TODAY’S GAME PLAN: from the trading

desk, this is not research

DATA/HEADLINES 8:15ET ADP Employment Change; 8:30ET Advance Goods Trade Balance, Wholesale Inventories, Retail

Inventories, GDP Annualized QoQ, Personal Consumption, GDP Price Index; 10:00ET Pending Home Sales

ADP private payrolls 177K, Exp. 195K, Last 324K

TODAY’S HIGHLIGHTS:

- Russia will not probe Prigozhin plane crash under international rules (go figure)

- Researchers warn about synthetic opioids more powerful than fentanyl

- HURRICANE IDALIA MAKES LANDFALL IN FLORIDA, NHC SAYS

Global equities edged up as data suggested US inflation pressures were moderating but were on course to end August with their worst monthly performance of 2023. MSCI’s

global stock gauge has fallen more than 3% in August. China defended its business practices after US Commerce Secretary Gina Raimondo said American firms had told her it had become “uninvestable.” She insisted the US does not want to decouple from China.

The Chinese embassy said Beijing was working to further ease market access for foreign companies. Australian CPI growth slowed more than expected in July. In Japan, consumer confidence unexpectedly fell this month to 36.2, after consensus was for a gain.

EQUITIES:

US equity futures fluctuated following Tuesday’s rally, as investors await key inflation and labor market data points for clues on the Federal Reserve’s policy outlook. The ADP report

on private-sector employment is in focus today after signs of a slowdown in the labor market helped lift indices to gains on Tuesday. Also, a second reading on second-quarter growth could confirm those hopes for a “soft landing” for the US economy. Both releases

will set the stage for Thursday’s PCE inflation report and Friday’s August jobs report. Analysts were positive about Alphabet’s artificial intelligence updates at its Google Cloud Next event. The tech giant also announced a new AI infrastructure and software

as part of an expanded partnership with Nvidia

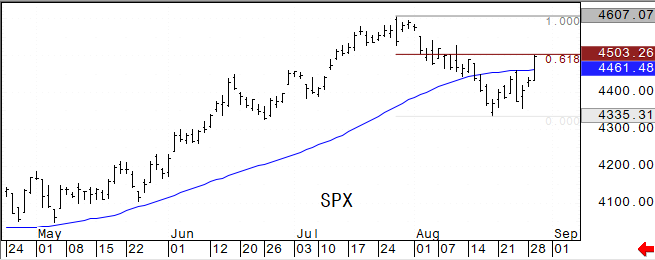

Futures ahead of the data: E-Mini S&P -0.04%, Nasdaq -0.05%, Russell 2000 -0.2%, Dow =0.05%. SPX has key Fibonacci resistance around the 4503 area (.618 retracement).

In premarket trading, HP (HPQ) falls 8% after the technology hardware company cut its full-year cash flow and profit outlook as the PC recovery takes longer than anticipated. Ambarella

(AMBA) drops 21% after its forecast for third-quarter revenue fell short of expectations, prompting a slew of price target cuts from analysts. Box (BOX) falls 9% after the infrastructure software company cut its full-year revenue forecast. Sunrun (RUN) rises

4% after Citi analyst Vikram Bagri raised the recommendation to buy from neutral on the residential solar energy company. Texas Instruments (TXN) shares are down 2.5% after Bernstein downgraded the chipmaker to underperform from market perform. Salesforce

(CRM) reports post-market, and investors expect new AI products and a recent price increase will boost revenue.

European stocks reversed early gains after the latest round of price data suggested inflation may not yet be fully on the retreat in the euro region. Reports showed inflation accelerated

in four of six German states in August. The eurozone’s economic sentiment indicator slipped to 93.3 in August, down from 94.5 in the prior month. In the UK, July mortgage approvals fell to the fewest since February, while home sales in Britain are on track

to hit a decade low this year. Utilities led the decline in the Stoxx Europe 600 as Orsted A/S plunged more than 20% after the Danish power generator forecast potential impairments of up to $2.3 billion relating to its US portfolio. Among other individual

movers, Prudential Plc climbed more than 4% after posting a rise in new business profit. Stoxx 600 -0.1%, DAX -0.3%, CAC -0.2%, FTSE 100 +0.4%. Basic Resources +0.8%, Media +0.5%, Banks +0.4%. Utilities -1.5%, Technology -0.6%.

Asian stocks climbed for a third day as data from the US to Australia weakened the case for higher interest rates, helping boost risk appetite. The MSCI Asia Pacific Index rose as much

as 1% before erasing more than half of its advance as China’s rally halted. A sub-gauge of financials weighed on the broader Chinese market on profit concerns. China asked Citic Trust and CCB Trust, two of the nation’s biggest financial firms, to examine the

books of shadow bank Zhongrong, potentially paving the way for a state-led rescue. Australia’s benchmark outperformed, climbing 1.2% as the country’s cooling inflation data bolstered the case for an interest-rate hold. Philippines +1.1%, Vietnam +0.7%, Taiwan

+0.6%, Topix +0.4%, Kospi +0.3%, Hang Seng Index was flat, CSI 300 -0.05%, Hang Seng Tech -0.9%.

FIXED INCOME:

Treasuries are under pressure as the US trading day begins, paced by bunds, where bear-flattening ensued after some German regional inflation gauges rose more than

forecast. Focal points of US session include August ADP employment change ahead of broader jobs report Friday. 10 year yield is +3bps at 4.15% with the 2s10s curve steeper by 4.5bps, following short-end-led declines of more than 10bp Tuesday. 2 year yield

~1.9%. Markets are pricing in an 87% chance of the Fed standing pat at its meeting next month, the CME FedWatch tool showed. BlackRock said US 10-year yields need to rise to about 4.5% before they offer value. State Street sees about a 75% chance the Fed

boosts rates in November but said that will be the end of its hiking cycle. Meanwhile, the Boston Fed warned that firms have yet to feel the full hit from tightening.

METALS:

Gold steadied after rising to the highest since early August on easing Fed rate hike bets.

Gold held gains as investors await US ADP Employment Change data for further action. The precious metal capitalized on softer job openings data, which accelerated hopes of an unchanged

interest rate decision to be taken at the September monetary policy meeting by the Federal Reserve. Spot gold +0.1%, silver -0.4%.

ENERGY:

Oil prices extended gains after industry data showed a large draw in crude inventories in the US, and as a hurricane in the Gulf of Mexico kept investors on edge.

Hurricane Idalia downgraded to an “extremely dangerous” Category 3 as it makes landfall this morning on Florida’s west coast, with winds as high as 130 mph. Chevron evacuated non-essential workers from its Blind Faith and Petronius platforms, and Tampa International

Airport was closed. US oil stockpiles slumped by 11.5 million barrels last week, the API said. That would cut total holdings to the lowest this year if confirmed by the EIA today.

Soldiers seized power in OPEC member Gabon, which could hit the country’s crude supplies and tighten the market further. The military takeover is the ninth in sub-Saharan

Africa since 2020. WTI +0.7%, Brent +0.5%, US Nat Gas +1.1%, RBOB +0.8%.

CURRENCIES:

In currency markets, the dollar is flat ahead of some key economic data. The euro erased early losses after Spanish and regional German CPI data. Spanish inflation

quickened again in August. The yen weakened 0.4% versus the dollar and remained at levels that led to intervention in the currency market last year by Japanese authorities. AUD/USD drops 0.5% before halving losses; Australia’s CPI rose 4.9% in July from a

year earlier, compared with economists’ estimate of 5.2%; the result was the third consecutive slowdown. US$ Index -0.05%, GBPUSD +0.1%, USDJPY +0.25%, AUDUSD -0.1%, EURUSD +0.02%.

Bitcoin %, Ethereum %. The crypto space traded lower after Bitcoin jumped more than 6% in the previous session as a US court ruling potentially paved the way for

the country’s first Bitcoin exchange-traded fund.

TECHNICAL LEVELS:

|

ESU23 |

10 Year Yield |

Dec Gold |

Oct WTI |

Spot $ Index |

|

|

Resistance |

4589.00 |

5.325% |

2029.0 |

89.20 |

107.180 |

|

|

4561.00 |

4.710% |

2004.0 |

87.50 |

106.000 |

|

|

4545.00 |

4.500% |

1985.0 |

84.89 |

105.380 |

|

|

4525.00 |

4.375% |

1974.0 |

82.97 |

104.700 |

|

|

4512.00 |

4.360% |

1969.0 |

82.05 |

104.450 |

|

Settlement |

4506.75 |

1965.1 |

81.16 |

||

|

|

4488.00 |

3.980% |

1940.5 |

76.75 |

103.100 |

|

|

4449/53 |

3.700% |

1919.5* |

76.30 |

102.600 |

|

|

4420.50 |

3.590% |

1907.0* |

74.27 |

102.000 |

|

|

4411.00 |

3.265% |

1866.0 |

71.75 |

101.440 |

|

Support |

4362.00 |

3.000% |

1842.0 |

68.20 |

100.620 |

Colors within the report:

Green is always the 200 period (day, week).

Red is always 21,

Blue = 50,

Brown =

100 *Stars have added importance

UPGRADES:

- Hercules Capital (HTGC) raised to buy at Compass Point; PT $17.50

- Sunrun (RUN) raised to buy at Citi; PT $21

DOWNGRADES:

- Abcam ADRs (ABCM) cut to market perform at SVB; PT $24

- Ambarella (AMBA) cut to market perform at Cowen; PT $65

- Bancolombia ADRs (BCOLO CB) cut to market perform at Itau BBA; PT $33

- Centene (CNC) cut to equal-weight at Morgan Stanley; PT $73

- GreenTree Hospitality ADRs (GHG) cut to underweight at Morgan Stanley

- Highwoods (HIW) cut to equal-weight at Wells Fargo; PT $22

- Peloton (PTON) cut to neutral at Macquarie; PT $7

- Rockwell Automation (ROK) cut to underweight at Barclays; PT $287

- Thorne HealthTech (THRN) cut to market perform at Cowen; PT $10.20

INITIATIONS:

- AZZ (AZZ) rated new buy at B Riley; PT $64

- Align Technology (ALGN) rated new buy at HSBC; PT $450

- BCB Bancorp (BCBP) rated new buy at Janney Montgomery; PT $18.50

- Cognex (CGNX) rated new neutral at Citi; PT $52

- Fluence Energy (FLNC) rated new overweight at Barclays; PT $31

- Gulfport Energy (GPOR) rated new outperform at Evercore ISI; PT $135

- Macatawa Bank (MCBC) rated new buy at Janney Montgomery; PT $11

- Stem Inc (STEM) rated new equal-weight at Barclays; PT $6

Data sources: Bloomberg, Reuters, CQG

No responses yet