TODAY’S GAME PLAN: from

the trading desk, this is not research

DATA/HEADLINES ET : 10:00am

Conf. Board Consumer Confidence,

Conf. Board Expectations,

Richmond Fed Manufact. Index,

Fed’s Goolsbee and Waller speaks, 10:30am Dallas Fed Services Activity,

10:45 a.m.: Fed’s Bowman speaks,

3:30 pm.: Fed’s Barr speaks.

TODAY’S HIGHLIGHTS:

- The Carolina Panthers fired the head coach, Frank Reich, on Monday after a 1-10 start to the 2023

season. - The UK has detected its first human case of a new type of swine flu, influenza A(H1N2)v.

- Suspect pleads not guilty after three men of Palestinian descent shot in Vermont.

World stocks were broadly lower and showed uncertainty as treasuries stabilized following a previous rally. Investors await a series

of speeches by Federal Reserve officials on Tuesday and key economic data later this week. Citi’s Chris Montagu noted a slightly bearish net positioning in S&P 500 futures. Israeli forces and Hamas fighters are observed to be adhering to a truce for the fifth

morning on Tuesday. The ceasefire was extended at the last minute for at least two more days. Elsewhere, preliminary estimates from Adobe Digital Insights indicated that spending online on Monday was on track to reach a record $12.4 billion. Oil prices increased,

gold saw a slight uptick, and the dollar slightly declined.

EQUITIES:

US equities were slightly lower and set for a quiet opening. Investors are questioning if the significant November market gains were

excessive, with Citigroup Inc. strategists noting that net positioning in the S&P 500 is currently appearing “slightly bearish.” Affirm (AFRM US) shares rose 3.1% following an upgrade by Jefferies to hold from underperform, citing stabilizing credit performance

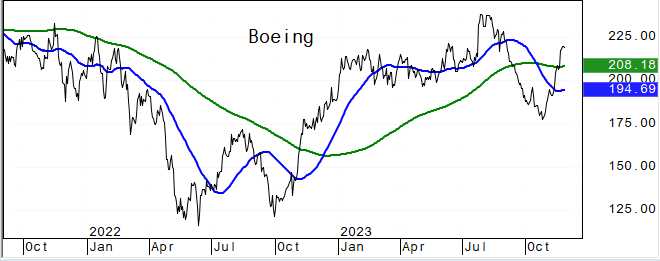

and ongoing momentum in buy-now-pay-later services. Boeing (BA US) gained 2.1% as RBC Capital Markets upgraded the stock to outperform, noting a significant shift in sentiment amid strong demand. Cool Co. (CLCO US) dropped 9.1% after Pareto described the liquefied

natural gas shipping company’s results as soft. Avidity Biosciences (RNA) rises 35% as the firm expands its cardiovascular collaboration with Bristol Myers Squibb. Other notable premarket movers: Block (SQ US) +1.1%, Coinbase (COIN US) +0.7%, Newmont Corp

(NEM US) +0.6%, Palo Alto Networks (PANW US) -1.1%, Edwards Life (EW US) -2.9%, Zscaler (ZS US) -6.5%.

Futures ahead of the bell: E-Mini S&P -0.2%, Nasdaq -0.2%, Russell 2000 -0.3%, Dow -0.1%.

European shares retreated, extending a pause in their November rally, as investors await inflation data later in the week for insights into future monetary policy. The Stoxx

Europe 600 Index edged lower with consumer and health care stocks facing the most significant decline. Argenx SE plunged 17% after its only medicine failed to meet the primary endpoint in a study. Despite the two-day retreat, European stocks are on track for

their best monthly return since January. The focus shifts to US and euro zone inflation readings later in the week, expected to show the smallest annual increases since early or mid-2021, supporting the sentiment that interest rates have peaked. In the UK,

Prime Minister Rishi Sunak’s commitment to economic revival may benefit domestic-oriented shares, with the FTSE 250 surging 10% since October 26. The market expects some short-term consolidation, but overall sentiment remains constructive on European equities

in the medium term. Stoxx 600 -0.6%, DAX -0.1%, CAC -0.6%, FTSE 100 -0.4%.

Asian stocks rose, led by South Korean and Taiwanese markets, buoyed by lower Treasury yields ahead of a crucial US inflation report. The MSCI Asia Pacific Index increased by

0.5%, driven by gains in tech giants like TSMC and Samsung Electronics. Japanese stocks fell as the yen strengthened, while Hong Kong saw declines and mainland China shares posted modest gains. Chipmaker stocks gained further on reports of Chinese President

Xi Jinping’s planned visit to local tech firms. Adani Group companies surged after India’s Supreme Court concluded hearings related to a stock plunge investigation. Meanwhile, BYD declined after UOB Kay Hian downgrades its rating to sell, citing concerns like

peaking retail sales volume, inventory buildup, decreasing capacity utilization, and price-cut pressures. China Education Group shares plummet up to 21% in Hong Kong, marking the most significant drop in 22 months, following a profit decline announcement.

Singapore -0.5%, Topix -0.2%, Vietnam +0.6%, Sensex +0.3%, Kospi +1%, ASX 200 +0.4%, Taiwan +1.2%, Thailand +0.5%, Indonesia +0.6%, CSI 300 +0.2%.

FIXED INCOME:

Treasuries saw a slight increase in yields, ranging from 1 to 3 basis points, reversing some of the gains from the previous day. Italian bonds underperformed

core euro-zone bonds following comments from the ECB’s Nagel about the need for a significant reduction in the central bank’s balance sheet. US 10-year yields were approximately 2 basis points lower on the day at 4.41%, with the auction cycle concluding with

a $39 billion 7-year note sale. The auction’s (WI) yield was around 4.5%, indicating an improvement compared to the previous auction in October. The US session includes a 7-year note auction, various economic data releases such as house-price indices and consumer

confidence, and several scheduled speeches from Federal Reserve officials, including Goolsbee, Waller, Bowman, and Barr.

METALS:

Gold steadied near its highest level since May, with the recent advance fueled by a slump in Treasury yields as traders loaded up on bets that the Federal

Reserve will start cutting interest rates next year. Gold +0.1%, Silver +0.1%.

ENERGY:

Oil prices edged higher amid speculation about potential deeper output cuts from OPEC+. Brent crude hovered around $81 per barrel, rebounding

from recent losses. Saudi Arabia, OPEC+’s de-facto leader, urged members to reduce production quotas, but resistance exists among some members. Hedge funds have become less bullish on crude, evident in reduced net-long positions and bearish signals in options

and timespreads. WTI +0.9%, Brent +0.9%

CURRENCIES:

In currency markets, the Dollar Index remained relatively unchanged. In November, hedge funds increased bullish bets on the dollar despite its overall

decline. However, sentiment varies across currency pairs, with a notable shift against the pound and Australian dollar contributing to the rise in net long positions. The yen initially gained in the Asia session but lost traction due to month-end re-balancing.

GBP/USD was flat, supported by corporate demand. AUD/USD pared some gains but remained higher after comments by Reserve Bank of Australia’s Michele Bullock about stickier-than-forecast inflation. US$ Index +0.06%, GBPUSD flat, USDJPY +0.2%, EURUSD flat, AUDUSD

+0.1%, USDNOK -0.4%.

Bitcoin edged higher, anticipation of an eventual US spot Bitcoin exchange-traded fund has helped to spur inflows into digital-asset

investment products for a ninth consecutive week. Bitcoin +0.4%, Ethereum +0.4%.

TECHNICAL LEVELS:

|

ESZ23 |

10 Year Yield |

Dec Gold |

Jan WTI |

Spot $ Index |

|

|

Resistance |

4652.00 |

5.500% |

2100.0 |

86.29 |

107.990 |

|

|

4624.00 |

5.325% |

2085.4 |

84.57 |

107.350 |

|

|

4611.00 |

5.000% |

2056.0 |

80.90 |

106.450 |

|

|

4597.50 |

4.775% |

2029.4 |

80.10 |

105.800 |

|

|

4571.00 |

4.620% |

2019.7 |

78.18 |

104.750 |

|

Settlement |

4561.00 |

2012.4 |

74.86 |

||

|

|

4540/41 |

4.350% |

1981.5 |

72.16 |

103.620 |

|

|

4518.00 |

3.990% |

1963.9 |

70.16w |

102.550 |

|

|

4500.00 |

3.640% |

1950.6 |

66.80 |

101.240 |

|

|

4470.00 |

3.245% |

1944.0 |

65.00 |

100.000 |

|

Support |

4439.00 |

3.000% |

1921.5 |

62.55 |

99.580 |

Colors within the report:

Green is always the

200 period (day, week). Red is always 21,

Blue = 50,

Brown =

100 *Stars have added importance

- Upgrades

- Affirm

Holdings (AFRM) Raised to Hold at Jefferies; PT $30 - Boeing (BA)

Raised to Outperform at RBC; PT $275 - Crocs (CROX)

Raised to Strong Buy at Raymond James; PT $115 - NLight (LASR)

Raised to Speculative Buy at Benchmark; PT $17 - RLJ

Lodging (RLJ) Raised to Outperform at Oppenheimer;

PT $13 - Downgrades

- Asur (ASURB

MM) ADRs Cut to Sell at Citi; PT $222 - Booz

Allen (BAH) Cut to Equal-Weight at Wells Fargo; PT

$138 - Edwards

Life (EW) Cut to Underperform at Wolfe; PT $57 - Freeline

Therapeutics (FRLN) ADRs Cut to Neutral at HC Wainwright - MEG

Energy (MEG CN) Cut to Sector Perform at Scotiabank;

PT C$27 - Morgan

Stanley (MS) Cut to Hold at SocGen; PT $80 - Shopify (SHOP

CN) Cut to Underweight at Piper Sandler - Welltower (WELL)

Cut to Sector Perform at RBC; PT $97 - Initiations

- CCL

Industries (CCL/B CN) Reinstated Sector Outperform

at Scotiabank - Chipotle (CMG)

Reinstated Buy at William O’Neil - Confluent (CFLT)

Rated New Outperform at Bernstein; PT $34 - Estee

Lauder (EL) Rated New Buy at HSBC; PT $180 - First

Citizens (FCNCA) Rated New Market Perform at Raymond

James - Glaukos (GKOS)

Rated New Buy at Truist Secs; PT $88 - Gracell

Biotech (GRCL) US Rated New Outperform at Evercore

ISI(Earlier) - Hannon

Armstrong (HASI) Rated New Neutral at Goldman; PT

$26 - LendingClub (LC)

Rated New Overweight at Piper Sandler; PT $8 - Lexeo

Therapeutics (LXEO) Rated New Buy at Chardan Capital

Markets - Rated

New Outperform at Leerink; PT $19 - Rated

New Overweight at JPMorgan; PT $20 - Rated

New Outperform at RBC; PT $22 - Rated

New Buy at Stifel; PT $20 - Mach

Natural Resources (MNR) Rated New Buy at Johnson Rice;

PT $27 - Profound

Medical (PRN CN) Rated New Hold at Stifel; PT $11 - SharkNinja (SN)

Rated New Buy at Canaccord; PT $61 - TScan

Therapeutics (TCRX) Rated New Outperform at LifeSci

Capital

Data sources: Bloomberg, Reuters, CQG

No responses yet