This post goes out as an email to our subscribers every day and is posted for free here around 2 PM ET. To get your real-time copy, sign up for the free or premium version here: Opening Print Subscribe.

No Rate Cuts, No Problem? Markets Shake Off Weakness

Follow @MrTopStep on Twitter and please share if you find our work valuable!

Our View

If you haven’t noticed, buying the lower opens has been the money trade. I don’t know how many there have been in 2025, but the vast majority have been bought! I’d say that’s a bullish sign, but we all know that tape bombs have been a major issue for the bulls.

It looks to me like the ES is backfilling and consolidating. According to FactSet, the CPI number for January is projected to rise 2.9% year over year (FactSet CPI Report). Will this be a problem for the ES? It should be, but the public doesn’t seem too concerned, or maybe it’s already priced in.

The index markets started the day in the red after President Trump signed off on 25% tariffs on steel and aluminum imports to the U.S. but shook off the weakness, with the S&P cash closing up 0.7% cash close to cash close, its smallest daily advance since November. The YM closed up 0.4%, and the NQ closed down .24% after Fed Chairman Powell told Congress that the economy was doing well and that the central bank would take its time deciding when to cut interest rates.

I’m 100% sure there will be no rate cuts in March or May. The Fed knows it can’t afford to make any more mistakes, and I think rate cuts are off the table for at least the first six months if not longer.

Our Lean

After what Powell had to say and all the back-and-fill action in the ES and NQ, I think there’s a good chance the futures rally today. I know there’s a brick wall at the 6110-6120 level, but I also know that MrTopStep has a trading rule that says “no stops go untouched.” There’s a high concentration of stops go all the way up to the 6138 level.

If I’m wrong, then we could see a move back down to the 6030-6060 level. I’d rather buy a gap down than sell a gap up.

Usual February Weak Trading

Stocks are experiencing the typical midwinter struggles. Historically, the market tends to rally during the first half of February, but those gains often fade after mid-month—sometimes even earlier in post-election years.

MiM and Daily Recap

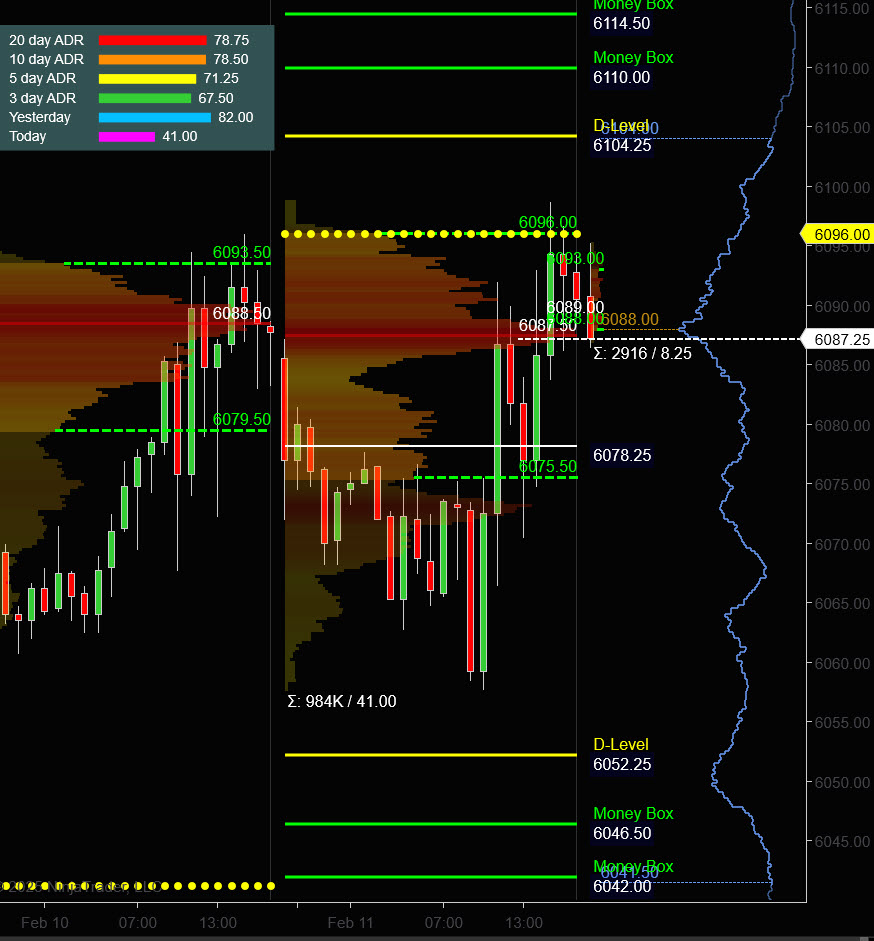

The ES traded lower in the overnight session, hitting a low of 6057.75 at 9:00 a.m. before buyers stepped in. The market opened the regular session at 6065.00 and quickly gained traction, climbing to 6079.50 by 10:00 a.m. After a brief pullback to 6066.50 at 10:06 a.m., buyers regained control, pushing prices higher throughout the morning. The contract printed a session high of 6092.00 at 10:51 a.m., marking a strong rally from the overnight lows.

From there, selling pressure emerged, leading to a slight retracement down to 6088.75 at 11:30 a.m. before another leg lower to 6070.50 at 12:09 p.m., marking the midday low. However, dip buyers quickly stepped in, propelling prices back to 6084.00 at 12:30 p.m. This back-and-forth action defined much of the session, as the market maintained an upward bias with periodic pullbacks.

By 1:45 p.m., the ES had recovered to 6093.00 before another brief dip to 6083.75 at 2:12 p.m. The afternoon session saw another push higher, reaching 6098.75 at 2:42 p.m., the highest point of the day. However, the market struggled to sustain those gains, as it slipped back to 6090.50 at the cleanup close.

In terms of session performance, the ES closed the regular session at 6092.50, up 27.50 points (+0.45%) from the open, while the full session closed at 6090.50, a modest 5-point gain (+0.08%) over the prior day’s close.

Overall, the market displayed a firm but choppy tone, with buyers stepping in on pullbacks. The morning rally from the 6057.75 low to the 6092.00 high set the bullish tone, but midday selling briefly tested support before another push higher in the afternoon. Despite some weakness into the close, the ES remained well above the prior day’s lows, reinforcing a constructive outlook.

The MiM (Market on Close) imbalance built up a slow sell side to about -850M, but there was no clear symbol lean indicating strong exit or entry sentiment from fund traders.

In the end, it was a slow grind. In terms of the ES’s overall tone, it remained firm, but there was a significant lack of trade. In terms of the ES’s overall activity, volume was low again at 984K.

The yield on the 10-year note rose for a fourth consecutive trading day, settling at 4.536%, up from 4.492% on Monday. Gold dipped 0.1% from its Monday record, ending at $2,912.50 per troy ounce, though it’s still up 11% for the year. Meanwhile, crude oil gained 1.5% to $77.00 a barrel, marking its third consecutive session of gains.

Technical Edge

MrTopStep Levels:

Fair Values for February 12, 2025:

-

SP: 20.36

-

NQ: 81.75

-

Dow: 95.6

Daily Market Recap 📊

-

NYSE Breadth: 46.9% Upside Volume

-

Nasdaq Breadth: 48.4% Upside Volume

-

Total Breadth: 47.9% Upside Volume

-

NYSE Advance/Decline: 50.9% Advance

-

Nasdaq Advance/Decline: 40.0% Advance

-

Total Advance/Decline: 44.3% Advance

-

NYSE New Highs/New Lows: 67 / 62

-

Nasdaq New Highs/New Lows: 92 / 214

-

NYSE TRIN: 1.16

-

Nasdaq TRIN: 0.70

Weekly Market 📈

-

NYSE Breadth: 47.7% Upside Volume

-

Nasdaq Breadth: 56.7% Upside Volume

-

Total Breadth: 53.1% Upside Volume

-

NYSE Advance/Decline: 50.9% Advance

-

Nasdaq Advance/Decline: 47.6% Advance

-

Total Advance/Decline: 48.8% Advance

-

NYSE New Highs/New Lows: 204 / 166

-

Nasdaq New Highs/New Lows: 344 / 394

-

NYSE TRIN: 1.06

-

Nasdaq TRIN: 0.83

Guest Posts — Polaris Trading Group

Prior Session was Cycle Day 3: Positive 3-Day Cycle Statistic (91%) remains intact as price traded above the CD1 Low (6041.25) and fulfilled its initial target (6085). Overall activity was muted as traders await the all-import CPI Report. Range for this session was 41 handles on 984k contracts exchanged.

FREE TRIAL link to PTG/Taylor Three Day Cycle

For a more detailed recap of the trading session, click on this link: Trading Room RECAP 2.11.25

…Transition from Cycle Day 3 to Cycle Day 1

Transition into Cycle Day 1: Today begins a new cycle with the objective to establish a secure low from which to stage the next rally.

Odds of Decline > 10 = 79%…> 20 = 56%

Traders have been in a “holding-pattern” ahead of the all-important Consumer Price Index (CPI) print today @ 8:30 am. Below is a preview of expectations.

Stay alert for potential “spike” price moves on the release!

Upcoming US CPI Report: Market Expectations and Implications

The upcoming Consumer Price Index (CPI) report, scheduled for release on February 12, 2025, is anticipated to show that inflation remained relatively stable in January. Market forecasts suggest a 0.3% month-over-month increase in the headline CPI, slightly below December’s 0.4% rise, maintaining the year-over-year rate at approximately 2.9%.

Core CPI, which excludes volatile food and energy prices, is also expected to rise by 0.3% month-over-month, with a year-over-year increase of 3.1%, down from 3.2% in December.

These projections indicate that while inflation has moderated from its mid-2022 peak of 9.1%, it remains above the Federal Reserve’s 2% target. Factors such as recent tariff implementations and a strong labor market, evidenced by low unemployment and robust wage growth, could contribute to persistent inflationary pressures.

Investors are closely monitoring these developments, as higher-than-expected inflation could influence Federal Reserve policy decisions, potentially delaying anticipated interest rate cuts.

Of course, nothing changes for PTG…Simply follow your plan. Take only Triple A setups and manage the $risk. ALWAYS HAVE HARD STOP-LOSSES in-place on the exchange.

PTG’s Primary Directive (PD) is to ALWAYS STAY IN ALIGNMENT with the DOMINANT FORCE.

As such, scenarios to consider for today’s trading.

Bull Scenario: Price sustains a bid above 6090+-, initially targets 6110 – 6115 zone.

Bear Scenario: Price sustains an offer below 6090+-, initially targets 6075 – 6070 zone.

PVA High Edge = 6096 PVA Low Edge = 6075 Prior POC = 6087

ES (Profile)

Thanks for reading, PTGDavid

Trading Room Summaries

Polaris Trading Group Summary – Tuesday, February 11, 2025

The trading day started with a bearish setup as price action sustained an offer below 6075, leading to downside targets being met early in the session. NASDAQ (NQ) followed a similar path, reaching the outlined 21705 – 21655 target zone.

A key turning point occurred when Fed Chair Jerome Powell testified at 10 AM, bringing a positive market reaction. This fueled an upside resolution, leading to an ES gap fill, as discussed earlier in response to Sorem’s question about gap trading. Price climbed past the 6075 LIS (Line in the Sand), targeting 6095 – 6105, which was later fulfilled.

During midday, price oscillated around 6075, with lighter volume as traders awaited Wednesday’s CPI report. Bears controlled the market into lunch, but overall, price remained range-bound throughout the afternoon.

By the close, the market remained in a neutral stance, reflecting hesitation ahead of the CPI print. A small MOC (Market-on-Close) buy imbalance ($530M) shifted to a sell imbalance ($600M) just before the session ended.

Key Takeaways & Lessons Learned:

-

Successful execution of the bear scenario early in the day, hitting downside targets.

-

Fed testimony influenced a market reversal, demonstrating the importance of news-driven price action.

-

Gap-fill strategy worked effectively, reinforcing the significance of market structure.

-

Patience was key in the afternoon as the market remained range-bound, emphasizing the value of waiting for clear setups.

The session wrapped up with traders awaiting CPI data, which is expected to bring more volatility today. See you for the CPI fireworks!

Discovery Trading Group Room Preview – Wednesday, February 12, 2025

-

Market Focus:

-

The key event today is the 8:30 AM ET release of January’s Consumer Price Index (CPI), a crucial inflation metric influencing potential Fed rate cuts. Market reaction to CPI will likely dictate today’s direction.

Fed & Macro Updates:

-

Fed Chair Jerome Powell reiterated before the Senate Banking Committee that the Fed is in no rush to change policy, citing persistent inflation and uncertainty around Trump’s trade policies.

-

Inflation remains above the Fed’s 2% target, though it continues to decline.

-

Last Friday’s UoM Consumer Sentiment survey hit a seven-month low, signaling potential economic concerns.

-

Powell addressed concerns about housing affordability, emphasizing that rate normalization could help but that the core issue is supply constraints, which are beyond the Fed’s control.

-

The insurance industry crisis was also a focus, as companies like State Farm have canceled policies due to mounting losses, affecting mortgage availability in high-risk areas.

Market Conditions & Sentiment:

-

Volatility declined Tuesday but could spike today depending on CPI reaction.

-

Large traders (whales) lean bearish into CPI, with overnight volume remaining light.

-

S&P 500 (ES) remains in a sideways grind, awaiting a catalyst for direction.

Earnings Calendar:

-

Premarket reports: AUR, AVTR, GOLD, BAM, CME, CCI, CVS, D, ECX, MLM, NI, OC, OSR, SW, SONY, IPG, KHC, VRT, WAT, WAB.

-

After-market reports: AR, APP, CSCO, CRBG, CW, EQIX, HUBS, KGC, MGM, PAYC, PPC, RDDT, HOOD, ROL, SCI, SLF, TTD, WMB, TYL, WTR, WCN.

Key Economic Events Today:

-

CPI release @ 8:30 AM ET (Market-moving event)

-

Crude Oil Inventories @ 10:30 AM ET

Chart Update:

-

The ES trendline setup remains unchanged from yesterday, continuing its sideways consolidation.

-

ES -Week to Week

The intraday bull/bear line for NQ today is at 6,085.75. Holding above this level could provide buyers with momentum toward 6,103 and the upper range level of 6,128 for the day. A sustained breakout beyond this area could target 6,134.25.

If sellers regain control below 6,085.75, watch for a move toward 6,071.5 and then the 6,057.75 level. Further downside could lead to a test of 6,045.25, which is the lower range limit for the day.

Today’s CPI number will inject volatility into the market and hopefully move us out of the 6,100 to 6,040 trading range we have been stuck in for the last few weeks.

NQ – Week to Week

The intraday bull/bear line for NQ today is at 21,780.25. Staying above this level could provide a push toward the 21,900 zone, with the upper range target for the day around the 22,000 area. Yesterday’s high at 21,871 serves as a key bullish marker.

The longer-term bull/bear line remains at 22,080.50, keeping the market in a mixed trend.

If NQ remains below 21,780.25, expect downside pressure toward 21,649.5 and 21,616. The lower range target for the day is 21,564. CPI volatility could bring the outer levels into play as the market reacts to inflation data.

Calendars

Today

Important Upcoming

Earnings

Affiliate Disclosure: This newsletter may contain affiliate links, which means we may earn a commission if you click through and make a purchase. This comes at no additional cost to you and helps us continue providing valuable content. We only recommend products or services we genuinely believe in. Thank you for your support!

Disclaimer: Charts and analysis are for discussion and education purposes only. I am not a financial advisor, do not give financial advice and am not recommending the buying or selling of any security.

Remember: Not all setups will trigger. Not all setups will be profitable. Not all setups should be taken. These are simply the setups that I have put together for years on my own and what I watch as part of my own “game plan” coming into each day. Good luck!

This post goes out as an email to our subscribers every day and is posted for free here around 2 PM ET. To get your real-time copy, sign up for the free or premium version here: Opening Print Subscribe.

Comments are closed