This post goes out as an email to our subscribers every day and is posted for free here around 2 PM ET. To get your real-time copy, sign up for the free or premium version here: Opening Print Subscribe.

Too Many Hands on the Wheel, but the ES Still Knows Which Way Is Up

Follow @MrTopStep on Twitter and please share if you find our work valuable!

FREE Two-Week Offer for the Opening Print Premium. Open up the Lean and other premium features for the next Two Weeks!

Our View

I’ve thought a lot about this over the last few days, life has become much more complex in the past few years. Post-2020 surveys have shown that over 65% of decisions are now harder than they were two years ago. This is largely due to more stakeholders being involved—now averaging 11–13 people per major decision, up from 6–7 a decade ago.

This has been amplified by VUCA (volatility, uncertainty, complexity, and ambiguity) conditions like pandemics, geopolitical tension, AI disruption, supply chain issues, as well as information overload from data and AI tools, which are causing analysis paralysis and delays. The result is longer decision cycles, more conflicting views, higher cognitive load, and general inefficiencies—especially in high-stakes decisions in business, finance, and trading. Routine decisions, by contrast, remain relatively simple.

The trend, driven by digitization and globalization, isn’t reversing. Experts suggest adapting with agile mindsets, leveraging AI assistance, focusing on experimentation, and reducing noise.

In trading contexts—such as yen volatility or equity futures—this complexity reflects the same increased macro and policy noise that’s making positioning more difficult. Yes, I used AI to help answer my question, but what I’ve noticed in people around me is that even a simple task that should take seconds or minutes can now drag on for days or weeks.

Personally, I try to knock things off my list as fast as possible. But I’ll admit, when I don’t, the decisions tend to linger. When I did the AI study, it confirmed what I already suspected: the post-2020 period—specifically the March 2020 COVID pandemic—was a major turning point, both financially and mentally.

Our View

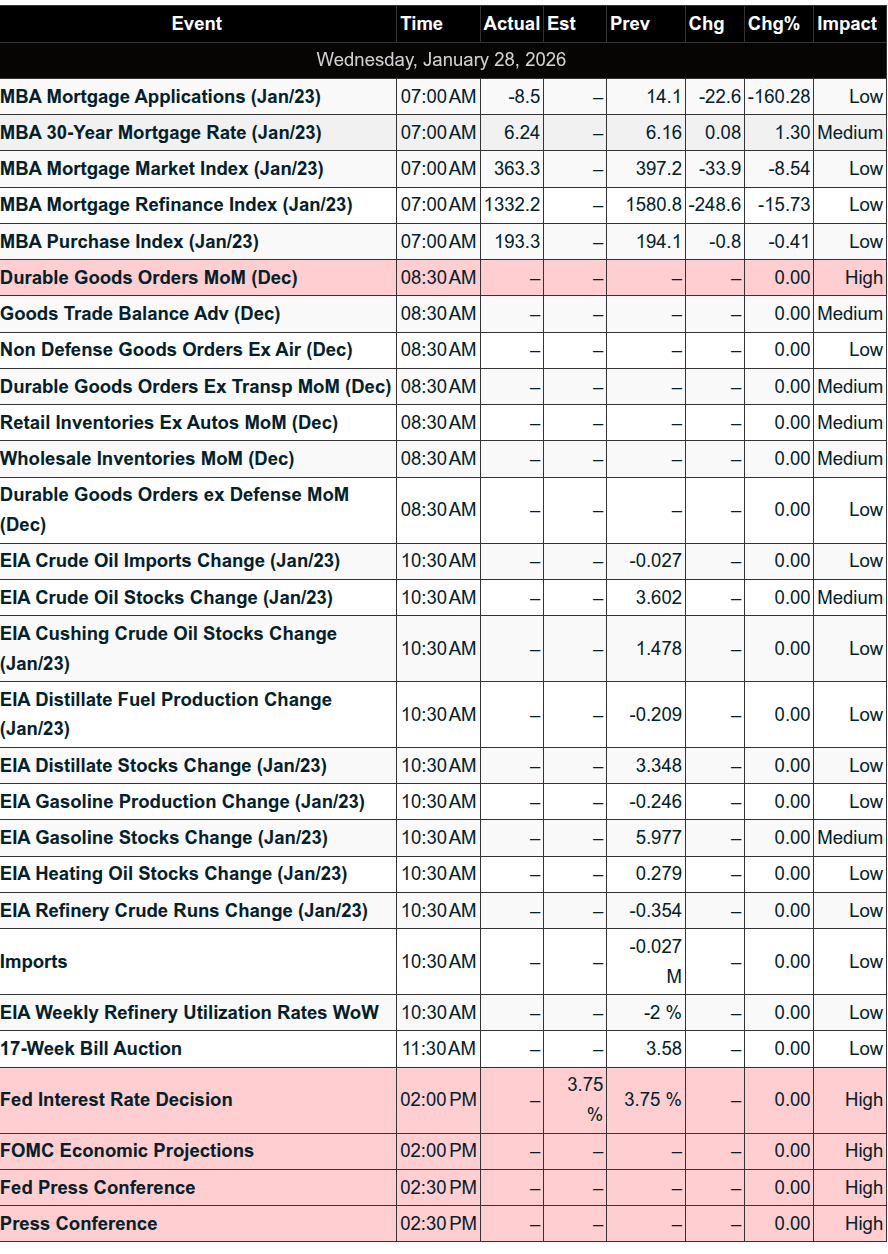

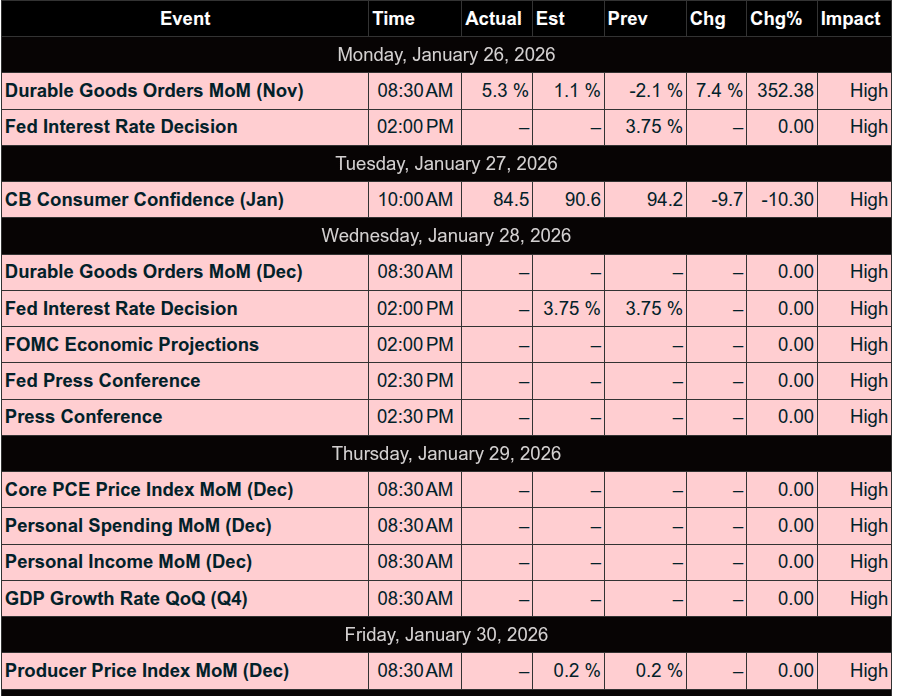

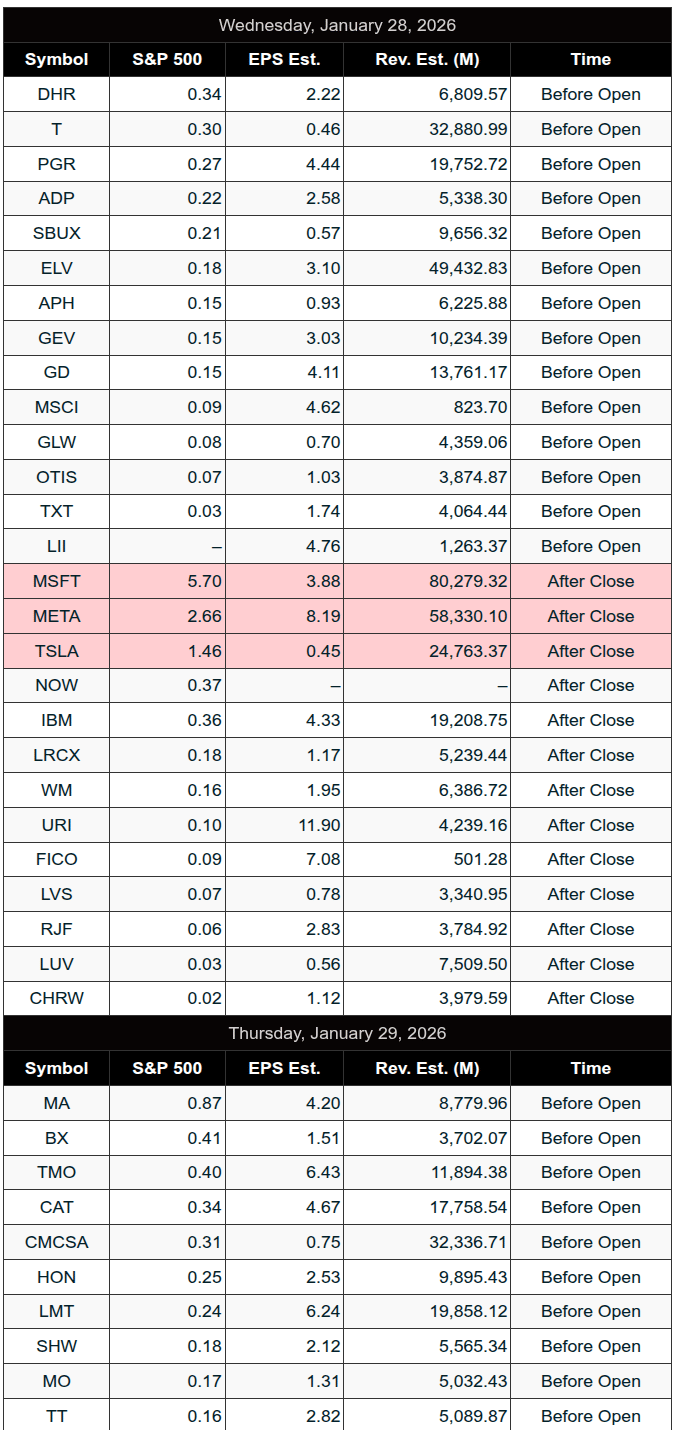

There are no economic releases today, but it is day two of the Fed’s two-day meeting, with META, TSLA, and MSFT reporting after the close.

In most instances when the ES sells off late in the day, it rallies on Globex. But the potential kicker today may be a rally in the European markets following India’s PM Modi announcing a landmark India-EU Free Trade Agreement. Finalized after nearly 20 years, it’s being called the “mother of all deals”—covering 2 billion people and 25% of global GDP, slashing tariffs on 96% of goods.

I’ve talked before about how important U.S.–India relations are as a counterbalance to China and Russian aggression. But Trump failed to cut a deal and is now threatening higher tariffs. I know some will disagree, but I don’t think this trade deal helps the U.S. Instead, it serves as a strategic hedge against U.S. protectionism—boosting EU exports like cars and wine, while opening markets for Indian textiles and jewelry.

Our Lean — Danny’s Trade (Premium only)

Market Recap

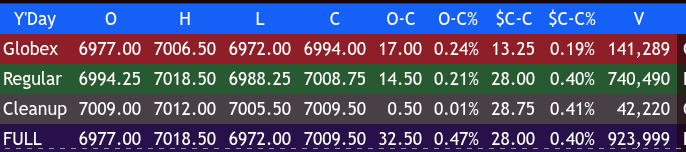

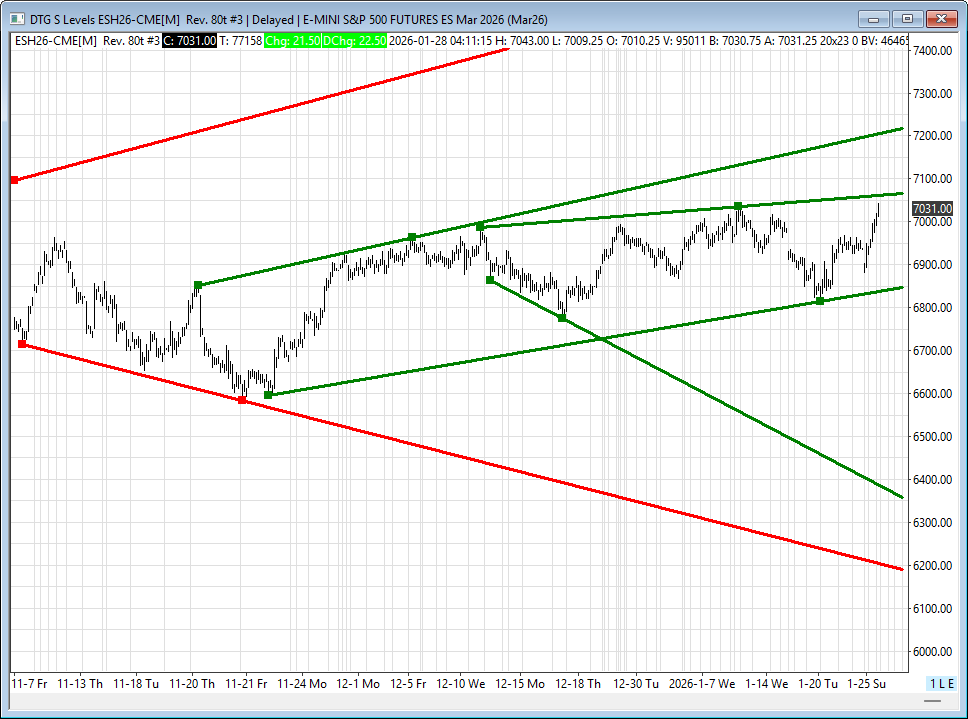

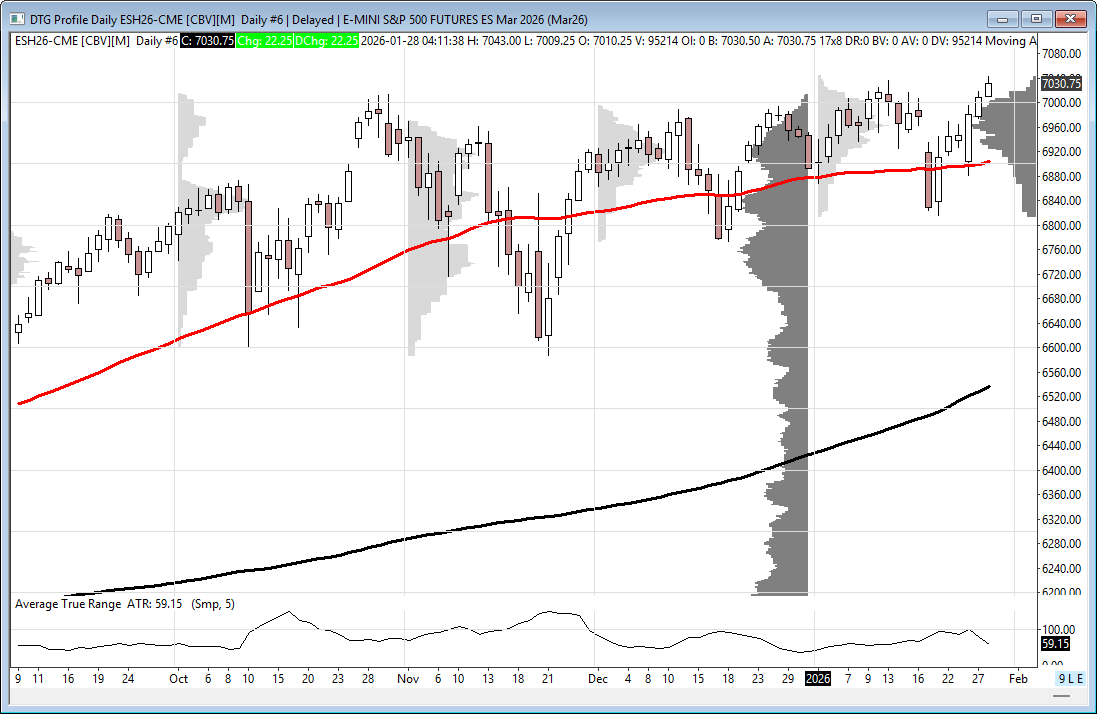

The ES traded up to 7006.50 on Globex with a total of 140k contracts traded and opened Monday’s regular session at 6994.25, up 13.5 points or +0.19%.

After the open, the ES and NQ did the exact same thing they did on yesterday’s gap-up—they sold off. The ES traded down to 6988.50, then took out the Globex high and traded up to 7007.75 at 10:01. It pulled back to 6998.00 and then rallied up to 7018.75 at 11:45.

That’s when I posted this:

IMPRO:Dboy:[11:46:17 AM]: 7020 + pr minus a few

The ES then sold off down to 7002.00 at 1:05. After the pullback, the ES traded up to a lower high at 7015.25 at 1:55.

At 2:08, I saw that the total ES volume was only 565k. When you take out the 140k from Globex, the total volume during the day session was only 425k, which was creating a very “thin to win” type trade.

The ES traded back down to 7011.25 and then up to 7014.25 as the 3:50 imbalance showed $3 billion to sell. It traded 7008.75 on the 4:00 cash close. After 4:00, the ES traded down to 7005.25 and settled at 7008.50, up 27.50 points or +0.39%, and has now been up five sessions in a row, up 179 points or +2.6% total.

The NQ settled at 26,073.00, up 224 points or +0.57%, also up five sessions in a row for a total gain of 943.75 points or +3.21%.

The YM settled at 49,159, down 406 points or -0.82%, but up three of the last five sessions for a total gain of 465 points or +1.01%.

The RTY settled at 2,677.60, up 6.7 points or +0.25%, also up three of the last five sessions for a total gain of 18.90 points or +0.67%.

In the end, it was exactly what I posted in the recap—it was a low-volume, “thin to win” type trade. In terms of the ES’s overall tone, every dip, whether it was 5 points or 10 points, was bought. In terms of the ES’s overall trade, volume was very low with only 925k contracts traded.

I tried to look up the last time ES volume was this low outside a holiday week or for a full session, and all I can say is this: 925k ES volume is exceptionally rare. I get it—the ES and NQ are coming off a five-day rally, and I understand the “thin to win” concept. But I think it’s more than that.

It feels like there’s no place to go in the U.S. stock market right now, while all eyes are on the weakness in the U.S. dollar and record highs in gold and silver. The dollar (DXY) was down another 0.85%, for a total loss of -3.23% over 5 of the last 6 sessions.

On Tap Today

-

2:00 pm: FOMC interest-rate decision

-

2:30 pm: Fed Chair Powell press conference

-

Earnings after the bell: Tesla (TSLA), Meta (META), and Microsoft (MSFT)

Guest Posts

Transition from Cycle Day 1 → Cycle Day 2

🚨 FED DAY PREVIEW —

“All Hat, No Cattle… or Is It?”

Ah yes.

Fed Day.

The market’s favorite episode of America’s Next Top Interest Rate.

Today’s main event isn’t about what the Fed does —

because spoiler alert: rates are staying put.

No one’s cutting.

No one’s hiking.

The rate button is bolted to the floor.

👉 This is a PRESSER DAY.

And that’s where the fun begins.

🎤 Jerome Powell: Professional Vibe Curator

Powell’s job today is simple (and impossible):

-

Sound confident without sounding cocky

-

Sound cautious without sounding terrified

-

Say “data dependent” 47 times without blinking

🎯 Cycle Day 2 Focus — Scenarios in Play

🟢 Bull Case (Buyers Stay in Control)

-

Hold north of 7010 ± 5

-

Upside objectives:

7025 → 7030 → 7035

Momentum remains constructive as long as acceptance holds above the pivot zone.

🔴 Bear Case (Rotation / Reset)

-

Hold south of 7010 ± 5

-

Downside objectives:

6995 → 6985 → 6975

Failure to reclaim the pivot opens the door for a controlled reset.

— PTG

From Jeff Hirsch Stock Trader’s Almanac

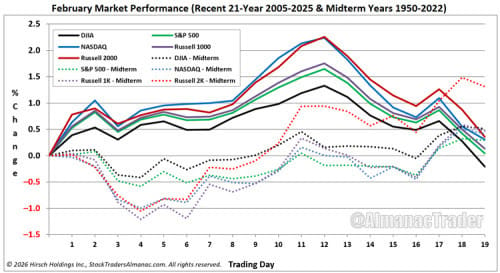

February has opened strongly but then reverses after President’s Day

February’s first trading day has been bullish for DJIA, S&P 500, NASDAQ, Russell 1000 and 2000. Average gains on the first day over the most recent 21-year period (solid lines in above chart) range from 0.39% by DJIA to 0.78% by Russell 2000. However, after a strong opening day, positive momentum has tended to stall out until around the seventh or eighth trading days. From there until around the 12-trading day all five indexes have historically enjoyed gains. But those gains have not held with the indexes beginning to decline after Presidents’ Day through the end of February.

Midterm-year February performance (dotted lines in above chart) has taken a different trajectory with weakness typically prevailing until around the sixth trading day, but afterwards the major indexes have demonstrated strength through the end of February with some consolidation around monthly options expiration and/or Presidents’ Day holiday.

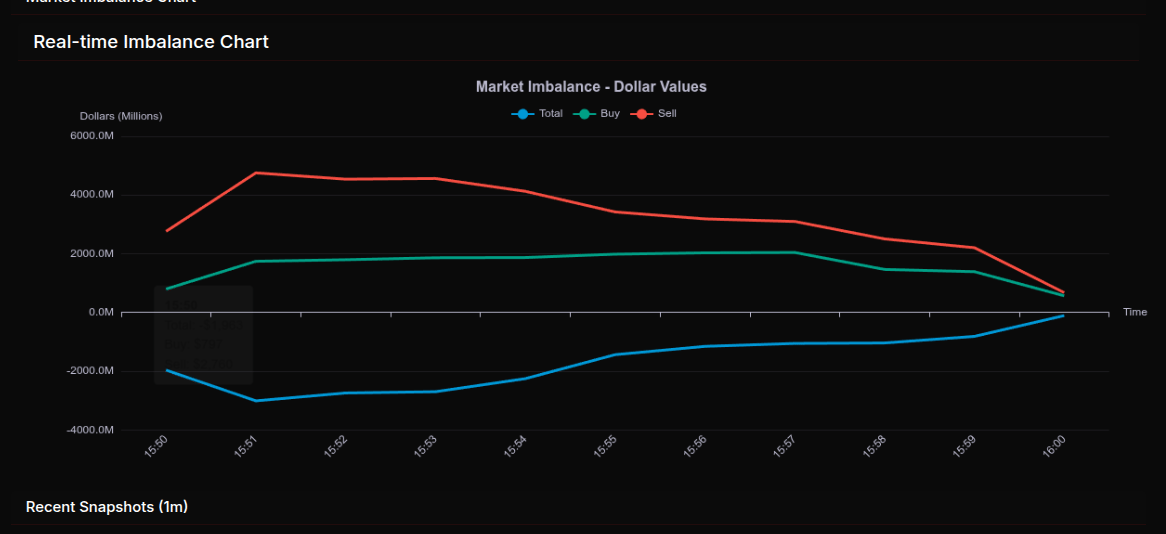

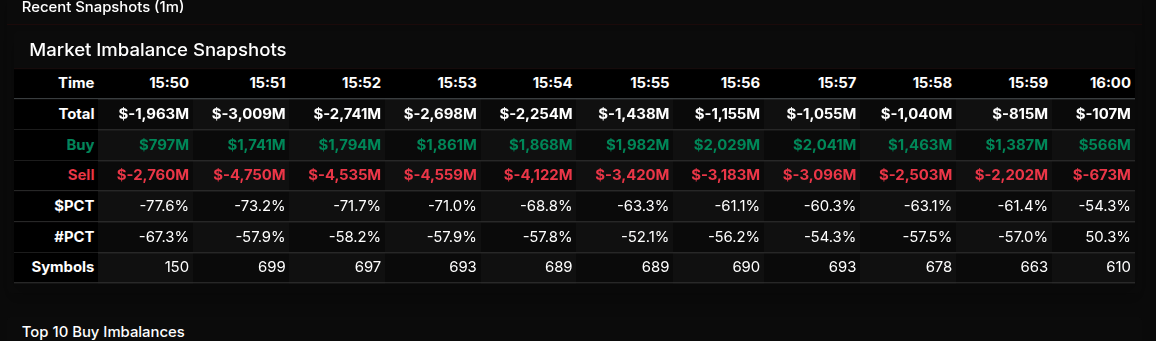

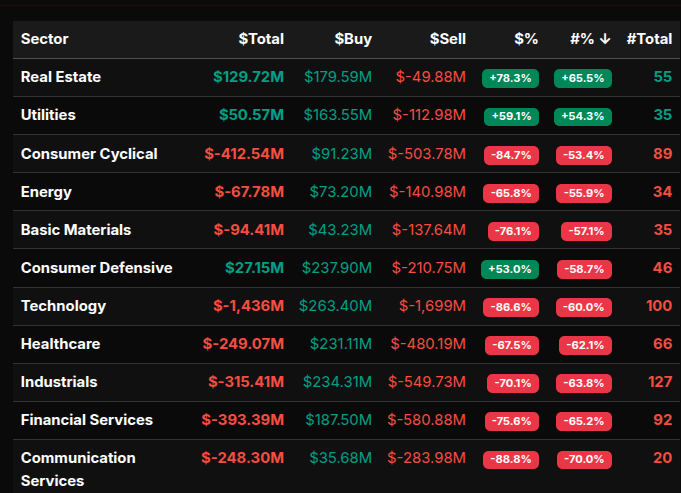

MOC Recap

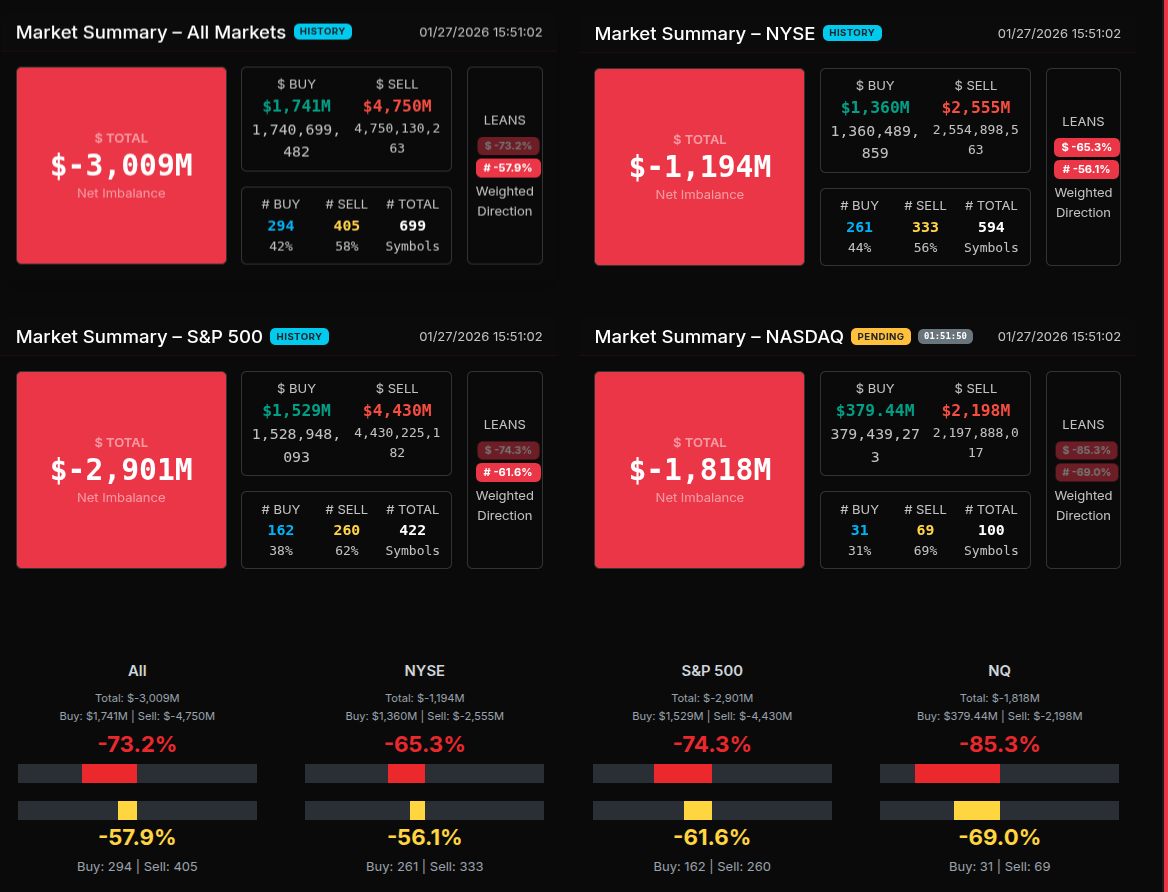

The Market-on-Close auction opened with a heavy sell imbalance and remained decisively one-sided through most of the window. Early snapshots showed total imbalances near –$3.0B, driven by persistent sell programs that peaked just after 15:51, when sell volume surged above $4.7B while buy interest struggled to keep pace. From that point forward, the imbalance steadily moderated, but the market never meaningfully flipped, finishing with residual sell pressure into the close.

Sector behavior made the tone clear. Technology was the dominant source of supply, posting a net imbalance near –$1.44B with a lean well beyond –66%, marking a wholesale liquidation rather than rotation. Consumer Cyclical, Financial Services, Industrials, Communication Services, and Healthcare all registered sell leans between –67% and –89%, confirming broad institutional distribution. These were not subtle reallocations — they were programmatic sells across growth, cyclicals, and defensives alike.

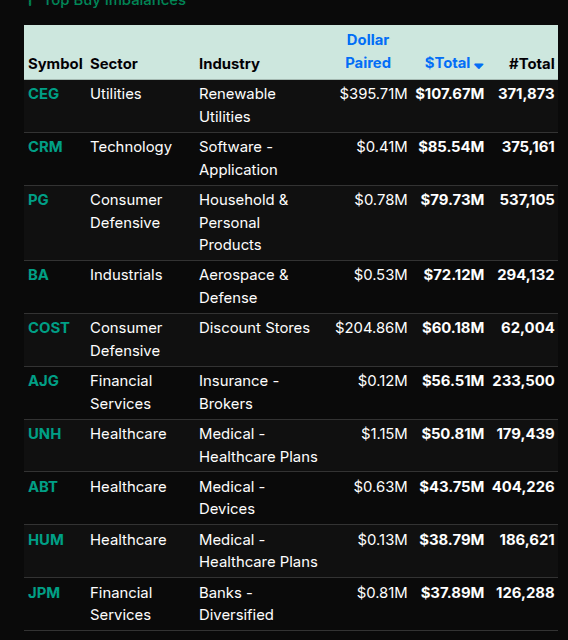

Notably, Utilities and Real Estate stood out on the buy side. Real Estate posted a +78% lean and Utilities nearly +60%, both comfortably above the +66% threshold that signals more directional buying rather than simple sector rotation. Consumer Defensive also showed positive dollar flow, but with mixed participation, suggesting selective buying rather than aggressive accumulation.

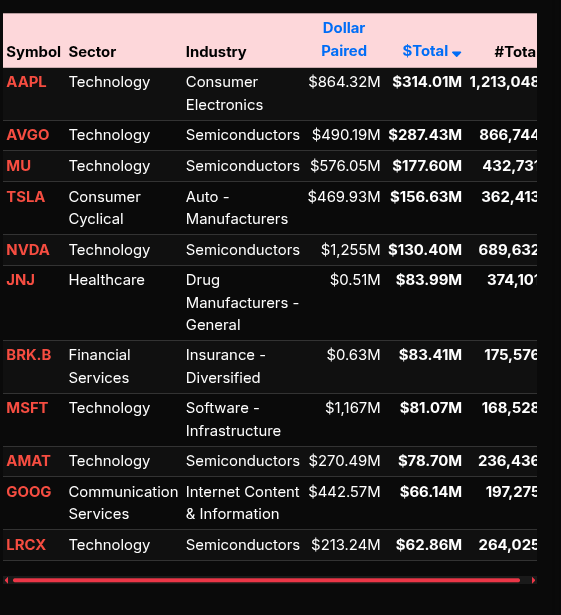

At the single-stock level, sell pressure was concentrated in mega-cap technology and high-beta leaders. AAPL, NVDA, MSFT, AVGO, MU, and TSLA all appeared among the largest dollar-weighted sell imbalances, reinforcing the broader Technology sector unwind. On the buy side, Utilities and Defensive names dominated, including CEG, PG, COST, and select Healthcare and Financial stocks, consistent with late-day risk reduction rather than dip-buying.

Into the final minutes, the imbalance compressed sharply as sell programs tapered and buy flow increased, pulling the net closer to flat by 16:00. Still, the structure of the auction points to a distributional close, with defensive allocation and risk-off positioning driving the tape rather than opportunistic rotation.

Technical Edge

Fair Values for January 28, 2026:

-

SP: 28.51

-

NQ: 123.86

-

Dow: 139.81

Daily Market Recap 📊

For Tuesday, January 27, 2026

• NYSE Breadth: 57% Upside Volume

• Nasdaq Breadth: 69% Upside Volume

• Total Breadth: 67% Upside Volume

• NYSE Advance/Decline: 55% Advance

• Nasdaq Advance/Decline: 57% Advance

• Total Advance/Decline: 49% Advance

• NYSE New Highs/New Lows: 219 / 51

• Nasdaq New Highs/New Lows: 339 / 149

• NYSE TRIN: 0.82

• Nasdaq TRIN: 0.59

Weekly Market 📈

For the week ending Friday, January 23, 2026

• NYSE Breadth: 53% Upside Volume

• Nasdaq Breadth: 55% Upside Volume

• Total Breadth: 54% Upside Volume

• NYSE Advance/Decline: 50% Advance

• Nasdaq Advance/Decline: 51% Advance

• Total Advance/Decline: 51% Advance

• NYSE New Highs/New Lows: 437 / 76

• Nasdaq New Highs/New Lows: 742 / 335

• NYSE TRIN: 0.86

• Nasdaq TRIN: 0.83

ES & NQ Futures trading levels (Premium only)

Trading Room Summaries

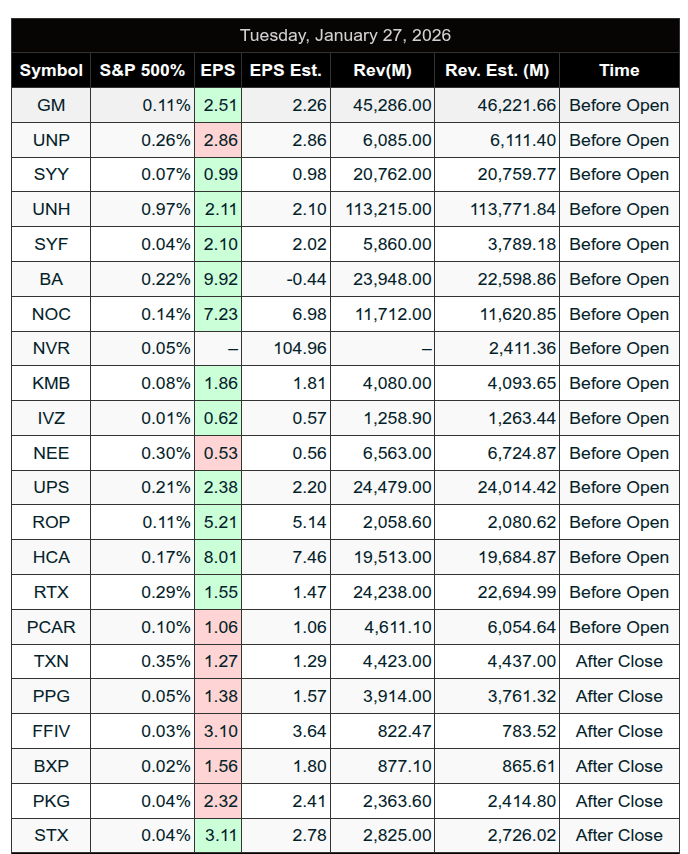

Polaris Trading Group Summary – Tuesday, January 27, 2026

Tuesday marked Cycle Day 1, and the PTG trading room executed the session with discipline and precision. PTGDavid laid out a clear bullish roadmap in the morning briefing, and the market followed through cleanly. Key levels in both ES and NQ were respected, and multiple targets were fulfilled. Traders capitalized on a well-structured long setup in ES, while educational discussions throughout the session added meaningful insights.

Key Highlights & Positive Trades:

-

Pre-Market Planning:

David outlined a bullish scenario based on holding above the 6970 support level in ES. He provided clear upside targets at 6995, 7010, and 7015, with potential continuation toward the 7020–7030 zone. -

ES Trade – Liquidity Break & Fail (LB&F) Setup:

Price briefly swept below 6995 but failed to accelerate lower, then quickly reclaimed the level. This confirmed the LB&F setup and triggered a strong long trade. All outlined targets were met, including the final 7015 level. -

NQ Trades – Target Fulfillment:

NQ fulfilled its projected upside targets of 25987 and 26075. These targets were based on holding above the 25835–level, which the market respected early in the session. -

Cycle Day 1 Confirmation:

There was brief confusion early in the session, but it was clarified that Tuesday was indeed Cycle Day 1. This helped frame expectations for potential range expansion. -

Educational Discussion – Strategy Conflicts:

David discussed the challenge of managing conflicting signals (e.g., A10 short setups versus long pullbacks). He explained it using the analogy of managing a diversified portfolio, encouraging traders to think in broader terms about strategy alignment. -

Compliance & Risk Management:

The group shared a valuable discussion on the risks of holding both long and short positions simultaneously in funded accounts. Several traders referenced examples of violations and account losses, reinforcing the need for strict rule adherence.

Market Conditions:

-

Strong Morning Momentum:

The early session followed through on the bullish thesis. Buyers stepped in on early pullbacks, and the market advanced steadily, hitting each of the projected resistance levels. -

Midday Slowdown:

Momentum faded into the afternoon. David noted a potential pullback developing before stepping away for lunch. The market quieted notably after the morning’s directional move. -

Closing Imbalance:

A $3 billion MOC sell imbalance hit the tape near the close — the second consecutive day of large for-sale imbalances. David remarked that the market was likely signaling something beneath the surface, hinting at potential institutional repositioning.

Lessons Learned:

-

A strong pre-market plan provides structure and confidence when levels hold.

-

The LB&F setup offered a textbook reversal opportunity once the trap under 6995 failed.

-

Managing strategy conflict requires mental flexibility and risk awareness.

-

Traders must understand and respect the rules of funded accounts to avoid violations.

-

Large closing imbalances can offer clues about broader market intent beyond intraday moves.

Discovery Trading Group Room Preview – Wednesday, January 28, 2026

-

Macro Focus:

-

Fed Day: The January FOMC decision is scheduled for today at 2:00pm ET.

-

No rate change expected after three cuts in 2025.

-

Key focus will be on Powell’s tone at 2:30pm ET — markets are looking for signals on how long rates may stay elevated.

-

Fed speakers, including Esther George, suggest the Fed is likely to hold steady for some time, evaluating “meeting by meeting.”

-

Rate cuts remain data-dependent, particularly on inflation trends.

-

-

AI Trade Leading Market Sentiment:

-

ASML: Blew out Q4 expectations with $15.8B in bookings (vs. $8.15B est.); shares +7.5% overnight, up 41% YTD.

-

ASML now valued over $500B and is the sole producer of advanced lithography equipment.

-

SK Hynix: Doubled profits (+137%) on strong AI-driven memory demand; shares +9% premarket on earnings beat and share cancellation news.

-

ASML holds 61% of the high-bandwidth memory (HBM) market.

-

-

China Precious Metals Frenzy:

-

Gold surges to a record $5,300, Silver is up 60% YTD.

-

Chinese investor demand has surged amid a weakening USD and local pricing premiums from a 13% VAT.

-

Tensions flare at the Shenzhen Jiewo Rui platform over withdrawal issues, with some users clashing with police.

-

Trump downplays concerns about the weakening dollar, contributing to overnight USD softness.

-

-

S&P Futures (ES) – Technical Levels:

-

ES futures hit new all-time highs overnight, testing trendline resistance at 7062/67s.

-

Resistance above: 7213/18s.

-

Key supports: 6840/45s, 6360/55s, 6183/78s.

-

Volatility continues to contract with bullish momentum intact.

-

-

Earnings Calendar:

-

Premarket Today: Amphenol (APH), ASML, AT&T (T), ADP, CGI Group (GIB), Corning (GLW), GE Vernova (GEV), General Dynamics (GD), MSCI, OTIS, Starbucks (SBUX), Progressive (PGR), United Microelectronics (UMC), and more.

-

After the Bell: Meta (META), Microsoft (MSFT), Tesla (TSLA), IBM, Southwest Airlines (LUV), Waste Management (WM), and others.

-

Tomorrow Morning: Caterpillar (CAT), Comcast (CMCSA), Dow (DOW), Honeywell (HON), Lockheed Martin (LMT), Mastercard (MA), SAP, Thermo Fisher (TMO), Valero (VLO), and more.

-

-

Economic Data:

-

Light calendar today.

-

Weekly Crude Oil Inventories data due at 10:30am ET.

-

Affiliate Disclosure: This newsletter may contain affiliate links, which means we may earn a commission if you click through and make a purchase. This comes at no additional cost to you and helps us continue providing valuable content. We only recommend products or services we genuinely believe in. Thank you for your support!

Disclaimer: Charts and analysis are for discussion and education purposes only. I am not a financial advisor, do not give financial advice and am not recommending the buying or selling of any security.

Remember: Not all setups will trigger. Not all setups will be profitable. Not all setups should be taken. These are simply the setups that I have put together for years on my own and what I watch as part of my own “game plan” coming into each day. Good luck!

This post goes out as an email to our subscribers every day and is posted for free here around 2 PM ET. To get your real-time copy, sign up for the free or premium version here: Opening Print Subscribe.

Comments are closed