This post goes out as an email to our subscribers every day and is posted for free here around 2 PM ET. To get your real-time copy, sign up for the free or premium version here: Opening Print Subscribe.

Sell the Pops, Respect the Chaos — There’s a Pile of Trouble Lined Up This Week

Follow @MrTopStep on Twitter and please share if you find our work valuable!

Our View

There has been a lot of talk about Tech / AI losing some of its glimmer. I’m not sure about that, but what I am sure about is that there have been a lot of big rotations — especially last week. The Dow and S&P made new all-contract highs, while the Nasdaq is 1.4% off its 52-week high, and the Russell 2000 closed up 0.8% and up 4.6% on the week.

I saw a lot of rotations at my S&P desk for above futures repositioning for pension hedge funds, but it was much more defined for the portfolio managers, AIG, and Bank of America business. But it’s a whole different story today, as there is some type of rotation literally going on every day. It’s also something I believe can — and should — be tracked.

Our View

After offering a softer tone at the World Economic Forum in Davos, Trump returned to the U.S. and issued several new threats on social media. These included 100% tariffs on Canada if it pursues any deal with China, along with public statements containing personal insults directed at Prime Minister Mark Carney. He also revoked Canada’s invitation to participate in his proposed “Board of Peace” initiative, part of broader diplomatic maneuvers.

Trump continued his demands for U.S. control over Greenland, including strategic military bases and infrastructure such as a “golden dome”—though he ruled out the use of force after announcing a vague “framework deal.” He warned that any opposition would be “remembered,” and also threatened to sue JPMorgan Chase. Additionally, he floated the idea of invoking NATO’s Article 5 to address the U.S. southern border.

As I’ve always said, I know some will say it’s just his “art of the deal,” but I believe a more diplomatic approach—rather than bullying countries—may be more effective. It’s becoming very clear that the U.S. is losing allies quickly.

Our View

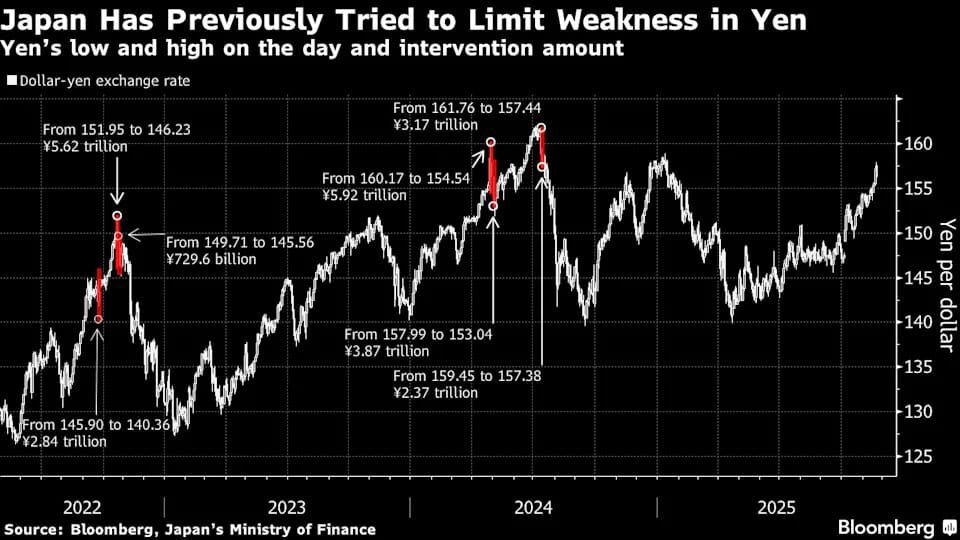

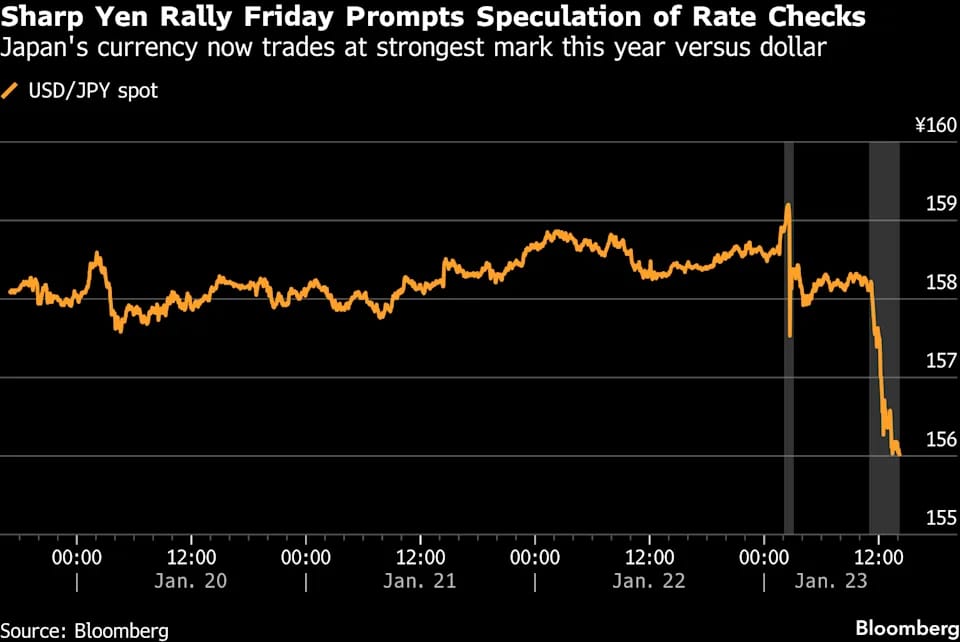

In the last five days, the DXY (U.S. Dollar Index) has fallen 1.88% and is down 1.91% year-to-date. Highlighting this week’s weakness was a warning from Japanese Prime Minister Sanae Takaichi, who suggested potential action on abnormal currency moves as speculation grows over possible intervention after the Federal Reserve Bank of New York reportedly contacted financial institutions to ask about the yen’s exchange rate. On Sunday, during a televised debate among party leaders, Takaichi said:

“It is not for me as a prime minister to comment on matters that should be determined by the market, but we will take all necessary measures to address speculative and highly abnormal movements.”

Japanese government officials have also issued warnings related to both bond yields and the yen, after yields on the country’s longest-duration bonds surged to record levels earlier last week before pulling back. Several major currencies have also rallied or shown relative strength against the U.S. dollar:

-

The Swiss franc (CHF), another safe-haven, benefited during periods of yen weakness prior to the rebound.

-

The euro (EUR) gained from broad-based dollar weakness and improving global risk appetite.

-

The Australian dollar (AUD) and New Zealand dollar (NZD) showed resilience, with bullish technical breaks and recoveries supported by commodity strength and global growth expectations.

-

The British pound (GBP) exhibited notable strength, backed by improved U.K. fiscal credibility and selective Bank of England restraint.

I had a floor operation in the CME currency quadrant for many years, with the main account being Dubai Holding—the global investment conglomerate owned by Sheikh Mohammed bin Rashid Al Maktoum, the Ruler of Dubai. It was one of the largest currency futures and options operations on the floor.

I also took an over $1 million hit from an account transferred over from Credit Agricole when they shut down their London brokerage unit. It was a small account that was short Swiss franc options.

I know most traders in the U.S. don’t think about currency moves that much, but when they happen, they can create extreme volatility across interest rates and stocks.

Below are 3-month and 5-year charts of the U.S. Dollar Index (DXY).

I think this should be a major concern for the U.S. dollar…

Our Lean

I didn’t even mention Senate Minority Leader Chuck Schumer saying, “Senate Democrats will not provide the votes” to fund immigration enforcement—part of a six-bill package set for action next week. This just adds to the already full boat of news hitting the tape.

I’m still a bull, but I have to admit—I think the markets are on shaky ground.

Trump’s armada is steaming into the Persian Gulf, and while there was a report that he’s not planning an attack but rather a blockade, a recent headline claimed the U.S. has informed Iraq, Jordan, Saudi Arabia, and the UAE of a pending attack on Iran.

It’s Sunday night and the ES opened down at 6904.00, made a low at 6870.00, and just traded up to 6933.00. It’s now at 6929.25, down 5.75 points.

-

February gold (GCG26) traded up to 5082.90 and is now trading 5074.90, up 95.20 or +1.91%

-

Silver (SIG26) made a high at 107.840 and is trading 107.300, up 6.298 or +6.24% and is down another 0.55% at 97.06

I still think this is the year of the VIX, and we have not seen anything yet.

Trump did a lot of backtracking last week, but he’s once again backing himself into a corner in the Middle East. I’ve told the PitBull many times that he’s been going too far, and only tonight did he finally admit it. He mentioned the U.S. $38.5 trillion debt and how Trump seems to just overlook it. When I brought up the DXY weakness, he noted the index traded down to 89.00 in January 2021.

That said, I’m going to stick with it. I know the ES can rally, I just don’t think it’ll hold.

Our lean: Sell the dead cat bounces. There’s a pile of shit coming our way this week.

I’ve been working hard on new AI levels, and in the next few days, I’ll be rolling them out. I’m not an “AI guy,” but I think all the big newsletters are using it, and I believe my work will be very good.

Type

Lower Bound

Upper Bound

Price Range

7,025.25

7,036.25

Price Range

7,005.00

7,017.50

Key Level

7,000.00

7,000.00

Price Range

6,981.75

7,001.75

Price Range

6,969.00

6,976.75

Price Range

6,900.00

6,920.00

Price Range

6,880.00

6,905.00

Price Range

6,865.00

6,875.00

Price Range

6,770.00

6,800.00

Key Level

6,748.00

6,748.00

Market Recap

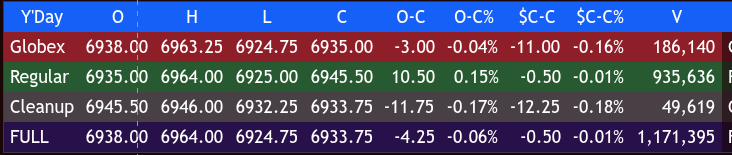

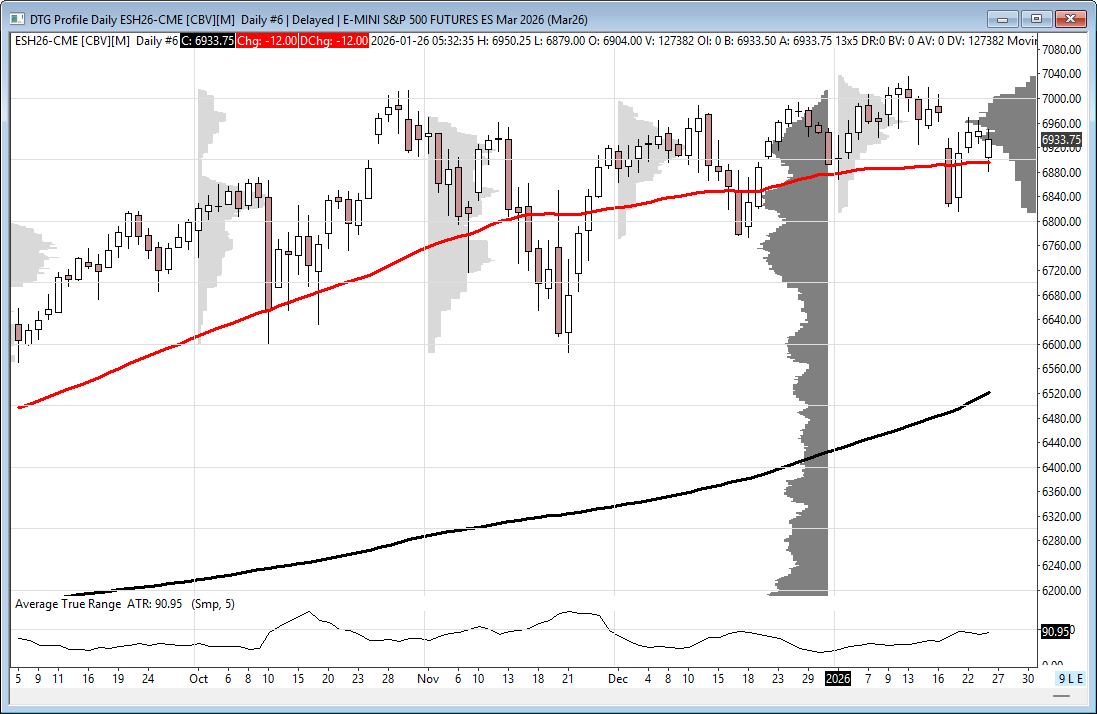

The ES traded up to 6964.00 on Globex and opened Friday’s regular session at 6938.00. After the open, the ES reached 6964.00 again mid-morning, with minor intraday peaks around 6963.25–6960.50, and then sold off down to the daily low at 6924.75. There were brief extensions during midday weakness and choppy rotations, followed by a rally back up to the 6940–6945 area through the afternoon in a low-volume chop with back-and-forth swings.

The ES held steady into the late session without significant late-day volatility and traded 6948.00 as the 3:50 cash imbalance showed $600 million to sell. It closed at 6945.50 on the 4:00 cash close, up +0.50 points or +0.01%.

After 4:00, the ES pulled back slightly to 6933.75 and settled at 6945.75, up 0.75 points or +0.01%.

-

NQH settled at 25,738.25, up +80.00 points or +0.31%

-

The YM settled at 49,263.00, down -295 points or -0.60%

-

The RTYH26 settled at 2,679.60, down -59.20 points or -2.17% on the day

In the end, it was a low-conviction trading session with rallies that faded quickly and only small bounces. In terms of the ES’s overall tone, it couldn’t hold meaningful moves in either direction.

In terms of the ES’s overall trade, volume was lighter than recent averages at 1,172,240 contracts, the lowest volume in 8 sessions.

This Week’s Major U.S. Economic Reports, Earnings, and Fed Speak

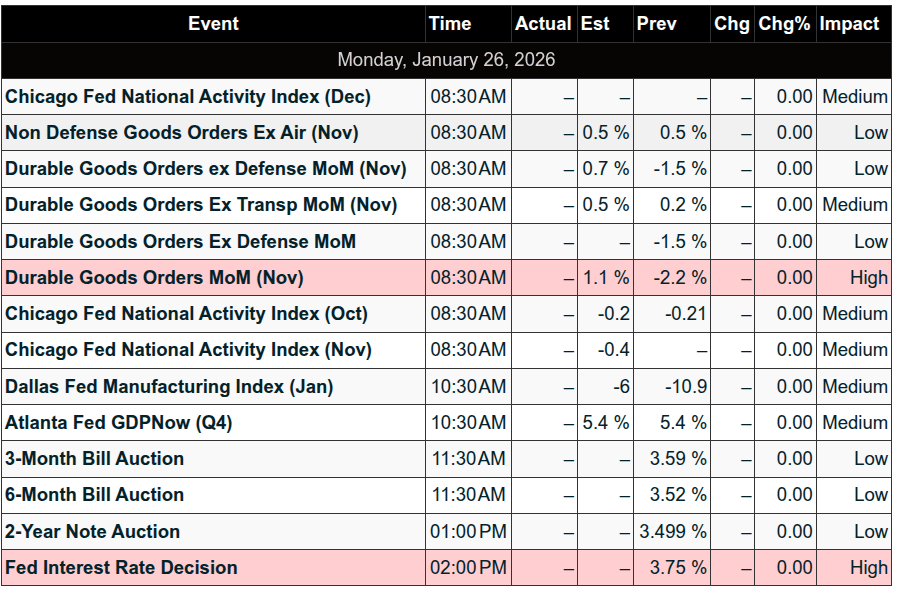

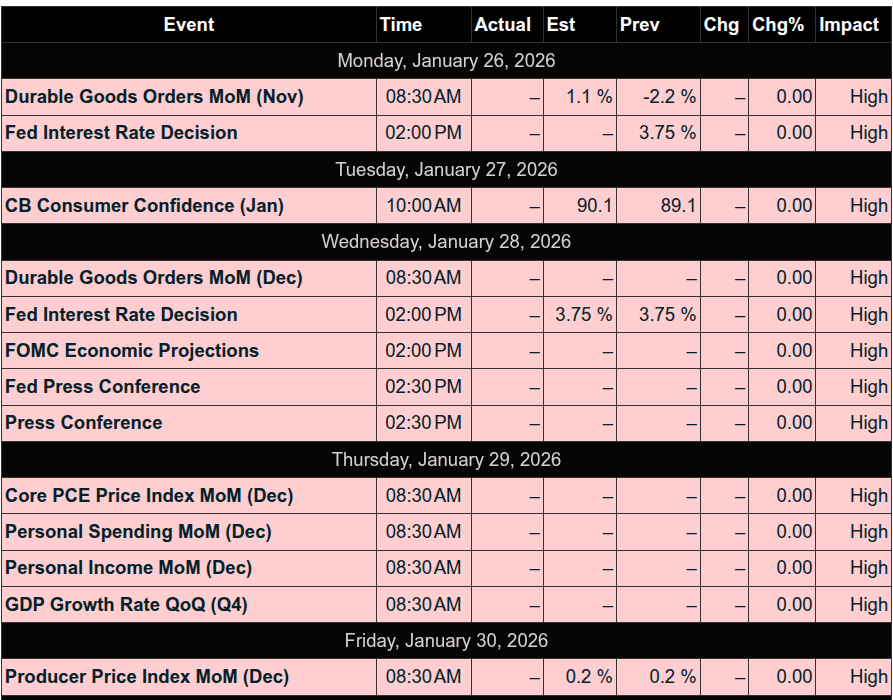

Monday, Jan. 26

-

8:30 am: Durable-goods orders (delayed report) – Nov.

-

8:30 am: Durable-goods minus transportation – Nov.

Tuesday, Jan. 27

-

10:00 am: Consumer Confidence – Jan.

Wednesday, Jan. 28

-

2:00 pm: FOMC interest-rate decision

-

2:30 pm: Fed Chair Powell press conference

-

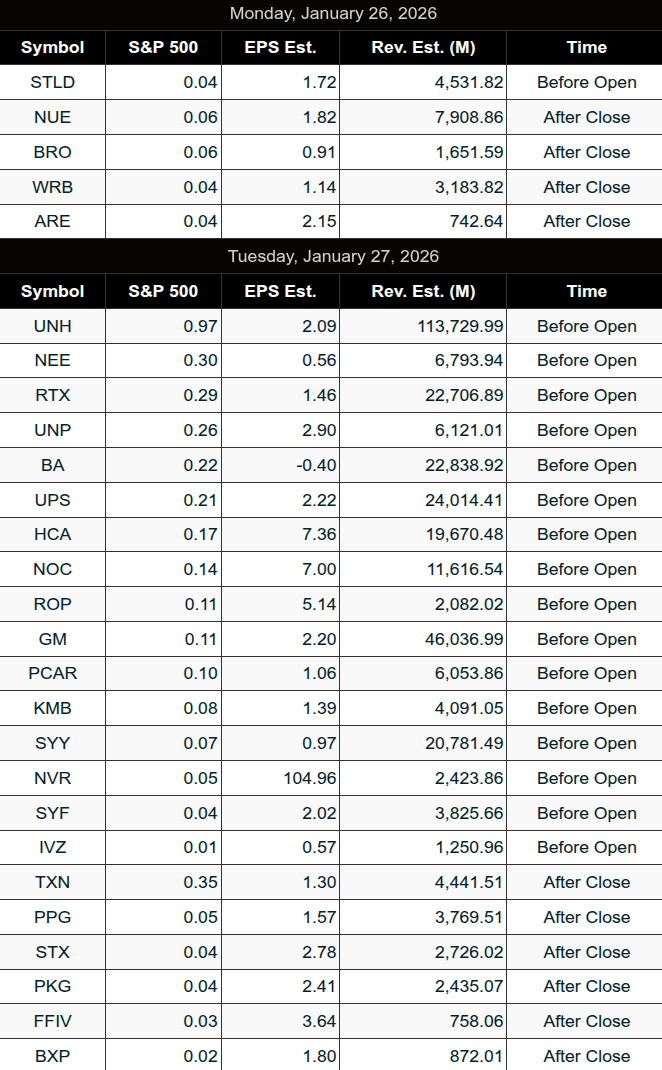

Tesla (TSLA), Meta (META), and Microsoft (MSFT) report earnings after the bell

Thursday, Jan. 29

-

8:30 am: Initial jobless claims – Jan. 24

-

8:30 am: U.S. trade deficit (delayed report) – Nov.

-

8:30 am: U.S. productivity (revised) – Q3

-

10:00 am: Wholesale inventories (delayed report) – Nov.

-

10:00 am: Factory orders (delayed report) – Nov.

-

Apple (AAPL) reports after the bell

Friday, Jan. 30

-

8:30 am: Producer Price Index (delayed report) – Dec.

-

9:45 am: Chicago Business Barometer (PMI) – Jan.

-

1:30 pm: St. Louis Fed President Alberto Musalem speaks

-

5:00 pm: Fed Vice Chair for Supervision Michelle Bowman speaks

Needless to say, this week is packed with major economic reports, the Fed’s two-day meeting, a long list of high-profile earnings reports, and continued headline risk. According to FactSet, a total of 103 S&P companies are reporting earnings this week.

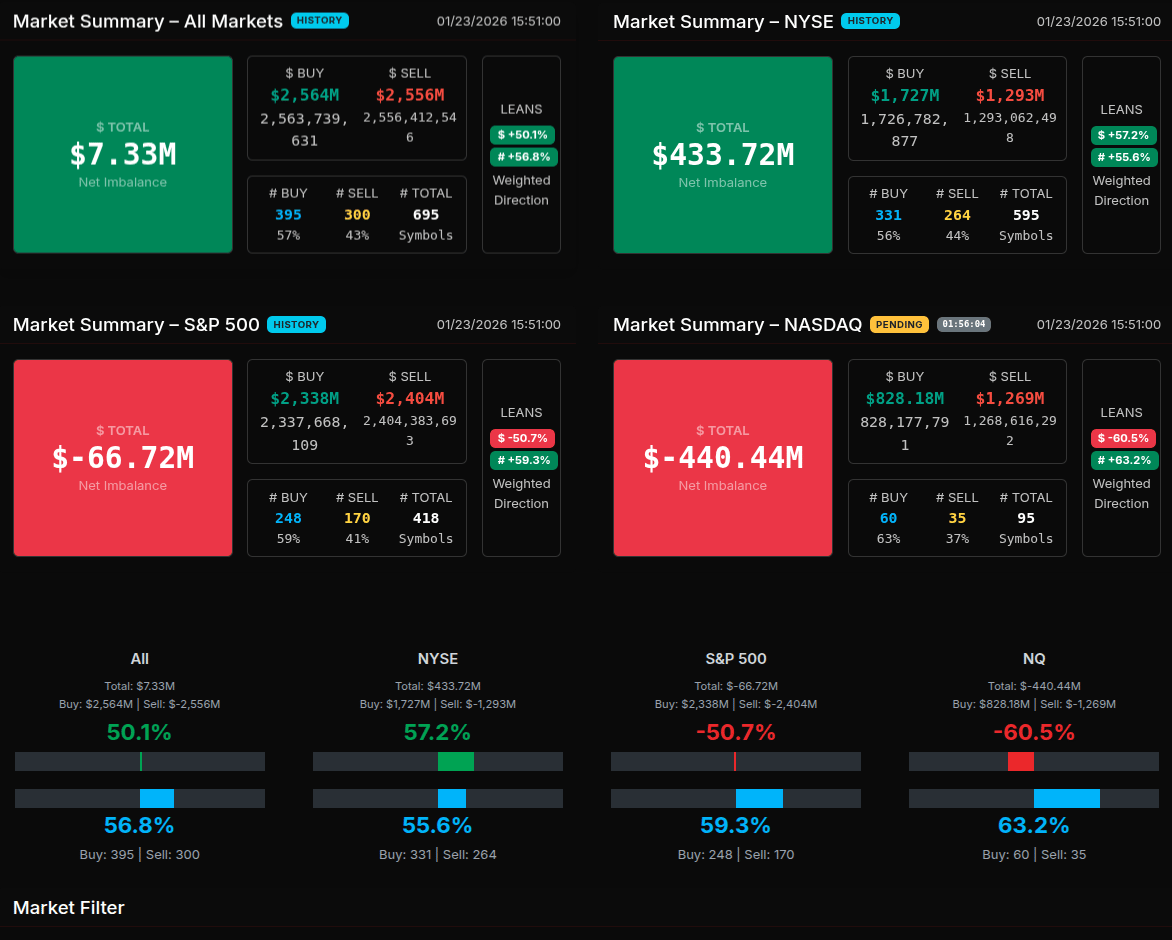

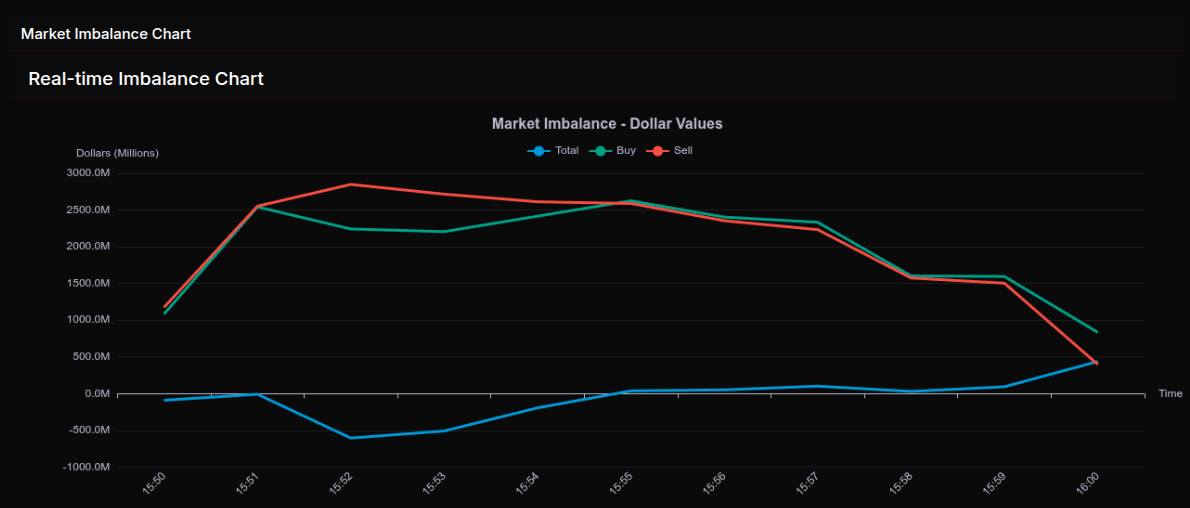

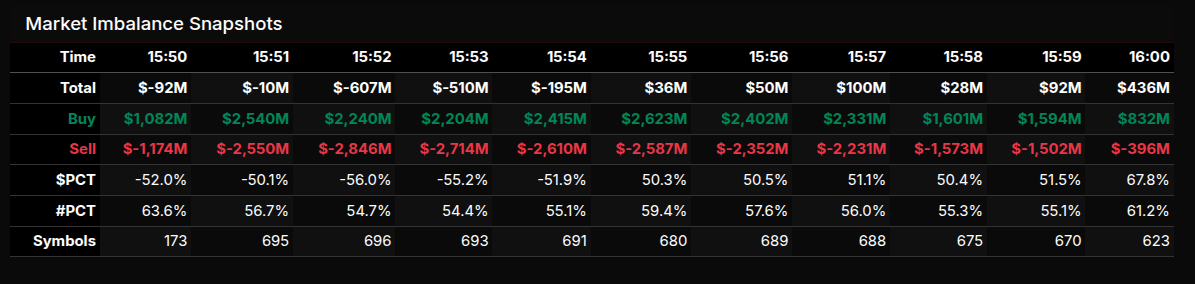

MiM

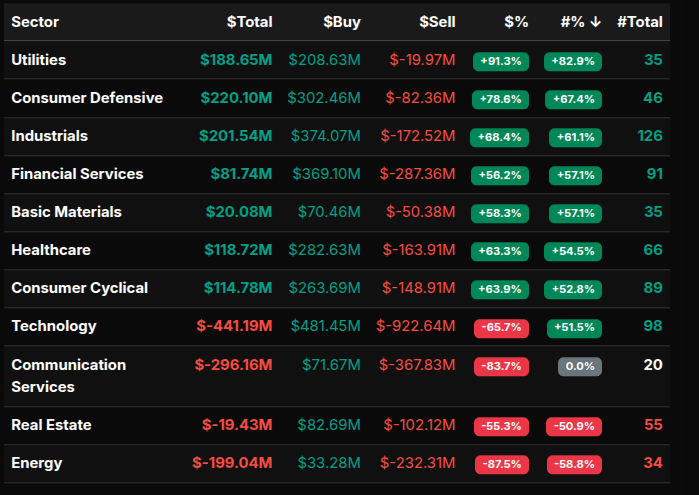

The market-on-close auction developed in clear phases, beginning with broad sell pressure before flipping to a late buy imbalance that tightened into the 4:00 cash close. Early snapshots between 15:50 and 15:54 showed persistent sell dominance, with total imbalances reaching as much as -$607M and sell percentages holding above -50%, signaling institutional distribution rather than rotation. By 15:55, the tone shifted decisively. Buy dollars overtook sell flow, and the net imbalance moved positive, culminating in a +$436M print at 16:00 with a +67.8% buy skew — a clear wholesale-style bid into the close.

Sector flows reinforced this transition. Defensive areas led on the buy side, with Utilities (+91.3%), Consumer Defensive (+78.6%), and Industrials (+68.4%) all showing strong positive skew, suggesting end-of-day risk balancing and allocation rather than speculative chasing. Healthcare and Consumer Cyclical also posted solid buy percentages in the low-to-mid 60s, consistent with rotation rather than panic covering. In contrast, Technology (-65.7%), Communication Services (-83.7%), and Energy (-87.5%) remained heavy sellers, marking these groups as sources of liquidity rather than destinations.

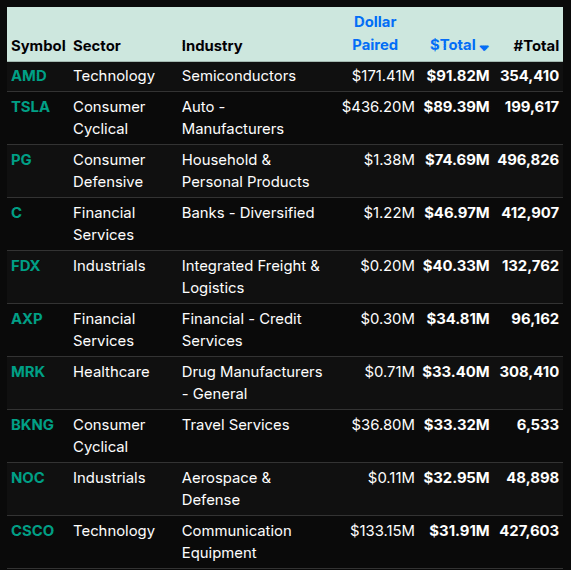

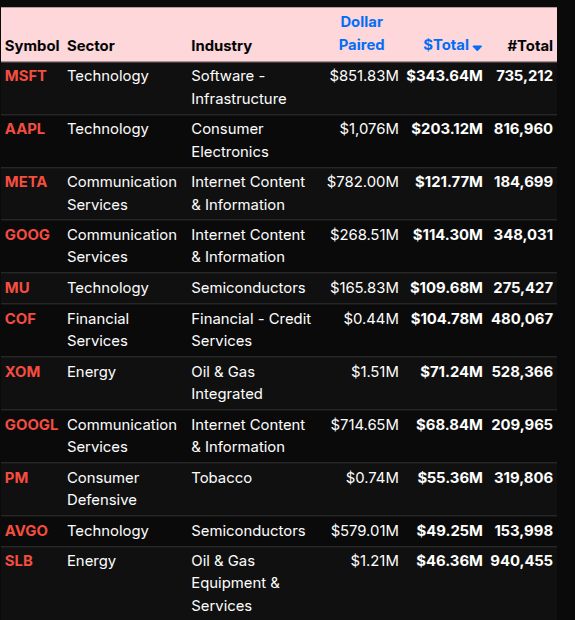

Single-name activity added clarity. On the sell side, mega-cap technology and communication names dominated dollar flow, including MSFT, AAPL, META, GOOG, and GOOGL, confirming that large-cap growth was used to fund broader reallocation. Semiconductor names showed mixed behavior, with MU and AVGO attracting buys while AMD still printed meaningful sell-side flow. Energy selling was concentrated in XOM and SLB, aligning with the sector-level weakness.

Index-level summaries reflected this split. NYSE finished with a strong +$433.7M imbalance and a +57.2% lean, while the S&P 500 (-$66.7M) and NASDAQ (-$440.4M) closed with negative totals and sell-side skews near or beyond the -50% threshold. Overall, the auction was less about risk-on enthusiasm and more about structured rotation — sellers in growth and energy funding defensive and industrial accumulation into the close.

Technical Edge

Fair Values for January 26, 2026

-

SP: 28.61

-

NQ: 123.17

-

Dow: 144.46

Daily Breadth Data 📊

For Friday, January 23, 2026

-

NYSE Breadth: 44% Upside Volume

-

Nasdaq Breadth: 48% Upside Volume

-

Total Breadth: 48% Upside Volume

-

NYSE Advance/Decline: 40% Advance

-

Nasdaq Advance/Decline: 40% Advance

-

Total Advance/Decline: 40% Advance

-

NYSE New Highs/New Lows: 173 / 21

-

Nasdaq New Highs/New Lows: 263 / 83

-

NYSE TRIN: 0.76

-

Nasdaq TRIN: 0.68

Weekly Breadth Data 📈

For Week Ending January 23, 2026

-

NYSE Breadth: 53% Upside Volume

-

Nasdaq Breadth: 55% Upside Volume

-

Total Breadth: 54% Upside Volume

-

NYSE Advance/Decline: 50% Advance

-

Nasdaq Advance/Decline: 51% Advance

-

Total Advance/Decline: 51% Advance

-

NYSE New Highs/New Lows: 437 / 76

-

Nasdaq New Highs/New Lows: 742 / 335

-

NYSE TRIN: 0.86

-

Nasdaq TRIN: 0.83

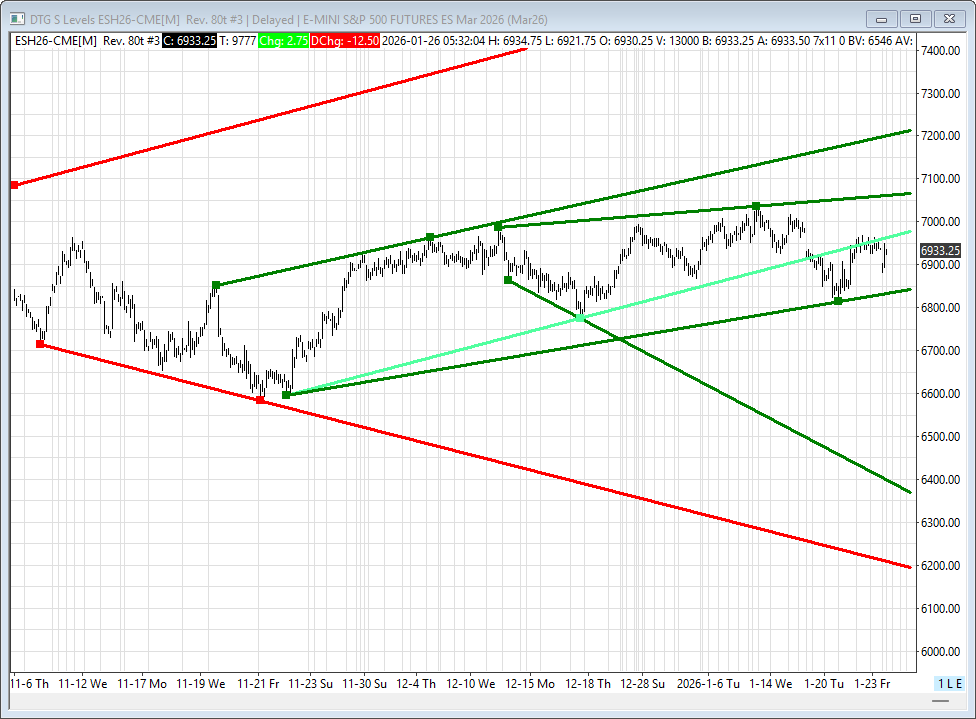

Today’s BTS Levels:

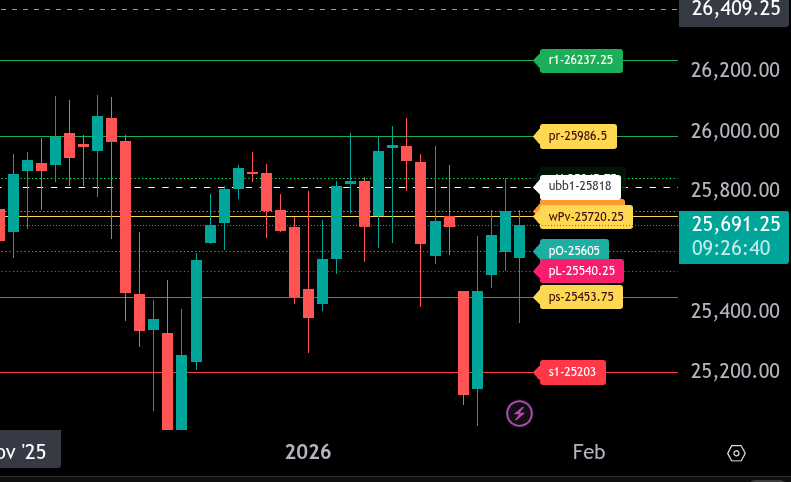

ES H

The bull/bear line for the ES is at 6945.25. This is the key pivot for today’s trade. Acceptance above this level keeps the tone constructive, while failure to hold keeps the market vulnerable to rotation lower.

ES is currently trading near 6939.75, just below the bull/bear line. This places the market in a neutral-to-bearish posture early, with chop likely unless 6945.25 is reclaimed and held.

Below the market, first support comes in at 6938.00, followed by 6931.50. A failure through these levels opens the door to 6924.75. If selling accelerates, the lower range target sits at 6887.25, with extreme downside risk toward 6832.75.

On the upside, a sustained move above 6945.25 targets 6964.00. Above that, the upper range target is 7003.25, where responsive selling is expected on the first test.

Overall, ES remains range-bound unless it can reclaim and hold above 6945.25. Strength above this level favors a rotation toward 6964.00 and potentially 7003.25. Failure to regain the bull/bear line keeps the risk skewed toward 6931.50 and 6924.75, with deeper downside possible if sellers gain momentum.

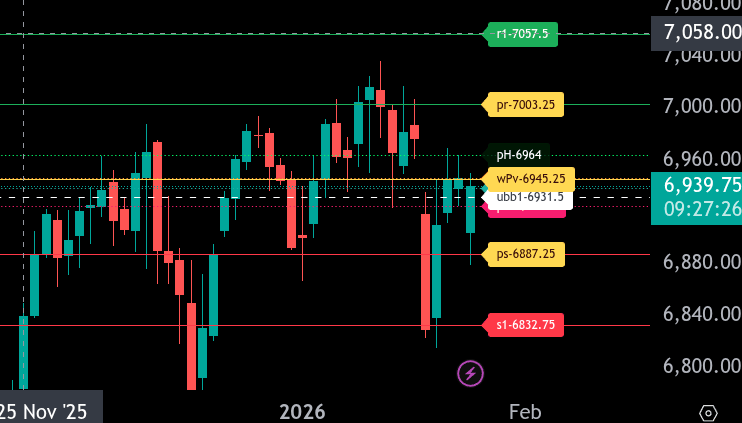

NQ H

The bull/bear line for the NQ is at 25,720.25. This is the key level that defines today’s bias. Acceptance above this level favors rotational upside attempts, while sustained trade below keeps pressure on the downside.

NQ is currently trading near 25,690, remaining below the bull/bear line and signaling short-term weakness. Failure to reclaim 25,720.25 keeps downside risk active, with immediate support at 25,605 and then 25,540.25. A break below 25,453.75 opens the door for a deeper liquidation toward 25,203.

On the upside, resistance begins at 25,738.25, followed by 25,845.75. If NQ can reclaim and hold above 25,720.25, buyers can press toward 25,986.50, with the reach target sitting at 26,237.25.

Overall, the tone remains bearish below 25,720.25. Bulls need a clean reclaim and acceptance above this level to shift momentum higher. Until then, rallies are vulnerable to rejection.

Calendars

Today’s Economic Calendar

This Week’s Important Economic Events

Upcoming Earnings – SP500

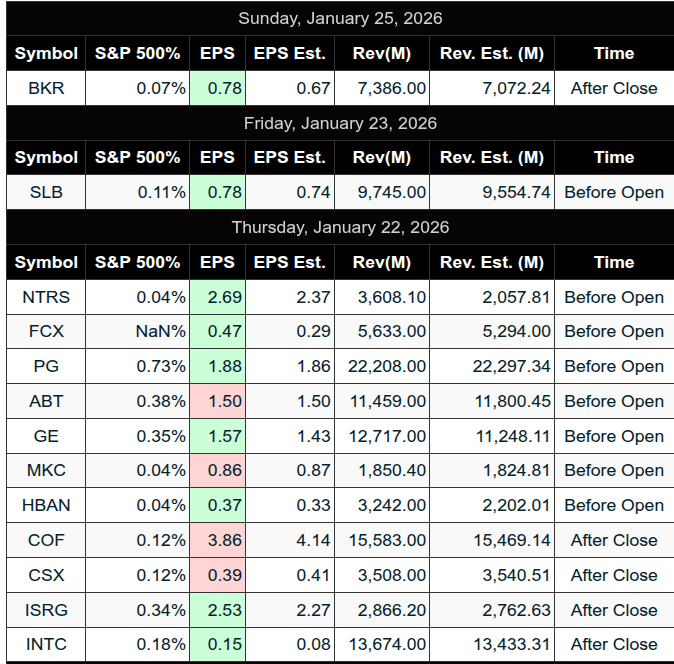

Recent Earnings

Room Summaries:

Polaris Trading Group Summary – Friday, January 23, 2026

Friday was structured around Cycle Day 2 (CD2) – often a “balancing/consolidation” day, and that played out as expected. ES traded largely within defined boundaries, with early fulfillment of key levels, followed by 2-way traffic and consolidation. Meanwhile, NQ led directional momentum, fulfilling multiple bullish targets and driving market sentiment.

Key Trade Highlights & Fulfilled Levels:

-

ES Initial Upside Target Zone (TZ) at 6965 was quickly fulfilled early in the session.

-

LIS (Line in Sand) for the session was 6945.

-

Price rotated lower into the Lower TZ: 6935–6915, with 6925 target also fulfilled.

-

6925 acted as strong support, defended by bulls, aligning with the day’s DTS Briefing.

-

Price action was contained within the “sandbox” range: 6925–6940, confirming consolidation tone.

-

A positive 3-day cycle target of 6958.85 was also hit, reflecting bullish control within the day’s range.

-

NQ was the star, fulfilling bullish cycle targets up to 25775 and the Money Box Zone.

-

Notably, a “monster rejection” from DLMB Zone on NQ provided a powerful reversal opportunity – a highlight for the day.

Lessons & Insights:

-

DTS Briefing provided excellent guidance, particularly around key support/resistance levels (6925 / 6965).

-

David highlighted that Volume Point of Control (POC) near highs indicates bullish acceptance rather than rejection—market seeking fair value at higher levels.

-

There was a good Q&A around strategy independence (A4 vs. A10 signals), helping members understand trade signal logic and how to handle overlapping strategies.

-

Distribution vs. Accumulation was clarified: these are clearer in hindsight, but volume structure offered clues for interpreting ongoing balance vs. initiative activity.

End of Day Wrap-Up:

-

David confirmed Cycle Targets were fulfilled, with the day completing as a “Normal” CD2.

-

A notable $600M MOC Sell Imbalance was logged late in the session.

-

Weather updates rolled in — with David expecting 18–24 inches of snow in Connecticut, closing out with some humor and camaraderie.

DTG Room Preview – Monday, January 26, 2026

MARKET & MACRO SUMMARY

Equities

• S&P 500 closed lower again last week, down ~0.4%, extending recent pressure ahead of this week’s key catalysts.

• Futures are softer this morning, with major indices sliding about 0.3–0.4% ahead of the Fed decision and Big Tech earnings.

• Volatility contracted last week as the bull breakout failed to materialize; ES 50‑day is acting as support, while former up‑channel resistance remains near-term upside resistance.

Federal Reserve & Policy

• The January FOMC meeting is live this week, and markets almost fully price no rate change.

• Attention remains on Trump’s choice for the next Fed Chair once Powell’s term ends — Rick Rieder has surged as the leading candidate in betting markets.

Geopolitical Shocks & Bonds

• Geopolitical concerns — Iran, Venezuela, Greenland/Europe tensions — are feeding broader risk aversion and underpinning safe‑haven flows.

• Declining dollar trends and weaker demand for US debt are supportive for non‑rate assets.

PRECIOUS & INDUSTRIAL COMMODITIES – RUNNING HOT

Gold & Silver

• Gold just hit fresh record highs above $5,100/oz on strong safe‑haven demand and dollar weakness.

• Silver continues parabolic gains above $100/oz and is up ~50%+ YTD.

• Metals rally framed as fear gauge tied to policy uncertainty, tariff risks, and central bank positioning.

Industrial Metals

• Strong demand backdrop remains for copper, lithium, and other base metals as AI data center build‑outs and electrification demand persist.

Energy & Natural Gas

• Natural gas saw extraordinary moves as Winter Storm impacts linger, with supply volatility and outages reported across the US.

Policy Support for Miners

• US government planning capital injections and financing for strategic rare earth/mineral producers — boosting related equities pre‑market.

EARNINGS & SCHEDULE HIGHLIGHTS

This Week’s Key Reports

Premarket

• Ryanair, Steel Dynamics, Nucor, BRO, WRB.

Tuesday

• Boeing, GM, UPS, UnitedHealth, HCA, Kimberly‑Clark, NextEra, Northrop Grumman, PACCAR, RTX, Sysco, Synchrony.

Big Tech Focus

• Microsoft, Meta, Tesla, Apple all reporting this week — earnings and commentary on AI capex & ROI will be central.

TECHNICAL MARKET STRUCTURE (ES)

Resistance Levels

• ~6963–65s (former up‑channel)

• ~7062–67s

• ~7213–18s

Support Levels

• ~6833–36s

• ~6386–81s

• ~6192–87s

Trend is balanced; break above resistance broadens upside, while downside follow‑through opens deeper support zones.

WEEK AHEAD ECONOMIC CALENDAR

• Durable Goods @ 8:30 ET (today).

• Fed decision & press.

• Multiple major earnings and macro data releases.

Key Themes for Traders This Week:

• Nasdaq & S&P direction hinges on Fed guidance + Big Tech narratives

• Precious metals remain in fear‑driven uptrend

• A weaker USD and geopolitical uncertainty are broad market tailwinds

• Rate pause likely — no cuts priced until later in 2026

Affiliate Disclosure: This newsletter may contain affiliate links, which means we may earn a commission if you click through and make a purchase. This comes at no additional cost to you and helps us continue providing valuable content. We only recommend products or services we genuinely believe in. Thank you for your support!

Disclaimer: Charts and analysis are for discussion and education purposes only. I am not a financial advisor, do not give financial advice and am not recommending the buying or selling of any security.

Remember: Not all setups will trigger. Not all setups will be profitable. Not all setups should be taken. These are simply the setups that I have put together for years on my own and what I watch as part of my own “game plan” coming into each day. Good luck!

This post goes out as an email to our subscribers every day and is posted for free here around 2 PM ET. To get your real-time copy, sign up for the free or premium version here: Opening Print Subscribe.

Comments are closed