TODAY’S GAME PLAN: from the trading

desk, this is not research

DATA/HEADLINES 8:50ET Fed’s Cook speaks; 9:45ET S&P Global US Manufacturing PMI, Composite PMI; 1:00ET Fed’s Daly

and Kashkari speak

TODAY’S HIGHLIGHTS:

- Migrant encounters at US-Mexico border on pace to reach record highs in September

- China climate envoy says phasing out fossil fuels ‘unrealistic’

- China and Syria will upgrade their relationship to a strategic partnership

- Ukraine and the United States have agreed to launch joint weapons production

- Chunks of an asteroid that could tell us about the earliest days of the 4.5 billion-year-old solar system

are set to land in the Utah desert Sunday

Global shares fluctuated after a week packed with central bank meetings. MSCI’s index of global equities was slightly weaker and down about 2.5% for the week. The

“higher for longer” mantra is now the official stance of the US Federal Reserve, European Central Bank and the Bank of England. Significant outliers include the Bank of Japan, which kept interest rates ultra-low on Friday, and the People’s Bank of China, where

recent better economic prospects allowed it to keep rates on hold on Thursday. A contraction in UK economic activity deepened further in September compared to August, marked by growing unemployment and recession risks, additional PMI data showed today. Meanwhile,

China is considering relaxing foreign ownership caps in listed local companies to lure global funds back to its stock market. The increasing possibility that monetary policy will lead to recession is prompting investors to dump stocks at the fastest pace since

December, strategists at Bank of America said.

EQUITIES:

US equity futures nudge higher, signaling a pause in a three-day selloff at the end of a bruising week for investors forced to accept the idea of higher-for-longer interest rates. The

S&P 500 added 0.2%, a modest rebound after the index fell the most since March on Thursday. House Speaker Kevin McCarthy’s attempt to restart his stalled spending agenda failed on Thursday when Republicans for a third time blocked a procedural vote on defense

spending, raising the risk of a government shutdown in just 10 days. Focus this morning will now turn to Manufacturing PMI with expectations of a rise to 48.2 in September from 47.9, and the services gauge may also edge up.

Futures ahead of the bell: E-Mini S&P +0.3%, Nasdaq +0.5%, Russell 2000 +0.3%, Dow +0.15%.

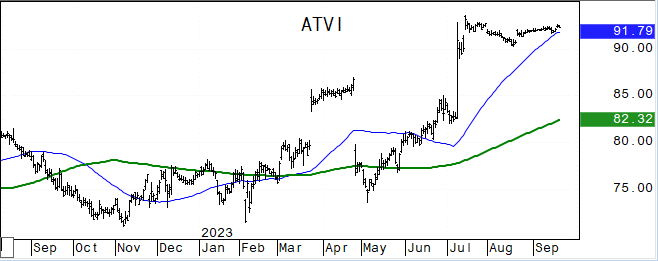

In pre-market trading, Activision Blizzard (ATVI) gained 1.8% as Microsoft’s $69 billion acquisition of the gaming company looked set to clear its final regulatory hurdle. Alibaba Group

(BABA +4%) and other US-listed Chinese stocks are rallying, a day after the Nasdaq Golden Dragon China Index fell to the lowest level since July. Wayfair (W) gains 2.4% after Bernstein raises the online home-furnishings retailer to market perform from underperform.

Scholastic (SCHL) shares fall 18% after the children’s publishing company reported a larger-than-expected adjusted loss per share for the first quarter. Roku (ROKU) is up 1.5% after CFRA upgraded the streaming-video platform company to hold from sell. Coeur

Mining (CDE) is up 5% after RBC upgrades to outperform from sector perform.

European indices pared early losses with UK’s FTSE 100 outperforming amid a weaker pound and gain for AstraZeneca following a positive drug trial update. A preliminary “flash” reading

of the UK composite PMI dropped to 46.8 from 48.6, the lowest PMI score since the pandemic lockdown of January 2021. The survey is closely watched by the BoE. But UK consumer confidence climbed in September to the highest in almost two years and retail sales

grew 0.4% in August, rebounding from a revised 1.1% slump the previous month. Euro-area private sector activity shrank for the fourth consecutive month. The composite PMI hit 47.1 in September, an improvement on August but still in contraction. While Germany’s

downturn eased, it deepened in France. In individual moves in Europe, Adevinta ASA soared after the classifieds company said it received a takeover proposal from private equity investors including Blackstone and Permira. Stoxx 600 -0.2%, DAX -0.2%, CAC -0.5%,

FTSE 100 +0.5%. Basic Resources +0.5%, Energy +0.5%, Healthcare +0.1%, Technology is flat. Construction -1.3%, Banks -0.9%.

Shares in Asia were mixed, as a rebound in Chinese shares offset bearish sentiment from rising expectations that the Federal Reserve will keep interest rates higher for longer. The rally

in Chinese likely reflects short covering on expectations of more policy support measures over the weekend. The MSCI Asia Pacific Index rose 0.3%, snapping a four-day losing streak, led by communication services. Japanese shares pared losses as the yen weakened

after the Bank of Japan held policy steady. Japan’s consumer inflation stayed hot, as consumer prices excluding fresh food rose 3.1% from a year ago in August, instead of slowing as forecast. Indian indices settled lower for the fourth straight day, dragged

mainly by pharmaceutical, realty and metal stocks. Hang Seng Tech Index +3.7%, CSI300 +1.8%, Philippines +0.8%, Taiwan +0.2%, ASX 200 +0.05%. Kospi -0.3%, Sensex -0.3%, Vietnam -1.6%.

FIXED INCOME:

Treasury yields are slightly richer across the curve after longer-dated ones rose during Asia session, with 10-year breaching 4.5% for the first time since 2007.

It’s back around 4.48%, about 1bp richer on the day. 30-year yields hit their highest in a dozen years. US session includes the first Fed speakers since Wednesday’s policy decision. ECB interest rates have reached a level that may help inflation return to

target if held for a sufficient time, Chief Economist Philip Lane said. Next week we have US 2yr, 5yr, and 7yr supply.

METALS:

Gold edged higher after dropping the most in more than two weeks in the previous session as markets digested hawkish commentary from the Federal Reserve. The metal

is on track for a small weekly gain despite the Fed signaling there was one more hike to come this year. Spot gold +0.3%, silver +1.2%.

ENERGY:

Oil prices rose as renewed global supply concerns from Russia’s fuel export ban counteracted demand fears. Both benchmarks are on track for a small weekly drop after

gaining more than 10% in the previous three weeks amid concerns about tight global supply. Russia’s Transneft suspended deliveries of diesel to two key Baltic and Black Sea terminals on Friday, state media agency Tass said. Russia temporarily banned exports

of gasoline and diesel to all countries outside a circle of four ex-Soviet states with immediate effect, the government said on Thursday. European natural gas prices fell as Chevron and labor unions in Australia agreed to end strikes at major export plants.

WTI +1%, Brent +0.8%, US Nat Gas +0.7%, RBOB +0.9%.

CURRENCIES:

The US dollar is headed for its 10th consecutive weekly increase, lifted by a fall in the euro on grim euro-zone economic data. The euro fell before trimming some

losses on fresh signs of frailty in the euro-area economy as data showed private-sector activity in France and Germany continued to shrink in September. The euro zone economy will likely contract in the third quarter and won’t return to growth anytime soon,

HCOB’s flash purchasing managers’ index showed. The yen fell, following the Bank of Japan’s decision to hold interest rates in negative territory, suggesting it was in no rush to phase out its massive stimulus program. Traders were extra wary of intervention

after the BOJ noted it was watching the impact of FX moves on Japan’s economy. In emerging markets, Indian bonds and the rupee rallied after JPMorgan said it would add Indian debt to its widely tracked emerging markets index, setting the stage for billions

of dollars in foreign inflows. US$ Index +0.25%, GBPUSD -0.4%, EURUSD -0.2%, USDJPY +0.45%, AUDUSD +0.5%, NZDUSD +0.6%.

Bitcoin +0.2%, Ethereum +0.6%. Binance CEO filed court papers seeking to dismiss a lawsuit by the SEC, claiming that the agency overstepped its authority.

TECHNICAL LEVELS:

|

ESZ23 |

10 Year Yield |

Dec Gold |

Nov WTI |

Spot $ Index |

|

|

Resistance |

4542.00 |

5.500% |

2083.5 |

98.00 |

|

|

|

4502/09 |

5.325% |

2047.0 |

97.07 |

108.500 |

|

|

4482.00 |

5.000% |

2022.0 |

95.00 |

107.990 |

|

|

4454.00 |

4.710% |

1996.0 |

93.74 |

107.195 |

|

|

4402.00 |

4.500% |

1981.8 |

92.00 |

105.880 |

|

Settlement |

4372.00 |

1939.6 |

89.63 |

||

|

|

4348/50* |

4.140% |

1933.7* |

87.50 |

104.460 |

|

|

4331.00 |

4.000% |

1907.0* |

83.00/50 |

103.100 |

|

|

4305.00 |

3.750% |

1866.0 |

82.25 |

102.680 |

|

|

4288.00 |

3.530% |

1842.0 |

81.40/60 |

101.950 |

|

Support |

4245.00 |

3.265% |

1821.0 |

76.75 |

100.910 |

Colors within the report:

Green is always the 200 period (day, week).

Red is always 21,

Blue = 50,

Brown =

100 *Stars have added importance

- Upgrades

- (CDE) Coeur Mining Raised to Outperform at RBC; PT $4

- (CHTR) Charter Communications Raised to Overweight at Wells Fargo

- (ROKU) Roku Raised to Hold at CFRA; PT $75

- (W) Wayfair Raised to Market Perform at Bernstein; PT $65

- Downgrades

- (BA) Boeing Cut to Hold at CFRA; PT $210

- (DE) Deere Cut to Hold at Canaccord; PT $400

- (HEI) Heico Cut to Sell at CFRA; PT $151

- (HWM) Howmet Aerospace Cut to Sell at CFRA

- (ICE) Intercontinental Exchange Cut to Neutral at Goldman; PT $125

- (SPLK) Splunk Cut to Hold at Loop Capital; PT $157

- (SPLK) Cut to Sector Perform at RBC; PT $157

- (SPLK) Cut to Hold at Canaccord; PT $157

- (SPLK) Cut to Neutral at Baird; PT $157

- (SPLK) Cut to Market Perform at BMO; PT $157

- (SPLK) Cut to Sector Weight at KeyBanc

- (TVTX) Travere Therapeutics Inc Cut to Equal-Weight at Wells Fargo

- Initiations

- (ALEC) Alector Rated New Overweight at Cantor; PT $13

- (ARM) ARM Holdings ADRs Rated New Neutral at Susquehanna; PT $48

- (AZUL4 BZ) Azul ADRs Rated New Buy at HSBC; PT $12.30

- (CART) Maplebear Rated New Neutral at BTIG

- (CCCS) CCC Intelligent Solutions Rated New Buy at Stifel; PT $14

- (COEP) Coeptis Therapeutics Rated New Buy at Ladenburg Thalmann; PT $3

- (DG) Dollar General Rated New Reduce at HSBC; PT $102

- (DOMO) Domo Rated New Neutral at DA Davidson; PT $10

- (EXITO CB) Almacenes Exito ADRs Reinstated Market Perform at Itau BBA

- (HD) Home Depot Rated New Hold at HSBC; PT $365

- (IKNA) Ikena Rated New Outperform at Wedbush; PT $11

- (ITRI) Itron Rated New Buy at Seaport Global Securities; PT $80

- (KNSL) Kinsale Capital Rated New Outperform at Wolfe; PT $521

- (KR) Kroger Rated New Hold at HSBC; PT $52

- (LOW) Lowe’s Rated New Hold at HSBC; PT $250

- (NXT) NEXTracker Rated New Outperform at Wolfe; PT $52

- (O) Realty Income Rated New Equal-Weight at Wells Fargo; PT $59

- (ORIC) ORIC Pharma Rated New Outperform at Wedbush; PT $14

- (RCM) RCM Reinstated Buy at Citi; PT $20

- (RL) Ralph Lauren Rated New Outperform at Raymond James; PT $135

- (RYAN) Ryan Specialty Rated New Outperform at Wolfe; PT $59

- (SLDB) Solid Biosciences Rated New Overweight at Cantor; PT $5

- (TGT) Target Rated New Hold at HSBC; PT $140

- (USPH) US Physical Therapy Rated New Overweight at JPMorgan; PT $108

- (WMT) Walmart Rated New Buy at HSBC; PT $200

Data sources: Bloomberg, Reuters, CQG

No responses yet