot more upside this year, I’m really starting to get concerned about next year. I do not think the ES will have such an easy 2026. Markets continue to overlook all the negatives, but for how long?

Analysts at Morgan Stanley anticipate a mild recession manifesting in 2026, driven by tariff uncertainties leading to corporate layoffs and delayed Federal Reserve rate cuts focused on controlling inflation. This could cause earnings per share (EPS) growth to dip into modestly negative territory early in the year, weighing on stock valuations and market performance. Even if the downturn is less severe than past recessions due to recent “rolling recessions” and muted private sector growth, it might still trigger volatility and pullbacks in the index.

Escalating trade tensions under the Trump administration, including higher tariffs (potentially increasing the effective U.S. tariff rate by 10 percentage points to 13%), could raise inflation, reduce consumer spending, and exacerbate economic challenges. Goldman Sachs has cited these factors, along with lower GDP growth projections (1.7% for Q4 2025), as reasons for downgrading S&P 500 EPS forecasts to $280 for 2026 (down from $288), implying only 7% growth. Persistent tariffs might also spark global retaliation, further straining sectors like tech and communications.

Increased Uncertainty and Equity Risk Premium: Heightened policy uncertainty from trade policies and fiscal pressures could elevate the equity risk premium, making stocks less attractive relative to other investments. This might prolong any downturn, especially if combined with broader global challenges.

Like I said, Trump can’t sit idle: 35% tariff on Canada; shocked the EU and Mexico with tariffs; gave ICE agents “total authorization” to protect themselves; threatened to revoke Rosie O’Donnell’s citizenship; and announced plans for higher levies on copper, pharmaceuticals, and semiconductors. I know I could list more, but I think you get the point.

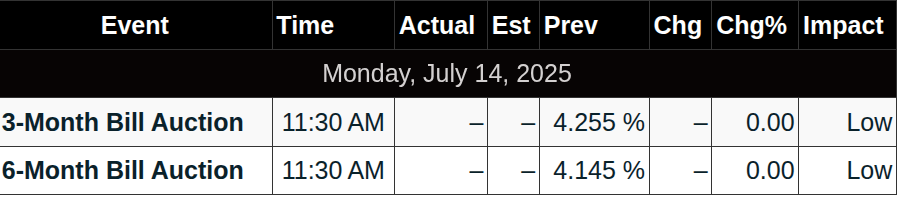

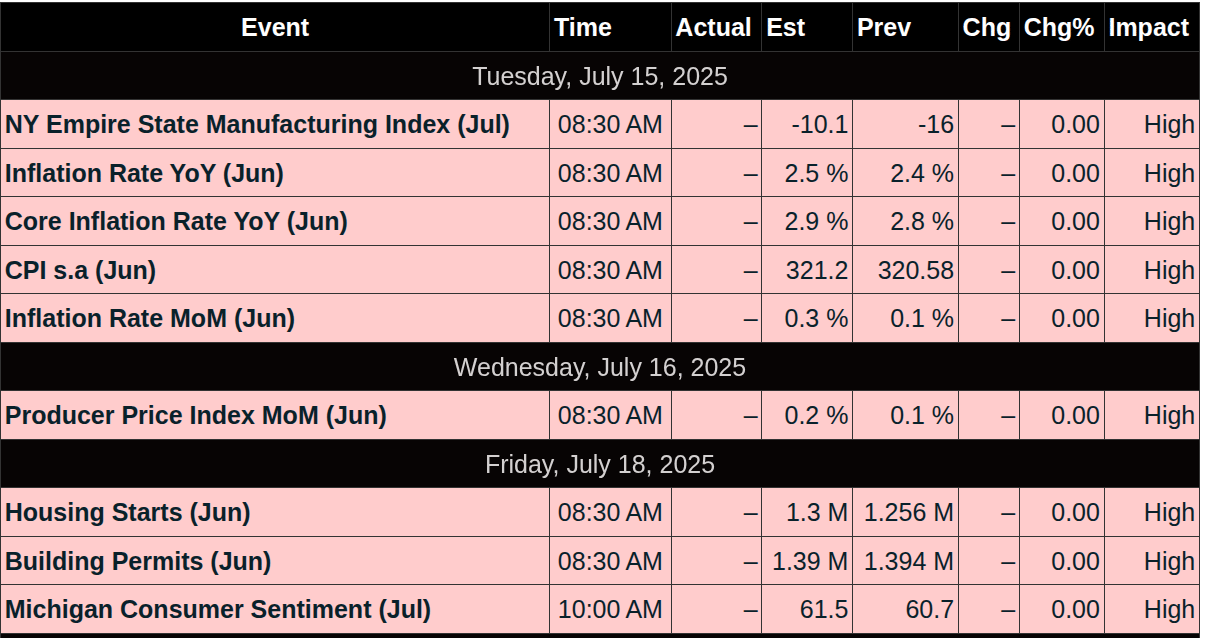

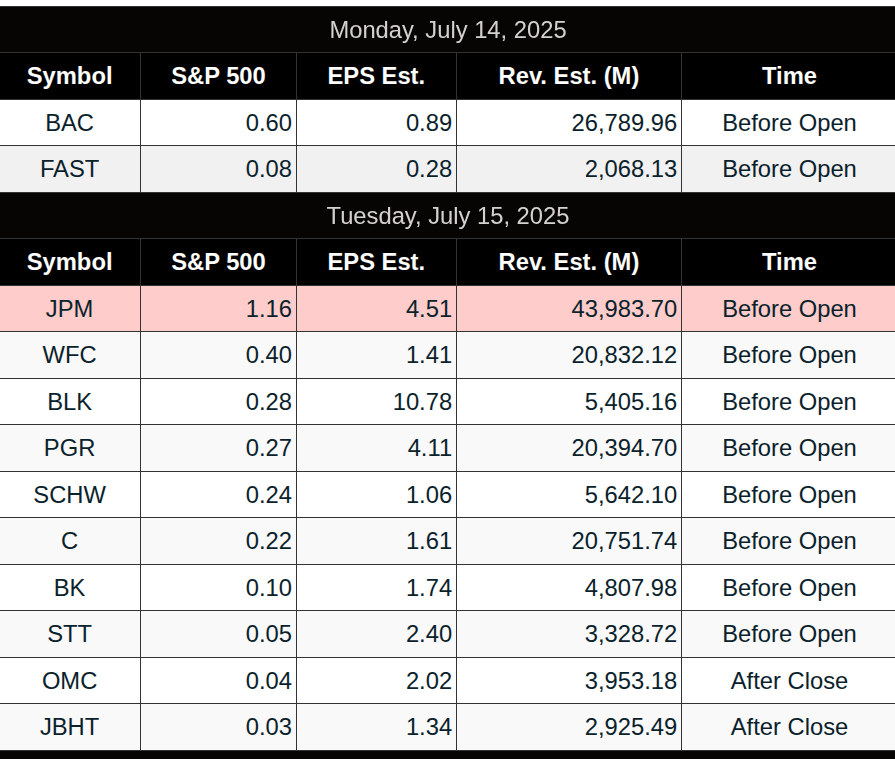

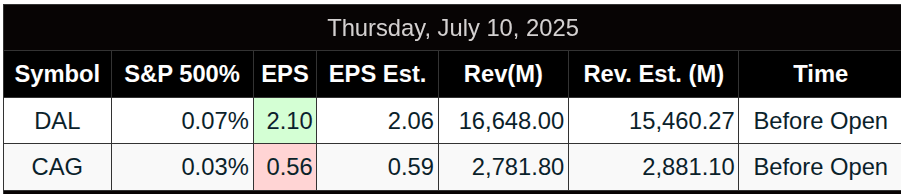

This week has a big economic and earnings schedule. Tuesday, JP Morgan and Wells Fargo report earnings at 7:00, CitiBank reports at 8:00 am, CPI, and four Fed speakers. Wednesday, Johnson & Johnson and B of A report at 6:45 am, Goldman Sachs reports at 7:30 am, PPI, Industrial Production, Beige Book, and two Fed speakers. Thursday has Jobless Claims, Retail Sales, Import Price Index, Philadelphia Fed Manufacturing Survey, Business Inventories, Home Builder Confidence Index, and four Fed speakers. Netflix reports earnings after the close at 4:01. Friday has Housing Starts, Building Permits, and Consumer Sentiment.

On the earnings front, Ned Davis Research said in a note that “Another reading in the upper 70s would suggest that companies have a grasp not only on tariffs but also on the broader macro environment.” This week is bank earnings week. In focus will be whether executives indicate if they are able to forecast and make decisions in areas such as capital investment and hiring despite the still-shifting trade backdrop.

Our Lean

Over the last few weeks, there has been an absence of economic reports and Fed speak—that all changes this week. The ES opened lower last night and made a low at 6263.00 and traded up to the 6279 area. Recently, most of Trump’s tariff drops have been bought, and on the 14th of the month (today) new money tends to get put to work (mid-month rebalancing). While the ES and NQ have bounced, the metals continue to outperform.

Our lean: The ES is entering a big area of support at the 6245–6250 level, with resistance at the 6320–6325 level. If the ES gaps lower, I am buying the open or the first drop under the lower open. I think the headline hell continues.

Since December: Platinum +50%, Copper +35%, Silver +33%, Palladium +33%, Gold +30%, Steel +30%, Gasoline +16%, Bitcoin +8%, Uranium +4%, Mag7 ETF -3%.

MiM and Daily Recap

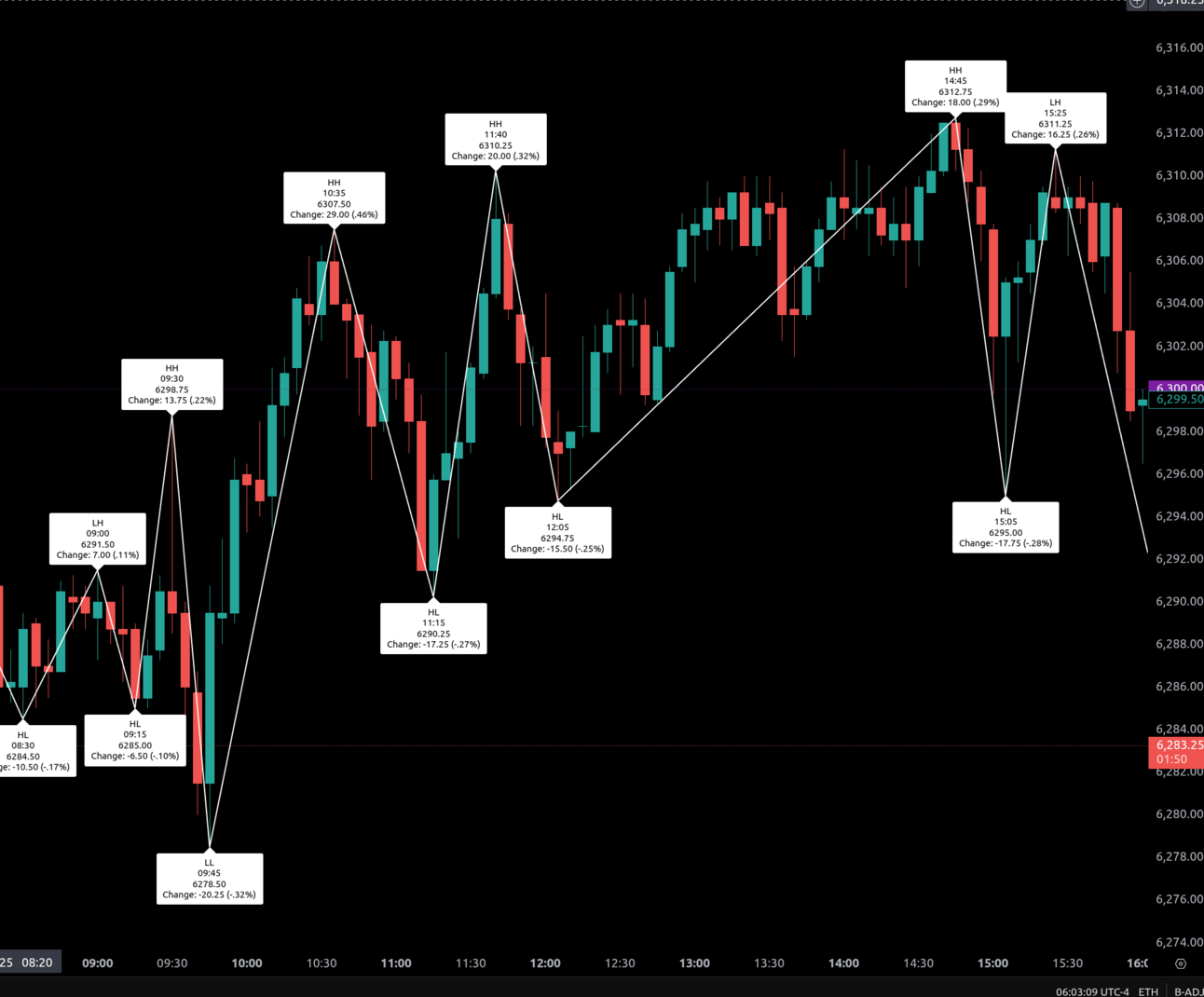

The overnight Thursday into Friday Globex session opened at 6323.00 and initially traded higher, reaching a peak of 6330.25 by 19:45 ET. This was followed by a steep decline to 6283.00 at 20:30, marking a 47.25-point drop (-0.75%). A rebound ensued, lifting prices to 6311.50 at 21:15 before sellers reasserted control and drove the ES to a fresh overnight low of 6276.75 by 06:00 ET, down 34.75 points (-0.55%) from the prior high. The Globex session settled at 6290.50, a net decline of 32.50 points (-0.51%) from its open.

The cash session began at 6290.50 and quickly tested support at 6278.50 during the first minutes. Buyers stepped in, driving the ES up to 6297.75 at 09:30 and extending the move to a morning high of 6307.50 by 10:35. This early rally added 29.00 points (+0.46%) from the Globex low. A retracement followed, pulling price back to 6282.50 by 10:55. The mid-morning saw renewed strength with a climb to 6310.25 at 11:40. This level proved to be resistance, triggering a slide to 6295.00 at 12:05. The afternoon saw the strongest push of the day, peaking at 6312.75 by 14:15 ET, a 17.75-point gain (+0.28%) off the midday low. However, sellers emerged again in the final hour, pressing prices to 6295.00 by 15:05.

From there, a late-day rebound effort took ES to 6312.25 by 15:25, before another sharp pullback set the closing tone. The session finished the regular hours at 6299.00, up 8.50 points (+0.14%) from the cash open and down 25.50 points (-0.40%) versus the prior cash close.

Volume was low, with 791,369 contracts traded during the regular session and a full-session total barely exceeding 1 million contracts.

The day’s overall tone was mixed, as early buying attempts failed to establish sustained momentum. The repeated inability to hold gains above 6310 hinted at persistent supply pressure overhead.

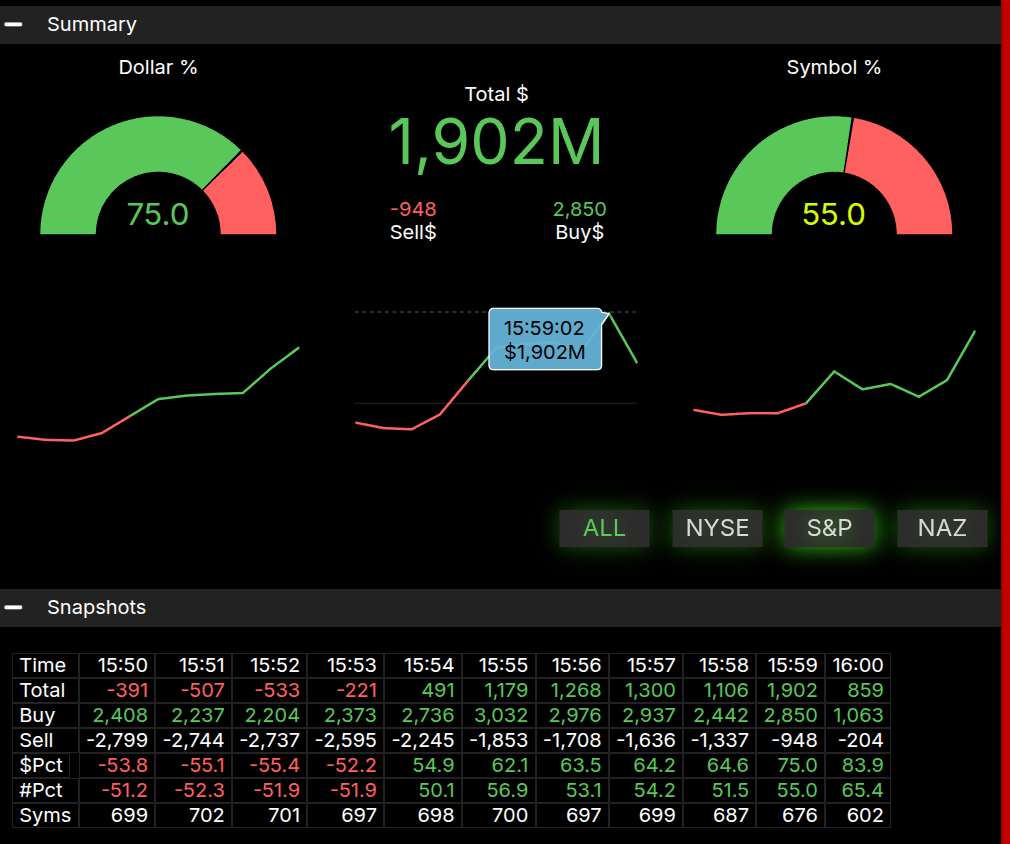

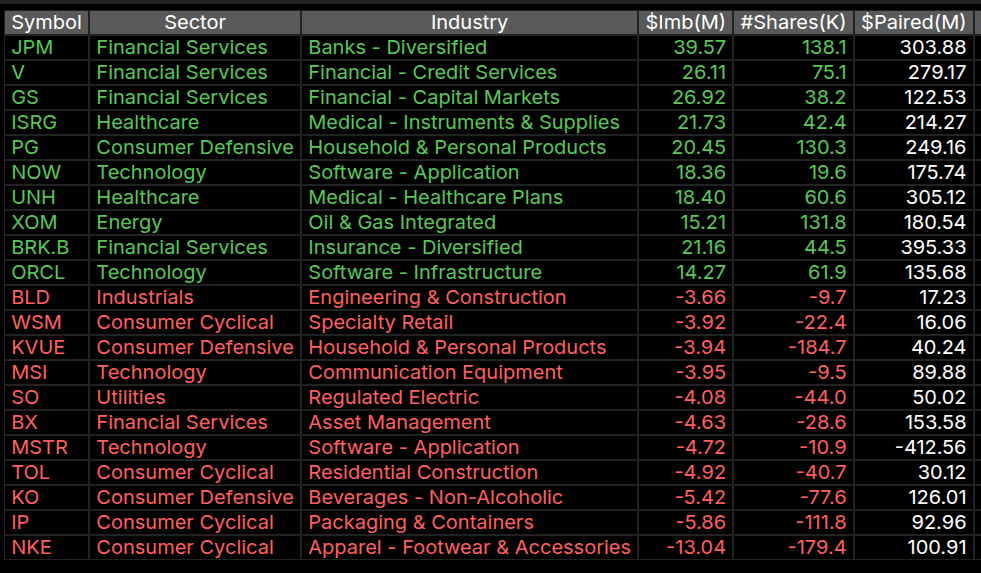

Market-on-Close imbalance data showed a strong buy skew, with total dollar imbalance at $1.902 billion to buy and the symbol imbalance reading 55.0%, which did not exceed the 66% threshold for an extreme signal. While the sizeable buy interest supported a modest afternoon lift, it did not prevent the late pullback that capped gains.

In summary, the ES spent most of the day oscillating in a wide but contained range, with repeated rallies failing to break decisively higher. The inability to close near session highs and the negative Globex performance left the tape leaning cautiously neutral to slightly bearish. Participants will be watching whether supply at the 6310–6315 zone continues to constrain upside in the next session.

Technical Edge

Fair Values for July 14, 2025:

-

SP: 39.77

-

NQ: 169.31

-

Dow: 220.12

Daily Breadth Data 📊

For Friday, July 11, 2025

• NYSE Breadth: 31% Upside Volume

• Nasdaq Breadth: 47% Upside Volume

• Total Breadth: 45% Upside Volume

• NYSE Advance/Decline: 28% Advance

• Nasdaq Advance/Decline: 27% Advance

• Total Advance/Decline: 28% Advance

• NYSE New Highs/New Lows: 61 / 17

• Nasdaq New Highs/New Lows: 113 / 52

• NYSE TRIN: 0.86

• Nasdaq TRIN: 0.42

Weekly Breadth Data 📈

For the Week Friday, July 11, 2025

• NYSE Breadth: 50% Upside Volume

• Nasdaq Breadth: 61% Upside Volume

• Total Breadth: 57% Upside Volume

• NYSE Advance/Decline: 45% Advance

• Nasdaq Advance/Decline: 45% Advance

• Total Advance/Decline: 45% Advance

• NYSE New Highs/New Lows: 264 / 35

• Nasdaq New Highs/New Lows: 453 / 157

• NYSE TRIN: 0.81

• Nasdaq TRIN: 0.50

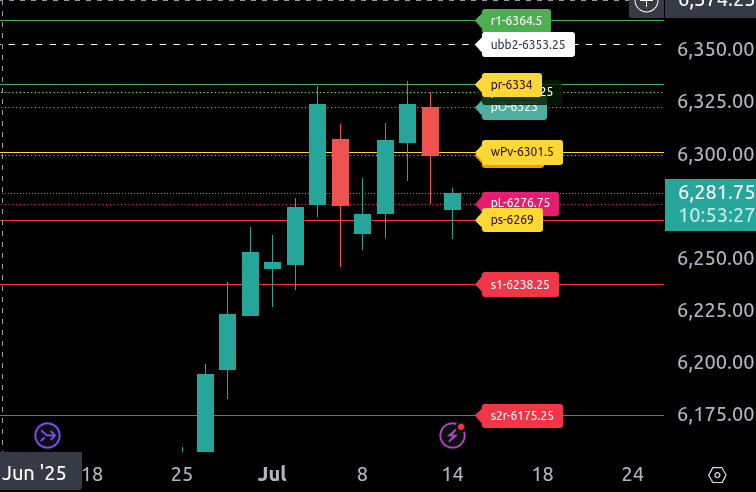

Today’s BTS Levels:

ES

The bull/bear line for the ES is at 6301.50. This is the key pivot level that must be reclaimed for bullish momentum to resume. Currently, ES is trading around 6282.25, indicating weakness below the bull/bear line.

If the price remains below 6301.50, expect continued downside pressure targeting 6269.00, the lower range target for today. A break below this area could extend the decline toward deeper support near 6238.25.

On the upside, if ES can reclaim 6301.50 and hold above it, the first resistance comes in at 6334.00, the upper range target for today. Strength above this level could drive a test of higher resistance near 6353.25 and then 6364.50.

Overall, the trend remains bearish below 6301.50, and caution is warranted until this level is decisively reclaimed by the bulls.

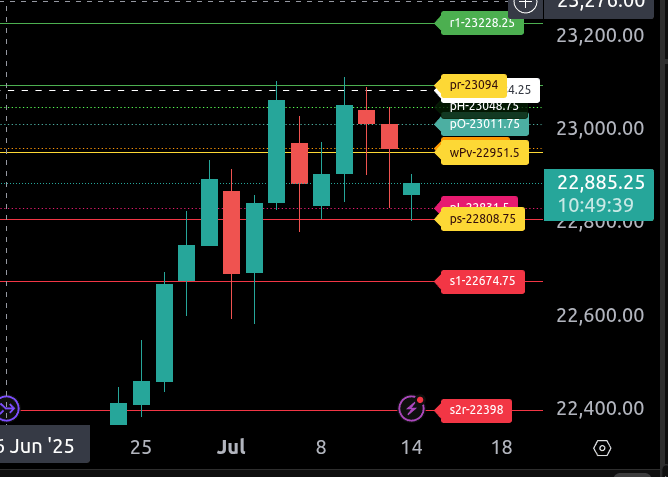

NQ

The bull/bear line for the NQ is at 22,951.50. This is the critical level that defines whether the market retains a bearish bias or can reclaim bullish momentum. With the current price trading around 22,885.75, NQ remains below this level, indicating continued selling pressure if buyers fail to step back in.

On the downside, if weakness persists, the lower range target comes in at 22,808.75. A decisive break below this level opens the door toward deeper support at 22,674.75.

On the upside, if NQ reclaims the bull/bear line at 22,951.50, the first resistance is 23,011.75 and then 23,048.75. Sustained strength above these areas would set the stage to test 23,094 and the upper range target at 23,084.25.

Overall, the trend remains bearish while trading below 22,951.50. Bulls need to defend against further downside and reclaim the bull/bear line to shift sentiment back toward the upper targets.

Calendars

Today’s Economic Calendar

This Week’s Important Economic Events

Today’s Earnings

Recent Earnings

Room Summaries:

Polaris Trading Group Summary – Friday, July 11, 2025

Positive Trades & Highlights:

-

Crude Oil (CL) Open Range Long:

-

TGT 1 hit early, confirming the initial bullish bias.

-

TGT 2 filled soon after, capturing more upside momentum.

-

David actively managed the trailing stop, first moving it to breakeven, then up to TGT 1 for protection.

-

Eventually, the CL stop trail was elected, locking in gains. A textbook example of scaling and protecting profits.

-

-

ES & NQ Open Range Shorts:

-

ES and NQ were called short as pre-market ranges resolved lower.

-

The ES Bear Stacker play showed good tactical entry on weakness.

-

While NQ was stopped out just shy of target, this illustrated the importance of respecting stops even when trades nearly work.

-

-

Clear trend signals developed mid-morning, with several members noting signs of a trend day emerging.

Key Lessons Learned:

-

Order Discipline:

David emphasized: “I have no control over trade outcomes. I can only control the orders I enter.” This underscored why the NQ stop-out, while frustrating, was accepted without hesitation. -

Risk Management in Action:

The progression on CL—scaling out, trailing stops, and accepting exits—demonstrated professional trade management. -

Market Context Matters:

Despite early indecision (“still inside OR”), participants stayed patient until setups confirmed, rather than forcing trades. -

Adaptation to Narrow Ranges:

Blibby71 and others noted the week’s unusually tight 90-handle range, highlighting the need to adjust expectations and targets accordingly. -

Community Learning:

Several questions (for example, about partial entries on slope changes and retrace probabilities) led to good dialogue and learning moments.

Overall, this was a constructive day with solid wins on CL, disciplined exits on NQ, and valuable reminders about following process over prediction.

DTG Room Preview – Friday, July 11, 2025

-

Tariffs in Focus: Trade tensions remain front and center. The EU has prepared a $24.5B list of U.S. goods for potential tariffs if no deal is reached, following President Trump’s threat of a 30% tariff on EU and Mexican imports. The EU will pause counter-tariffs until early August while negotiations continue.

-

Inflation Data Ahead: June CPI is due this week, with markets watching for tariff impacts on inflation and implications for potential Fed rate cuts in two weeks. Political pressure on the Fed is rising as the White House signals Powell could be removed “if there’s cause.”

-

Safe Havens Climb: Silver closed at a 14-year high amid strong haven demand and tightening supply. Bitcoin surged past $120K, supported by uncertainty around Trump’s policies and a pro-crypto stance.

-

Earnings Season Starts: Key reports this week include Wells Fargo, Netflix, ASML, TSMC, PepsiCo, United Airlines, and American Express. Fastenal reports premarket today.

-

Volatility & Technical Levels: Market volatility remains moderate with the ES 5-day ADR at 53.75. No significant large-trader bias overnight. ES continues consolidating below all-time highs. Key trendline resistance: 6385–6388, 6456–6461. Support: 6114–6119, 6085–6090, 5655–5660.

Affiliate Disclosure: This newsletter may contain affiliate links, which means we may earn a commission if you click through and make a purchase. This comes at no additional cost to you and helps us continue providing valuable content. We only recommend products or services we genuinely believe in. Thank you for your support!

Disclaimer: Charts and analysis are for discussion and education purposes only. I am not a financial advisor, do not give financial advice and am not recommending the buying or selling of any security.

Remember: Not all setups will trigger. Not all setups will be profitable. Not all setups should be taken. These are simply the setups that I have put together for years on my own and what I watch as part of my own “game plan” coming into each day. Good luck!

This post goes out as an email to our subscribers every day and is posted for free here around 2 PM ET. To get your real-time copy, sign up for the free or premium version here: Opening Print Subscribe.

Comments are closed