TODAY’S GAME PLAN: from the trading

desk, this is not research

DATA/HEADLINES 10:00ET SEC’s Gensler testifies at Senate Banking Committee; 1:00ET 10 year note auction

TODAY’S HIGHLIGHTS:

- Quarter of Libyan city of Derna wiped out by burst dam, 1,000 bodies recovered

- DOJ begins antitrust trial against GOOGLE, the biggest antitrust case in 20 years

- Bill Gross blasts Jeffrey Gundlach’s investment record

- China says it is willing to deepen mutually beneficial cooperation with Russia

Global stocks held firm a day ahead of crucial US inflation data that could influence when or whether the Federal Reserve raises rates further. Britain’s labor market

showed more signs of cooling in the three months through July, data showed today, although pay growth hit another record high. Concern over China’s sputtering economy has created a “dramatic shift” in investors’ equity allocation — a rush toward the US and

an exodus from emerging markets, Bank of America’s latest global fund manager survey showed. Among the surveyed, a net zero percent expect stronger economic growth for the country in the near future, a massive reversal from 78% in February. Chinese real estate

is now seen as the number one source for the next global credit event.

EQUITIES:

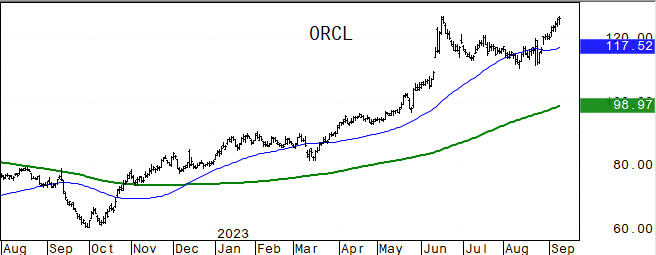

US equity futures are lower as technology stocks were in retreat as Oracle Corp. fell ~10% after posting slowing cloud sales, dimming enthusiasm about the sector. Tech stocks are set

to be the center of attention today, with Apple preparing to announce a new product lineup and SoftBank-owned chip designer Arm Ltd. gearing up for the biggest initial public offering of the year. Arm’s bankers plan to stop taking orders for its IPO today

as it’s already 10 times oversubscribed. Meanwhile, the first of two major DOJ cases against Google goes to trial today.

Futures ahead of the bell: E-Mini S&P -0.25%, Nasdaq -0.35%, Russell 2000 -0.2%, Dow -0.1%.

In premarket trading, Oracle plunged 10% with Morgan Stanley analysts saying the results raise questions about the timing of generative AI demand turning into revenue across the broader

business. Acelyrin (SLRN) sinks 58% after the biopharmaceutical company’s lead product did not meet the primary endpoint of a clinical trial. AngloGold Ashanti ADRs (AU +3%) are raised to outperform from market perform at BMO Capital Markets. Geron Corp. (GERN)

climbs 7% as Goldman Sachs raised its rating to buy from neutral. Humacyte (HUMA) jumps as much as 16% ahead of the biotech company’s announcement of its top-line data from a trial that evaluates its Human Acellular Vessel (HAV), used to treat traumatic vascular

injuries. MoonLake Immunotherapeutics (MLTX) shares rise 18% as analysts see Acelyrin’s izokibep setback as a boost for MoonLake’s sonelokimab.

European gauges are mixed as investors awaited key US inflation data on Wednesday. The Stoxx 600 Index was mostly flat, as defensive sectors including telecoms and healthcare outperformed

cyclicals such as technology and chemicals. Britain’s FTSE 100 outperformers on expectations that the jobs data will lead to a softer pound and make British stocks more attractive to investors overseas. UK wage growth held at a record high, a sign of persistent

inflation that will keep pressure on the Bank of England to raise interest rates again. Investor confidence in Germany’s economy improved for a second month, while lingering at a level that will do little to relieve concerns over the country’s status as Europe’s

growth laggard. The market is split on whether the ECB will deliver its final interest rate increase for the year this week. Among individual names, packaging company Smurfit Kappa Group plunged as much as 13% after it agreed on the terms of an $11 billion

merger with WestRock. Stoxx 600 -0.15%, DAX -0.6%, CAC -0.3%, FTSE 100 +0.35%. Retail +0.9%, Telecom +0.7%, Chemicals -1.25%, Technology -1.2%.

Stocks in Asia were mixed, with Japan and Taiwan closing higher while Chinese equities fell after swinging between gains and losses. China gauges continue to struggle as investors await

retail sales and factory data due Friday for possible signs of recovery in the economy. The MSCI Asia Pacific Index edged higher by 0.1%, with Toyota and TSMC among the biggest boosts. Hong Kong benchmarks dropped, though they narrowed losses following a report

that Country Garden got approval to extend repayment on some yuan bonds. Elsewhere in the region, South Korean shares fell amid losses in chip and EV battery names, while equities in Vietnam jumped. Vietnam +1.8%, Nikkei 225 +0.95%, Taiwan +0.85%, ASX 200

+0.2%, Sensex +0.1%. CSI 300 -0.2%, Hang Seng Index -0.4%, Kospi -0.8%.

FIXED INCOME:

US yields remain within 1bp of Monday’s closing levels ahead of $35 billion 10-year reopening auction. Demand was soft for Monday’s 3-year sale. 10-year note auction

is poised to draw the highest yield since 2007, as did the 3-year, which tailed by around 1bp; cycle concludes with $20b 30-year reopening Wednesday. Dollar IG issuance slate contains a handful of names, including Slovenia 10Y benchmark, and another busy day

is expected ahead of CPI and PPI due Wednesday and Thursday; eleven names priced almost $11b Monday.

METALS:

Gold is under pressure as investors turn cautious ahead of the US Consumer Price Index data for August. The precious metal turns vulnerable as a strong recovery in

gasoline prices indicates that headline inflation likely expanded at a higher pace in August. Gold -0.5%, silver -0.7%.

ENERGY:

Oil prices rose, boosted by a tighter supply outlook ahead of US inflation data due Wednesday, which will reflect the impact of oil supply cuts and rising prices

as well as Fed rate policy. OPEC will release its monthly oil market report later today, followed by a report by the International Energy Agency on Wednesday. The US added 300,000 barrels of crude to its strategic reserves last week. Demand for all three

major fossil fuels–oil, coal and natural gas–will peak this decade, marking the “beginning of the end” of fossil fuels and a “historic turning point” in the world’s transition toward renewable energy, the head of the International Energy Agency said Tuesday.

WTI +0.9%, Brent +0.7%, US Nat Gas +2.2%, RBOB +0.1%.

CURRENCIES:

In FX markets, the dollar recovered some recent losses while the euro and pound weakened on concern that Europe faces a growing threat of stagflation. Sterling rose

to a fresh day high after UK labor data came out, before reversing gains. EUR/USD dropped as much as 0.4% as investors looked ahead to the European Central Bank’s policy decision on Thursday. The yen is weaker after strengthening over 1% on Monday in reaction

to Ueda saying it’s possible the BOJ will have enough information by year-end to judge if wages will continue to rise — a key factor in deciding whether to pare back its super-easy monetary policy. US$ Index +0.3%, GBPUSD -0.35%, EURUSD -0.3%, USDJPY +0.25%,

AUDUSD -0.2%, USDNOK +0.45%.

Bitcoin +3.9%%, Ethereum +4.3%.

TECHNICAL LEVELS:

|

ESZ23 |

10 Year Yield |

Dec Gold |

Oct WTI |

Spot $ Index |

|

|

Resistance |

4635.00 |

5.325% |

2040.0 |

93.74 |

108.500 |

|

|

4620.00 |

4.710% |

2029.0 |

91.50 |

107.990 |

|

|

4597.50 |

4.500% |

2004.0 |

90.00 |

107.195 |

|

|

4573.00 |

4.375% |

1996.0 |

89.18 |

105.883 |

|

|

4551/53 |

4.360% |

1978.4 |

88.08 |

105.380 |

|

Settlement |

4539.50 |

1947.2 |

87.29 |

||

|

|

4521.00 |

4.050% |

1939.1 |

84.08 |

103.100 |

|

|

4506.00 |

3.940% |

1927.0* |

81.62 |

102.370 |

|

|

4483.00 |

3.725% |

1907.0* |

79.10 |

101.700 |

|

|

4434.00 |

3.680% |

1866.0 |

76.31 |

100.710 |

|

Support |

4350.00 |

3.500% |

1842.0 |

73.56 |

100.000 |

Colors within the report:

Green is always the 200 period (day, week).

Red is always 21,

Blue = 50,

Brown =

100 *Stars have added importance

UPGRADES:

- AngloGold ADRs (ANG SJ) raised to outperform at BMO

- BRP Inc. (DOO CN) raised to buy at Citi; PT $94

- Banco de Chile ADRs (CHILE CI) raised to outperform at Bradesco BBI; PT $26

- CVS (CVS) raised to outperform at Wolfe; PT $80

- CareTrust REIT (CTRE) raised to outperform at RBC; PT $23

- Equinox Gold (EQX CN) raised to sector perform at RBC; PT C$7.25

- Geron (GERN) raised to buy at Goldman; PT $4

- Iamgold (IMG CN) raised to sector perform at RBC; PT $2.75

- K92 Mining (KNT CN) raised to outperform at RBC; PT C$10

- Santander Chile ADRs (BSAN CI) raised to outperform at Bradesco BBI

DOWNGRADES:

- Avantax Inc (AVTA) cut to neutral at Cantor; PT $26

- Enphase Energy (ENPH) cut to hold at Truist Secs; PT $135

- First National (FXNC) cut to neutral at Janney Montgomery; PT $19

- Hostess Brands (TWNK) cut to equal-weight at Consumer Edge Research

- Hostess Brands (TWNK) cut to hold at Truist Secs

- Osisko Development Corp (ODV CN) cut to sector perform at RBC; PT C$6

- Perion (PERI) cut to market perform at Raymond James

- RTX Corp (RTX) cut to equal-weight at Barclays; PT $75

- RTX Corp (RTX) cut to sector perform at RBC; PT $82

- Sight Sciences (SGHT) cut to market perform at William Blair

- Sight Sciences (SGHT) cut to neutral at Piper Sandler; PT $5.50

INITIATIONS:

- Ambrx Biopharma ADRs (AMAM) rated new buy at BTIG; PT $26

- Berkshire Hills (BHLB) rated new sell at Seaport Global Securities

- Block Inc (SQ) reinstated buy at Berenberg; PT $75

- Boston Properties (BXP) rated new sector weight at KeyBanc

- Brandywine Realty (BDN) rated new overweight at KeyBanc; PT $6

- Brookline Bancorp (BRKL) rated new buy at Seaport Global Securities

- City Office REIT (CIO) rated new sector weight at KeyBanc

- Cousins Properties (CUZ) rated new underweight at KeyBanc; PT $19

- Douglas Emmett (DEI) rated new sector weight at KeyBanc

- Eastern Bankshares (EBC) rated new buy at Seaport Global Securities

- Eli Lilly (LLY) rated new buy at DBS Bank; PT $615

- Endeavor Group (EDR) rated new outperform at Cowen; PT $28

- Gitlab (GTLB) rated new buy at Canaccord; PT $62

- Gitlab (GTLB) rated new outperform at Bernstein

- Global Blue Group Holding (GB) rated new buy at Deutsche Bank; PT $8

- Guess (GES) rated new buy at B Riley; PT $31

- HarborOne (HONE) rated new neutral at Seaport Global Securities

- INDB US (INDB) rated new sell at Seaport Global Securities; PT $45

- Kilroy (KRC) rated new overweight at KeyBanc; PT $47

- Kinross Gold (K CN) rated new buy at Desjardins; PT C$8.50

- Magna Mining Inc (NICU CN) rated new speculative buy at Canaccord

- Omega Healthcare (OHI) rated new sector perform at RBC; PT $33

- Repay Holdings Corp (RPAY) rated new hold at Berenberg; PT $9

- Rexford Industrial (REXR) rated new sector perform at Scotiabank

- Talon Metals (TLO CN) rated new speculative buy at Canaccord

- Verano Holdings (VRNO CN) rated new buy at Eight Capital; PT C$14

- Washington Trust (WASH) rated new buy at Seaport Global Securities

- Webster Financial (WBS) rated new buy at Seaport Global Securities

- Western (WNEB) New England rated New Buy at Seaport Global Securities

Data sources: Bloomberg, Reuters, CQG

No responses yet