TODAY’S GAME PLAN: from the trading

desk, this is not research

DATA/HEADLINES 8:30ET Employment Report*; 10:00ET U of Mich Sentiment

TODAY’S HIGHLIGHTS:

- Hunter Biden was indicted on nine federal tax charges from 2016 through 2019

- A Ron DeSantis event organized by super PAC Never Back Down was canceled this week due to a lack of interest

- Jon Rahm joins LIV Golf League

Global stocks edged higher after China vowed to strengthen the government’s fiscal policy to boost domestic demand. China’s Politburo said the country will spur domestic

demand and consolidate and enhance the economic recovery in 2024. Focus will be on the US jobs report that will be closely watched for clues on next week’s Federal Reserve policy meeting. Both the Fed and the European Central Bank will deliver rate decisions

next week. Meanwhile, the Palestinian Authority is working with US officials on a postwar plan for Gaza.

EQUITIES:

US equity futures are mixed to lower as investors awaited a pivotal US jobs report for more evidence of whether the labor market is cooling fast enough for the Federal

Reserve to cut interest rates. Non-farm payrolls figures are expected to show employers added 180,000 jobs last month. In corporate news, Honeywell agreed to acquire Carrier’s security business for about $5 billion, the WSJ reported. Lululemon fell post-market

after giving fourth-quarter revenue guidance that trailed estimates.

Futures ahead of the bell: E-Mini S&P -0.2%, Nasdaq -0.4%, Russell 2000 +0.2%, Dow -0.2%.

In pre-market trading, DocuSign (DOCU) falls as much as 3% after the e-signature company gave a margin outlook that was seen as cautious, considering its strong third-quarter results.

Bluebird Bio (BLUE) shares rise as much as 4.2% after Morgan Stanley upgrades the gene-therapy firm to equal-weight from underweight ahead of the likely approval of its Lovo-cel therapy to treat sickle cell disease. Eneti Inc. (NETI) gains 9.5% after Cadeler

A/S extended the expiration date for its share exchange offer to acquire all the outstanding shares. Hello Group ADRs (MOMO) are up 8.8%, after the China-based social networking platform reported third-quarter results that beat expectations. Lululemon (LULU)

drops 2.7% after the activewear company’s fourth-quarter revenue guidance failed to meet consensus expectations. Smartsheet (SMAR) shares are up 3.8%, after the software company reported third-quarter results that beat expectations and raised its full-year

forecast.

European shares advanced, set for a fourth straight week of gains, as risk appetite remained high following a sharp slowdown in inflation in the bloc. The Stoxx Europe 600 Index is marginally

higher, with luxury and travel stocks leading gains after China vowed to strengthen the government’s fiscal policy to boost domestic demand. Vivendi SE advanced after Paris bourse operator Euronext said the French media conglomerate will be added to the CAC

40 Index. In London, supermarket shares were racing higher, with Sainsbury up 3%, its highest level in more than two years, after an upgrade from Goldman Sachs, and Ocado rose over 4%. Broader exposure beyond tech and depressed valuations have supported European

stocks, along with optimism over easing monetary policy. Stoxx 6– +0.35%, DAX +0.3%, CAC +0.7%, FTSE 100 +0.1%. Travel +1%, Technology +0.7%, Energy +0.7%, Autos +0.5%. Basic Resources -1.5%, REITs -0.1%.

Asian equities were mixed as sharp losses in Japan tempered gains in technology stocks. The MSCI Asia Pacific Index fell 0.2%, with Toyota Motor, Tencent and Shi-Etsu Chemical the biggest

drags on the index. Meanwhile, stocks closed higher in tech-heavy Korea and Taiwan. Japanese shares slid after the yen surged by the most against the dollar in almost a year on bets the Bank of Japan will end negative interest rates as early as this month.

Japan’s economy shrank an annualized 2.9% last quarter, worse than the estimate for a 2% contraction. The RBI kept its key rate at 6.5% for a fifth time and signaled it’s nowhere close to cutting rates as India’s economy grows faster than expected. China CPI

data is due to be reported over the weekend. Kospi +1%, Taiwan +0.6%, Sensex +0.4%, ASX 200 +0.3%, Vietnam +0.25%, CSI 300 +0.25%. Hang Seng Index -0.1%, Nikkei 225 -1.7%.

FIXED INCOME:

Treasuries wavered ahead of the US job report with traders seeking justification of the recent record-breaking bond market rally driven by expectations for a succession

of rate cuts next year. Fund managers pulled $4.8 billion from Treasuries, the biggest weekly outflow since August 2022, in the run-up to the labor market report, according to EPFR Global data. Treasuries slightly cheaper across the curve amid bigger losses

in core European rates. US 10-year yield rises 3bps to 4.18%, 2 year yield ~4.62% and curves flatten slightly.

METALS:

Gold traded in a tight range overnight, with focus on the upcoming US jobs data. A stronger dollar has been keeping gold on a path for its first weekly drop in four

weeks. Traders are keen to understand how the Federal Reserve will adjust its monetary policy in the next meeting, with today’s job data as one of the main indicators. Spot gold -0.05%, silver -0.2%.

ENERGY:

Crude oil prices rose after Saudi Arabia and Russia called for more OPEC+ members to join output cuts. Oil benchmarks are still headed for a seventh straight weekly

decline after sliding to their lowest levels since June yesterday. Brent and WTI crude futures are on track to fall roughly 4% for the week and remain on course for the longest weekly losing streak since 2018 on concerns about a global glut. WTI +1.8%, Brent

+1.8%, US Nat Gas +0.3%, RBOB +2.4%.

CURRENCIES:

In currency trading, the dollar was mixed against major peers. The yen erased an advance that brought it to its strongest level since August amid speculation the

Bank of Japan will start lifting its sub-zero benchmark rate soon. USDJPY held its key 200 day moving average on the move after falling nearly 4% yesterday. The outsized move Thursday may have been amplified by speculators closing bearish wagers on the yen,

after leveraged funds boosted these to the highest level in more than a year last week. US$ Index +0.2%, USDJPY +0.1%, GBPUSD -0.1%, EURUSD -0.1%, AUDUSD +0.1%, NZDUSD -0.3%, USDSEK +0.4%.

Bitcoin +0.6%, Ethereum -0.2%. Global investment manager VanEck predicts Bitcoin will hit an all-time high in November next year. VanEck analysts predict an inflow

of over $2.4 billion in newly approved US Spot Bitcoin ETFs in Q1 2024.

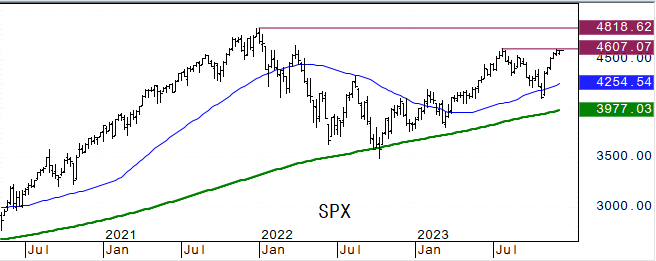

TECHNICAL LEVELS:

|

ESZ23 |

10 Year Yield |

Feb Gold |

Jan WTI |

Spot $ Index |

|

|

Resistance |

4680.00 |

5.500% |

2180.0 |

81.00 |

107.350 |

|

|

4652.00 |

5.325% |

2150.0 |

79.00 |

106.300 |

|

|

4634.00 |

5.000% |

2135.0 |

78.02 |

105.500 |

|

|

4608.00 |

4.725% |

2100.5 |

76.75 |

104.350 |

|

|

4598.50 |

4.585% |

2075.0 |

72.15 |

103.560 |

|

Settlement |

4589.50 |

2036.6 |

69.34 |

||

|

|

4567.00 |

4.020% |

2026.7 |

68.80 |

102.540* |

|

|

4545.00 |

3.640% |

1991.5 |

66.80 |

101.240 |

|

|

4502.00 |

3.245% |

1968.5 |

63.64 |

100.000 |

|

|

4480.00 |

3.000% |

1960.9 |

62.00 |

99.580 |

|

Support |

4439.00 |

|

1949.0 |

60.00 |

99.000 |

Colors within the report:

Green is always the 200 period (day, week).

Red is always 21,

Blue = 50,

Brown =

100 *Stars have added importance

- Upgrades

- ALX Oncology (ALXO) Raised to Buy at Jefferies; PT $18

- American Woodmark (AMWD) Raised to Hold at Deutsche Bank

- Bluebird Bio (BLUE) Raised to Equal-Weight at Morgan Stanley; PT $7

- Broadcom (AVGO) Raised to Buy at Summit Insights

- Cushman & Wakefield (CWK) Raised to Outperform at Wolfe; PT $12

- Equifax (EFX) Raised to Buy at Deutsche Bank

- First Solar (FSLR) Raised to Overweight at Morgan Stanley; PT $237

- Imperial Oil (IMO CN) Raised to Neutral at JPMorgan; PT C$97

- NOV Inc (NOV) Raised to Overweight at JPMorgan; PT $25

- NVR (NVR) Raised to Hold at Deutsche Bank

- Owens Corning (OC) Raised to Buy at Deutsche Bank

- Qorvo (QRVO) Raised to Overweight at Morgan Stanley; PT $134

- Riot Platforms Inc (RIOT) Raised to Neutral at JPMorgan; PT $12

- Semtech (SMTC) Raised to Buy at CFRA; PT $25

- SLM (SLM) Raised to Overweight at Wells Fargo; PT $20

- Taylor Morrison (TMHC) Raised to Buy at Deutsche Bank

- Watsco (WSO) Raised to Buy at Deutsche Bank

- Downgrades

- Adecoagro (AGRO) Cut to Underweight at JPMorgan; PT $10.50

- Airbnb (ABNB) Cut to Hold at DBS Bank; PT $145

- Apple Hospitality (APLE) Cut to Equal-Weight at Wells Fargo; PT $17

- AZEK (AZEK) Cut to Hold at Deutsche Bank

- Beam Therapeutics (BEAM) Cut to Hold at Jefferies; PT $30

- Casey’s (CASY) Cut to Market Perform at BMO; PT $290

- Cerevel Therapeutics (CERE) Cut to Market Perform at Cowen; PT $45

- Cintas (CTAS) Cut to Hold at Deutsche Bank

- CleanSpark (CLSK) Cut to Neutral at JPMorgan; PT $8

- Deckers Outdoor (DECK) Cut to Neutral at Citi; PT $710

- DiamondRock Hospitality (DRH) Cut to Equal-Weight at Wells Fargo

- FactSet (FDS) Cut to Hold at Deutsche Bank

- HashiCorp (HCP) Cut to Market Perform at Cowen; PT $23

- KB Home (KBH) Cut to Sell at Deutsche Bank

- Lam Research (LRCX) Cut to Equal-Weight at Morgan Stanley

- Laurentian Bank of Canada (LB CN) Cut to Hold at TD; PT C$26

- MBIA (MBI) Cut to Neutral at Roth MKM; PT $15

- MEG Energy (MEG CN) Cut to Neutral at JPMorgan; PT C$33

- Pool Corp (POOL) Cut to Hold at Deutsche Bank

- Qualcomm (QCOM) Cut to Equal-Weight at Morgan Stanley; PT $132

- Sherwin-Williams (SHW) Cut to Hold at CFRA; PT $287

- SiteOne Landscape (SITE) Cut to Sell at Deutsche Bank

- Sunstone Hotel (SHO) Cut to Underweight at Wells Fargo; PT $9.50

- Verisk (VRSK) Cut to Hold at Deutsche Bank

- Initiations

- Aerovate Therapeutics (AVTE) Rated New Overweight at Wells Fargo

- Alcoa (AA) Rated New Hold at HSBC; PT $29

- Allogene (ALLO) Rated New Buy at Citi; PT $7

- Alnylam (ALNY) Rated New Equal-Weight at Wells Fargo; PT $171

- BellRing Brands (BRBR) Reinstated Neutral at DA Davidson; PT $60

- Biohaven (BHVN) Rated New Outperform at Baird; PT $58.11

- Bowman Consulting Group (BWMN) Rated New Buy at Roth MKM; PT $45

- Bridgebio (BBIO) Rated New Overweight at Wells Fargo; PT $58

- CB Financial Services (CBFV) Rated New Neutral at Janney Montgomery

- Celcuity (CELC) Rated New Buy at HC Wainwright; PT $27

- Clean Harbors (CLH) Rated New Overweight at Wells Fargo; PT $190

- Cogent Biosciences Inc (COGT) Rated New Overweight at JPMorgan; PT $18

- CVB Financial (CVBF) Rated New Equal-Weight at Stephens; PT $21

- East West Bancorp (EWBC) Rated New Overweight at Stephens; PT $79

- Endava (DAVA) ADRs Rated New Neutral at JPMorgan; PT $77

- Eventbrite (EB) Rated New Buy at B Riley; PT $13

- Freshpet (FRPT) Rated New Buy at DA Davidson; PT $104

- Frontier Lithium (FL CN) Rated New Market Perform at BMO

- Gaming and Leisure (GLPI) Reinstated Neutral at Goldman; PT $51

- Hershey (HSY) Rated New Neutral at DA Davidson; PT $205

- Hubbell (HUBB) Rated New Outperform at Cowen; PT $338

- Insmed (INSM) Rated New Overweight at Wells Fargo; PT $55

- Keros Therapeutics (KROS) Rated New Overweight at Wells Fargo; PT $60

- Klaviyo (KVYO) Rated New Buy at Loop Capital; PT $40

- Lancaster Colony (LANC) Rated New Neutral at DA Davidson; PT $185

- Lithium Ionic (LTH CN) Rated New Outperform at BMO; PT C$5

- Mondelez (MDLZ) Rated New Buy at DA Davidson; PT $83

- MoonLake Immunotherapeutics (MLTX) Rated New Buy at Citi; PT $72

- Morphic (MORF) Rated New Buy at Citi; PT $46

- Nanobiotix SA (NANO FP) ADRs Rated New Outperform at Leerink; PT $11

- Nexstar Media (NXST) Rated New Neutral at Citi; PT $158

- NextEra Energy (NEE) Reinstated Buy at Citi; PT $69

- Patriot Battery Metals I (PMET CN) Rated New Outperform at BMO; PT C$16

- Pliant Therapeutics (PLRX) Rated New Overweight at Wells Fargo; PT $41

- Prime Medicine (PRME) Rated New Neutral at Citi; PT $10

- PTC Therapeutics (PTCT) Rated New Overweight at Wells Fargo; PT $37

- Quantum-Si (QSI) Rated New Buy at HC Wainwright; PT $3

- Redfin (RDFN) Rated New Neutral at B Riley; PT $8

- Simply Good Foods (SMPL) Rated New Neutral at DA Davidson; PT $42

- Solid Biosciences (SLDB) Rated New Buy at HC Wainwright; PT $9

- Southern California (BCAL) Rated New Equal-Weight at Stephens; PT $17

- Southern Co (SO) Reinstated Buy at Citi; PT $82

- Stericycle (SRCL) Rated New Underweight at Wells Fargo; PT $40

- SunOpta (SOY CN) Rated New Buy at DA Davidson; PT C$10.87

- Tango Therapeutics (TNGX) Rated New Buy at B Riley; PT $16

- Ultragenyx (RARE) Rated New Overweight at Wells Fargo; PT $72

- United Therapeutics (UTHR) Rated New Overweight at Wells Fargo; PT $309

- VICI Properties (VICI) Reinstated Buy at Goldman; PT $36

- Vital Farms (VITL) Reinstated Buy at DA Davidson; PT $21

- WaFd Inc (WAFD) Reinstated Equal-Weight at Stephens; PT $32

- Xenon Pharmaceuticals (XENE) Rated New Outperform at Baird; PT $63

Data sources: Bloomberg, Reuters, CQG

No responses yet