TODAY’S GAME PLAN: from the trading

desk, this is not research

DATA/HEADLINES ET 7:00 a.m: Mexico 3Q GDP, 8:30 a.m: Canada Sep. Retail Sales, 9:45 a.m: US Nov. S&P Global Manufacturing

and Services PMIs

TODAY’S HIGHLIGHTS:

- Irish police have made 34 arrests after Dublin rioting

- Dallas Cowboys’ DaRon Bland sets single-season record with 5th pick-6

World stocks were mostly higher and are on track for the best month in three years, up 8.6% in the MSCI All Country World Index.

Global stock funds saw significant inflows of about $40 billion in the two weeks through Nov. 21, the most in nearly two years, according to Bank of America Corp.’s Michael Hartnett,

citing EPFR Global data. However, cash funds continue to dominate with additions of nearly $1.2 trillion in 2023, compared to $143 billion into equities, while bond funds have experienced overall outflows. Elsewhere, a short pause in the war between Israel

and Hamas began, with the first group of hostages expected to be released later today. Hamas is meant to return 50 of the almost 240 hostages captured on Oct. 7, while Israel will release 150 jailed Palestinians and allow more aid into Gaza.

EQUITIES:

US equity futures were higher after the Thanksgiving holiday, maintaining gains in November amid optimism that interest rates have peaked and won’t lead to a recession.

The VIX Index is at 13, near the year’s lowest levels. Investors remain optimistic about a soft landing for the US economy, betting that the Federal Reserve is finished with monetary tightening. Manufacturing and services PMI data later in the day may provide

additional insights into the growth and corporate earnings outlook

Nvidia shares fell 2% in premarket trading following a report of a delay in launching a new artificial intelligence chip. iRobot (IRBT) shares rose 37% after reports that Amazon

is expected to receive unconditional EU antitrust approval for its acquisition of the household appliance company.

Tesla shares declined 0.9%, facing pressure from potential steeper price cuts by competitor BYD for its Dynasty series models and an ongoing strike in Sweden.

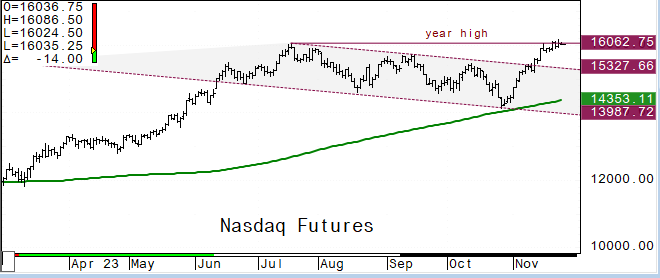

Futures ahead of the bell: E-Mini S&P +0.1%, Nasdaq was flat, Russell 2000 +0.2%, Dow +0.2%.

European shares edged higher, with the Stoxx Europe 600 Index up 0.2%. Energy and insurance stocks led gains, while miners declined. BASF SE rose following reports

of a potential acquisition by Abu Dhabi National Oil Co. Focus is on US manufacturing PMI data later in the day. European stocks reached a two-month high, set for the best month since January, boosted by optimism about more dovish central banks amid easing

inflation. ECB President Christine Lagarde suggested the possibility of a pause in tightening, while Governing Council Member Robert Holzmann sees equal chances of a rate hike or cut in Q2 2024. Individual moves include Team17 stock dropping 42% as some game

titles underperform, and Mercedes Benz Group AG and Porsche Automobil Holding SE shares declining after Barclays analysts downgrade their recommendations. Investors show increased interest in equities, with global stock funds experiencing inflows of about

$40 billion in the two weeks through Nov. 21, while European equities continue their 37th week of outflows at $32 million, according to Bank of America.

Stoxx 600 +0.1%, DAX flat, CAC +0.1%, FTSE 100 -0.4%.

REITs +0.6%, Financial Services +0.4%, Tech was flat, Energy +0.3%, Retail -0.2%.

Asia stocks slid, paring weekly gains, led by Chinese equities as optimism wanes over Beijing’s measures to support the property sector. The MSCI Asia Pacific Index

dropped 0.4%, with Tencent, AIA Group, and Alibaba weighing it down. Mainland China and Hong Kong suffer notable losses, while Japanese benchmarks rose after a holiday. Japan’s key inflation measure accelerated for the first time in four months, clouding the

outlook for the BOJ. CPI excluding fresh food inched up to 2.9% in October from 2.8% in September. The Hang Seng China Enterprises Index slipped 2.2%, erasing Thursday’s gains on fading property sector optimism. Despite the decline, the key Asia stock gauge

has gained 7% this month, its best since January. Next week, attention turns to US and China growth data, along with central bank meetings in New Zealand, Thailand, and South Korea. Notable movers include BYD’s 5.5% decline, Japan’s defense-related firms rising,

and SeAH Besteel Holdings and Dentium jumping on inclusion in the Kospi 200 Index.

Philippines +0.4%, Singapore -0.4%, Topix +0.5%, Vietnam +0.6%, Sensex -0.1%, Kospi -0.7%. ASX 200 +0.1%, Taiwan -0.04%, Thailand -0.5%, Indonesia +0.8%, CSI 300 –0.6%.

FIXED INCOME:

Treasuries remained weaker, having retreated from session highs reached when UK and euro-zone yields increased on Thursday. Two-, five-, and seven-year yields touched

weekly highs ahead of the next week’s compressed auction cycle, starting on Monday with two- and five-year notes. Yields are higher by 4bp-6bp across the curve, with the 10-year at 4.46%, rising as much as 8bp to 4.486%, just shy of the weekly high reached

on Monday. The upcoming auction cycle includes $54 billion in two-year and $55 billion in five-year notes on Monday, followed by $39 billion in seven-year notes on Tuesday.

METALS:

Gold edged higher and is on track for a second weekly gain, supported by a weakening US dollar and expectations of looser monetary policy in 2024. Anticipation of

Fed rate cuts boosts gold, countering persistent ETF outflows. Investors eye US PMIs on Friday for economic health assessment, with weaker readings potentially reinforcing bets on future Fed rate cuts. Gold +0.2%, Silver +0.7%.

ENERGY:

Oil prices inched lower amid OPEC+ dispute on output quotas, leading to a delayed meeting now scheduled online for Nov. 30. The disagreement, centered on African

quotas, adds uncertainty to the group’s production policy for the coming year. Crude faces back-to-back monthly losses, down 16% from late September highs, influenced by increased supplies, rising US stockpiles, and geopolitical factors. The market awaits

the OPEC+ meeting’s outcome for clarity on future oil dynamics.WTI -0.8%, Brent +0.1%.

CURRENCIES:

In currency markets, the US dollar inched lower and is set for a second consecutive weekly decline ahead of US PMI data, with front-end volatility supported, focusing

on next week’s inflation reports.USD/JPY initially declined but recovered, influenced by Japan’s inflation acceleration. EUR/NOK edged higher amid expectations of a rate hike by Norges Bank. ECB’s Holzmann mentions equal probability of a rate hike or cut in

Q2 2024. Germany’s IFO business confidence index falls short of expectations. GBP/USD rose on positive UK consumer confidence data, and AUD/USD increased with exporters buying spot from local banks. US$ Index -0.2%, GBPUSD +0.3%, USDJPY +0.1%, EURUSD +0.1%,

AUDUSD +0.2%, USDNOK +0.2%.

Colors within the report:

Green is always the 200 period (day, week).

Red is always 21,

Blue = 50,

Brown =

100 *Stars have added importance

Data sources: Bloomberg, Reuters, CQG

No responses yet