TODAY’S GAME PLAN: from

the trading desk, this is not research

DATA/HEADLINES 9:45ET S&P Global US Services PMI; 10:00ET ISM Services Index; 2:00ET Fed’s Beige

Book

TODAY’S HIGHLIGHTS:

- Ben Shelton, 20, becomes the youngest American man to reach a U.S. Open semifinal since Andy Roddick in 2003.

- Tropical Storm Lee is expected to rapidly intensify into an ‘extremely dangerous’ hurricane in the Atlantic by this weekend

Global equities slipped as investors continued to focus on weakening growth prospects in Europe and Asia while tracking bets on a near-term rate hike in the resilient

U.S. economy. Japan issued its strongest warning in weeks against rapid declines in the yen, with its top currency official saying the nation is ready to take action amid speculative moves in the market. Elevated oil prices and weak economic data from Germany

reignited stagflation concerns across the euro area, causing European stocks to extend their slide. The dollar edged higher, while oil-linked currencies retreated as Brent crude slid. Treasury yields were little changed. Gold prices were steady, while Bitcoin

climbed for the first time in three days.

EQUITIES:

US equity-index futures fell on Wednesday as investors remained wary of higher bond yields as recently rising oil prices revived inflation concerns. Apple fell as

much as 0.8% premarket after WSJ reported that China ordered officials at central government agencies not to use iPhones and other foreign-branded devices for work or bring them into the office. Amazon slipped 0.6% premarket after WSJ reported the FTC plans

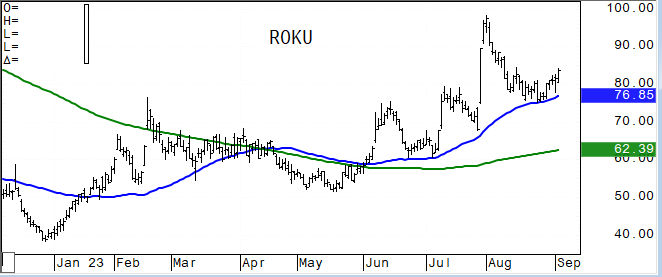

to file a lawsuit against Amazon later this month. Roku rose as much as 13% in premarket trading on Wednesday after the maker of set-top boxes consumers use to watch Netflix Inc. and other streaming services, announced plans to cut about 10% of its workforce.

AeroVironment shares rallied 14% after the drone maker boosted its revenue forecast for the full year. VFS US +2.3%, STZ US +1.0%, STM US +0.9%, DXCM US +0.7%, TOAST +4%.

Futures ahead of the bell: E-Mini S&P -0.2%, Nasdaq -0.2%, Russell 2000 -0.08%, Dow -0.2%.

European stocks declined for a sixth straight session as weak German data weighed on sentiment. German factory orders plummeted in July, another sign that the woes of Europe’s biggest economy continued

into the third quarter. The Stoxx 600 was down 0.6%, led by declines in the financial services, bank, insurance, and consumer products sectors. The FTSE 100 opened 0.9% lower as stocks lost for the third straight day. AstraZeneca Plc contributed the most to

the FTSE 100 decline, decreasing 1.7%. Intertek Group Plc had the largest drop, falling 2.4%. Telefonica shares rose 3.2 percent after Saudi Telecom Company (STC) acquired a 9.9 percent stake in the giant Spanish telecom company, at a value of 2.1 billion

euros ($2.25 billion), in a move that made it the largest shareholder. Stoxx 600 -0.7%, DAX -0.5%, CAC -0.8%, FTSE 100 -0.6%.

Stocks in Asia were little changed as Chinese equities declined amid caution over the impact of government stimulus, while shares in Japan advanced on a forex boost. The MSCI Asia Pacific Index fluctuated

in a narrow range, with Tencent and Samsung among the biggest drags while Toyota and Sony provided support. Japanese equities extended Asia’s best rally so far in 2023, even as the government warned over the sharp decline in the yen, which has bolstered gains

in shares of the nation’s exporters. Chinese property stocks surged, with market watchers pointing to speculative flows betting on more policy support for the struggling sector. Suppliers to Huawei extended gains on optimism over the technology company’s new

phone model. Meanwhile, Australian stocks fell while the Aussie dollar held onto a decline following second-quarter gross domestic product data that came in line with estimates. Toyota shares advanced as much as 2.1%, extending an intraday record. Orora declined

as much as 14%, the most since June 2020, after the packaging services company raised A$1.2 billion through a placement and institutional entitlement offer to fund a deal to buy bottlemaker Saverglass. Hang Seng Index -0.04%, Kospi -0.7%, ASX 200 -0.7%. Vietnam

+0.8%, Nikkei 225 +0.6%, Sensex +0.1%, Philippines +0.2%, Taiwan -0.3%.

FIXED INCOME:

Treasuries edged higher and held small gains, trimming yields from the highest levels in a week reached amid Tuesday’s corporate new-issue explosion and crude oil prices jumping

to YTD highs. Yields lower across the curve by 1bp-2bp, 10-year around 4.25%, down from session high near 4.27%. Focal points of US session include ISM services gauge at 10am New York time and comments by Boston Fed’s Collins at 8:30am.

METALS:

Gold prices steadied, following a 0.9% drop in the previous session. Investors are awaiting upcoming US data including a services gauge from the Institute For Supply Management, which

may steer the US central bank’s policy over the rest of the year. Gold was flat, silver -0.5%.

ENERGY:

Oil prices slipped on Wednesday as traders digested a decision by OPEC+ leaders Saudi Arabia and Russia to extend supply curbs through the end of the year. Russia

and Saudi Arabia surprised many investors by curtailing output through the end of the year, pushing oil prices to their highest levels of 2023.WTI -0.2%, Brent -0.4%, Nat Gas +0.7%.

CURRENCIES:

The US dollar index was little changed, while the yen pared an advance fueled by commentary from Japanese officials. Kanda said officials are seeing speculative moves in the yen and won’t rule out

any options if currency moves continue. AUD/USD gained 0.4% before paring most of the advance; Australia’s economy maintained its momentum in the three months through June as gross domestic product advanced 0.4%, official data showed Wednesday. EUR/USD edged

higher; ECB Governing Council member Klaas Knot, a hawk, said investors largely betting against an interest-rate increase next week are “maybe” underestimating the likelihood of it happening. Elsewhere, the yuan slipped to the weakest level in 10 months. US$

Index -0.1%, GBPUSD -0.07%, USDJPY +0.2%, EURUSD +0.1%, AUDUSD +0.1%, NZDUSD +0.1%, USDCAD -0.06%.

Bitcoin +0.03%, Ethereum +0.1%.

Colors within the report:

Green is always the 200 period (day, week).

Red is always 21,

Blue = 50,

Brown =

100 *Stars have added importance

UPGRADES:

- AeroVironment Inc (AVAV) raised to outperform at Baird; PT $128

- American Air (AAL) raised to outperform at BNPP Exane; PT $20

- Baytex Energy (BTE CN) raised to sector outperform at Peters & Co

- CME Group (CME) raised to neutral at BofA; PT $204

- Celanese (CE) raised to overweight at KeyBanc; PT $149

- Cenovus Energy (CVE CN) raised to sector outperform at Scotiabank

- Constellation Brands (STZ) raised to outperform at Cowen; PT $300

- First Solar (FSLR) raised to equal-weight at Morgan Stanley

- ResMed (RMD) raised to buy at Needham; PT $180

- Semtech (SMTC) raised to buy at Needham; PT $35

- Toast (TOST) raised to buy at UBS; PT $30

DOWNGRADES:

- Block Inc (SQ) cut to neutral at UBS; PT $65

- Enbridge (ENB CN) cut to equal-weight at Wells Fargo; PT C$50

- Enbridge (ENB CN) cut to sector perform at Peters & Co; PT C$50

- Enerflex (EFX CN) cut to sector perform at Peters & Co; PT C$12.50

- Kinetik (KNTK) cut to neutral at Citi; PT $34

- Kiwetinohk Energy (KEC CN) cut to sector perform at Peters & Co; PT C$18

- Olin (OLN) cut to neutral at Goldman; PT $57

- Plains All American (PAA) cut to neutral at Citi; PT $15.50

- Plains GP (PAGP) cut to neutral at Citi; PT $15.50

- Procaps Group (PROC) cut to hold at Brookline Capital; PT $4.50

- Southwest Air (LUV) cut to neutral at BNPP Exane; PT $34

- Stem Inc (STEM) cut to equal-weight at Morgan Stanley

INITIATIONS:

- Actinium (ATNM) rated new buy at HSBC; PT $11.60

- Amgen (AMGN) rated new buy at HSBC; PT $320

- Biogen (BIIB) rated new buy at HSBC; PT $360

- Bitdeer Technologies Group (BTDR) rated new buy at HC Wainwright

- Bluebird Bio (BLUE) rated new buy at HSBC; PT $4.21

- Denali Therapeutics (DNLI) rated new buy at B Riley; PT $38

- Fair Isaac (FICO) rated new outperform at Raymond James; PT $1,007

- Farmer Mac (AGM) rated new outperform at KBW; PT $220

- Gilead (GILD) rated new reduce at HSBC; PT $71

- Intapp (INTA) rated new overweight at Barclays; PT $43

- Iqvia (IQV) rated new buy at HSBC; PT $260

- J&J (JNJ) rated new hold at HSBC; PT $175

- Labcorp (LH) rated new hold at HSBC; PT $210

- LeMaitre Vascular (LMAT) reinstated outperform at Oppenheimer; PT $70

- LivaNova (LIVN) rated new hold at HSBC; PT $52

- Lucid (LCID) rated new neutral at Baird; PT $7

- Luckin Coffee ADRs (LKNCY) rated new buy at Sealand Securities

- Penumbra (PEN) rated new equal-weight at Morgan Stanley; PT $265

- Prime Medicine (PRME) rated new buy at JonesTrading; PT $20

- SLGG US (SLGG) rated new speculative buy at Taglich Brothers

- Silk Road Medical (SILK) rated new outperform at Oppenheimer; PT $30

- Thermo Fisher (TMO) resumed buy at Citi; PT $625

- Trade Desk (TTD) rated new outperform at William Blair

- Uber (UBER) rated new outperform at CICC; PT $53

- UnitedHealth (UNH) rated new hold at HSBC; PT $540

- Zoetis (ZTS) rated new buy at HSBC; PT $230

Data sources: Bloomberg, Reuters, CQG

No responses yet