TODAY’S GAME PLAN: from the trading

desk, this is not research

DATA/HEADLINES 8:30ET CPI*; 1:00ET 30 Year Bond Auction

TODAY’S HIGHLIGHTS:

- Harvard President Claudine Gay will stay in office after receiving backing from the university’s governing

board - Small business optimism index ticked lower again

- Japan’s oldest person dies at 116

Global stocks rose ahead of the Federal Reserve’s final scheduled policy decision for 2023 on Wednesday along with those of the European Central Bank, Bank of England,

Norges Bank and the Swiss National Bank on Thursday. The MSCI All-World index, which is trading around four-month highs, rose 0.2%. Focus today will be on the US consumer price figures which are expected to show inflation still cooling, but staying well above

the Fed’s 2% annual target, with core CPI expected to come in at 4%.

EQUITIES:

Nasdaq announced annual changes to the Nasdaq-100 Index: Adding CDW, DASH, SPLK, MDB, CCEP, ROP; effective Dec 18th- Removing: ALGN, EBAY, JD, ENPH, ZM, LCID.

US equity futures nudged higher ahead of a crucial US inflation print which could provide clues for the final Federal Reserve decision of the year. The US Federal

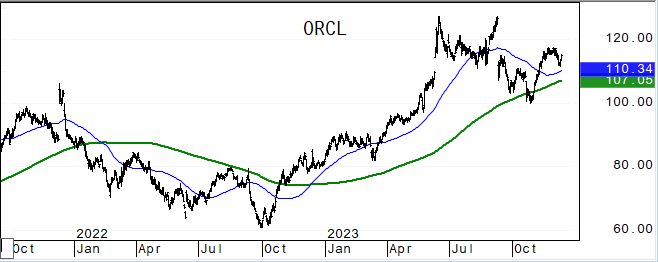

Reserve is widely expected to hold rates on Wednesday, with most market focus on whether it will try to temper policy easing expectations after investors’ aggressive dovish repricing. Oracle Corp. fell as much as 9.7% in post-market trading after the software

company’s second-quarter revenue disappointed amid slowing cloud sales momentum. Google lost an antitrust battle with Epic Games. The ruling threatens to upend the mobile app economy and could cost the technology giant billions of dollars in revenue.

Futures ahead of the bell: E-Mini S&P +0.1%, Nasdaq +0.25%, Russell 2000 +0.3%, Dow +0.2%.

In pre-market trading, Alphabet (GOOGL) falls as much as 1.3% as Google lost an antitrust court fight to Fortnite maker Epic Games. 4 Therapeutics (CCCC) surges 38% after signing a license

and collaboration agreement with Merck to develop degrader-antibody conjugates to treat cancer. Gaotu Techedu ADRs (GOTU) soar as much as 8.5%, extending Monday’s gains, after the education firm’s livestream shopping channel gains steam on China’s short-form

video platform Douyin. Illumina (ILMN) drops 2% as BofA downgrades the DNA-sequencing company to underperform from neutral. Macy’s (M) slips 3% after Citi downgraded the department-store operator to sell from neutral, expressing skepticism that a buyout offer

from Arkhouse Management and Brigade Capital Management will actually materialize. Seagen (SGEN) gains 3.3% after Pfizer says it has received all required regulatory approvals to close its acquisition of the biotech firm on Dec. 14. Wyndham (WH) shares rise

about 2.8% after Choice Hotels starts an exchange offer to buy Wyndham.

European gauges fluctuated with France’s CAC 40 Index eyeballing a record high. Consumer products stocks and retailers gained the most in the region, while telecoms lagged. UK wage growth

slowed at the sharpest pace in nearly two years, a fresh sign the economy is cooling. German ZEW investor outlook unexpectedly rose to 12.8 for December from 9.8 in November. AstraZeneca rose after agreeing to buy vaccine developer Icosavax. Hargreaves Lansdown

and other UK wealth managers slid after the Financial Conduct Authority wrote to investment platforms regarding concerns about interest earned on customers’ cash balances. Stoxx 600 -0.05%, DAX is flat, CAC +0.2%, FTSE 100 +0.35%. Media +0.6%, Technology +0.3%.

Telecom -0.6%, Energy -0.5%.

Asian stocks mostly advanced, driven by a recovery in Hong Kong shares as traders hope a meeting of key Chinese economic policymakers will result in additional stimulus measures to boost

the economy. The MSCI Asia Pacific Index climbed 0.5%, with Alibaba, Tencent and TSM providing the biggest boosts. AI-linked stocks helped boost Korea and Taiwan indexes. Thailand’s stock benchmark entered a bear market, falling over 20% from its 2022 high,

as the ongoing selloff by foreign investors and slower economic growth weighed on sentiment. Japanese PPI slowed to 0.3% in November, the weakest in almost three years. Hang Seng Index +1.1%, Philippines +1%, Indonesia +0.5%, ASX 200 +0.5%, Kospi +0.4%, Singapore

+0.4%, CSI 300 0.2%, Vietnam +0.2%, Taiwan +0.2%, Nikkei 225 +0.2%. Topix -0.2%, Thailand -0.5%, Sensex -0.5%.

FIXED INCOME:

Treasuries gained ahead of November CPI data, which was probably flat again thanks to cheaper energy. The yield on 10-year Treasury notes fell 4.5 basis points to

~4.19% after lackluster three- and 10-year note auctions on Monday. In the twenty four 10 year Treasury auctions since the end of 2021, there have been 20 tails. Investors were reluctant to buy Treasuries in the auctions given thinner liquidity with the inflation

data and the Fed meeting looming. Treasuries are richer by 3bp to 5bp across the curve, paced by core European rates where front-end gilts soar as money markets price in additional BOE rate cuts after UK wage growth slowed. US session includes CPI data and

30-year bond reopening of November auction that tailed by more than 5bp.

METALS:

Gold edged higher after touching a three-week low in the previous session. The US consumer price index due this morning will be closely watched for a clearer sense

of whether the disinflation trend is continuing. The Fed is widely expected to hold rates after its meeting Wednesday. The market will be looking for signs of policymakers tempering expectations for easing after aggressive dovish bets led to wild fluctuations

in gold. Spot gold +0.3%, silver +0.6%.

ENERGY:

Oil pared gains to trade lower after an attack on a fuel tanker in the Red Sea by Houthi militants raised concerns around shipping and geopolitical risks. The tanker

was struck by a missile as it navigated the Red Sea, the latest in a string of incidents that have turned the area into the world’s riskiest waters. The COP28 climate talks in Dubai ran into overtime as negotiators worked on a new draft deal. Oil has dropped

for the past seven weeks, the longest losing run since 2018, on continuous pressure from robust supplies globally. WTI -0.6%, Brent -0.7%, US Nat Gas +0.7%, RBOB -0.3%.

CURRENCIES:

In currency markets, the dollar slipped ahead of US inflation figures that could set the tone for trading in a week filled with central bank meetings. Headline US

CPI number for November is forecast to decline to 3.1%, the lowest reading since the June print released in July, which coincided with this year’s low point for the dollar. The yen recovered some of the previous day’s losses, which were triggered by a Bloomberg

report that cited sources as saying Bank of Japan officials saw little need to exit their negative-rates policy. The BOJ meets next week. Short-term volatility in major currencies has risen to multi-month highs in anticipation of the December central bank

policy decisions. The pound fluctuated after data showed wage growth slowed at the sharpest pace in almost two years. US$ Index -0.35%, GBPUSD +0.1%, USDJPY -0.6%, EURUSD +0.3%, AUDUSD +0.3%, USDNOK -0.5%, USDCHF -0.5%.

Bitcoin +1.6%, Ethereum +0.4%. Bitcoin rose after posting its steepest drop in almost four months.

TECHNICAL LEVELS:

|

ESH23 |

10 Year Yield |

Feb Gold |

Jan WTI |

Spot $ Index |

|

|

Resistance |

4761.00 |

5.500% |

2118.0 |

81.00 |

|

|

|

4738.50 |

5.325% |

2098.0 |

79.00 |

107.350 |

|

|

4720.50 |

5.000% |

2052.0 |

78.02 |

106.300 |

|

|

4700.00 |

4.725% |

2027.0 |

76.75 |

105.100 |

|

|

4686.00 |

4.570% |

2006.8 |

72.15 |

104.350 |

|

Settlement |

4678.50 |

1993.7 |

71.32 |

||

|

|

4650.00 |

4.020% |

1986.5 |

68.80 |

103.560 |

|

|

4529.00 |

3.640% |

1973.9 |

66.80 |

102.540* |

|

|

4613.00 |

3.245% |

1962.5 |

63.64 |

101.240 |

|

|

4594.00 |

3.000% |

1935.6 |

62.00 |

100.000 |

|

Support |

4439.00 |

|

1900.0 |

60.00 |

99.580 |

Colors within the report:

Green is always the 200 period (day, week).

Red is always 21,

Blue = 50,

Brown =

100 *Stars have added importance

- Upgrades

- Albemarle (ALB) Raised to Neutral at BofA; PT $149

- Amalgamated Financial (AMAL) Raised to Overweight at JPMorgan; PT $29

- Amgen (AMGN) Raised to Outperform at RBC; PT $300

- BlackRock (BLK) Raised to Outperform at BNPP Exane; PT $885

- Boyd Group Services (BYD CN) Raised to Sector Outperform at Scotiabank

- Eagle Materials (EXP) Raised to Neutral at JPMorgan; PT $200

- EverQuote (EVER) Raised to Outperform at Raymond James; PT $13

- Extra Space (EXR) Raised to Overweight at Wells Fargo; PT $155

- Henry Schein (HSIC) Raised to Overweight at JPMorgan; PT $82

- HP Inc (HPQ) Raised to Overweight at Morgan Stanley; PT $35

- HubSpot (HUBS) Raised to Overweight at Piper Sandler; PT $610

- Itron (ITRI) Raised to Neutral at JPMorgan; PT $68

- Lundin Mining (LUN CN) Raised to Neutral at JPMorgan; PT C$8.90

- Manulife Financial (MFC CN) Raised to Outperform at RBC; PT C$34

- Martin Marietta (MLM) Raised to Overweight at JPMorgan; PT $530

- Nike (NKE) Raised to Buy at DZ Bank; PT $130

- PVH (PVH) Raised to Buy at Goldman; PT $126

- Ralph Lauren (RL) Raised to Neutral at Goldman; PT $132

- Sempra (SRE) Raised to Overweight at JPMorgan; PT $86

- Sonos (SONO) Raised to Overweight at Morgan Stanley; PT $20

- Sprouts Farmers (SFM) Raised to Buy at Goldman; PT $49

- Stelco Holdings (STLC CN) Raised to Overweight at JPMorgan; PT C$52

- Vulcan Materials (VMC) Raised to Overweight at JPMorgan; PT $245

- Zillow (ZG) Raised to Market Outperform at JMP; PT $60

- Zscaler (ZS) Raised to Outperform at Macquarie

- Downgrades

- AMC Networks (AMCX) Cut to Neutral at Seaport Global Securities

- Arthur J Gallagher (AJG) Cut to Market Perform at Raymond James

- Bluebird Bio (BLUE) Cut to Reduce at HSBC; PT $2.31

- CDW (CDW) Cut to Equal-Weight at Morgan Stanley; PT $216

- Comerica (CMA) Cut to Neutral at JPMorgan; PT $57

- Ecolab (ECL) Cut to Hold at CFRA; PT $193

- Emera (EMA CN) Cut to Underweight at JPMorgan; PT C$50

- Fortis (FTS CN) Cut to Underweight at JPMorgan; PT C$53

- Gol (GOLL4 BZ) ADRs Cut to Sell at Deutsche Bank; PT $3

- GoPro (GPRO) Cut to Underweight at Morgan Stanley; PT $3

- Grocery Outlet (GO) Cut to Sell at Goldman; PT $24

- Illumina (ILMN) Cut to Underperform at BofA; PT $100

- Lam Research (LRCX) Cut to Hold at Deutsche Bank; PT $725

- Macy’s (M) Cut to Sell at Citi; PT $14

- Progressive (PGR) Cut to Market Perform at Raymond James

- Public Storage (PSA) Cut to Equal-Weight at Wells Fargo; PT $280

- RingCentral (RNG) Cut to Hold at Jefferies; PT $35

- Shopify (SHOP CN) Cut to Sell at DZ Bank; PT C$88.25

- Tryp Therapeutics (TRYP CN) Cut to Neutral at Ladenburg Thalmann

- X4 Pharmaceuticals Inc (XFOR) Cut to Neutral at B Riley; PT $1

- Initiations

- Acadia Pharma (ACAD) Rated New Buy at Deutsche Bank; PT $25

- Acumen Pharma (ABOS) Rated New Buy at Deutsche Bank; PT $8

- Addus HomeCare (ADUS) Rated New Outperform at Cowen

- Alector (ALEC) Rated New Buy at Deutsche Bank; PT $12

- Alexander & Baldwin (ALEX) Rated New Buy at Janney Montgomery; PT $20

- Amylyx Pharmaceuticals (AMLX) Rated New Buy at Deutsche Bank; PT $36

- AZEK (AZEK) Rated New Outperform at Wolfe; PT $43

- Bausch + Lomb (BLCO CN) Bausch + Lomb Rated New Hold at Stifel; PT C$21.72

- Boeing (BA) Rated New Outperform at William Blair

- Camden Property (CPT) Rated New Equal-Weight at Morgan Stanley; PT $95

- Campbell Soup (CPB) Rated New Equal-Weight at Wells Fargo; PT $47

- Compass Pathways (CMPS) ADRs Rated New Buy at Deutsche Bank; PT $16

- Conagra (CAG) Rated New Equal-Weight at Wells Fargo; PT $31

- Electronic Arts (EA) Rated New Peerperform at Wolfe

- Enhabit (EHAB) Rated New Market Perform at Cowen; PT $12

- Freshpet (FRPT) Rated New Overweight at Wells Fargo; PT $90

- fuboTV (FUBO) Rated New Overweight at Cantor; PT $5

- Gannett Co (GCI) Rated New Buy at Compass Point; PT $5

- Heico (HEI) Rated New Outperform at William Blair

- Immunovant (IMVT) Rated New Buy at Deutsche Bank; PT $50

- J M Smucker (SJM) Rated New Overweight at Wells Fargo; PT $140

- Karuna Therapeutics (KRTX) Rated New Buy at Deutsche Bank; PT $227

- Kellanova (K) Rated New Equal-Weight at Wells Fargo; PT $56

- Lamb Weston (LW) Rated New Overweight at Wells Fargo; PT $120

- Mid-America (MAA) Rated New Equal-Weight at Morgan Stanley; PT $128

- Neumora Therapeutics (NMRA) Rated New Hold at Deutsche Bank; PT $13

- Neurocrine Bio (NBIX) Rated New Buy at Deutsche Bank; PT $136

- Post Holdings (POST) Rated New Equal-Weight at Wells Fargo; PT $92

- Prothena (PRTA) Rated New Buy at Deutsche Bank; PT $62

- Roivant Sciences (ROIV) Rated New Buy at Deutsche Bank; PT $14

- RxSight (RXST) Rated New Buy at Stifel; PT $40

- Sage Therapeutics (SAGE) Rated New Hold at Deutsche Bank; PT $21

- Sarepta (SRPT) Rated New Buy at Deutsche Bank; PT $109

- Skyward Specialty Insurance Group (SKWD) Rated New Buy at Jefferies

- Solo Brands (DTC) Rated New Neutral at B Riley; PT $5.50

- Take-Two (TTWO) Rated New Outperform at Wolfe

- Tapestry (TPR) Resumed Equal-Weight at Morgan Stanley; PT $38

- Traeger (COOK) Rated New Buy at B Riley; PT $3.50

- TransDigm (TDG) Rated New Outperform at William Blair

- Trex (TREX) Rated New Peerperform at Wolfe

- Tsakos Energy (TNP) Reinstated Buy at Fearnley; PT $40

- Urgent.ly (ULY) Rated New Buy at Needham; PT $7

Data sources: Bloomberg, Reuters, CQG

No responses yet