TODAY’S GAME PLAN: from the trading

desk, this is not research

DATA/HEADLINES 8:30ET US Oct. Retail Sales, PPI, US Nov. Empire Manufacturing; 9:30ET Fed’s Barr speaks; 10:00ET

US Sept. Business Inventories; 3:30ET Fed’s Barkin speaks

PPI -0.5% MoM, Exp. 0.1%, Last 0.4%; PPI core 0.0%, Exp. 0.3%, Last 0.2%. PPI 1.3% YoY, Exp. 1.9%, Last 2.2%; PPI core 2.4%, Exp. 2.7%, Last 2.7%; US RETAIL SALES – Headline: -0.1% (exp.

-0.3%, prev. 0.7%, rev. 0.9%)

TODAY’S HIGHLIGHTS:

- US House voted 336-95 to pass a temporary spending bill that would avert a government shutdown

- IDF called on all Hamas operatives in the Al Shifa hospital to surrender

World stocks gained as investors welcomed cooler-than-expected inflation readings in the US and the UK as evidence that central banks may be done with their aggressive

interest-rate hikes. The MSCI world equity index rose 0.5% to its highest since mid-September, following a rally across Asia aided by a report of stimulus in China. Strong industrial output and retail sales data in China and a report from Bloomberg News that

China plans to provide 1 trillion yuan ($137 billion) of low-cost financing to boost the housing market aided sentiment. Also, British inflation cooled more than expected in October as energy prices dropped but there was also a wider softening of price pressures,

data showed. Japan’s economy shrank 2.1% on an annualized basis in the third quarter, far worse than estimated. Meanwhile, the Israeli military entered Gaza’s Shifa hospital compound as part of what it called a “precise and targeted operation” against Hamas.

EQUITIES:

US equity are higher, building on post CPI gains as investors await today’s data on retails sales and producer prices for further confirmation that an economic slowdown

will allow the Federal Reserve to stop tightening monetary policy. Russell 2000 led yesterday’s gains as beaten down US small caps rallied with traders erasing bets on more Fed hikes. House lawmakers passed a temporary government funding bill that greatly

lowers the risk of a shutdown. The legislation now goes to the Senate where Democrats are expected to back it, even though it doesn’t include Ukraine and Israel aid they support.

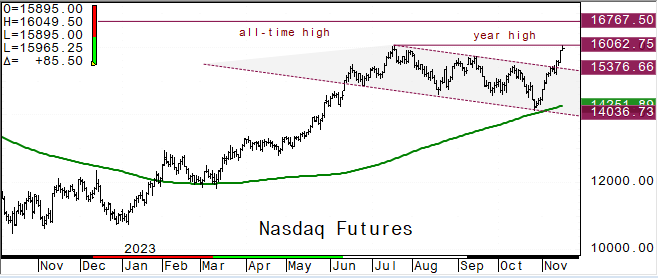

Futures ahead of the bell: E-Mini S&P +0.5%, Nasdaq +0.5%, Russell 2000 +0.4%, Dow +0.25%. Nasdaq nearing the July high.

In pre-market trading, Target Corp. rallied more than 15% as profits beat estimates, reflecting fewer discounts and better inventory management. Advance Auto (AAP) falls about 5% after

cutting its earnings per share guidance for the full year. Arcturus Therapeutics (ARCT) rises 19% after reporting results and saying it should now have enough cash resources to last until the end of 2026. Catalent (CTLT) rises 5% after reaffirming its adjusted

Ebitda forecast for the full year. Goodyear Tire & Rubber (GT) gains 8.6% after the company said it will actively pursue strategic alternatives for its chemical business, the Dunlop brand and the off-the-road equipment tire business. Varex Imaging (VREX) slips

9.8% after the maker of X-ray equipment posted disappointing fiscal 4Q revenue. ZIM Integrated Shipping (ZIM) falls 8% after cutting its adjusted Ebitda guidance for the full year.

European stocks rose, extending Tuesday’s rally on optimism that inflation is cooling. London’s FTSE 100 index gained 1% after UK inflation slowed more than forecast. UK annual consumer

price inflation sank to a lower-than-expected 4.6% from 6.7% in September, official data showed, the smallest increase in two years and the biggest monthly fall since April 1992. Core inflation fell to 5.7% from 6.1%, while service sector inflation fell to

6.6% from 6.9%. Europe’s Stoxx 600 Index gained 0.7%, led by miners on an improving demand outlook for steel in China. Among individual names, Infineon Technologies AG gained about 7% after the German chipmaker forecast higher sales, helped by strength in

its automotive business. French train maker Alstom SA slumped 17% after announcing a plan to cut jobs and sell assets. Siemens Energy (ENR.GR) is trading higher after German government agrees to provide €7.5B of state guarantees to the group as part of a €15B

rescue package. DAX +0.8%, CAC +0.6%. Basic Resources +2.8%, Technology +1..9%. Telecom -0.3%.

Shares in Asia were broadly higher on hopes for the Chinese economy after strong data on consumption and new government stimulus. The PBOC injected the most cash since 2016 into the

banking system to boost growth. Industrial output in China grew 4.6% in October and retail sales rose 7.6%, improving from 5.5% in September, but real estate remains in the doldrums with investment in January-October down 9.3% year-on-year. The MSCI Asia Pacific

Index climbed 2.3%, its biggest single-day rally in more than a year as tech shares provided the biggest boost. Tencent’s earnings beat with revenue climbing 10%. The Hang Seng Index rose nearly 4% as mainland property developers outperformed. Shares in Australia

were led higher by notable outperformance in real estate and tech following a decline in yields. The Nikkei 225 was near the top of the leader board as a deeper-than-expected contraction in Japan’s third-quarter GDP adds to the case for continued stimulus

from the Bank of Japan. Hang Seng +3.9%, Nikkei 225 +2.5%, Kospi +2.2%, ASX 200 +1.4%, Sensex +1.1%, CSI 300 +0.7%.

FIXED INCOME:

Treasuries are slightly cheaper across the curve as futures edge lower into early US session, leaving yields higher by 1bp-2bp across the curve. After dropping 19

basis points (bps) on Tuesday in their biggest one-day drop since March 10-year Treasury yields eased another basis point to steady around 4.46%. Curve spreads are within 1bp of Tuesday’s close. Traders are now gearing up for what may be a fundamental shift

in the investment landscape. Fed swaps indicate the odds of another hike have fallen to almost zero — with the market pricing in 50 basis points of rate cuts by July.

METALS:

Gold extended gains despite a stronger dollar. Base metals are firmer across the board following the upbeat Chinese activity data. The precious metal rose for a

third day after jumping as much as 1.2% in the previous session, when the US consumer price index excluding food and fuel — a measure favored by economists as a better indicator of underlying inflation — rose less than expected. Spot gold +0.4%, silver +2%.

ENERGY:

Crude oil prices are slightly lower after settling relatively flat yesterday despite the softer inflation data and subsequent slide in the dollar. Oil dipped amid

signs the United States is at peak production, offsetting positive crude demand signals from top consumer China. US crude inventories rose by 1.3 million barrels last week, while Cushing supplies also increased, according to API. The US weekly EIA data will

be released in two parts today to account for last week’s systems upgrade. Last week’s data will be released at the usual time of 10:30ET while this week’s data is due at 13:00ET. WTI -0.3%, Brent -0.5%, US Nat Gas +2.5%, RBOB -1.4%.

CURRENCIES:

In currency markets, the dollar edged up after its biggest drop in a year yesterday after cooler US inflation data added to investor conviction that the Federal

Reserve may not raise rates again. Sterling eased back from Tuesday’s two-month highs after data showed British inflation ran at its slowest pace in two years in October, at 4.6%, below forecasts of 4.8% and below September’s 6.7% reading. That news strengthened

optimism that the Bank of England may also be finished raising rates. Kiwi outperforms underpinned by encouraging Chinese activity data. US$ Index +0.05%, GBPUSD -0.25%, USDJPY -0.05%, EURUSD -0.05%, AUDUSD +0.4%, USDNOK -0.75%, NZDUSD +0.6%.

Bitcoin +1.8%, Ethereum +1.9%. Bitcoin is modestly firmer but overall action has been contained amid a lack of fresh catalysts. JPMorgan said its digital token JPM

Coin may be handle as much as $10 billion in daily transactions in the next year or two.

TECHNICAL LEVELS:

|

ESZ23 |

10 Year Yield |

Dec Gold |

Dec WTI |

Spot $ Index |

|

|

Resistance |

4652.00 |

5.500% |

2056.0 |

87.34 |

108.970 |

|

|

4624.00 |

5.325% |

2029.4 |

85.71 |

107.990 |

|

|

4600.00 |

5.000% |

2019.7 |

83.70 |

107.350 |

|

|

4561/66 |

4.810% |

1998.0 |

81.60 |

106.785 |

|

|

4525.00 |

4.600% |

1982.2 |

80.00 |

105.880 |

|

Settlement |

4511.00 |

1966.5 |

78.26 |

||

|

|

4480.00 |

4.350% |

1938.1 |

76.77 |

104.850 |

|

|

4452.00 |

3.930% |

1921.5 |

74.25 |

104.380 |

|

|

4438.00 |

3.640% |

1898.4 |

72.88 |

103.800 |

|

|

4407.00 |

3.245% |

1865.5 |

70.00 |

103.420 |

|

Support |

4371.00 |

|

1849.0 |

66.80 |

102.550 |

Colors within the report:

Green is always the 200 period (day, week).

Red is always 21,

Blue = 50,

Brown =

100 *Stars have added importance

- Upgrades

- Centessa Pharmaceuticals (CNTA) ADRs Raised to Buy at Jefferies

- Holley (HLLY) Raised to Buy at Jefferies; PT $5

- Power of Canada (POW CN) Raised to Buy at Desjardins; PT C$39

- Premium Brands (PBH CN) Raised to Buy at Stifel Canada; PT C$108

- VF Corp (VFC) Raised to Neutral at JPMorgan; PT $19

- Vipshop (VIPS) ADRs Raised to Buy at Citi; PT $20

- Wix.com (WIX) Raised to Overweight at Barclays; PT $130

- Downgrades

- Argonaut Gold (AR CN) Cut to Hold at Desjardins; PT 60 Canadian cents

- Beauty Health (SKIN) Cut to Hold at Jefferies; PT $1.50

- Bluegreen Vacations Hold (BVH) Cut to Hold at Truist Secs

- Bristol Myers (BMY) Cut to Neutral at Cantor

- Canadian Solar (CSIQ) Cut to Underweight at JPMorgan; PT $22

- Energizer Holdings (ENR) Cut to Underweight at JPMorgan; PT $33

- Cut to Sector Perform at RBC; PT $38

- Cut to Underweight at Morgan Stanley; PT $33

- Fluent (FLNT) Cut to Hold at Canaccord; PT $2

- GreenPower Motor (GPV CN) Cut to Neutral at BTIG

- Pioneer Natural (PXD) Cut to Neutral at Mizuho Securities; PT $301

- RTX Corp (RTX) Cut to Neutral at Redburn; PT $80

- SQZ Biotech (SQZB) Cut to Hold at Brookline Capital; PT $5,204

- Workhorse Group (WKHS) Cut to Neutral at BTIG

- Initiations

- AerCap Holdings (AER) Rated New Overweight at Barclays; PT $80

- AGNC Investment (AGNC) Rated New Equal-Weight at Barclays; PT $8

- Air Lease (AL) Rated New Overweight at Barclays; PT $46

- American Express (AXP) Rated New Overweight at Barclays; PT $184

- BioMarin (BMRN) Rated New Overweight at Wells Fargo; PT $100

- Bread Financial Holdings (BFH) Rated New Underweight at Barclays

- BrightSpire Capital Inc (BRSP) Rated New Equal-Weight at Barclays

- Chord Energy (CHRD) Reinstated Overweight at Wells Fargo; PT $189

- Datadog (DDOG) Rated New Outperform at CICC; PT $116

- Digi International (DGII) Rated New Buy at B Riley; PT $34

- Discover Financial (DFS) Rated New Equal-Weight at Barclays; PT $99

- Essent (ESNT) Rated New Overweight at Barclays; PT $60

- First American (FAF) Rated New Equal-Weight at Barclays; PT $53

- FNF (FNF) Rated New Equal-Weight at Barclays; PT $44

- Lifezone Metals (LZM) Rated New Buy at Liberum; PT $17.50

- Lithium Americas (LAC CN) Rated New Outperform at National Bank; PT C$16

- Magnolia Oil & Gas (MGY) Reinstated Equal-Weight at Wells Fargo

- Matador Resources (MTDR) Reinstated Overweight at Wells Fargo; PT $73

- MGIC (MTG) Rated New Equal-Weight at Barclays; PT $19

- Mr Cooper (COOP) Rated New Overweight at Barclays; PT $74

- Navient (NAVI) Rated New Equal-Weight at Barclays; PT $17

- NMI Holdings (NMIH) Rated New Overweight at Barclays; PT $37

- OneMain (OMF) Rated New Overweight at Barclays; PT $51

- PennyMac (PFSI) Rated New Overweight at Barclays; PT $82

- Permian Resources (PR) Reinstated Overweight at Wells Fargo; PT $17

- Perspective Therapeutics (CATX) Rated New Buy at JonesTrading; PT $1.40

- Radian (RDN) Rated New Equal-Weight at Barclays; PT $28

- Reneo Pharma (RPHM) Rated New Outperform at William Blair

- Rocket Cos. (RKT) Rated New Underweight at Barclays; PT $6

- SLM (SLM) Rated New Overweight at Barclays; PT $16

- SM Energy (SM) Reinstated Equal-Weight at Wells Fargo; PT $40

- SoFi Technologies (SOFI) Rated New Equal-Weight at Barclays; PT $8

- Spectaire (SPEC) Rated New Hold at Jefferies; PT $2.50

- Synchrony Financial (SYF) Rated New Equal-Weight at Barclays; PT $31

- UWM Holdings (UWMC) Rated New Underweight at Barclays; PT $4

- Warner Music (WMG) Rated New Equal-Weight at Wells Fargo; PT $35

Data sources: Bloomberg, Reuters, CQG

No responses yet