How to Own the Long End?

A special guest post

Follow @MrTopStep on Twitter and please share if you find our work valuable.

Today’s very special guest piece comes from Dan at GTC Traders. Please enjoy this wonderful piece, either today or this weekend with a cup of coffee. Cheers

Long End Bonds?

We have heard several traders ask in social media streams …

“Why would anyone on planet Earth be looking to buy Bonds or have any bullish stance in an ETF like TLT?”

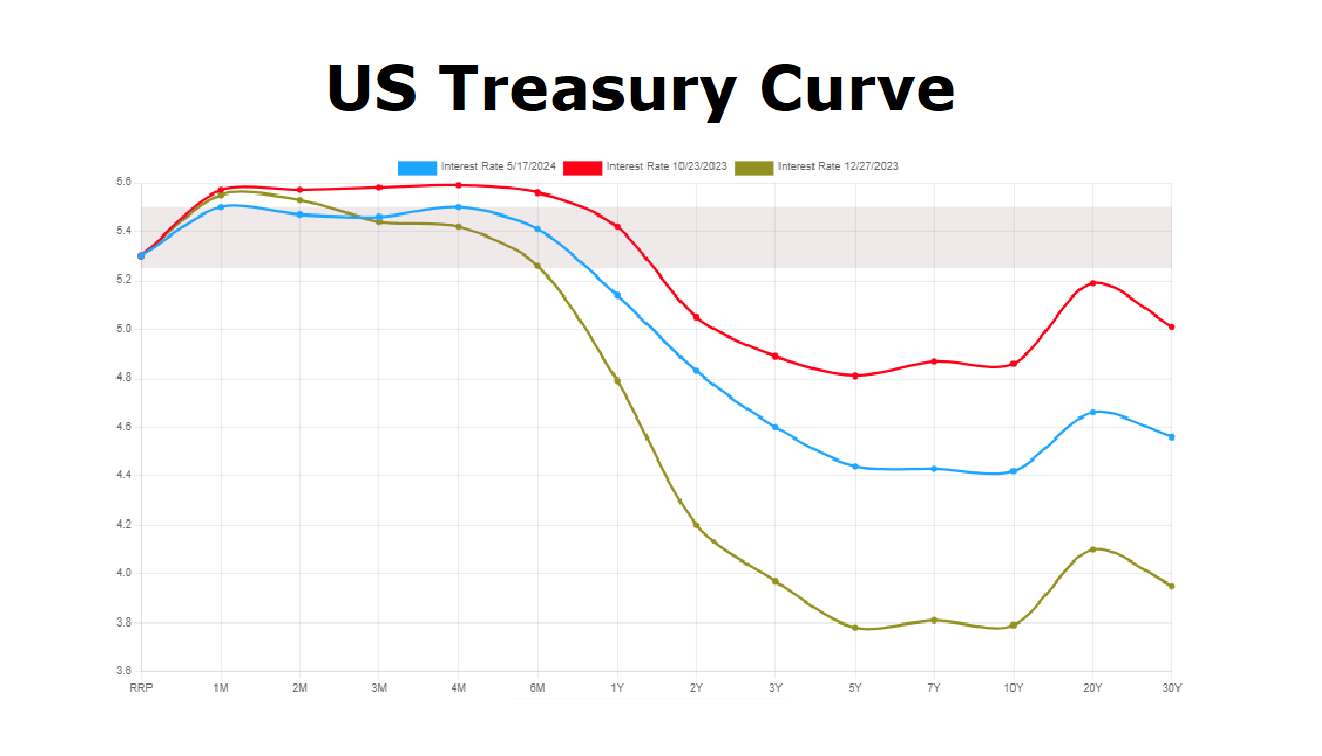

Good question. Any look at the Treasury Curve would show that long end bonds (or it’s derivative ETF equivalent TLT) is nearly the worst place you can be in terms of yield.

It just doesn’t seem to make sense. Especially as we have stated previously, we are bearish duration (higher yields). Even more confusing is that we currently long have a long TLT position, as we stated on May 3rd, 2024.

“Dan if you are in the Higher for Longer Camp (H4L+) and Bonds are the worst place to be for yield? Then why in the world are you long TLT at the moment? Why not hold 52 week bills for higher yield? Or short STIRs if you are bearish yield?”

Two words.

Mandate. And Periodicity.

Mandate

At times a Firm, Pension, SFO, etc operates under a Portfolio Mandate that requires a specific approach. Briefly, a Portfolio Mandate is a codified approach that dictates the rules that must be followed for the firm operating under such a mandate. For many decades Bonds offered the best yield; such institutions would codify that the firm must hold bonds. So now, even today when Bonds offer a worse yield? They don’t have a choice. Our Private Proprietary Firm has such a mandate and requires we operate in Equities (Stocks), ETF’s and Stock Options. Though I have no problem trading Futures. But in that firm? I must trade Equity instruments.

Since bonds have been in such an awful state for so long a time period, the problem simply put is …

“Great. How do we hold Bond exposure to fulfill our mandate and not get murdered by higher rates?”

Periodicity

As we outlined last week; while we are in the higher inflation and interest rates for longer ‘camp’, at the moment? That is in the long-term. The reverse of Globalization and structural inflation within the United States could take some time to play out.

As we all know while a market may trend in direction for some time there is always a ‘rotation’ and ‘back fill’ for a time. In a bull-market in the S&P? You’ll get a retracement for a time, and prices will fall 3% to 4%.

So while in the longer-term, we are bearish duration? In the short-term with some help by a weaker CPI print; we were willing to play bullish duration. For at least a while. As a trade. We playing such a retracement with our bullish duration trade in TLT.

This has paid off. But in the long term? We are bearish on Bond and TLT price. In the short-term, we bought TLT and this has paid off since May 3rd.

So while bearish duration in the LONG term; we bought the long end for cheaper yields in the SHORT term and are up.

Great. Wonderful. That’s the past. What now? Especially if we are bullish on yield?

Hedging and Price Structures

We can continue to hold TLT. As can anyone who wishes to continue to hold TLT. And then simply hedge it off if the long end begins to sell off to higher yields.

The price level we are watching on TLT is the $90.87 region. In the Futures? This would correspond to the 116’24 level in the Bonds (ZB).

TBF is a 1:1 Inverse TLT ETF. So one could buy TBF; price ratio’d out to match the TLT position, to hedge any drop in price to higher yields, in TLT. With the ZB? One could hedge with the UB (Ultra-Bonds).

With a 20% ratio’d hedge; the price drop of TLT is negated with TBF. One can thus adhere to mandates, quantitative or otherwise. At the same time that 20% padding has both the dividend of TLT, and the dividend of TBF adding to the aforementioned 20% padding. If wrong on price? Keeping the hedge ratio at 20%, one can still make money on the long TLT position.

And the above hedge ratio can be adjusted to the conviction of the trader. 10%, or even 50%. It becomes a little capital intensive by eating up buying power as you increase the hedge ratio? But in this way one can still hold TLT and even outperform TLT over time.

Which is what we are looking to do. Hedge if we consistently trade below that $90.87 structure, or the 116’24 level in the Bonds (ZB).

As always these are our thoughts. Not yours.

Stay safe and trade well.

Comments are closed