TODAY’S GAME PLAN: from the trading

desk, this is not research

DATA/HEADLINES 8:15ET ADP Employment Change; 8:30ET Initial Jobless Claims; 9:45ET S&P Global US Services PMI

TODAY’S HIGHLIGHTS and News:

-

Mark Zuckerberg sold nearly half a billion dollars of Meta shares in the last two months

-

A caravan of 15,000 people are en route to the US border

Global shares edged higher after suffering their biggest rout to start a year since 1999, as data from China helped equity markets shake off their New Year blues.

China’s Caixin Services PMI came in at 52.9 versus 51.6 expected. There was a large upward revision to both the euro area services and composite PMIs but the survey period was based on just nine days of data due to the Christmas holiday. Both German and French

inflation surveys showed prices moving up again. European inflation data and the monthly US jobs report tomorrow will provide more information about whether central banks have room to start lowering interest rates. Geopolitics is also in focus amid fears the

war against Hamas could morph into a wider regional conflict. Bloomberg sources said US and its allies are considering possible military strikes against Houthis.

EQUITIES:

Yesterday’s ISM showed that the grand total of 5.6% of purchasing managers are experiencing any growth. The lowest since April 2009.

US equity futures fluctuated after stumbling in the first two sessions of 2024 as investors awaited fresh clues on the timing of possible interest-rate cuts. A growing number of firms

are bracing their clients for near-term stock declines following a blockbuster two-month rally. Traders are turning their attention to key employment data on Friday for signs on the health of the economy. Apple fell overnight, poised to extend losses for

a fourth session after Piper Sandler cut its rating to neutral from overweight on concerns about iPhone inventory levels. AbbVie is lower after CVS said it’s replacing the drugmaker’s blockbuster Humira with cheaper copycats in its commercial prescription

plans.

Futures ahead of the bell: E-Mini S&P -0.03%, Nasdaq -0.3%, Russell 2000 -0.1%, Dow +0.2%.

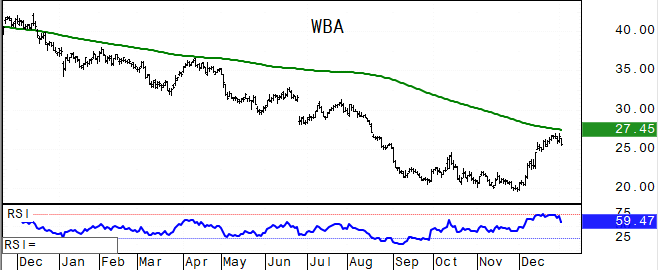

In pre-market trading, Mobileye Global shares were diving 28% after the autonomous-driving systems company said it expects a 50% fall in revenue in the first quarter of the year. Walgreens

(WBA) climbed as much as 4.7% after an earnings beat. The company also almost halved its quarterly dividend. Home Depot (HD) rises 1.4% and Dollar General (DG) gains 1.8% as both companies are upgraded to overweight from equal-weight at Barclays. Illumina

(ILMN) slips 2% on a Cowen downgrade. Mattel (MAT) falls 2.6% after Roth MKM cuts its recommendation on the toymaker to neutral from buy

European gauges are trading slightly higher with energy and banks leading gains, outweighing losses in technology and retail shares. French inflation edged higher in December as service

prices grew more quickly. In corporate news, Next rallied after the British home and clothing retailer raised its profit forecast. JD Sports Fashion tumbled 23% after the British sportswear retailer slashed its profit forecast, weighing on Adidas AG and Puma

SE. Stoxx +0.2%, DAX +0.1%, CAC +0.2%, FTSE 100 +0.2%. Energy +1.3%, Banks +1%. Technology -1%, Retail -0.9%.

Shares in Asia were mixed. The MSCI Asia Pacific Index gained 0.2%, with Toyota, Takeda and Daiichi Sankyo giving the biggest boosts. Japan’s Topix Index closed higher on its first trading

day of the year. India’s stock benchmark traded close to a record high as energy and bank shares advanced. Shares in China fell for a third consecutive session amid a lack of enthusiasm for Beijing’s efforts to spur the economy. Philippines +1.6%, Indonesia

+1.1%, Sensex +0.7%, Vietnam +0.6%, Topix 0.5%. ASX 200 +0.4%, Kospi -0.8%, Singapore -0.8%, CSI 300 -0.9%.

FIXED INCOME:

Treasuries are lower with the curve steeper, following bigger losses seen across core European rates. Bunds were pressured lower after German PMI numbers for December

were revised higher, and the latest state inflation numbers are higher than the earlier NRW release. US yields are cheaper by up to 6bp across long-end of the curve with 2s10s, 5s30s spreads steeper by 3bp and 1bp on the day; 10-year yields on session highs

leading into early US session, cheaper by 6bps at 3.98%.

METALS:

Gold inched higher, rising for the first time in five days as Federal Reserve policymakers pushed back against expectations for aggressive monetary easing early this

year. The focus is now on US data which will guide the pace of the Fed’s rate cuts. Spot gold +0.1%, silver is flat.

ENERGY:

Oil continued its surge as conflict in the Middle East added to supply concerns. Brent crude traded near $79 a barrel after supply disruptions in Libya and as Iran

said attacks that killed almost 100 people in the country were carried out to punish its stance against Israel. WTI +1%, Brent +0.7%, US Nat Gas +5.7%, RBOB +0.2%.

CURRENCIES:

In currency markets, the yen weakened on speculation that it’ll be harder for the Bank of Japan to abolish negative interest rates after a powerful earthquake hit

the country on New Year’s Day. The dollar edged lower against most Group-of-10 peers after a four-day gain, as traders mulled minutes from the Federal Reserve’s December meeting and awaited ADP payrolls. The euro rose after French inflation edged higher in

December. US% Index -0.1%, GBPUSD +0.2%, EURUSD +0.25%, USDJPY +0.7%, AUDUSD -0.2%, USDSEK -0.5%, USDCHF +0.2%.

Bitcoin +0.8%, Ethereum +0.5%.

TECHNICAL LEVELS:

|

ESH24 |

10 Year Yield |

Feb Gold |

Feb WTI |

Spot $ Index |

|

|

Resistance |

4900.00 |

5.250% |

2200.0 |

78.15 |

107.350 |

|

|

4873.00 |

5.000% |

2180.0 |

77.79 |

106.600 |

|

|

4841.50 |

4.600% |

2152.3 |

75.77 |

104.780 |

|

|

4803.50 |

4.350% |

2117.0 |

73.84 |

104.000 |

|

|

4780.00 |

4.030% |

2100.0 |

72.40 |

103.400 |

|

Settlement |

4746.50 |

2042.8 |

72.70 |

||

|

|

4740.00 |

3.840% |

2026.7 |

69.73 |

100.550 |

|

|

4717.00 |

3.640% |

2019.0 |

67.98 |

100.000 |

|

|

4688.00 |

3.245% |

1987.9 |

66.80 |

99.580 |

|

|

4647.00 |

3.000% |

1975.5 |

66.63 |

98.940 |

|

Support |

4594.00 |

2.700% |

1950.0 |

62.00 |

98.000 |

Colors within the report:

Green is always the 200 period (day, week).

Red is always 21,

Blue = 50,

Brown =

100 *Stars have added importance

- Upgrades

- Allstate (ALL) Raised to Overweight at Morgan Stanley; PT $171

- American Express (AXP) Raised to Overweight at JPMorgan; PT $205

- Armstrong World (AWI) Raised to Neutral at UBS

- Cognizant (CTSH) Raised to Peerperform at Wolfe

- Comerica (CMA) Raised to Buy at Goldman; PT $70.50

- Con Edison (ED) Raised to Sector Weight at KeyBanc

- Dollar General (DG) Raised to Overweight at Barclays; PT $154

- Emerson Electric (EMR) Raised to Buy at Mizuho Securities; PT $118

- Epam Systems (EPAM) Raised to Outperform at Wolfe; PT $355

- Ferguson (FERG) Raised to Overweight at Wells Fargo; PT $210

- Fox Corp (FOXA) Raised to Peerperform at Wolfe

- General Motors (GM) Raised to Outperform at Wolfe

- Home Depot (HD) Raised to Overweight at Barclays; PT $372

- Intercorp Finl (IFS) Raised to Outperform at Itau BBA; PT $26

- Merck & Co (MRK) Raised to Outperform at Cowen; PT $135

- Micron (MU) Raised to Overweight at Piper Sandler; PT $95

- Murphy USA (MUSA) Raised to Buy at Jefferies; PT $425

- Power of Canada (POW CN) Raised to Outperform at RBC; PT C$45

- Principal Financial (PFG) Raised to Inline at Evercore ISI

- PTC Inc. (PTC) Raised to Overweight at JPMorgan; PT $200

- Sprouts Farmers (SFM) Raised to Inline at Evercore ISI; PT $45

- Tal Education (TAL) ADRs Raised to Buy at BofA; PT $15.70

- Verizon (VZ) Raised to Outperform at Wolfe; PT $46

- Xylem (XYL) Raised to Market Perform at Raymond James

- Downgrades

- Aflac (AFL) Cut to Underperform at Evercore ISI

- Akoustis Technologies (AKTS) Cut to Neutral at Piper Sandler; PT $1

- American Express (AXP) Cut to Sell at DZ Bank; PT $157

- Ameriprise (AMP) Cut to Inline at Evercore ISI

- Apple (AAPL) Cut to Neutral at Piper Sandler; PT $205

- Autoliv (ALV) Cut to Peerperform at Wolfe

- Bath & Body Works (BBWI) Cut to Equal-Weight at Barclays; PT $45

- Bird Construction (BDT CN) Cut to Sector Perform at National Bank

- BJ’s Wholesale (BJ) Cut to Equal-Weight at Wells Fargo; PT $70

- Brunswick (BC) Cut to Market Perform at Raymond James

- Builders FirstSource (BLDR) Cut to Hold at Truist Secs

- Capital One (COF) Cut to Neutral at JPMorgan; PT $131

- Clarus (CLAR) Cut to Hold at Jefferies; PT $7

- CNO Financial (CNO) Cut to Underperform at Evercore ISI; PT $26

- Collegium (COLL) Cut to Hold at Jefferies; PT $37

- Enphase Energy (ENPH) Cut to Sector Weight at KeyBanc

- First Watch Restaurant (FWRG) Cut to Hold at Stifel; PT $20

- Five Below (FIVE) Cut to Equal-Weight at Wells Fargo; PT $215

- Floor & Decor (FND) Cut to Equal-Weight at Wells Fargo; PT $105

- Guess (GES) Cut to Hold at Jefferies; PT $24

- Illumina (ILMN) Cut to Market Perform at Cowen; PT $144

- Installed Building (IBP) Cut to Hold at Truist Secs

- Intact Financial (IFC CN) Cut to Sector Perform at RBC; PT C$228

- International Game (IGT) Cut to Hold at Jefferies; PT $29

- Itron (ITRI) Cut to Market Perform at Raymond James

- Macom (MTSI) Cut to Neutral at Piper Sandler; PT $85

- Mattel (MAT) Cut to Neutral at Roth MKM; PT $20

- Microchip (MCHP) Cut to Neutral at Piper Sandler; PT $80

- Mobileye (MBLY) Cut to Peerperform at Wolfe

- Northwestern (NWE) Cut to Sector Weight at KeyBanc

- Papa John’s (PZZA) Cut to Sell at Stifel; PT $65

- PayPal (PYPL) Cut to Market Perform at Oppenheimer

- Pfizer (PFE) Cut to Market Perform at Cowen; PT $32

- PulteGroup (PHM) Cut to Neutral at UBS

- Qorvo (QRVO) Cut to Neutral at Piper Sandler; PT $120

- RealReal (REAL) Cut to Neutral at Baird; PT $2.75

- Revolve Group (RVLV) Cut to Neutral at Baird; PT $17

- Cut to Hold at Jefferies; PT $17

- Rivian (RIVN) Cut to Peerperform at Wolfe

- Rocket Cos. (RKT) Cut to Underweight at JPMorgan; PT $10.50

- Roper (ROP) Cut to Market Perform at Cowen; PT $535

- Skyworks (SWKS) Cut to Neutral at Piper Sandler; PT $90

- SLM (SLM) Cut to Neutral at JPMorgan; PT $20

- Steven Madden (SHOO) Cut to Hold at Jefferies; PT $40

- SunPower (SPWR) Cut to Market Perform at Raymond James

- Sunrun (RUN) Cut to Sector Weight at KeyBanc

- TDCX (TDCX) ADRs Cut to Hold at HSBC; PT $6.60

- Telus (T CN) Cut to Neutral at JPMorgan; PT C$26

- Tenaris (TEN IM) ADRs Cut to Hold at Jefferies; PT $39.60

- TopBuild (BLD) Cut to Hold at Truist Secs

- UniFirst (UNF) Cut to Neutral at Baird; PT $185

- United Natural (UNFI) Cut to Underweight at Wells Fargo; PT $15

- Visteon (VC) Cut to Peerperform at Wolfe

- Western Union (WU) Cut to Underperform at Wolfe; PT $13

- YETI Holdings (YETI) Cut to Hold at Canaccord; PT $50

- Yum (YUM) Cut to Hold at Stifel; PT $135

- Initiations

- AN2 Therapeutics (ANTX) Rated New Market Outperform at JMP; PT $30

- Atex Resources Inc (ATX CN) Rated New Outperform at BMO; PT C$2

- Cadeler (CADLR NO) ADRs Rated New Buy at Stifel; PT $35

- CI&T Inc (CINT) Reinstated Hold at Canaccord; PT $5.50

- Eli Lilly (LLY) Reinstated Buy at William O’Neil

- FMC Corp (FMC) Rated New Buy at Roth MKM; PT $74

- Fortrea (FTRE) Rated New Buy at Jefferies; PT $44

- Immunome (IMNM) Rated New Outperform at Cowen

- Inovio (INO) Reinstated Market Outperform at JMP; PT $1

- Neurogene Inc (NGNE) Rated New Outperform at Cowen

- Revolution Medicines (RVMD) Rated New Outperform at Wedbush; PT $41

- Safehold Inc (SAFE) Rated New Buy at Jefferies; PT $33

- Synopsys (SNPS) Rated New Buy at President Capital Management; PT $618

- Tyler Tech (TYL) Reinstated Market Outperform at JMP; PT $490

- Xenon Pharmaceuticals (XENE) Rated New Buy at Citi; PT $62

Data sources: Bloomberg, Reuters, CQG

Comments are closed