TODAY’S GAME PLAN: from the trading

desk, this is not research

DATA/HEADLINES 8:30ET Housing Starts, Building Permits; Kansas City Fed Services Activity; 8:45ET Fed’s Collins

speaks, Fed’s Barr speaks; 9:30ET Fed’s Daly speaks; 9:45ET Fed’s Goolsbee speaks

TODAY’S HIGHLIGHTS:

- US forces have been attacked at least 57 times in less than a month by Iran-backed proxies

- Treasuries Suffer First Outflows Since 2021 as China and Japan cut stockpiles

- IBM suspended advertising on X after a report showed ads for firms including Apple and Oracle ran alongside

pro-Nazi posts - SpaceX is poised to launch its deep-space Starship rocket tomorrow

World stocks held near two-month peaks, while oil prices were set for a fourth week of declines in a boost for the inflation outlook. Global equity funds saw significant

inflows in the week ending Nov. 15, buoyed by investor hopes that cooler-than-expected US inflation would prompt the Federal Reserve to pause interest rate hikes. Money markets now pricing in roughly 100 basis points worth of rate cuts next year in the United

States and the euro area. November so far has seen one of the strongest performances for stock markets this year, with MSCI’s world stock index and the S&P 500 index over 7% higher each. A slew of central bankers from the ECB, Bank of England and Fed are due

to speak today and traders will be watching for possible pushback against rate-cut expectations from policy makers.

EQUITIES:

US equity futures climbed, looking to build on the week’s solid gains, with Gap soaring 20% in post-market trading after reporting third-quarter profit that exceeded

forecasts. According to Bank of America strategist Michael Hartnett, technical and macroeconomic headwinds are building and investors should offload risky assets after the recent gains. The bank’s bull and bear indicator suggests offloading the S&P 500 above

the 4,500 level. Meanwhile, President Biden signed a stopgap bill to extend funding into early 2024, averting a government shutdown for now but kicking a politically-divisive debate over federal spending into a presidential election year.

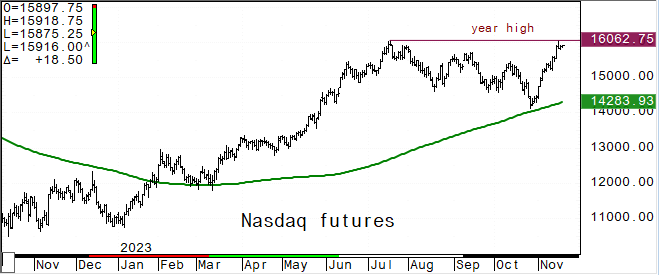

Futures ahead of the bell: E-Mini S&P +0.3%, Nasdaq +0.1%, Russell 2000 +1.2%, Dow +0.3%.

In premarket trading, Applied Materials (AMAT) fell over 7% after Reuters reported the company faces a US criminal probe for allegedly violating export restrictions to China. Gap (GPS

+20%) on Thursday forecast holiday-quarter sales below estimates but posted better-than-expected results for the third quarter thanks to easing supply expenses and cost-control efforts. ChargePoint (CHPT) tumbles 29% after the company replaced longtime CEO.

Alibaba (BABA) ADRs fall 3.3%, extending Thursday’s decline after the internet giant called off a spinoff of its cloud unit, citing tightening US curbs on advanced chips for China. Li Auto (LI) ADRs rise 3.8% after news that the Chinese carmaker and Wuxi AppTec

will join the Hang Seng Index. Coherus Biosciences (CHRS) gains 9% after Baird initiated coverage with a bullish rating, saying the company’s

broad commercial pipeline has positioned it for accelerating growth.

European stocks rise as investors ramp up bets on interest-rate cuts next year. British retail sales volumes fell unexpectedly in October as stretched consumers stayed at home, official

data showed. UK retail sales fell 0.3% m/m in October, well below consensus expectations for a +0.4% expansion. The number for September was also revised down to -1.1% m/m. Europe’s Stoxx 600 index jumped as much as 1.1% with all 20 sectors in the green –

real estate, basic resources and financial services are the best performers. Stoxx 600 +0.9%, DAX +0.9%, CAC +0.9%, FTSE 100 +0.8%. Basic Resources +1.8%, REITs +1.7%, Financial Services +1.7%, Travel +0.2%.

Asian gauges recouped earlier losses as gains in Japanese shares helped offset a selloff in Hong Kong. The MSCI Asia Pacific Index climbed 0.1% after erasing a drop of as much as 0.5%,

ending with its best weekly advance since July. Stocks were undermined by a 10% drop in Alibaba Group, which scrapped plans to list its $11 billion cloud unit as a fight between the US and China for technological dominance escalates. Chinese blue chips (CSI300)

were lower, having missed on the general rally this week. Chinese car companies, including Nio (-3%), fell after a Reuters report that US lawmakers raised concerns about the collection of sensitive data by these companies. Vietnam -2.2%, Hang Seng Index -2.1%,

Kospi -0.7%, Sensex -0.3%, Singapore -0.3%, ASX 200 -0.1%, CSI 300 -0.1%, Shanghai Composite +0.1%, Taiwan +0.2%, Philippines +0.3%, Topix +0.9%.

FIXED INCOME:

Treasuries added to Thursday’s gains with yields richer by 2bp to 3bp across the curve after touching lowest levels since September. Rate-sensitive two-year Treasuries

yields are down 23 basis points for the week at 4.82%, set for their best weekly performance since March. In Europe, two-year yields in Germany and Britain fell to their lowest levels since June. Gilt yields fell as much as 12 basis points as data showed a

surprise drop in UK retail sales last month. US 10-year yields around 4.405%, richer by ~3bp and curves are mostly flat. The US session includes four Fed speakers. Monday’s 20-year bond auction and 10yr TIPS auction on Tuesday, in a shortened holiday week,

may add some supply pressure to today’s trading.

METALS:

Gold climbed as the dollar and Treasury yields kept falling. Bullion rose 1.1% yesterday, in its strongest increase in nearly three weeks, as traders reacted to signals

that the labor market may finally be starting to weaken. Greenlight Capital reported a major increase in its exposure to gold as the hedge fund’s founder, David Einhorn, said Investors “are too complacent about geopolitical uncertainty.” Spot gold +0.5%,

silver +1.1%.

ENERGY:

Oil prices rose after sliding almost 5% on Thursday to four-month lows and sinking into a bear market, down over 20% from their September highs. Stronger-than-expected

non-OPEC production is driving the slump, according to Goldman, but it anticipates output from outside of core OPEC members to slow. JPMorgan says OPEC+ could surprise with even deeper curbs, but those would be difficult to orchestrate. Crude is on a run of

four straight weekly declines — the longest losing streak since May. WTI +1.3%, Brent +1.4%, US Nat Gas is flat, RBOB +1%.

CURRENCIES:

In FX markets, the sea change in market pricing for the Fed weighed on the dollar. The yen led Group-of-10 gains as dollar bulls trimmed exposure following the latest

dataset out of the US which added to signs that the Federal Reserve may be done with rate hikes. US$ Index -0.25%, GBPUSD +0.1%, USDJPY -0.9%, EURUSD +0.1%, AUDUSD +0.5%, USDNOK -0.6%.

Bitcoin +1.5%, Ethereum +0.5%.

TECHNICAL LEVELS:

|

ESZ23 |

10 Year Yield |

Dec Gold |

Jan WTI |

Spot $ Index |

|

|

Resistance |

4652.00 |

5.500% |

2081.0 |

86.29 |

107.990 |

|

|

4624.00 |

5.325% |

2056.0 |

84.94 |

107.350 |

|

|

4600.00 |

5.000% |

2029.4 |

80.00 |

106.785 |

|

|

4561/65 |

4.810% |

2019.7 |

78.17 |

105.810 |

|

|

4541.00 |

4.610% |

1998.0 |

76.17 |

104.800 |

|

Settlement |

4523.25 |

1987.3 |

73.09 |

||

|

|

4490.00 |

4.350% |

1981.4 |

72.16 |

103.800 |

|

|

4458.00 |

3.930% |

1938.1 |

70.04w |

103.620 |

|

|

4436.00 |

3.640% |

1921.5 |

66.80 |

102.550 |

|

|

4407.00 |

3.245% |

1898.4 |

65.00 |

101.240 |

|

Support |

4381.00 |

|

1865.5 |

63.64 |

100.000 |

Colors within the report:

Green is always the 200 period (day, week).

Red is always 21,

Blue = 50,

Brown =

100 *Stars have added importance

- Upgrades

- Analog Devices (ADI) Raised to Overweight at Morgan Stanley; PT $225

- Brookdale (BKD) Raised to Outperform at RBC; PT $9

- Expedia (EXPE) Raised to Outperform at Evercore ISI

- Hubbell (HUBB) Raised to Overweight at JPMorgan; PT $335

- Ivanhoe Mines (IVN CN) Raised to Overweight at Morgan Stanley; PT C$13.50

- Kulicke & Soffa (KLIC) Raised to Buy at Fubon; PT $57

- Larimar Therapeutics Inc (LRMR) Raised to Buy at Citi; PT $4.50

- Patterson-UTI (PTEN) Raised to Outperform at ATB Capital; PT $17

- Roblox (RBLX) Raised to Peerperform at Wolfe

- Zoom Video (ZM) Raised to Neutral at Citi; PT $66

- Downgrades

- Agilent (A) Cut to Neutral at UBS; PT $125

- Air Products (APD) Cut to Sell at Redburn; PT $240

- Airbnb (ABNB) Cut to Inline at Evercore ISI; PT $136

- Andlauer Healthcare Group (AND CN) Cut to Sector Perform at National Bank

- Ayr Wellness (AYR/A CN) Cut to Sector Perform at ATB Capital; PT C$3

- Canacol Energy (CNE CN) Cut to Market-Weight at Valores Bancolombia

- ChargePoint (CHPT) Cut to Neutral at Janney Montgomery; PT $5

- Cut to Neutral at Roth MKM; PT $2

- Cisco (CSCO) Cut to Hold at DZ Bank; PT $50

- Helmerich & Payne (HP) Cut to Sector Perform at ATB Capital; PT $47

- Marriott Vacations (VAC) Cut to Underperform at BofA; PT $65

- Tim Brasil (TIMS3 BZ) ADRs Cut to Equal-Weight at Barclays; PT $18

- Trane Technologies (TT) Cut to Hold at CFRA; PT $229

- Triumph Financial Inc (TFIN) Cut to Neutral at DA Davidson; PT $72

- ZIM Integrated Shipping (ZIM) Cut to Neutral at JPMorgan; PT $6.20

- Initiations

- Academy Sports & Outdoors (ASO) Rated New Buy at Truist Secs; PT $57

- Cava Group (CAVA) Rated New Market Perform at Raymond James

- Coherus Bio (CHRS) Rated New Outperform at Baird; PT $11

- Curis (CRIS) Rated New Buy at Truist Secs; PT $26

- D2L (DTOL CN) Rated New Buy at Stifel Canada; PT C$14

- Dada Nexus (DADA) ADRs Rated New Accumulate at CLSA; PT $4.60

- Deckers Outdoor (DECK) Rated New Buy at Truist Secs; PT $735

- Dick’s Sporting (DKS) Rated New Buy at Truist Secs; PT $134

- First Citizens (FCNCA) Rated New Buy at William O’Neil

- Fortuna Silver (FVI CN) Reinstated Outperform at BMO; PT C$5.50

- Icosavax (ICVX) Rated New Buy at Guggenheim; PT $28

- Intuitive Surgical (ISRG) Rated New Buy at HSBC; PT $318

- Janus Henderson (JHG) Rated New Equal-Weight at Morgan Stanley; PT $26

- Kenvue (KVUE) Rated New Neutral at Piper Sandler; PT $20

- Kimberly-Clark (KMB) Rated New Overweight at Piper Sandler; PT $146

- Lululemon (LULU) Reinstated Buy at Truist Secs; PT $500

- Nike (NKE) Rated New Hold at Truist Secs; PT $108

- On Holding (ONON) Rated New Hold at Truist Secs; PT $29

- Perrigo (PRGO) Rated New Overweight at Piper Sandler; PT $37

- TopBuild (BLD) Rated New Buy at Goldman; PT $355

- Tourmaline Bio Inc (TRML) Rated New Buy at Truist Secs; PT $43

- Under Armour (UAA) Rated New Hold at Truist Secs; PT $8

Data sources: Bloomberg, Reuters, CQG

No responses yet